1. What is the projected Compound Annual Growth Rate (CAGR) of the Biopolymer Packaging?

The projected CAGR is approximately 12.0%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Biopolymer Packaging

Biopolymer PackagingBiopolymer Packaging by Type (Polylactides (PLA), Bio-Polyethylene (PE), Bio-PolyethyleneTerephthalate(PET), Starch, Cellulose, Others), by Application (Cartons, Bags & Pouches, Bottles & Cans, Ampoules and Vials, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

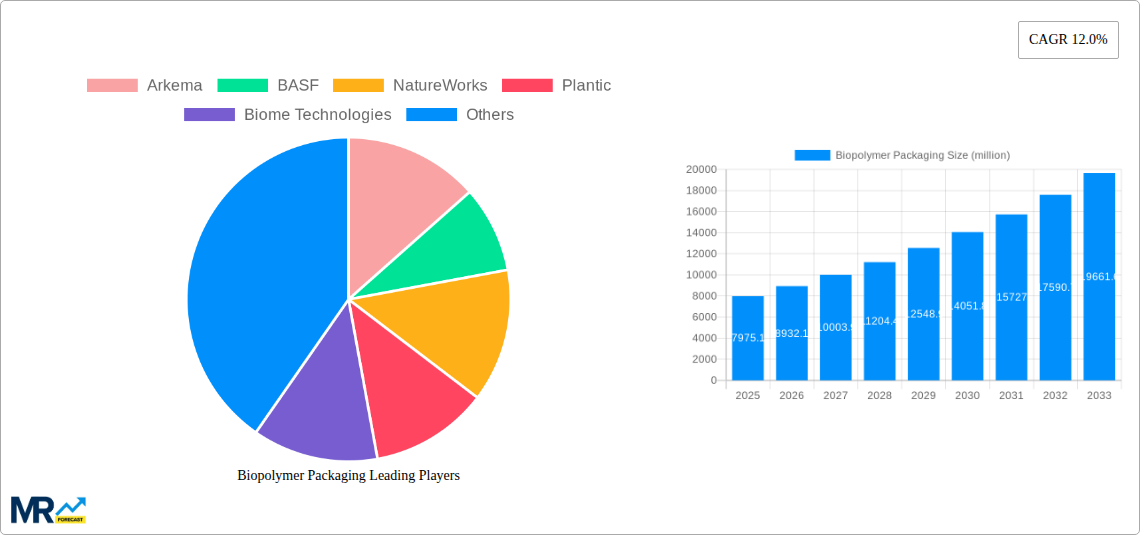

The global biopolymer packaging market is experiencing robust growth, projected to reach a significant $7975.1 million in 2025 with a remarkable Compound Annual Growth Rate (CAGR) of 12.0%. This expansion is fueled by a growing global consciousness around environmental sustainability and a strong consumer preference for eco-friendly alternatives to conventional plastics. Governments worldwide are also enacting stringent regulations to curb plastic waste, further accelerating the adoption of biopolymer packaging across various industries. Key drivers include advancements in biopolymer production technologies, leading to improved performance and cost-effectiveness, and the increasing availability of sustainable raw materials. The demand for biopolymer packaging is particularly strong in applications such as cartons, bags, pouches, bottles, and vials, where its biodegradability and compostability offer significant environmental benefits.

The biopolymer packaging market is characterized by a dynamic landscape of innovation and diversification. Polylactides (PLA) are leading the market due to their excellent properties and widespread applications. Bio-Polyethylene (PE), Bio-Polyethylene Terephthalate (PET), starch, and cellulose-based biopolymers are also gaining traction, each offering unique advantages for specific packaging needs. While the market presents immense opportunities, certain restraints, such as higher initial production costs compared to conventional plastics and challenges in large-scale manufacturing and infrastructure development for end-of-life management, need to be addressed. However, ongoing research and development, coupled with increasing investments from major players like Arkema, BASF, and NatureWorks, are poised to overcome these hurdles. The market is expected to witness significant growth across all major regions, with Asia Pacific, Europe, and North America leading the adoption due to supportive government policies and a concentrated presence of key industry players.

XXX The global biopolymer packaging market is experiencing a transformative surge, driven by an escalating demand for sustainable alternatives to traditional petroleum-based plastics. Over the Study Period: 2019-2033, this dynamic sector is projected to witness a compound annual growth rate (CAGR) that will reshape the packaging landscape. The Base Year: 2025 stands as a critical benchmark, with the Estimated Year: 2025 already revealing a substantial market valuation, poised for accelerated expansion throughout the Forecast Period: 2025-2033. The Historical Period: 2019-2024 laid the groundwork, showcasing initial adoption and innovation, but the coming years will be characterized by mainstream integration and significant market penetration. Key trends underscore this evolution, including the increasing consumer preference for eco-friendly products, which directly translates into higher demand for biodegradable and compostable packaging solutions. Regulatory bodies worldwide are also playing a pivotal role, implementing stringent policies to curb plastic waste and encourage the adoption of sustainable materials. This regulatory push is not only incentivizing manufacturers to invest in biopolymer research and development but also creating a more favorable market environment for their commercialization. Furthermore, advancements in material science are continuously expanding the functional properties of biopolymers, enabling them to compete with conventional plastics in terms of durability, barrier properties, and cost-effectiveness. This technological evolution is crucial for overcoming historical limitations and unlocking new application areas. The diversification of biopolymer types, from Polylactides (PLA) and Bio-Polyethylene (PE) to Bio-Polyethylene Terephthalate (PET), starch-based polymers, and cellulose derivatives, is offering a broader range of solutions for various packaging needs. Each type possesses unique characteristics, catering to specific industry requirements and sustainability goals. The integration of biopolymers across a wide spectrum of applications, including cartons, bags & pouches, bottles & cans, and ampoules & vials, signifies a significant shift towards a circular economy model. As the market matures, we anticipate a greater emphasis on end-of-life solutions, such as enhanced composting infrastructure and advanced recycling technologies for bioplastics, further solidifying their position as a viable and sustainable packaging paradigm for the future.

The biopolymer packaging market is being propelled by a confluence of powerful forces, fundamentally altering the global packaging industry's trajectory. Foremost among these drivers is the escalating global environmental consciousness. Consumers are increasingly aware of the detrimental impact of conventional plastic waste on ecosystems and are actively seeking out products with sustainable packaging. This consumer-led demand is exerting significant pressure on brands to adopt eco-friendly alternatives. Alongside this, a robust regulatory framework is emerging worldwide. Governments are implementing bans on single-use plastics, introducing extended producer responsibility (EPR) schemes, and offering incentives for the use of biodegradable and compostable materials. These policies are not merely restrictive but are actively fostering innovation and investment in the biopolymer sector. The inherent sustainability of biopolymers, derived from renewable resources like corn starch, sugarcane, and cellulose, offers a compelling alternative to fossil fuel-based plastics, reducing reliance on finite resources and lowering the carbon footprint associated with packaging production. Moreover, continuous advancements in research and development are enhancing the performance characteristics of biopolymers. Innovations are leading to improved strength, heat resistance, and barrier properties, making them suitable for a wider range of applications previously dominated by conventional plastics. This technological progress is crucial for expanding market adoption and ensuring competitive parity. Finally, the corporate social responsibility (CSR) initiatives of major companies are playing a significant role. As businesses prioritize sustainability goals and strive to enhance their brand image, they are increasingly incorporating biopolymer packaging into their product offerings, further normalizing and accelerating its adoption across various industries.

Despite the promising growth trajectory, the biopolymer packaging market is not without its inherent challenges and restraints that temper its widespread adoption. A significant hurdle remains the cost premium associated with biopolymer production compared to conventional petroleum-based plastics. While economies of scale are beginning to drive down prices, the initial investment and manufacturing complexities can still make biopolymers a more expensive option for many businesses. Furthermore, the performance limitations of certain biopolymers, particularly in terms of heat resistance, moisture barrier properties, and overall durability, can restrict their application in specific demanding scenarios. This necessitates ongoing research and development to engineer biopolymers that can match or exceed the functionalities of traditional plastics. The current infrastructure for the end-of-life management of bioplastics also presents a considerable challenge. While many biopolymers are designed to be compostable, the availability of industrial composting facilities is not widespread globally. This can lead to bioplastics ending up in landfills, where their intended biodegradability is not realized, or even contaminating conventional plastic recycling streams. Consumer awareness and understanding regarding proper disposal methods for different types of bioplastics are also lacking, contributing to improper waste management. Additionally, the sourcing of raw materials for biopolymers can raise concerns about land use, food security, and competition with agricultural resources, prompting a need for sustainable sourcing practices and the exploration of alternative feedstocks like agricultural waste. Finally, regulatory inconsistencies across different regions regarding labeling, biodegradability standards, and certification can create confusion for manufacturers and consumers alike, hindering seamless global market integration.

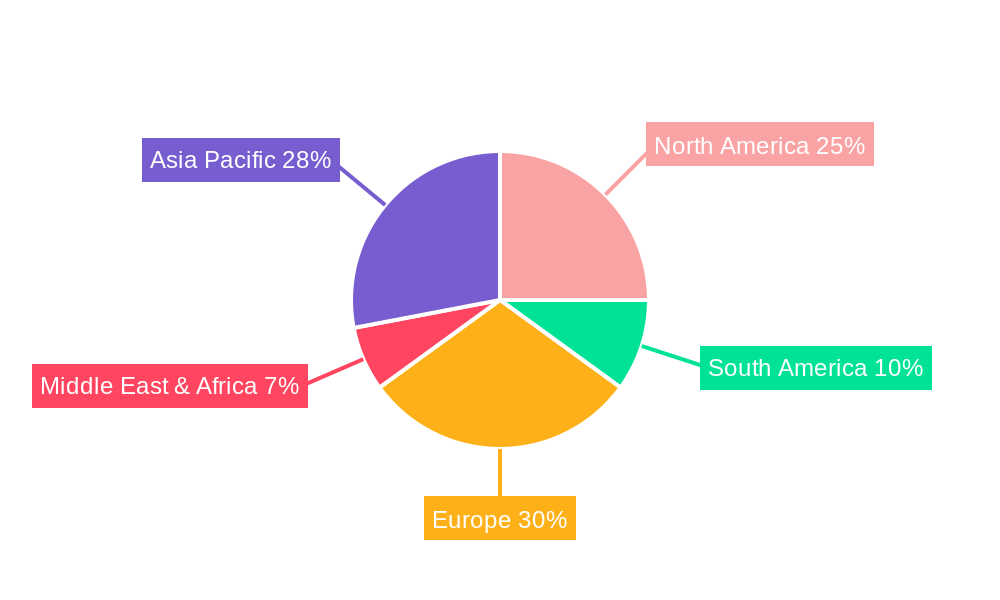

The biopolymer packaging market's dominance is expected to be shaped by specific regions and segments that exhibit strong adoption drivers and robust growth potential.

Dominant Region/Country: Europe is poised to lead the biopolymer packaging market during the forecast period.

Dominant Segment (Type): Polylactides (PLA) is projected to be the dominant type of biopolymer in the packaging sector.

Dominant Segment (Application): Bags & Pouches are expected to emerge as the dominant application segment within the biopolymer packaging market.

The biopolymer packaging industry is experiencing substantial growth catalysts, primarily driven by increasing environmental awareness and stringent government regulations aimed at reducing plastic waste. The rising consumer preference for sustainable products is compelling brands to adopt eco-friendly packaging solutions, thereby boosting demand for biopolymers. Furthermore, advancements in material science are continuously improving the performance and cost-effectiveness of bioplastics, making them more competitive with conventional plastics and expanding their application range. The development of robust composting and recycling infrastructure for bioplastics is also a key growth catalyst, addressing end-of-life concerns and promoting a circular economy model.

This comprehensive report delves into the intricate dynamics of the biopolymer packaging market, providing an in-depth analysis of its current state and future projections. It meticulously examines the market landscape from 2019 to 2033, with a specific focus on the Base Year: 2025 and the Forecast Period: 2025-2033. The study thoroughly explores key market drivers, including escalating environmental concerns and supportive regulatory frameworks, alongside the significant challenges such as cost and infrastructure limitations. It forecasts the market's trajectory, offering insights into the dominant regions and segments, thereby identifying key areas for investment and strategic development. The report also highlights the innovative strides made by leading players and identifies significant technological advancements shaping the industry's future. This detailed coverage aims to equip stakeholders with the knowledge necessary to navigate this evolving market and capitalize on emerging opportunities in sustainable packaging.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 12.0% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 12.0%.

Key companies in the market include Arkema, BASF, NatureWorks, Plantic, Biome Technologies, Plantic Technologies, Bio-On, Toray Industries, Spectra Packaging, United Biopolymers, .

The market segments include Type, Application.

The market size is estimated to be USD 7975.1 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Biopolymer Packaging," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Biopolymer Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.