1. What is the projected Compound Annual Growth Rate (CAGR) of the Beer Glass Bottle Packaging?

The projected CAGR is approximately 3.65%.

Beer Glass Bottle Packaging

Beer Glass Bottle PackagingBeer Glass Bottle Packaging by Type (500ml, 650ml, Other), by Application (Big Company, Small Company, World Beer Glass Bottle Packaging Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

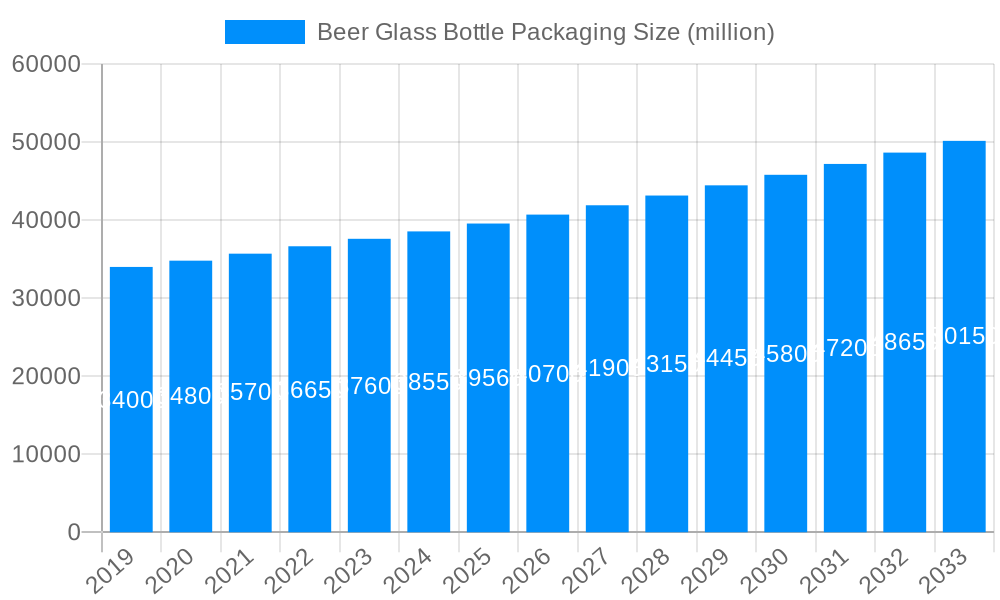

The global beer glass bottle packaging market, valued at approximately $42.44 billion in 2025, is projected to grow at a Compound Annual Growth Rate (CAGR) of 3.65% from 2025 to 2033. This expansion is propelled by several key drivers. The sustained popularity of beer, particularly craft varieties, necessitates premium packaging solutions, with glass bottles offering a perception of superior quality and bolstering brand image. Increasing consumer emphasis on sustainability and the inherent recyclability of glass further solidify its preference over alternatives like plastic. Emerging trends such as lightweighting glass bottles to optimize transportation costs and reduce environmental impact, alongside the adoption of innovative designs and labeling, are also contributing to market growth. However, challenges persist, including volatile raw material prices (glass, energy), potential supply chain disruptions, and competition from alternative packaging formats.

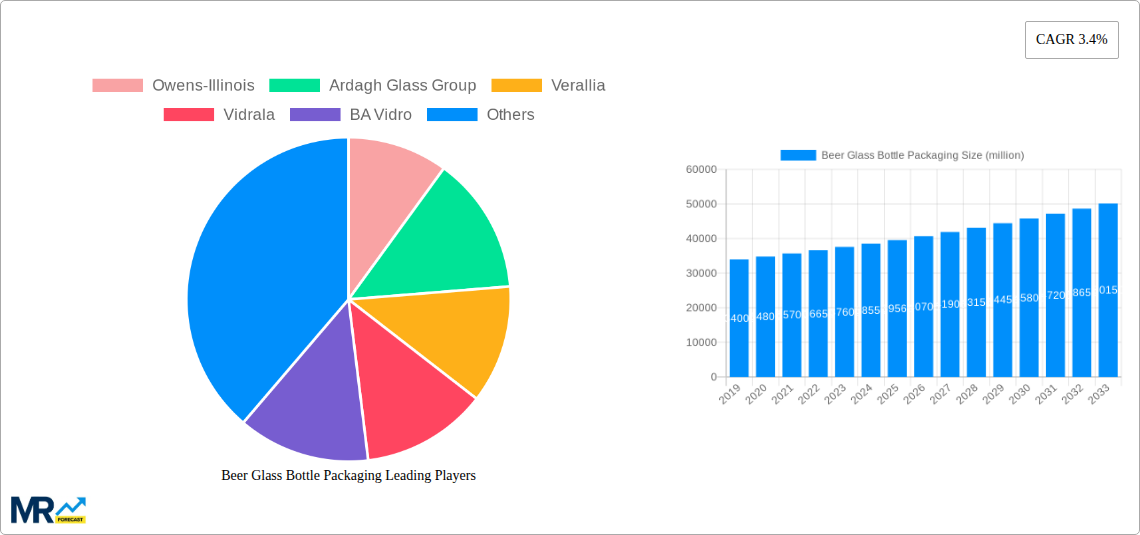

Market segmentation encompasses variations in bottle sizes (e.g., standard, stubby, long neck), closures (crown caps, screw caps), and color options. Leading manufacturers, including Owens-Illinois, Ardagh Glass Group, and Verallia, command a significant market share through their robust manufacturing capacities, global presence, and comprehensive product offerings. Regional dynamics indicate substantial contributions from North America and Europe, driven by established beer consumption habits and mature packaging industries. Emerging economies present considerable growth opportunities, supported by rising disposable incomes and increasing beer consumption. Continued innovation, strategic alliances, and efficient supply chain operations will be vital for market participants to maintain a competitive advantage and leverage opportunities within this dynamic market.

The global beer glass bottle packaging market is experiencing a dynamic shift, driven by evolving consumer preferences and industry innovations. Over the historical period (2019-2024), we witnessed a steady growth trajectory, with the market exceeding XXX million units. This upward trend is expected to continue throughout the forecast period (2025-2033), propelled by several key factors. The increasing demand for premium and craft beers, often packaged in attractive glass bottles, is a significant driver. Consumers are increasingly willing to pay a premium for perceived quality and sustainability, aligning perfectly with the inherent benefits of glass packaging. Furthermore, the growing popularity of eco-conscious packaging solutions is boosting the demand for glass bottles, as they are recyclable and readily available for reuse. However, the market is not without its challenges. Fluctuations in raw material prices, particularly energy costs involved in glass manufacturing, pose a significant threat. Additionally, the rising popularity of alternative packaging materials like aluminum cans presents strong competition. Despite these challenges, innovative designs, such as lightweighting technologies and improved decoration options, are creating new avenues for growth within the beer glass bottle packaging market. The estimated market size in 2025 is projected to reach XXX million units, showcasing a robust and resilient market segment within the broader beverage packaging industry. This growth reflects a confluence of factors, including the enduring appeal of glass, evolving consumer priorities, and strategic innovations within the manufacturing and packaging sectors. The market is characterized by both established players with extensive global reach and smaller, specialized companies catering to niche segments and regional markets. This diverse landscape ensures a continuous evolution of product offerings and packaging technologies.

Several factors are contributing to the robust growth of the beer glass bottle packaging market. The premiumization of beer is a key driver, with consumers increasingly seeking out high-quality, craft beers often packaged in distinctive glass bottles. The perceived quality and prestige associated with glass packaging enhances the brand image and justifies higher price points. Sustainability concerns are also playing a pivotal role. Glass is infinitely recyclable, appealing to environmentally conscious consumers and aligning with the growing corporate social responsibility initiatives of breweries. This shift towards sustainable packaging options is further reinforced by stringent government regulations and consumer pressure, pushing manufacturers to prioritize environmentally friendly materials. Furthermore, technological advancements in glass manufacturing, such as lightweighting techniques, are improving efficiency and reducing production costs. These innovations allow for cost-effective production without compromising the quality and aesthetic appeal of the final product. Finally, ongoing investments in advanced decoration technologies, including screen printing, embossing, and labeling, are enabling greater customization and branding opportunities, further driving market growth. The combination of these factors creates a compelling scenario for continued expansion within the beer glass bottle packaging sector.

Despite the positive market outlook, several challenges hinder the growth of beer glass bottle packaging. The volatility of raw material prices, especially energy costs involved in the high-temperature manufacturing process of glass, presents a significant obstacle. These price fluctuations can directly impact production costs and profit margins. The fragility of glass bottles necessitates careful handling and transportation, leading to potential breakage and increased costs associated with logistics and damage control. The weight of glass bottles also adds to transportation expenses compared to lighter alternatives like aluminum cans. Furthermore, the intense competition from alternative packaging materials, particularly aluminum cans, which offer superior portability and shatter resistance, poses a considerable threat. Aluminum cans' lower weight and higher production speeds often make them a more cost-effective option for large-scale breweries. Finally, regulatory changes and evolving environmental standards necessitate continuous investment in sustainable manufacturing practices and compliance measures. Addressing these challenges requires innovation in manufacturing processes, efficient logistics strategies, and a focus on highlighting the environmental benefits of glass packaging to offset the perceived drawbacks.

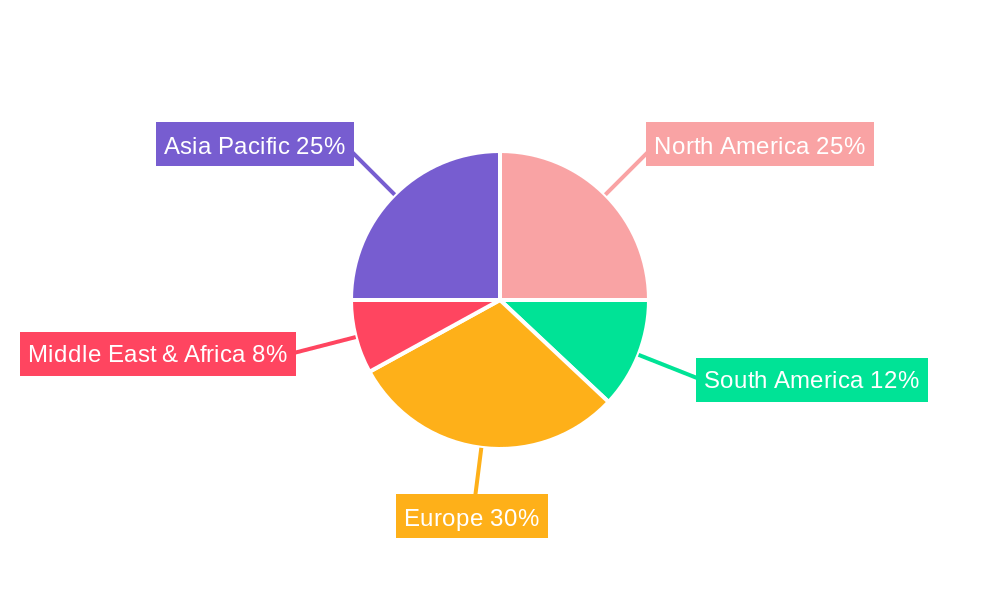

North America: This region is expected to maintain a significant market share due to high beer consumption, a strong craft beer culture, and a growing emphasis on sustainable packaging. The US, in particular, is a major market player, with a large and diverse range of breweries utilizing glass bottle packaging. The demand for premium and craft beers fuels the preference for aesthetically pleasing and perceived higher-quality glass bottles.

Europe: Similar to North America, Europe exhibits robust demand for glass beer bottles, driven by established brewing traditions and a conscious consumer base prioritizing sustainability. Several major glass manufacturers are based in Europe, contributing to the region's dominance. Countries like Germany, the UK, and Belgium, renowned for their beer production, continue to significantly contribute to the market size.

Asia-Pacific: This region is experiencing rapid growth, fueled by rising disposable incomes, increasing urbanization, and a burgeoning craft beer scene. However, the adoption of glass bottles might be slightly slower compared to established markets, owing to the presence of more affordable packaging alternatives. Nevertheless, the ongoing growth in consumer spending and increased awareness of sustainable practices are expected to drive the demand for glass beer bottles in the coming years.

Premium Beer Segment: The premium beer segment is a key driver of growth within the glass bottle packaging market. Premium and craft beer brands often choose glass packaging to enhance their image and emphasize quality, contributing to a higher average selling price and increased profitability. The association of glass with quality and tradition resonates well with consumers seeking a higher-end beer experience.

In summary, while several regions contribute to the global market, North America and Europe, driven by established beer cultures and consumer preferences, are projected to maintain significant market shares throughout the forecast period. The premium beer segment will continue to be a key growth driver due to the premiumization of the beer market, with consumers willing to pay a premium for the quality and perceived prestige associated with glass packaging.

The beer glass bottle packaging industry's growth is significantly catalyzed by the increasing consumer preference for premium and craft beers, which often utilize attractive and high-quality glass bottles. This is further bolstered by the growing awareness of sustainability and the environmentally friendly nature of glass packaging, as well as continuous innovation in lightweighting techniques and decorative options that enhance the appeal and cost-effectiveness of glass bottles. These factors create a synergistic effect, propelling the market forward.

This report provides a comprehensive analysis of the beer glass bottle packaging market, covering historical data, current market trends, and future projections. It delves into the key drivers and restraints shaping market growth, identifies leading players and their market strategies, and offers valuable insights into regional and segmental performance. The report provides a thorough understanding of the market dynamics, facilitating informed decision-making for stakeholders across the value chain.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.65% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 3.65%.

Key companies in the market include Owens-Illinois, Ardagh Glass Group, Verallia, Vidrala, BA Vidro, Vetropack, Wiegand Glass, Pochet Group, Zignago Vetro, Heinz Glas, Stölzle Glas Group, Piramal Glass, VERESCENCE, Nihon Yamamura, HNGIL, Vitro Packaging, Bormioli Luigi, Allied Glass, Vetrobalsamo, Ramon Clemente, Vetrerie Riunite, .

The market segments include Type, Application.

The market size is estimated to be USD 42.44 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Beer Glass Bottle Packaging," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Beer Glass Bottle Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.