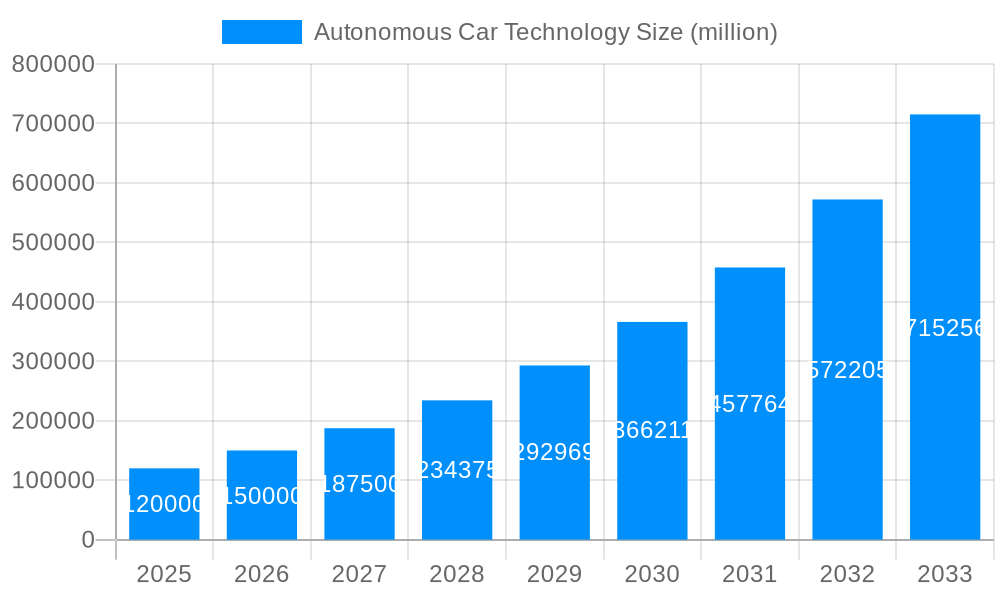

1. What is the projected Compound Annual Growth Rate (CAGR) of the Autonomous Car Technology?

The projected CAGR is approximately 16.44%.

Autonomous Car Technology

Autonomous Car TechnologyAutonomous Car Technology by Type (/> Advanced Driver Assistance System (ADAS), semi-autonomous car technology, fully-autonomous car technology), by Application (/> Adaptive Cruise Control (ACC), Blind Spot Monitoring (BSM), Forward Collision Warning (FCW), Intelligent Speed Adaptation (ISA), Lane Departure Warning (LDW), Night Vision System (NVS), Parking Assistance (PA), Pedestrian Detection System (PDS) and LIDAR, Adaptive Front Lights (AFL)), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The autonomous car technology market is poised for significant expansion, driven by rapid advancements in AI, sophisticated sensor technology, and growing consumer demand for enhanced safety and convenience. Substantial investments from leading automotive manufacturers and technology innovators are accelerating the development of advanced self-driving systems. Despite ongoing challenges including regulatory complexities, infrastructure development needs, and public trust concerns, the long-term trajectory for autonomous vehicles is exceptionally promising. We forecast a substantial market growth, with a CAGR of 16.44%, from a base market size of 31.54 billion in 2025 to 2033. This growth will be propelled by the increasing integration of Advanced Driver-Assistance Systems (ADAS) and the progressive deployment of fully autonomous vehicles, influenced by technological breakthroughs, supportive government policies, and enhanced sensor fusion and data processing capabilities.

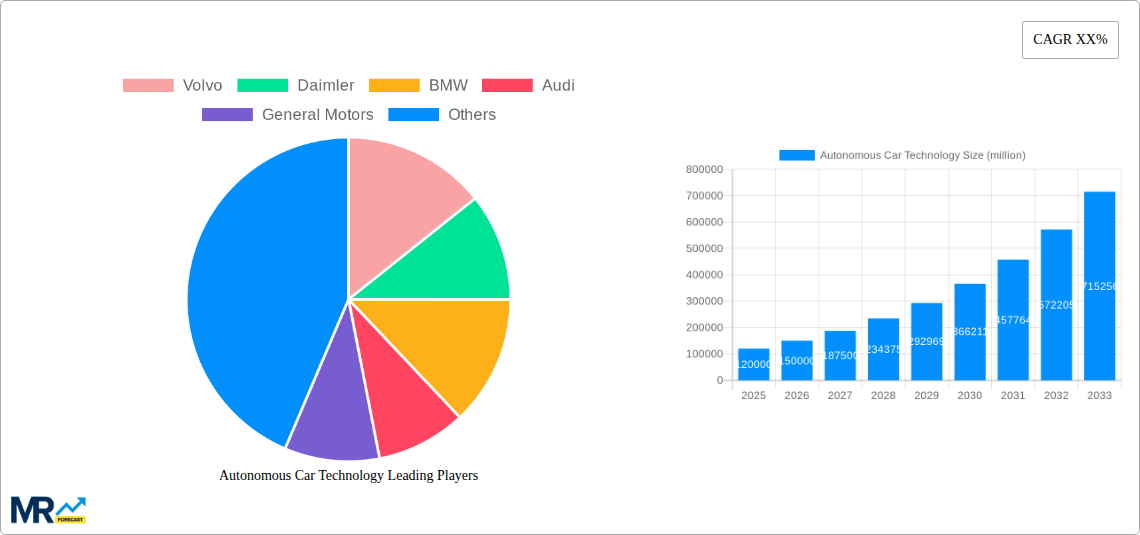

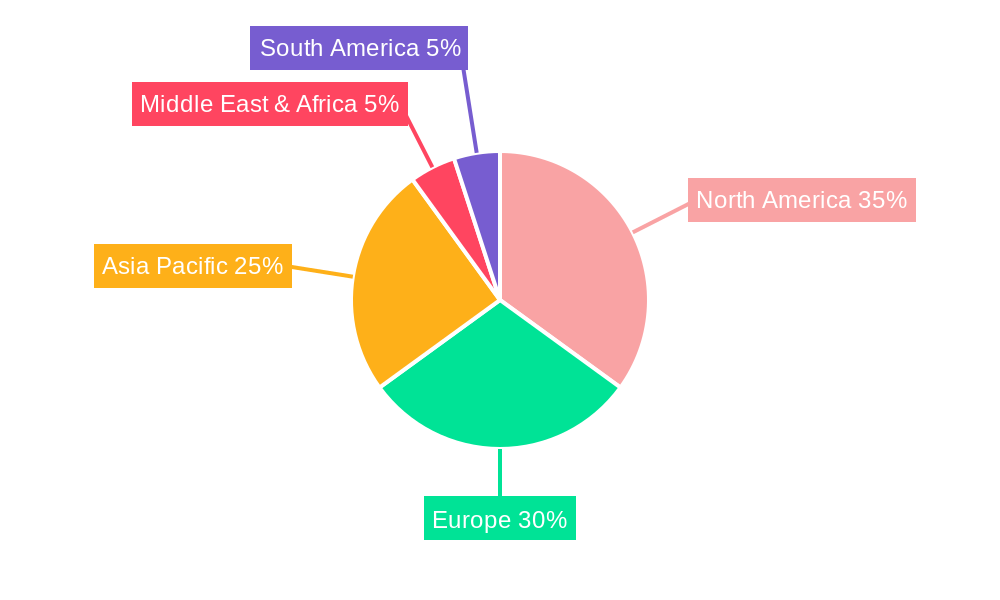

Market segmentation spans multiple levels of autonomy, from Level 2 (partial automation) to Level 5 (full automation). While Level 2 systems are currently dominant, the market is swiftly transitioning towards higher automation levels. Leading companies such as Volvo, Daimler, BMW, Audi, and Tesla are intensely competing for market leadership. Regional adoption rates will vary, with North America and Europe expected to lead initially due to established infrastructure and favorable regulations. However, the Asia-Pacific region is projected for rapid growth in later forecast years, supported by government initiatives and a burgeoning automotive sector. The development of robust cybersecurity protocols and the resolution of ethical considerations will be critical factors shaping the autonomous vehicle market's future.

The global autonomous car technology market is experiencing explosive growth, projected to reach tens of billions of dollars by 2033. This surge is driven by a confluence of factors, including advancements in sensor technology (LiDAR, radar, cameras), artificial intelligence (AI) for path planning and object recognition, and the decreasing cost of computing power necessary for real-time processing of vast amounts of data. The historical period (2019-2024) witnessed significant investments from both established automotive manufacturers and tech giants, leading to substantial progress in autonomous driving capabilities. While fully autonomous vehicles (Level 5 autonomy) remain a long-term goal, the market is currently witnessing a rapid expansion in advanced driver-assistance systems (ADAS) like adaptive cruise control and lane keeping assist, representing a stepping stone towards complete automation. The estimated year of 2025 shows a significant market consolidation, with several key players establishing themselves as leaders in specific segments, such as Level 2 or Level 3 autonomy. The forecast period (2025-2033) predicts continued growth, albeit with a likely shift in focus towards specific niche applications like robotaxis and autonomous trucking, driven by potential profitability and regulatory clarity. The market's expansion is not uniform across all regions, with developed nations leading the charge in technology adoption and infrastructure development. However, emerging economies are rapidly catching up, presenting new opportunities for market expansion in the coming decade. The base year of 2025 provides a crucial benchmark for evaluating the effectiveness of ongoing technological improvements and their impact on the overall market trajectory. Millions of units of autonomous vehicles are projected to be sold globally by 2033, a testament to the transformative potential of this technology. The increasing availability of high-definition maps and improved communication infrastructure also contributes to the overall growth of the market.

Several powerful forces are accelerating the development and adoption of autonomous car technology. Firstly, the relentless pursuit of enhanced road safety is a primary driver. Autonomous vehicles have the potential to significantly reduce accidents caused by human error, a leading cause of fatalities worldwide. Secondly, the promise of increased efficiency and reduced congestion in urban areas is highly attractive. Optimized traffic flow through coordinated autonomous vehicle movements can lead to significant fuel savings and reduced commute times. Thirdly, the burgeoning demand for convenient and accessible transportation, particularly for elderly populations and individuals with limited mobility, is fueling innovation in autonomous driving. Furthermore, the economic incentives for businesses, such as logistics companies and ride-sharing services, are compelling. Autonomous trucking, for example, promises significant cost reductions through increased efficiency and reduced labor costs. Finally, government regulations and supportive policies across several countries are playing a crucial role in shaping the industry and encouraging investments in research and development, further accelerating the pace of innovation. The increasing integration of autonomous features into mass-market vehicles further demonstrates the momentum in this technology.

Despite the significant advancements, several challenges and restraints hinder the widespread adoption of autonomous car technology. One major hurdle is the complexity of developing robust and reliable algorithms capable of handling unpredictable real-world scenarios. Unforeseen events and edge cases present significant difficulties in ensuring safe and dependable autonomous navigation. Secondly, ethical considerations surrounding accident liability and decision-making algorithms pose significant legal and philosophical questions that require careful consideration and regulation. Thirdly, the high cost of developing, testing, and deploying autonomous vehicles remains a substantial barrier, particularly for smaller companies. Furthermore, the need for extensive infrastructure improvements, including high-precision mapping and dedicated communication networks (like 5G), adds another layer of complexity and expense. Public perception and acceptance also play a vital role, with concerns regarding safety, security, and job displacement requiring effective communication and education to overcome. Finally, the regulatory landscape is still evolving, leading to inconsistencies across different jurisdictions and creating uncertainty for businesses investing in autonomous vehicle technology.

North America (USA & Canada): These regions are leading in technological innovation, venture capital investment, and supportive regulatory environments, fostering a robust ecosystem for autonomous vehicle development and testing. The presence of major automakers and technology companies contributes to this dominance. Millions of autonomous vehicles are projected to be deployed in these regions by 2033. The availability of advanced infrastructure also plays a significant role.

Europe (Germany, UK, France): Europe is a significant player, driven by strong automotive manufacturing industries and a focus on sustainable transportation solutions. Stringent safety regulations and an emphasis on data privacy are shaping the market's development.

Asia (China, Japan): China's rapidly growing economy and large domestic market present significant opportunities, although technological advancements need to keep pace with the demand. Japan, with its focus on robotics and advanced technology, is also a key player, although cultural acceptance and regulatory frameworks might present hurdles.

Segment Domination: The passenger vehicle segment will initially lead the market, particularly in the initial stages with Level 2 and Level 3 autonomy. However, the commercial vehicle segment (autonomous trucks and delivery vehicles) will see substantial growth in later years, driven by the potential for significant cost savings and efficiency gains. The robotaxi segment also holds immense potential for future growth, although its realization depends on regulatory clarity and overcoming public perception challenges. The market for components and software supporting autonomous driving will also continue to expand as more vehicles incorporate advanced driver-assistance systems.

The autonomous car technology industry's growth is fueled by several key factors. These include increasing government support and regulatory frameworks, fostering innovation and adoption; advancements in sensor technologies and AI, leading to more robust and reliable autonomous systems; the decreasing cost of essential components and processing power, making autonomous technology more accessible; and the burgeoning demand for safer, more efficient, and convenient transportation solutions, which are particularly appealing to commercial fleets and urban transport systems. Moreover, the strategic partnerships between traditional automakers and technology companies are driving significant innovation and development.

This report provides a comprehensive analysis of the autonomous car technology market, covering historical data, current market trends, future projections, and key players shaping the industry's trajectory. It delves into the driving forces and challenges facing the sector, offering valuable insights for businesses, investors, and policymakers navigating this rapidly evolving landscape. The report emphasizes the significance of technological advancements, regulatory developments, and market dynamics in shaping the future of autonomous driving. The detailed segmentation and regional analysis offers a granular understanding of market opportunities and potential challenges across different geographic locations and specific application segments.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.44% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 16.44%.

Key companies in the market include Volvo, Daimler, BMW, Audi, General Motors, Toyota, Ford, Tesla, Honda, Cisco, Cohda Wireless, Altera, Delphi, Google, Nissan, Fiat Chrysler Automobiles, Hyundai, Mitsubishi, Mazda, Aisin Seiki.

The market segments include Type, Application.

The market size is estimated to be USD 31.54 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Autonomous Car Technology," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Autonomous Car Technology, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.