1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive View Camera?

The projected CAGR is approximately 8.7%.

Automotive View Camera

Automotive View CameraAutomotive View Camera by Type (Rear View Camera, Side View Camera, Surround View Camera, World Automotive View Camera Production ), by Application (Commercial Vehicle, Passenger Vehicle, World Automotive View Camera Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

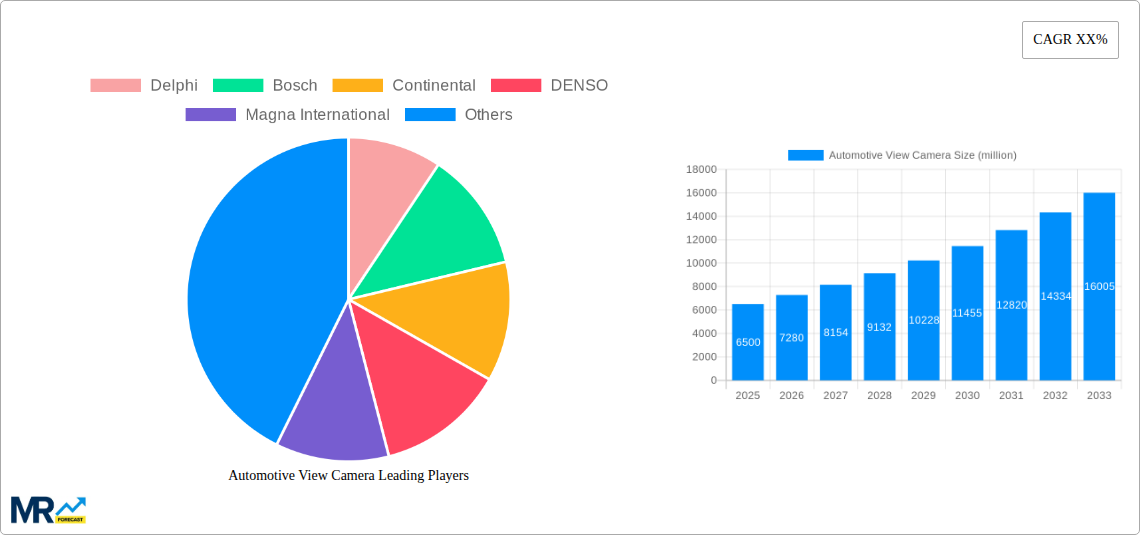

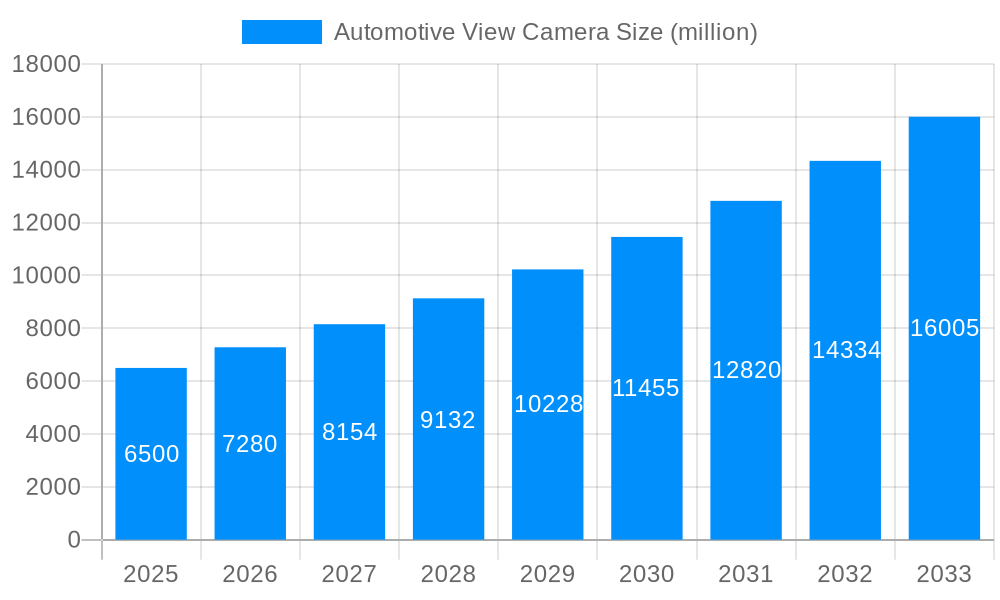

The global automotive camera market is projected for substantial growth, propelled by evolving safety mandates, the widespread adoption of Advanced Driver-Assistance Systems (ADAS), and escalating consumer preference for superior vehicle visibility and convenience. This market, estimated at $8.38 billion in 2025, is forecast to expand at a Compound Annual Growth Rate (CAGR) of 8.7% through 2033. Cameras are increasingly integral to modern vehicles, providing essential rear-view assistance and sophisticated 360-degree surround-view systems, thereby enhancing safety and reducing accidents. Demand is particularly robust in passenger vehicles, where features like parking assist and object detection are becoming standard, and in commercial vehicles, prioritizing operational efficiency and safety. Advancements in high-resolution sensors, low-light performance, and AI integration for object recognition are further stimulating market expansion.

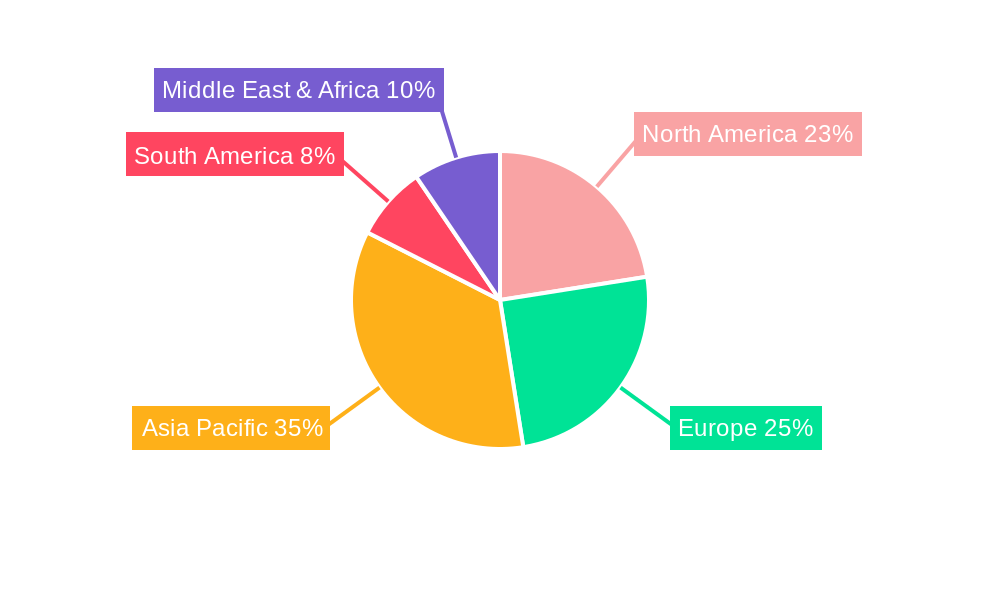

The Asia Pacific region, led by China and India, is set to emerge as a key market due to its substantial automotive manufacturing base and growing integration of smart vehicle technologies. Europe and North America, driven by stringent safety regulations and established automotive sectors, also represent significant markets. Market challenges include the cost of advanced camera systems, potential cybersecurity risks, and the necessity for standardized image processing. However, continuous innovation from industry leaders such as Bosch, Delphi, and Continental, alongside strategic partnerships and acquisitions, are expected to mitigate these hurdles. The market segmentation by camera type includes rear-view, side-view, and surround-view cameras, with surround-view cameras anticipated to lead growth due to their comprehensive safety advantages.

The automotive view camera market is experiencing a dramatic surge, driven by an ever-increasing demand for enhanced safety, driver assistance, and an immersive in-vehicle experience. The historical period from 2019 to 2024 has witnessed a robust expansion, with World Automotive View Camera Production units reaching approximately 45 million units in 2024. This growth is projected to accelerate significantly, with the Base Year of 2025 estimating production to touch 55 million units. The Estimated Year of 2025 will likely solidify this trend, paving the way for an impressive Forecast Period from 2025 to 2033. During this forecast period, the market is anticipated to witness a Compound Annual Growth Rate (CAGR) of over 15%, pushing the World Automotive View Camera Production to well over 150 million units by 2033. This substantial growth is attributed to several key factors, including stringent automotive safety regulations mandating advanced driver-assistance systems (ADAS) and the increasing consumer preference for vehicles equipped with sophisticated camera functionalities. The integration of these cameras is no longer a premium feature but is rapidly becoming a standard across various vehicle segments, from budget-friendly passenger cars to heavy-duty commercial vehicles. Furthermore, advancements in sensor technology, artificial intelligence (AI) for image processing, and miniaturization of camera components are making these systems more affordable and accessible, thereby broadening their adoption. The transition towards higher resolution cameras, wider fields of view, and specialized functionalities like night vision and thermal imaging will further fuel market expansion. The report will delve into the nuanced evolution of these trends, dissecting the specific contributions of different camera types such as Rear View, Side View, and the increasingly popular Surround View systems, and their impact on the global production landscape. The increasing complexity of autonomous driving systems will also be a significant factor, as cameras form a critical sensory input for these advanced technologies, driving innovation and market value.

The automotive view camera market's ascent is underpinned by a confluence of powerful driving forces. Foremost among these is the escalating global emphasis on vehicle safety. Regulatory bodies worldwide are increasingly mandating features like rearview cameras as standard equipment, directly impacting World Automotive View Camera Production. This regulatory push, coupled with a growing consumer awareness and demand for enhanced safety for both drivers and pedestrians, creates a fertile ground for market expansion. Beyond safety, the relentless pursuit of enhanced driver convenience and comfort is another significant propellant. Features such as parking assistance, blind-spot monitoring, and surround-view systems, all powered by advanced cameras, are transforming the driving experience. As vehicles become more integrated with smart technologies, the demand for cameras as a fundamental component for these systems continues to grow. The rapid advancements in automotive technology, particularly in the realms of Artificial Intelligence (AI) and Machine Learning (ML), are enabling cameras to perform more sophisticated tasks, such as object recognition, lane departure warnings, and even pedestrian detection, further solidifying their importance. The integration of cameras into advanced driver-assistance systems (ADAS) and the nascent stages of autonomous driving are also major catalysts, demanding higher performance and more comprehensive visual data.

Despite the robust growth trajectory, the automotive view camera market is not without its share of challenges and restraints. One of the primary hurdles is the cost of integration, especially for advanced systems, which can add a significant premium to vehicle prices, potentially impacting adoption rates in price-sensitive market segments. The complexity of manufacturing and supply chains for high-precision optical components and sophisticated processing units can also pose challenges, particularly in ensuring consistent quality and availability at scale. Furthermore, environmental factors such as extreme temperatures, dust, and moisture can affect camera performance and longevity, necessitating robust engineering and specialized housing, thereby increasing development and production costs. Data processing and bandwidth limitations for handling the vast amounts of data generated by multiple high-resolution cameras are also becoming a concern, requiring significant investment in on-board processing power and efficient data compression techniques. The rapid pace of technological obsolescence is another factor, as newer and more advanced camera technologies emerge, leaving older systems potentially outdated. Finally, cybersecurity concerns related to camera data and potential vulnerabilities in connected vehicle systems need to be addressed to build consumer trust and ensure the integrity of these safety-critical components.

The World Automotive View Camera Production is witnessing significant regional and segment-specific dominance, with Asia-Pacific, particularly China, emerging as a powerhouse in terms of both manufacturing and market demand. Between 2019 and 2033, Asia-Pacific is expected to account for over 40% of the global World Automotive View Camera Production volume. This dominance is fueled by the region's vast automotive manufacturing base, strong government support for advanced automotive technologies, and a rapidly growing middle class with increasing disposable income, driving demand for passenger vehicles equipped with these advanced features.

Within this region, Passenger Vehicle applications are poised to be the largest segment in terms of volume. The study period from 2019-2033 will see passenger cars contributing significantly to the World Automotive View Camera Production. By the Base Year of 2025, passenger vehicles are projected to account for approximately 70% of the total World Automotive View Camera Production units, estimated at 55 million. This is driven by the increasing trend of equipping even compact and mid-size passenger cars with rearview cameras and increasingly, surround-view systems. The affordability of these systems is decreasing, making them accessible to a wider consumer base.

Furthermore, the Surround View Camera segment is experiencing the most dynamic growth within the Type of cameras. While Rear View Camera systems, accounting for around 60% of the total units in 2025, will remain the largest segment by volume due to mandatory regulations, Surround View Camera systems are projected to grow at a CAGR of over 20% during the Forecast Period of 2025-2033. This rapid expansion is due to their ability to provide a comprehensive 360-degree view of the vehicle's surroundings, significantly enhancing parking convenience and low-speed maneuverability, a highly sought-after feature by consumers. The Estimated Year of 2025 will see surround view systems already capturing a substantial market share, estimated at 25 million units, and this is expected to grow exponentially.

In contrast, while Commercial Vehicle applications are a crucial segment, their market share in terms of sheer volume is expected to remain smaller than passenger vehicles during the study period. However, the adoption rate of advanced camera systems, particularly for safety and fleet management, is expected to be high in this segment, driven by operational efficiency and regulatory compliance requirements. The market value of cameras in commercial vehicles is expected to grow substantially due to the higher unit cost of these sophisticated systems.

The global automotive view camera market is a dynamic landscape where regional manufacturing prowess and evolving consumer preferences in specific vehicle segments are shaping the production and adoption trends, with Asia-Pacific and the passenger vehicle segment, particularly with surround-view technology, leading the charge.

Several key growth catalysts are propelling the automotive view camera industry forward. The persistent drive for enhanced vehicle safety, bolstered by increasingly stringent government regulations mandating ADAS features, is a primary driver. The accelerating consumer demand for convenience and sophisticated driver-assistance technologies, such as automated parking and blind-spot monitoring, significantly boosts adoption. Furthermore, rapid technological advancements in sensor resolution, image processing, and AI integration are enabling more sophisticated camera functionalities, making them indispensable for the development of autonomous driving systems. The decreasing cost of camera components and systems, driven by economies of scale and manufacturing efficiencies, is making these features more accessible across a wider range of vehicle segments.

This comprehensive report provides an in-depth analysis of the global automotive view camera market, covering the Study Period of 2019-2033. It meticulously examines World Automotive View Camera Production trends, dissecting the market by Type (Rear View, Side View, Surround View) and Application (Commercial Vehicle, Passenger Vehicle). The report offers detailed insights into the Base Year (2025) and Estimated Year (2025) figures, along with robust projections for the Forecast Period (2025-2033). Key market dynamics, including driving forces, challenges, and growth catalysts, are thoroughly explored. Furthermore, the report identifies leading players in the sector and highlights significant technological developments and industry shifts, providing a holistic view of this rapidly evolving market. The analysis includes quantitative data in millions of units, offering a clear understanding of market scale and future potential.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.7% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 8.7%.

Key companies in the market include Delphi, Bosch, Continental, DENSO, Magna International, Valeo, Stonebridge, FICOSA International S.A., Kappa Optronics GmbH, Minth Group, SL Corporation, Samvardhana Motherson, Aptiv PLC, Clarion, Mobileye, OmniVision Technologies, Hitachi Automotive Systems, Shenzhen Jepen, Shenzhen Mileview, .

The market segments include Type, Application.

The market size is estimated to be USD 8.38 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive View Camera," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive View Camera, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.