1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Valve Guide?

The projected CAGR is approximately 11.91%.

Automotive Valve Guide

Automotive Valve GuideAutomotive Valve Guide by Type (Gasoline Engine Valve Guide, Diesel Engine Valve Guide, World Automotive Valve Guide Production ), by Application (Passenger Car, Commercial Vehicle, World Automotive Valve Guide Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The global automotive valve guide market is poised for significant growth, driven by an increasing demand for efficient and durable engine components. Projected to reach a substantial market size of approximately USD 2.5 billion by 2025, the industry is expected to witness a Compound Annual Growth Rate (CAGR) of around 5.5% through 2033. This robust expansion is fueled by several key factors, including the escalating global vehicle production, particularly in emerging economies, and the continuous evolution of engine technology. The trend towards smaller, turbocharged, and more fuel-efficient engines necessitates advanced valve guide solutions that can withstand higher operating temperatures and pressures, thereby enhancing engine longevity and performance. Furthermore, stringent emission regulations worldwide are pushing manufacturers to adopt cleaner and more efficient combustion technologies, which directly impacts the demand for high-quality valve guides that contribute to optimal engine sealing and reduced emissions. The market also benefits from the growing aftermarket demand for replacement parts as the global vehicle parc ages.

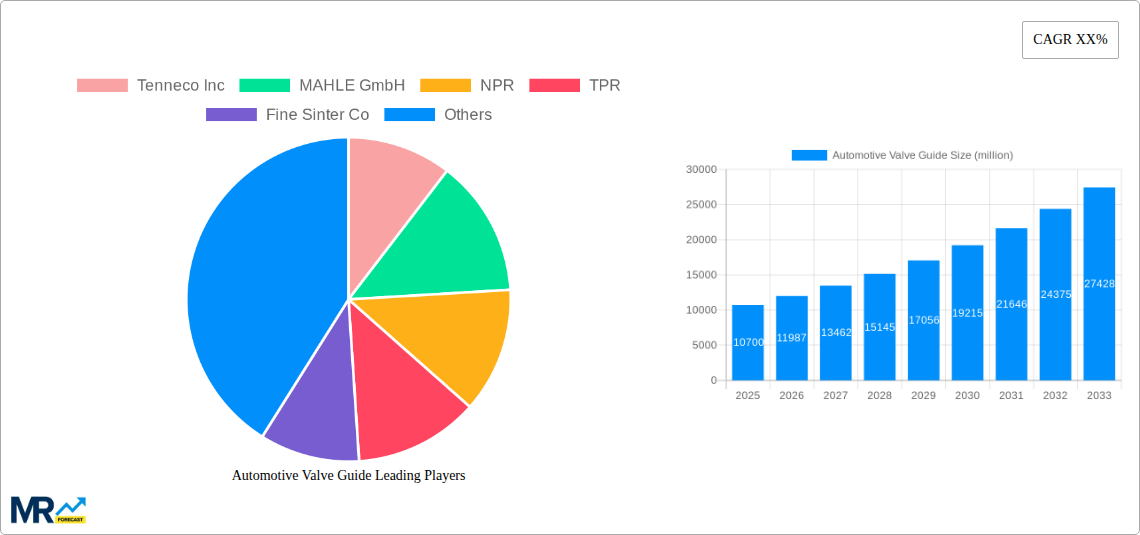

The market is segmented into gasoline and diesel engine valve guides, with the former likely holding a larger share due to the continued prevalence of gasoline engines in passenger cars, especially in major automotive hubs. However, the demand for diesel engine valve guides is expected to remain strong, particularly in the commercial vehicle sector where their durability and fuel efficiency are highly valued. Geographically, the Asia Pacific region is anticipated to lead the market growth, owing to its massive automotive manufacturing base in China and India, coupled with increasing disposable incomes and vehicle ownership. North America and Europe, while mature markets, will continue to contribute significantly due to their high production volumes of advanced vehicles and a strong replacement market. Key players such as Tenneco Inc., MAHLE GmbH, and NPR are actively investing in research and development to introduce innovative materials and manufacturing processes, such as advanced alloys and coating technologies, to meet the evolving demands for enhanced wear resistance, thermal management, and reduced friction in automotive valve guides.

Here is a unique report description for Automotive Valve Guides, incorporating the requested elements and structure:

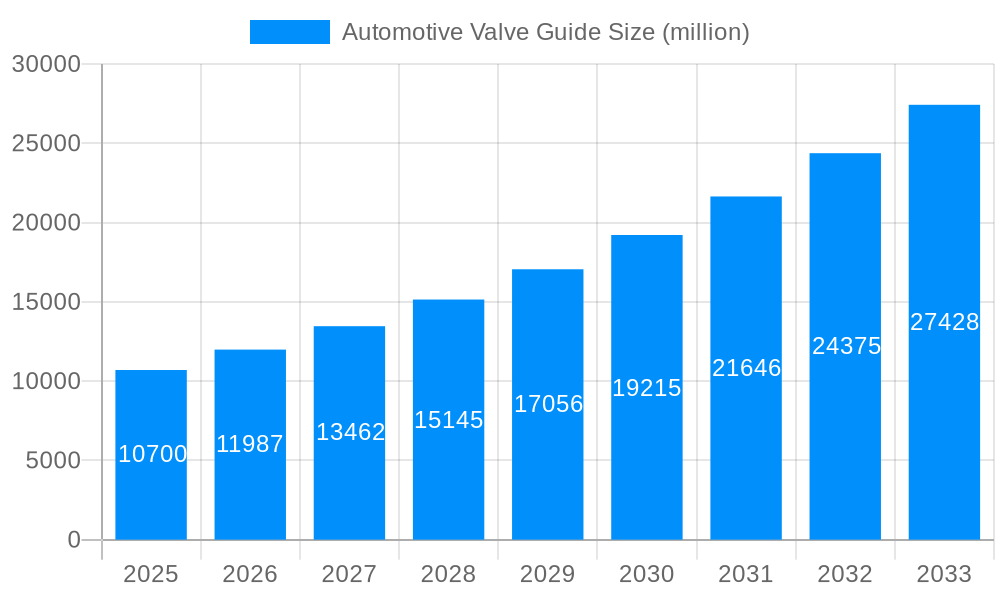

The global automotive valve guide market is poised for robust growth, projected to reach over 250 million units by 2033. This expansion is intricately linked to the evolving automotive landscape, marked by the increasing demand for enhanced engine efficiency, reduced emissions, and improved durability. During the historical period (2019-2024), the market experienced steady growth, fueled by the consistent production of internal combustion engine (ICE) vehicles. The base year, 2025, stands as a pivotal point, with the market estimated to have reached approximately 200 million units, reflecting the ongoing reliance on traditional powertrains. As we move into the forecast period (2025-2033), several key trends are expected to shape the market dynamics. The persistent demand for passenger cars, particularly in emerging economies, will continue to be a significant driver. Furthermore, the increasing stringency of emission regulations globally is pushing manufacturers to develop more sophisticated and efficient engine technologies, which, in turn, necessitates advanced valve guide solutions. This includes the development of lighter, more wear-resistant, and thermally stable valve guides that can withstand higher operating temperatures and pressures. The study period (2019-2033) highlights a trajectory of sustained upward momentum, demonstrating the enduring importance of valve guides even as alternative powertrains gain traction. The market's ability to adapt to these technological shifts and evolving regulatory environments will be crucial for its continued success. Innovations in materials science, such as advanced alloys and coatings, are also playing a vital role in improving valve guide performance and lifespan. The integration of these advanced materials will allow engines to operate more efficiently and reliably, directly impacting the demand for high-quality valve guides. The trend towards optimizing internal combustion engines for hybrid applications also presents a unique opportunity for valve guide manufacturers, as these engines often operate under varied load conditions, demanding robust and adaptable valve train components.

The automotive valve guide market is primarily propelled by the sheer volume of vehicle production worldwide. The continued global demand for passenger cars, a segment estimated to consume over 180 million units of valve guides annually by 2025, remains a cornerstone of market growth. This is further amplified by the commercial vehicle segment, which, while smaller in unit numbers, demands high-durability components due to its intensive operational cycles. Government regulations aimed at improving fuel economy and reducing tailpipe emissions are a critical impetus. Manufacturers are compelled to enhance engine efficiency, and valve guides, as crucial components of the valvetrain, play a vital role in sealing and controlling combustion. The development of more advanced ICE technologies, including turbocharged and direct-injection systems, places greater demands on valve guides, necessitating materials with superior thermal conductivity and wear resistance. This, in turn, drives innovation and the adoption of higher-performance valve guides. The study period from 2019 to 2033 will witness a continuous push towards optimizing ICE performance to meet stringent environmental standards, thereby sustaining the demand for these critical components. The aftermarket for vehicle maintenance and repair also contributes significantly, ensuring a steady demand for replacement valve guides throughout the vehicle's lifecycle.

Despite the positive growth trajectory, the automotive valve guide market faces several challenges and restraints that could temper its expansion. The most significant is the global shift towards electric vehicles (EVs). As EVs gain market share, the demand for ICE components, including valve guides, will inevitably decline in the long term. While ICE vehicles will remain dominant throughout the forecast period, the accelerating pace of EV adoption presents a substantial future restraint. Another challenge is the increasing maturity of ICE technology, which limits the scope for radical improvements in valve guide design using conventional materials. This necessitates a focus on incremental advancements and material innovation, which can be R&D intensive. Price sensitivity among automotive manufacturers, particularly in developing markets, can also pose a challenge. The drive to reduce manufacturing costs may lead to the adoption of lower-cost, albeit less durable, valve guide materials, potentially impacting the overall market value. Furthermore, supply chain disruptions, as evidenced during the historical period, can lead to production delays and increased costs, affecting both manufacturers and consumers. The complexity of modern engine designs, with tighter tolerances and higher operating temperatures, also demands highly precise manufacturing processes, which can increase production costs and introduce quality control challenges.

The Gasoline Engine Valve Guide segment, closely followed by the Diesel Engine Valve Guide segment, is expected to dominate the global automotive valve guide market in terms of production volume throughout the study period (2019-2033). This dominance stems from the sheer prevalence of internal combustion engines (ICE) in the automotive fleet.

Gasoline Engine Valve Guide: This segment is projected to account for a significant portion of the world's automotive valve guide production, estimated to be around 160 million units by the base year of 2025. The widespread adoption of gasoline engines in passenger cars across all major automotive markets, including Asia-Pacific, North America, and Europe, underpins this leadership. The continuous refinement of gasoline engine technology, aimed at improving fuel efficiency and reducing emissions in line with evolving regulations, further solidifies the demand for advanced gasoline engine valve guides. Innovations in materials like sintered alloys and copper-based composites are crucial for enhancing the thermal conductivity and wear resistance required for modern gasoline engines. The application in passenger cars, which represent the largest segment of vehicle sales globally, is the primary driver for gasoline engine valve guides. The projected growth in the passenger car segment, particularly in emerging economies, will continue to fuel the demand for these components.

Diesel Engine Valve Guide: While facing a more pronounced long-term threat from electrification and stricter emissions standards in some regions, diesel engine valve guides will remain a crucial segment, especially for commercial vehicles and heavy-duty applications. The world production for diesel engine valve guides is estimated to reach approximately 70 million units by 2025. These engines, known for their durability and fuel efficiency in specific applications, require robust valve guides capable of withstanding high compression ratios and operating pressures. The commercial vehicle sector, including trucks, buses, and heavy-duty machinery, is a primary consumer of diesel engines. The ongoing need for freight transportation and infrastructure development globally ensures a sustained demand for diesel-powered commercial vehicles, and consequently, for diesel engine valve guides. Regions with significant industrial activity and a strong logistics network, such as Asia-Pacific and parts of Europe, will continue to be major consumers of diesel engine valve guides. The development of advanced diesel engine technologies, such as selective catalytic reduction (SCR) and exhaust gas recirculation (EGR) systems, necessitates valve guides that can perform reliably under these complex operating conditions.

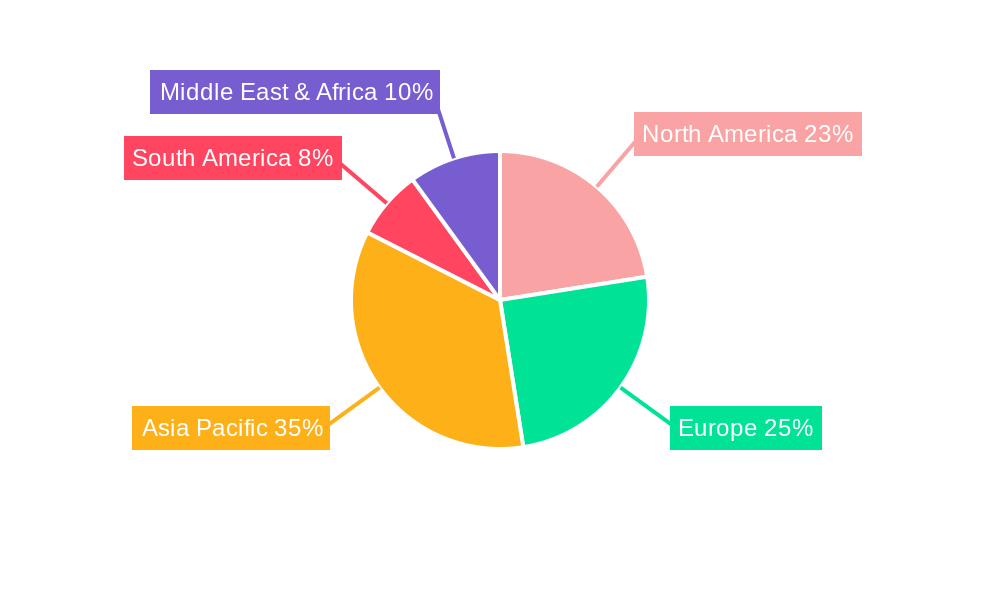

Asia-Pacific is anticipated to emerge as the leading region or country in the automotive valve guide market, driven by its massive automotive manufacturing base and burgeoning vehicle sales. The region's dominance is rooted in the high production volumes of both gasoline and diesel vehicles, catering to both domestic and export markets. Countries like China and India are expected to be significant contributors to this regional leadership, owing to their expanding middle class and increasing disposable incomes, which translate into higher passenger car and commercial vehicle sales. The presence of a robust automotive manufacturing ecosystem, coupled with favorable government policies promoting vehicle production and adoption, further bolsters the market in this region. The continuous advancements in automotive technology within Asia-Pacific, aimed at meeting both local and international emission standards, will necessitate a consistent demand for high-quality automotive valve guides.

The automotive valve guide industry is propelled by several growth catalysts. The sustained demand for internal combustion engine vehicles, especially in emerging economies, ensures a steady base of production. Increasingly stringent emission norms are forcing manufacturers to optimize engine performance, thereby driving the demand for advanced, more durable valve guides. Furthermore, innovations in material science, leading to enhanced wear resistance and thermal management capabilities in valve guides, are crucial for improving engine efficiency and lifespan, thereby acting as significant growth catalysts. The aftermarket segment, driven by vehicle maintenance and repair, also provides a consistent revenue stream.

This comprehensive report offers an in-depth analysis of the global automotive valve guide market, covering the study period from 2019 to 2033. It provides granular insights into market size, segmentation by type (Gasoline Engine Valve Guide, Diesel Engine Valve Guide) and application (Passenger Car, Commercial Vehicle), and regional dynamics. The report elaborates on key market trends, driving forces, challenges, and growth catalysts, supported by estimated figures like over 250 million units projected for 2033. It also details significant industry developments and profiles leading players, offering a holistic understanding of the market's past, present, and future trajectory.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.91% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 11.91%.

Key companies in the market include Tenneco Inc, MAHLE GmbH, NPR, TPR, Fine Sinter Co, Anhui Ring New Group, Anhui Jinyi New Material Corp, OM Internationals, BLEISTAHL, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive Valve Guide," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Valve Guide, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.