1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Solid-state LiDAR?

The projected CAGR is approximately 9.9%.

Automotive Solid-state LiDAR

Automotive Solid-state LiDARAutomotive Solid-state LiDAR by Application (Passenger Car, Commercial Vehicle), by Type (Roof & Upper Pillars, Headlight & Taillights, Bumper & Grill, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

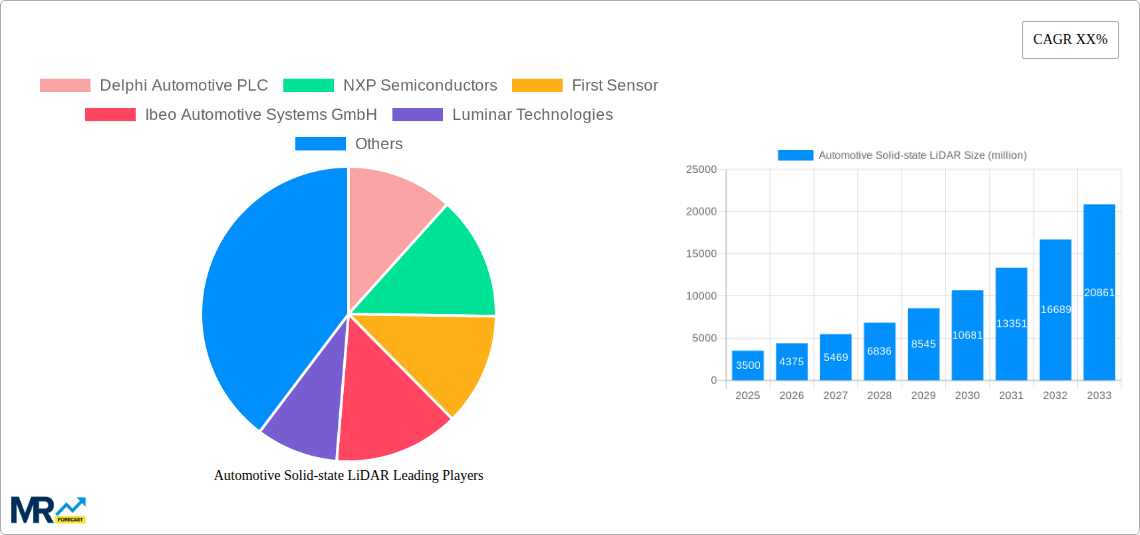

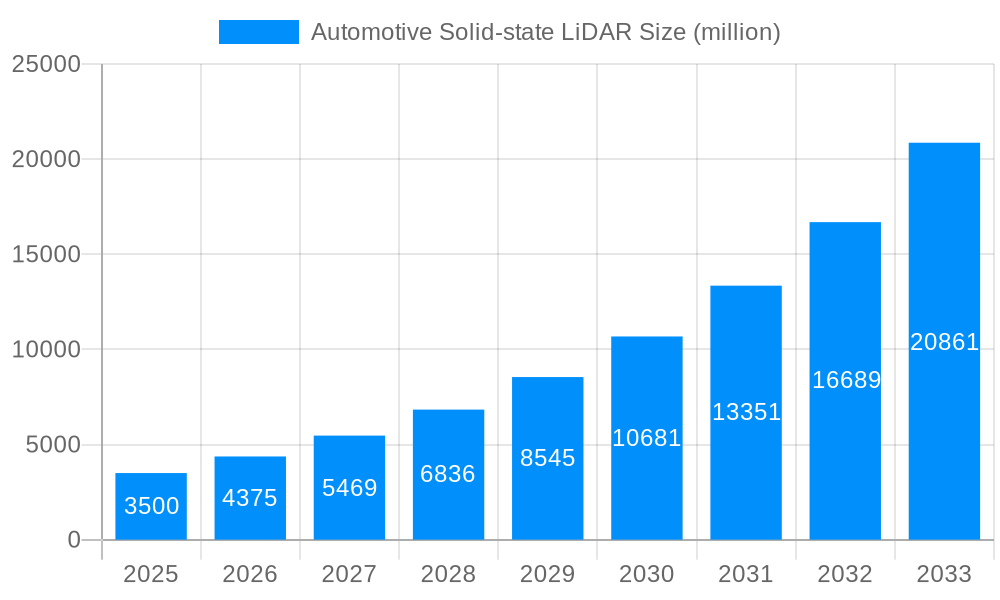

The Automotive Solid-state LiDAR market is poised for significant expansion, driven by the escalating demand for advanced driver-assistance systems (ADAS) and the accelerating development of autonomous driving technologies. With a projected market size of approximately USD 3,500 million in 2025, the sector is expected to witness robust growth, achieving a Compound Annual Growth Rate (CAGR) of around 25% through 2033. This substantial surge is fueled by key drivers such as stringent safety regulations mandating enhanced vehicle perception capabilities, the growing integration of LiDAR for precise object detection and ranging, and the continuous innovation in sensor technology leading to more compact, cost-effective, and higher-performance solid-state solutions. The rising adoption of ADAS features like adaptive cruise control, automatic emergency braking, and lane-keeping assist in mainstream passenger vehicles is a primary catalyst, alongside the aggressive push towards Level 4 and Level 5 autonomy in commercial fleets and robotaxis.

The market is characterized by a dynamic landscape of technological advancements and strategic collaborations among leading automotive component suppliers, semiconductor manufacturers, and specialized LiDAR technology providers. Key trends include the miniaturization of LiDAR units for seamless integration into vehicle designs, the development of more sophisticated software algorithms for data processing and interpretation, and the increasing focus on solid-state architectures over mechanical spinning designs due to their inherent advantages in durability, reliability, and cost. While the growth trajectory is strong, certain restraints, such as the high initial cost of sophisticated LiDAR systems and the ongoing efforts to standardize their integration and data protocols across the automotive industry, may present challenges. However, the continuous reduction in manufacturing costs and the expanding application scope beyond traditional automotive uses, into areas like advanced sensing for industrial automation and security, are expected to propel the market forward, with significant contributions anticipated from Passenger Cars and Commercial Vehicles, and particularly from segments like Roof & Upper Pillars and Headlight & Taillights, where integrated LiDAR solutions are becoming increasingly prevalent.

The automotive solid-state LiDAR market is poised for explosive growth, transitioning from niche applications to a mainstream necessity for advanced driver-assistance systems (ADAS) and autonomous driving (AD). Our comprehensive report, covering the study period of 2019-2033, with a base year of 2025, forecasts a significant surge in unit shipments, potentially reaching over 200 million units by 2033. This exponential rise is fueled by an ever-increasing demand for enhanced safety, sophisticated perception capabilities, and the relentless pursuit of Level 3 and beyond autonomous driving. The transition from mechanical scanning LiDARs to more robust, cost-effective, and compact solid-state solutions, such as MEMS and flash LiDAR, is a defining trend. This shift promises to democratize LiDAR technology, making it more accessible for mass-market passenger vehicles.

The market is witnessing a diversification of LiDAR applications beyond initial ADAS implementations. While passenger cars continue to be the primary driver, commercial vehicles, including trucks and delivery vans, are increasingly adopting LiDAR for platooning, autonomous logistics, and improved situational awareness, projecting significant unit adoption in this segment exceeding 50 million units by 2033. Furthermore, the integration of LiDAR is expanding into novel form factors. Previously confined to roof-mounted units, solid-state LiDAR is now being seamlessly embedded into headlights, taillights, bumpers, and grilles, offering discreet and aesthetically pleasing integration while expanding the sensor's field of view and redundancy. This trend is critical for achieving comprehensive 360-degree environmental perception. The base year 2025 represents a pivotal point where solid-state LiDAR starts to gain significant traction in production vehicles, moving beyond prototype and high-end luxury segments. By 2025, we anticipate the market to already be in the tens of millions of units, with substantial growth projected through the forecast period of 2025-2033, building upon the historical period of 2019-2024 which laid the groundwork for this technological advancement. Key market insights reveal that early adoption by Tier-1 suppliers and OEMs is accelerating, driven by performance improvements, cost reductions, and the growing regulatory push for enhanced vehicle safety.

The automotive solid-state LiDAR market's upward trajectory is underpinned by a confluence of powerful driving forces. Foremost among these is the escalating global emphasis on automotive safety and the reduction of road accidents. Governments worldwide are implementing stricter safety regulations, and consumers are increasingly prioritizing vehicles equipped with advanced safety features. LiDAR, with its ability to provide precise, high-resolution 3D mapping of the environment, acts as a crucial enabler for sophisticated ADAS functions like automatic emergency braking, adaptive cruise control, and pedestrian detection, significantly enhancing overall vehicle safety.

The relentless pursuit of autonomous driving capabilities by automakers is another potent catalyst. As the industry progresses towards higher levels of autonomy (Level 3 and beyond), the need for robust and reliable perception systems becomes paramount. Solid-state LiDAR offers a compelling solution, complementing other sensors like cameras and radar by providing accurate depth information and functioning effectively in diverse lighting and weather conditions where other sensors might falter. The significant advancements in solid-state LiDAR technology itself, leading to reduced costs, smaller form factors, and improved performance characteristics such as increased range and resolution, are also key drivers. These technological leaps are making LiDAR a more viable and attractive option for mass-market vehicle integration. The estimated market size in 2025 already reflects this growing momentum, with projections indicating substantial growth through 2033 as these driving forces continue to mature and converge.

Despite its immense potential, the automotive solid-state LiDAR market faces several significant challenges and restraints that are tempering its unbridled growth. A primary hurdle remains the cost of solid-state LiDAR sensors. While costs are steadily declining, they still represent a considerable investment, especially for non-premium vehicle segments. This cost barrier, though diminishing, continues to limit widespread adoption in budget-conscious vehicles.

Furthermore, the ongoing development and maturation of competing sensor technologies, particularly advanced radar and camera systems, present a challenge. These technologies are also continuously improving in performance and decreasing in cost, leading to ongoing debates about sensor fusion strategies and the optimal mix of sensors for different ADAS and AD functionalities. The perceived complexity of integrating LiDAR into existing vehicle architectures, including the need for sophisticated software and processing power to interpret the vast amounts of data generated, also poses a challenge for some OEMs. Finally, the standardization of LiDAR performance metrics and integration protocols is still evolving, creating some uncertainty for manufacturers and suppliers. While the historical period 2019-2024 saw initial development, the forecast period 2025-2033 will be crucial in overcoming these restraints for broader market penetration. The estimated market in 2025 will reflect these ongoing challenges.

The automotive solid-state LiDAR market is poised for significant regional and segmental dominance, driven by technological adoption, regulatory landscapes, and consumer demand.

Dominant Segments:

Application: Passenger Car: This segment is expected to be the undisputed leader in the automotive solid-state LiDAR market throughout the study period (2019-2033).

Type: Roof & Upper Pillars: While newer integration methods are emerging, the "Roof & Upper Pillars" category of LiDAR placement is expected to maintain a significant presence, particularly in the early to mid-forecast period.

Type: Headlight & Taillights: This segment is anticipated to experience robust growth and become increasingly dominant as the forecast period unfolds.

Dominant Regions/Countries:

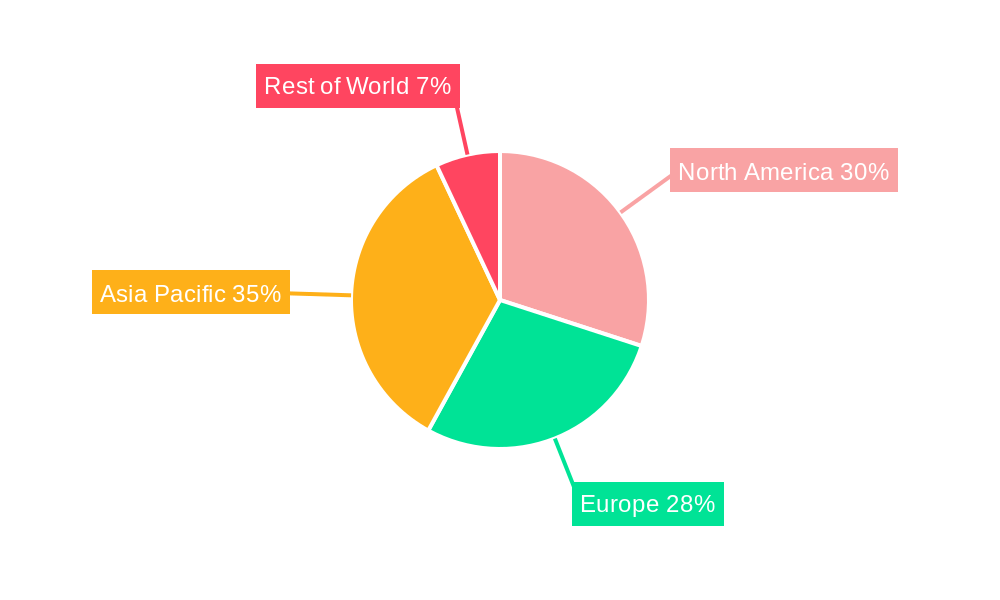

North America (United States):

Europe (Germany):

Asia-Pacific (China):

The automotive solid-state LiDAR industry is propelled by several key growth catalysts. The relentless pursuit of enhanced vehicle safety and the desire to reduce road fatalities is a primary driver, with LiDAR proving indispensable for advanced ADAS functionalities. The escalating development and deployment of autonomous driving technologies, from Level 2+ to full Level 5 autonomy, directly fuels demand for sophisticated perception systems like solid-state LiDAR. Furthermore, significant technological advancements are continuously improving LiDAR performance, reducing costs, and enabling more compact and robust designs, making them increasingly viable for mass-market integration. The evolving regulatory landscape, with governments mandating advanced safety features, also acts as a strong growth catalyst.

This comprehensive report delves deep into the intricate landscape of the automotive solid-state LiDAR market, offering unparalleled insights for stakeholders. We provide an in-depth analysis of market dynamics, including current trends and future projections, from the historical period of 2019-2024 through to 2033, with 2025 serving as the estimated base year. The report meticulously examines the driving forces behind market growth, such as the increasing demand for vehicle safety and the advancement of autonomous driving technologies. It also addresses the critical challenges and restraints, like cost and technological maturity, that shape market progression. Through detailed segmentation by application and type, and an exhaustive regional analysis, we identify key growth areas and dominant markets. Furthermore, the report highlights significant industry developments and profiles the leading players actively shaping this transformative sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.9% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 9.9%.

Key companies in the market include Delphi Automotive PLC, NXP Semiconductors, First Sensor, Ibeo Automotive Systems GmbH, Luminar Technologies, LeddarTech, Continental, Denso Corporation, HELLA GmbH, Robert Bosch GmbH, Quanergy Systems, Velodyne LiDAR, TetraVue, XenomatiX, InnoviZ Technologies, Valeo SA, .

The market segments include Application, Type.

The market size is estimated to be USD 3.8 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive Solid-state LiDAR," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Solid-state LiDAR, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.