1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Rear-View Camera?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Automotive Rear-View Camera

Automotive Rear-View CameraAutomotive Rear-View Camera by Application (Aftermarket, OEMs), by Type (Exterior Mirrors, Interior Mirrors, Under Rearview Mirrors), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

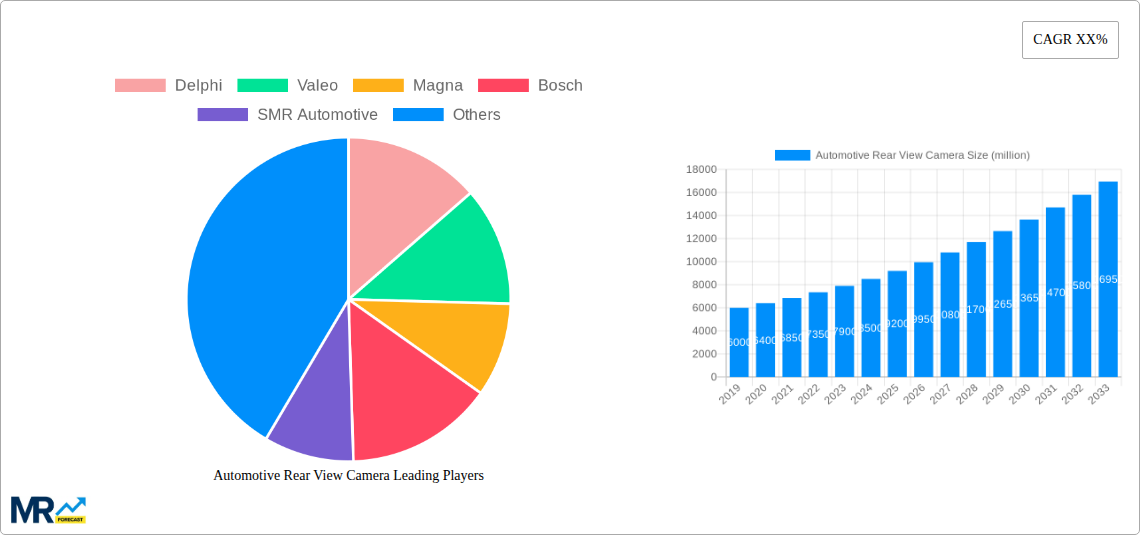

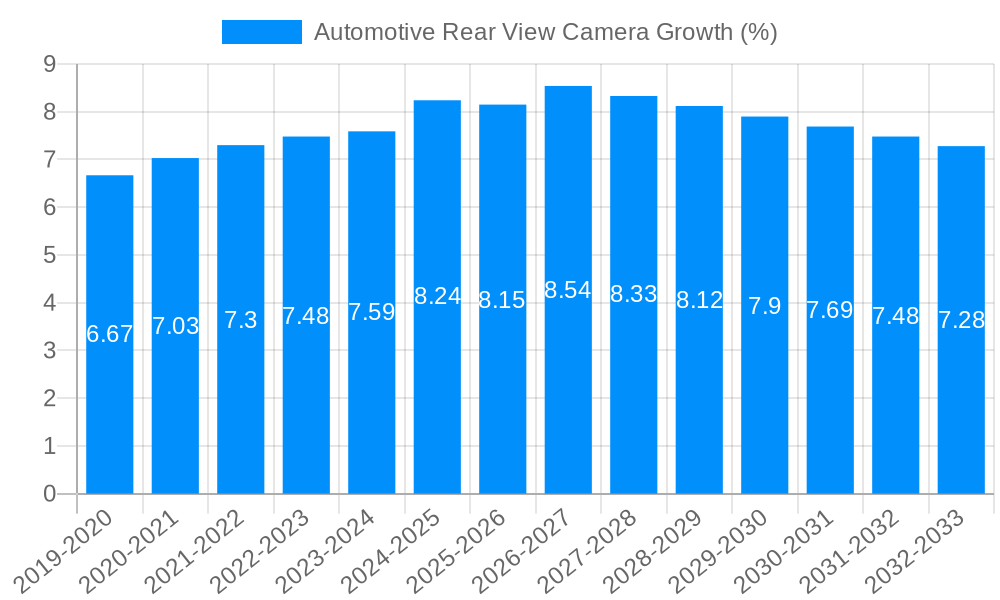

The global automotive rear-view camera market is poised for substantial growth, projected to reach an estimated market size of $2,100 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 12.5% anticipated over the forecast period of 2025-2033. This expansion is primarily fueled by increasing consumer demand for enhanced vehicle safety and driver assistance features, driven by heightened awareness of accident prevention. Government regulations mandating the integration of rear-view cameras in new vehicles, particularly in North America and Europe, are a significant catalyst, ensuring widespread adoption. The aftermarket segment is expected to witness a surge as older vehicles are retrofitted with these safety technologies, complementing the steady demand from Original Equipment Manufacturers (OEMs) integrating them as standard in new car models.

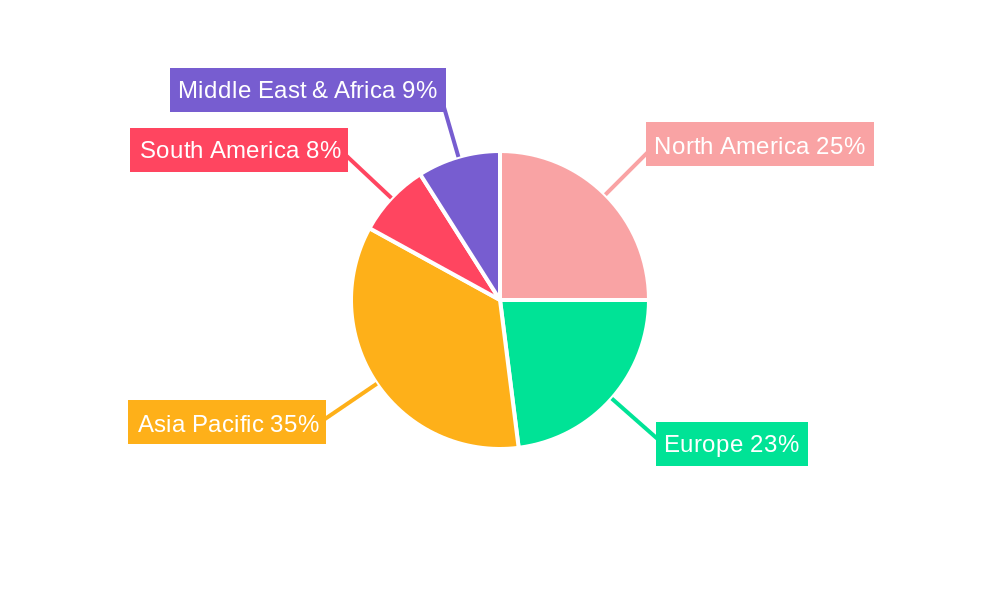

The market's growth trajectory is further supported by ongoing technological advancements, including the development of higher resolution cameras, wider fields of view, and integrated object detection capabilities that enhance situational awareness. The integration of artificial intelligence and machine learning algorithms into rear-view camera systems is also a key trend, enabling more sophisticated driver assistance functionalities. While the market benefits from strong demand drivers, potential restraints include the initial cost of integration for certain vehicle segments and the complexity of installation and calibration in the aftermarket. However, declining component costs and increasing economies of scale are expected to mitigate these challenges. The Asia Pacific region, led by China and India, is anticipated to be a major growth hub due to its expanding automotive production and increasing disposable incomes, leading to greater adoption of advanced safety features.

Here's a unique report description on Automotive Rear-View Cameras, incorporating your specified elements:

The automotive rear-view camera market is poised for substantial growth and transformation, driven by an intricate interplay of evolving consumer expectations, stringent safety regulations, and rapid technological advancements. During the study period of 2019-2033, with a base and estimated year of 2025, this sector is expected to witness a significant upswing, moving from millions of units historically in the 2019-2024 period to even greater penetration in the forecast period of 2025-2033. Key market insights reveal a paradigm shift from the rear-view camera being a mere luxury feature to an indispensable component of modern vehicle safety systems. The increasing adoption of Advanced Driver-Assistance Systems (ADAS) is a primary catalyst, as rear-view cameras serve as foundational sensors for functionalities like parking assistance, blind-spot monitoring, and even as precursors to more sophisticated autonomous driving capabilities. The consumer demand for enhanced safety and convenience, particularly for navigating crowded urban environments and tight parking spaces, is a persistent driver. Furthermore, governmental mandates and safety ratings, such as those from NHTSA in the United States and Euro NCAP in Europe, are increasingly making rear-view cameras a standard fitment, thereby accelerating their adoption across a wider spectrum of vehicles, from entry-level sedans to premium SUVs. The integration of higher resolution cameras, wider field-of-view lenses, and intelligent image processing algorithms is continuously improving the user experience, providing clearer and more comprehensive views of the vehicle's surroundings. The evolution towards digital mirrors, replacing traditional optical mirrors with high-definition displays fed by external cameras, represents a significant trend, offering improved visibility in adverse weather conditions and at night. This trend is expected to gain considerable momentum throughout the forecast period, fundamentally altering the design and functionality of rear-view systems. The market is also seeing a diversification of camera types, with an increasing focus on surround-view camera systems that provide a 360-degree perspective, further bolstering driver confidence and mitigating potential hazards. The underlying technology, from CMOS sensors to advanced processing chips, is also becoming more sophisticated and cost-effective, making these safety features accessible to a broader range of automotive segments. The shift towards electric vehicles (EVs) and the unique design considerations they present, such as the potential for aerodynamic improvements by replacing traditional wing mirrors with cameras, also presents a nascent but significant trend influencing the future trajectory of this market.

Several potent forces are collaboratively propelling the automotive rear-view camera market into an era of sustained expansion. Foremost among these is the undeniable commitment to enhancing vehicular safety. Rear-view cameras have proven their efficacy in significantly reducing accidents, particularly those involving low-speed maneuvers and reversing. This demonstrable impact has led to a strong push from regulatory bodies worldwide to make these systems a mandatory feature in new vehicles. Governments are recognizing the societal benefit of fewer accidents, and consequently, mandating their inclusion to protect drivers, passengers, and pedestrians alike. Beyond regulatory impetus, consumer awareness and demand play a crucial role. As drivers become more accustomed to the convenience and safety offered by rear-view cameras, they actively seek out vehicles equipped with them. The "connected car" trend further amplifies this demand, with rear-view cameras serving as fundamental components for integrated infotainment and driver-assistance systems. The proliferation of smartphones and the expectation of seamless digital experiences in vehicles translate into a desire for advanced visual aids. The automotive OEMs are responding to this demand, not only to meet regulatory requirements but also to differentiate their product offerings and cater to evolving consumer preferences. The continuous innovation in imaging technology, including higher resolutions, wider dynamic range, and improved low-light performance, makes the visual output more informative and less susceptible to environmental challenges. This technological advancement directly translates into a better user experience, further solidifying the camera's indispensable role.

Despite the robust growth trajectory, the automotive rear-view camera market is not without its share of challenges and restraints that manufacturers and suppliers must navigate. One significant hurdle lies in the cost associated with the integration of these advanced systems. While component costs have been declining, the overall system cost, including cameras, processors, displays, and wiring harnesses, can still represent a considerable expense, particularly for entry-level vehicle segments. This can lead to a price sensitivity among some consumers and OEMs, potentially slowing down the adoption rate in price-conscious markets or for more basic vehicle trims. The complex supply chain and the reliance on specialized components can also present vulnerabilities. Geopolitical factors, trade disputes, and disruptions in the availability of semiconductors can impact production volumes and lead times, creating uncertainty for market participants. Furthermore, the performance of rear-view cameras can be affected by environmental factors. Harsh weather conditions, such as heavy rain, snow, or fog, can obscure the camera lens, reducing visibility and potentially compromising the effectiveness of the system. The accumulation of dirt, mud, or ice on the lens is a persistent issue that requires regular cleaning, which consumers may not always prioritize. The evolving landscape of vehicle electronics also presents a challenge in terms of system integration and compatibility. Ensuring seamless integration with existing vehicle architectures and other ADAS features can be technically demanding and require significant investment in research and development. The potential for cybersecurity threats to connected vehicle systems, including those utilizing camera data, is another concern that needs to be addressed through robust security measures. Finally, the rapid pace of technological innovation means that older camera systems can quickly become obsolete, creating a need for continuous upgrades and a potential for market saturation with older technologies if not managed strategically.

The automotive rear-view camera market is characterized by distinct regional dynamics and segment preferences, with certain areas and applications poised to lead in terms of adoption and growth.

Dominant Regions/Countries:

Dominant Segments:

Application: OEMs (Original Equipment Manufacturers)

Type: Exterior Mirrors

Several key growth catalysts are fueling the expansion of the automotive rear-view camera industry. The primary catalyst remains the persistent drive for enhanced vehicular safety, leading to increasingly stringent government regulations mandating their fitment. This regulatory push ensures a foundational demand across all vehicle segments. Secondly, a growing consumer preference for advanced safety and convenience features, coupled with increased awareness of the benefits rear-view cameras offer in preventing accidents, is a powerful market driver. The continuous technological advancements, such as higher resolution imaging, wider fields of view, and improved low-light performance, are making these cameras more effective and user-friendly, encouraging wider adoption. Furthermore, the integration of rear-view cameras into broader Advanced Driver-Assistance Systems (ADAS) ecosystems, acting as essential sensors for parking assistance, blind-spot monitoring, and more, significantly boosts their relevance and demand.

This comprehensive report delves deep into the intricate dynamics of the automotive rear-view camera market, providing unparalleled insights from the historical period of 2019-2024 through to the projected future up to 2033, with a pivotal base and estimated year of 2025. It meticulously analyzes market trends, identifies the principal driving forces such as regulatory mandates and consumer demand, and scrutinizes the challenges and restraints including cost implications and environmental limitations. The report offers a detailed breakdown of key regional dominance, highlighting North America, Europe, and the rapidly growing Asia-Pacific region, while also dissecting the critical application segments, with a particular focus on the overwhelming dominance of OEMs. Furthermore, it elucidates the growth catalysts that are propelling the industry forward, such as technological innovation and ADAS integration. A detailed examination of the leading global players, alongside a timeline of significant developments, provides a holistic view of the market's evolution and future trajectory. This report is an essential resource for stakeholders seeking to understand and capitalize on the expanding opportunities within this vital automotive safety sector.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Delphi, Bosch, Continental, DENSO, Magna International, Valeo, .

The market segments include Application, Type.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive Rear-View Camera," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Rear-View Camera, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.