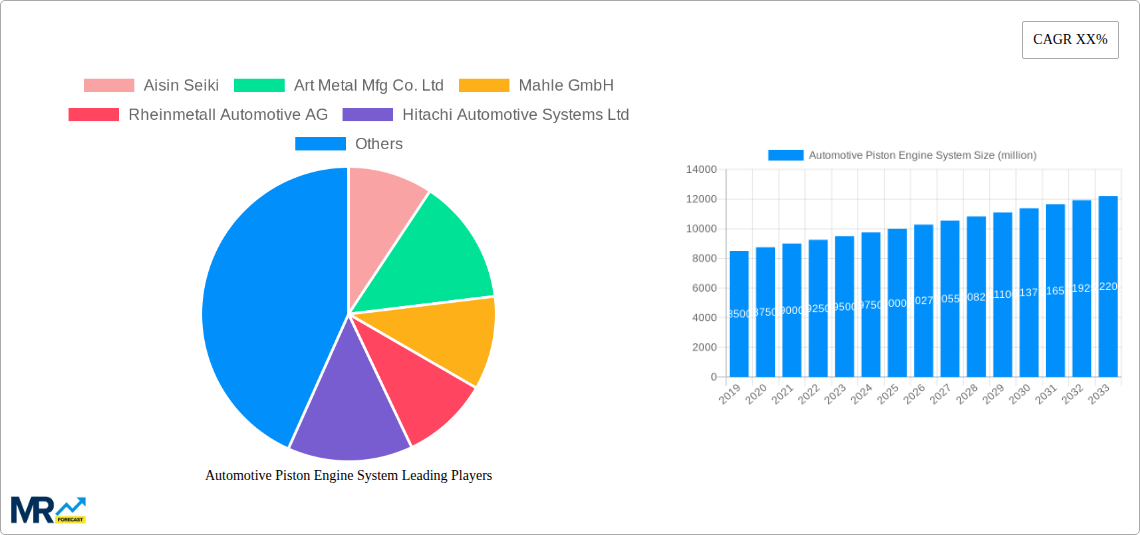

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Piston Engine System?

The projected CAGR is approximately 2.4%.

Automotive Piston Engine System

Automotive Piston Engine SystemAutomotive Piston Engine System by Type (Gasoline, Diesel, Biofuels), by Application (Commercial Vehicle, Passenger Vehicle), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

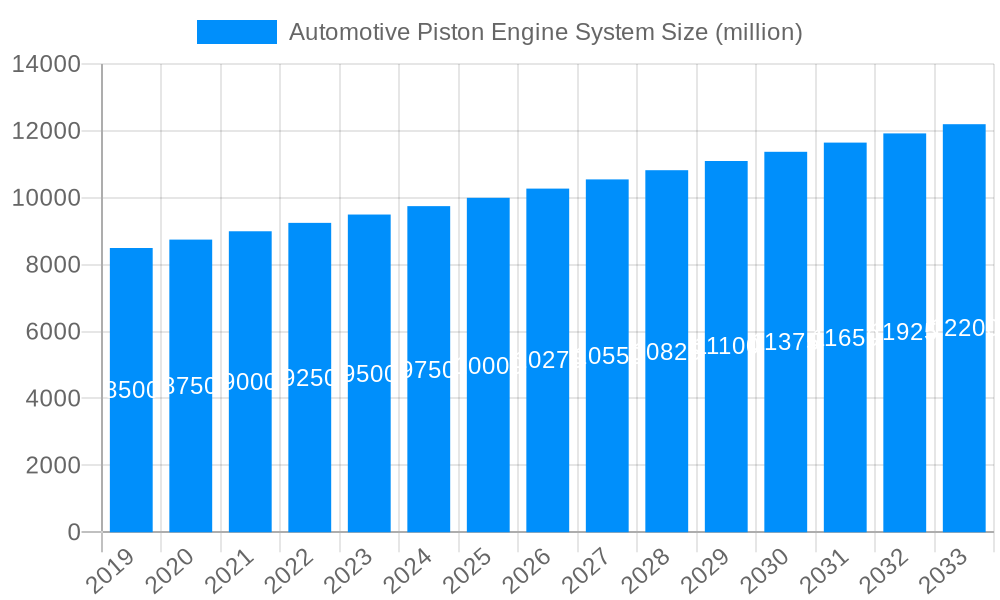

The global Automotive Piston Engine System market is poised for substantial growth, projected to reach an estimated market size of USD 10,000 million by 2025, with a Compound Annual Growth Rate (CAGR) of 5.5% through 2033. This robust expansion is primarily fueled by the sustained demand for internal combustion engine (ICE) vehicles, particularly in emerging economies and for specific commercial applications where electrification is still in nascent stages. The market is segmented by type, with Gasoline and Diesel engines continuing to dominate, albeit with a growing interest in Biofuels as a sustainable alternative. Application-wise, Commercial Vehicles are expected to be a significant growth engine due to increasing logistics and transportation needs, while Passenger Vehicles will maintain a substantial share. Key drivers include evolving automotive regulations that still permit ICE technology with improved efficiency, advancements in engine technology leading to better performance and reduced emissions, and the sheer volume of vehicle production globally.

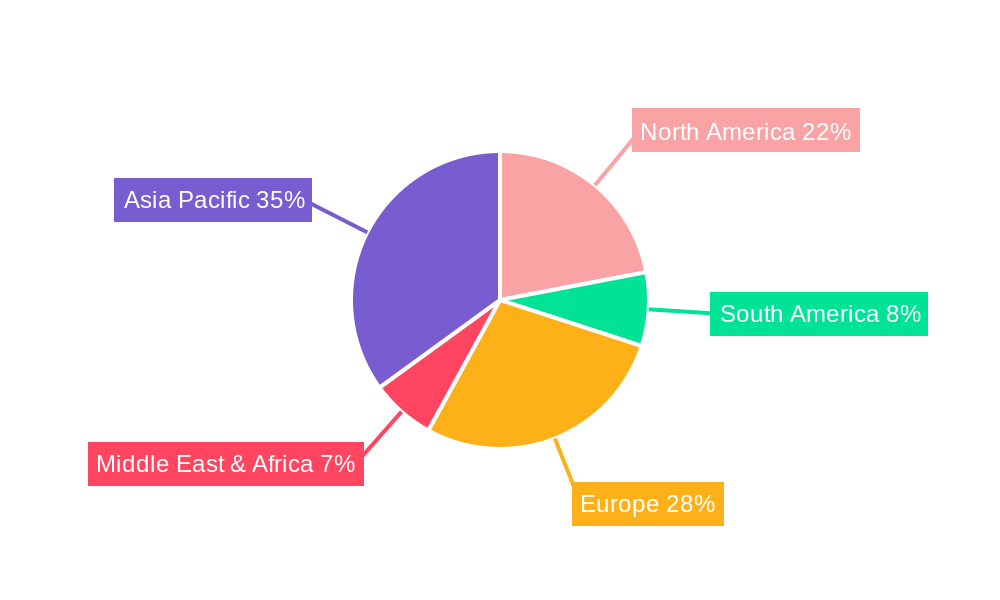

Despite the burgeoning EV revolution, the Automotive Piston Engine System market will witness steady growth driven by technological innovations and ongoing demand for ICE vehicles. Restraints such as stringent emission norms and the accelerating adoption of electric vehicles will necessitate a focus on enhancing the efficiency and environmental performance of piston engines. Players like Aisin Seiki, Mahle GmbH, and Rheinmetall Automotive AG are at the forefront, investing in research and development to optimize engine components and explore hybrid solutions. The market will also see consolidation and strategic collaborations as companies adapt to evolving industry landscapes. Geographically, Asia Pacific, led by China and India, is expected to be the largest and fastest-growing market, owing to its massive automotive production and consumption base. North America and Europe will also remain significant markets, with a focus on premium and performance-oriented ICE applications, alongside evolving emission standards.

This comprehensive report delves into the dynamic global market for Automotive Piston Engine Systems, meticulously analyzing its trajectory from the historical period of 2019-2024 through to an estimated 2025 and a detailed forecast spanning 2025-2033. With a base year of 2025, this study provides invaluable insights into market size, segmentation, regional dynamics, key trends, and the pivotal factors shaping the industry. The report estimates the global Automotive Piston Engine System market to reach XXX million units by 2033, showcasing a consistent yet evolving demand for internal combustion engine technology.

The automotive piston engine system market, despite the burgeoning adoption of electric vehicles, continues to demonstrate resilience and innovation, particularly within the historical period of 2019-2024 and projecting into the forecast period of 2025-2033. A key market insight is the ongoing optimization of existing piston engine technologies to meet increasingly stringent emissions standards and improve fuel efficiency. This includes advancements in direct injection, turbocharging, and variable valve timing, which have significantly enhanced performance while reducing environmental impact. The market is also witnessing a gradual shift in the composition of engine types. While gasoline engines have historically dominated, the demand for diesel engines, particularly in commercial vehicle applications requiring higher torque and fuel economy, remains substantial, albeit facing regulatory pressures in certain regions. Biofuels, while still a niche segment, are gaining traction as manufacturers explore sustainable alternatives to traditional fossil fuels, driven by a growing environmental consciousness and government mandates. The Passenger Vehicle segment continues to be the largest application, driven by global vehicle sales, but the Commercial Vehicle segment is showing robust growth due to the essential nature of logistics and transportation. The Industry Developments section, covering the period from 2019 to 2033, highlights a strategic focus on hybridization, where piston engines work in tandem with electric powertrains to achieve optimal efficiency and performance. This trend is expected to sustain the relevance of piston engines for a considerable period, even as the automotive landscape transforms. Furthermore, the report identifies a growing emphasis on lightweight materials and advanced manufacturing techniques to reduce engine weight and improve overall vehicle performance. The transition towards more efficient and cleaner piston engines is not just a technological evolution but a market imperative, driven by consumer demand for cost-effective and environmentally responsible transportation solutions. The estimated market size of XXX million units by 2033 underscores the continued, albeit potentially moderated, significance of piston engines in the global automotive ecosystem.

The sustained demand for automotive piston engine systems, projected to reach XXX million units by 2033, is propelled by a confluence of powerful driving forces. Primarily, the sheer volume of global vehicle production, especially within the passenger vehicle segment, continues to necessitate the manufacturing of millions of piston engines annually. Despite the rise of electric vehicles, internal combustion engines remain the most cost-effective and readily available powertrain solution for a significant portion of the global market, particularly in developing economies where charging infrastructure is less prevalent and upfront vehicle costs are a major consideration. Furthermore, advancements in piston engine technology, such as direct fuel injection, turbocharging, and sophisticated engine management systems, have significantly improved their efficiency and reduced emissions. These technological leaps have allowed piston engines to remain competitive and compliant with evolving environmental regulations, extending their lifecycle. The robust infrastructure for fuel supply and servicing associated with piston engines also contributes to their continued adoption. Consumers and fleet operators are accustomed to the existing fuel networks and the widespread availability of mechanics skilled in servicing these engines, reducing concerns about range anxiety and maintenance complexities often associated with newer powertrain technologies. The inherent robustness and proven reliability of piston engines, honed over decades of development, provide a strong sense of security for buyers, particularly in the commercial vehicle sector where uptime and dependability are paramount.

The automotive piston engine system market, despite its persistent strengths, faces significant challenges and restraints that are shaping its future trajectory towards the forecast period of 2025-2033. The most prominent restraint is the accelerating global shift towards electrification. Stringent government regulations aimed at reducing carbon emissions and phasing out internal combustion engine (ICE) vehicles are compelling automakers to invest heavily in battery electric vehicles (BEVs) and other zero-emission technologies. This regulatory pressure is leading to a decline in demand for new ICE vehicles in key markets, directly impacting the production volumes of piston engines. Consumer perception and growing environmental awareness also play a crucial role, with an increasing number of buyers opting for EVs due to their perceived sustainability and lower running costs, despite the higher initial purchase price. The volatile pricing of raw materials essential for piston engine manufacturing, such as aluminum, iron, and precious metals used in catalytic converters, can also impact profitability and competitiveness. Supply chain disruptions, as evidenced in recent years, pose a continuous risk, affecting production schedules and increasing costs. Furthermore, the substantial research and development investments required to meet ever-tightening emissions standards and improve fuel efficiency place a significant financial burden on manufacturers, potentially slowing down innovation in certain areas. The high cost of developing and implementing new ICE technologies that can compete with the performance and efficiency gains offered by EVs presents a formidable hurdle.

The global Automotive Piston Engine System market is poised for significant shifts, with Asia Pacific emerging as a dominant region, driven by robust demand from its burgeoning automotive industry and a substantial population. Within this region, China stands out as a key country, not only as a massive consumer of vehicles but also as a leading manufacturer of automotive components, including piston engines. The sheer scale of vehicle production in China, encompassing both passenger and commercial vehicles, translates into an enormous and sustained demand for piston engine systems. Factors contributing to Asia Pacific's dominance include the presence of major automotive manufacturing hubs, a growing middle class with increasing purchasing power for vehicles, and relatively more lenient emission regulations in some developing economies compared to highly regulated Western markets.

Considering the segments, Passenger Vehicles are expected to continue dominating the market in terms of unit volume. The ongoing global demand for personal transportation, coupled with the affordability of gasoline-powered vehicles in many developing nations, underpins this segment's strength. However, the Commercial Vehicle segment is anticipated to exhibit strong growth. This is primarily attributed to the essential role of commercial vehicles in global trade and logistics, which has seen a surge in demand in recent years. Furthermore, diesel engines, prevalent in commercial vehicles, offer superior torque and fuel efficiency for heavy-duty applications, making them indispensable for many businesses. The report anticipates the demand for gasoline engines to remain significant in passenger vehicles, particularly in emerging markets. However, the growth of biofuels as an alternative fuel source is also a noteworthy trend, driven by sustainability initiatives and government support, though its market share is expected to be more incremental compared to gasoline and diesel.

The dominance of Asia Pacific and the continued strength of the Passenger Vehicle segment, complemented by the robust growth in Commercial Vehicles, paint a clear picture of the market's future. The report’s analysis, covering the forecast period of 2025-2033, will provide granular data on these regional and segmental dynamics, offering strategic insights for stakeholders. The estimated market size of XXX million units by 2033 will be largely shaped by the purchasing patterns and regulatory landscapes within these dominant regions and segments.

Several key factors are acting as growth catalysts for the automotive piston engine system industry, ensuring its continued relevance even amidst the rise of alternative powertrains. The relentless pursuit of fuel efficiency and emission reduction through advanced technologies like direct injection and turbocharging keeps piston engines competitive. The significant investments by manufacturers in hybrid powertrains, where piston engines are integrated with electric motors, offer a balanced solution for performance and environmental responsibility, extending the life of ICE technology. Furthermore, the vast existing infrastructure for fueling and servicing piston engines provides a crucial advantage, making them a practical and cost-effective choice for many consumers and businesses globally.

This report offers an in-depth and granular analysis of the global Automotive Piston Engine System market, encompassing all crucial aspects for strategic decision-making. From the historical performance during 2019-2024 to the projected market landscape up to 2033, with a base year of 2025, it provides a complete picture. The study details market segmentation by type (Gasoline, Diesel, Biofuels) and application (Commercial Vehicle, Passenger Vehicle), alongside critical industry developments. It identifies the key drivers, challenges, and growth catalysts that are shaping the market dynamics. Furthermore, the report includes a comprehensive overview of leading players and their contributions. This detailed coverage ensures stakeholders gain a thorough understanding of market trends, competitive landscape, and future opportunities within the Automotive Piston Engine System sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 2.4%.

Key companies in the market include Aisin Seiki, Art Metal Mfg Co. Ltd, Mahle GmbH, Rheinmetall Automotive AG, Hitachi Automotive Systems Ltd, Shriram Pistons & Rings Ltd, Magna International Inc., Tenneco Inc, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive Piston Engine System," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Piston Engine System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.