1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Main Control Chip?

The projected CAGR is approximately 5.1%.

Automotive Main Control Chip

Automotive Main Control ChipAutomotive Main Control Chip by Type (Computing Chip, Control Chip), by Application (Smart Cockpit, ADAS, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

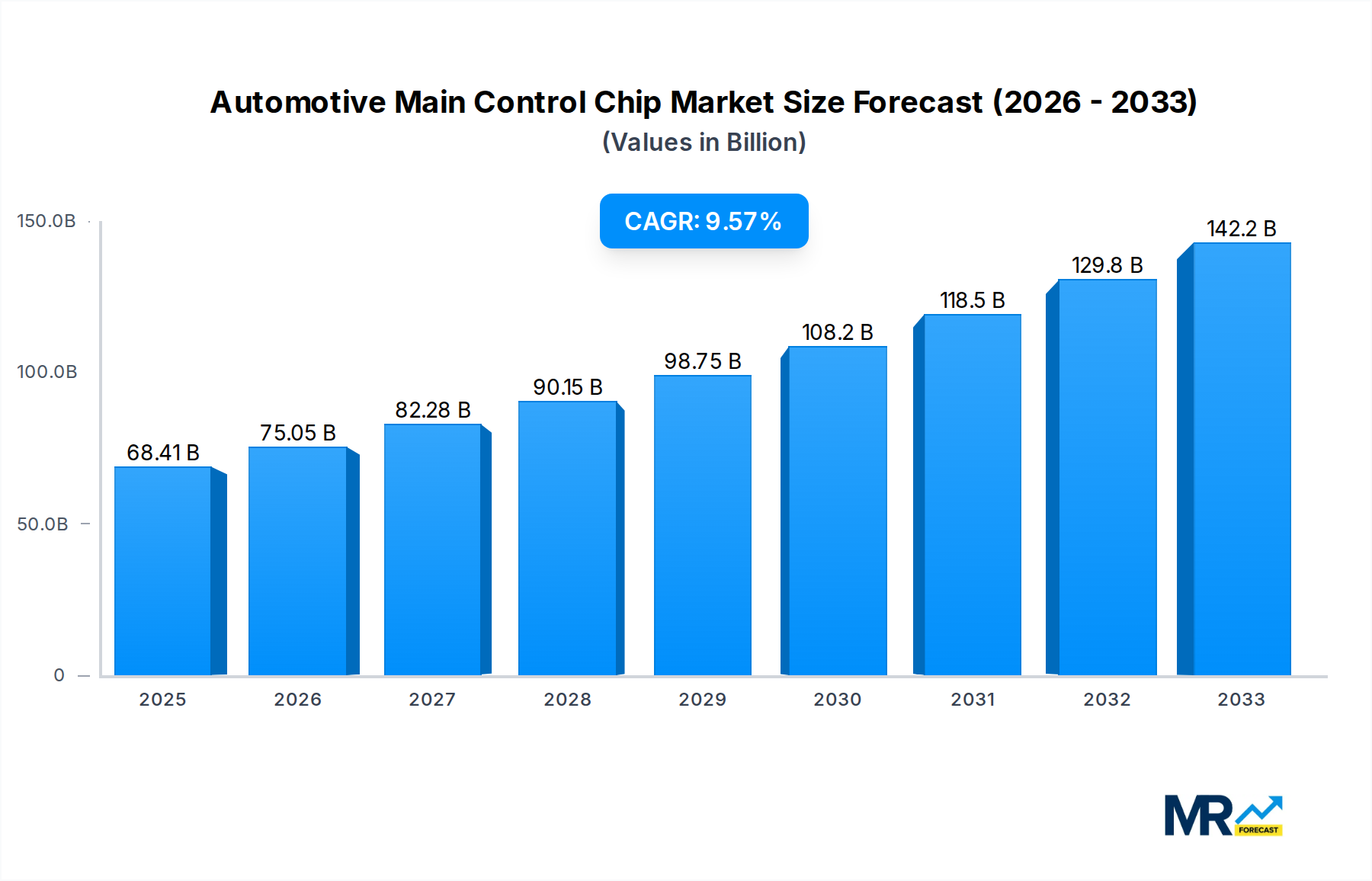

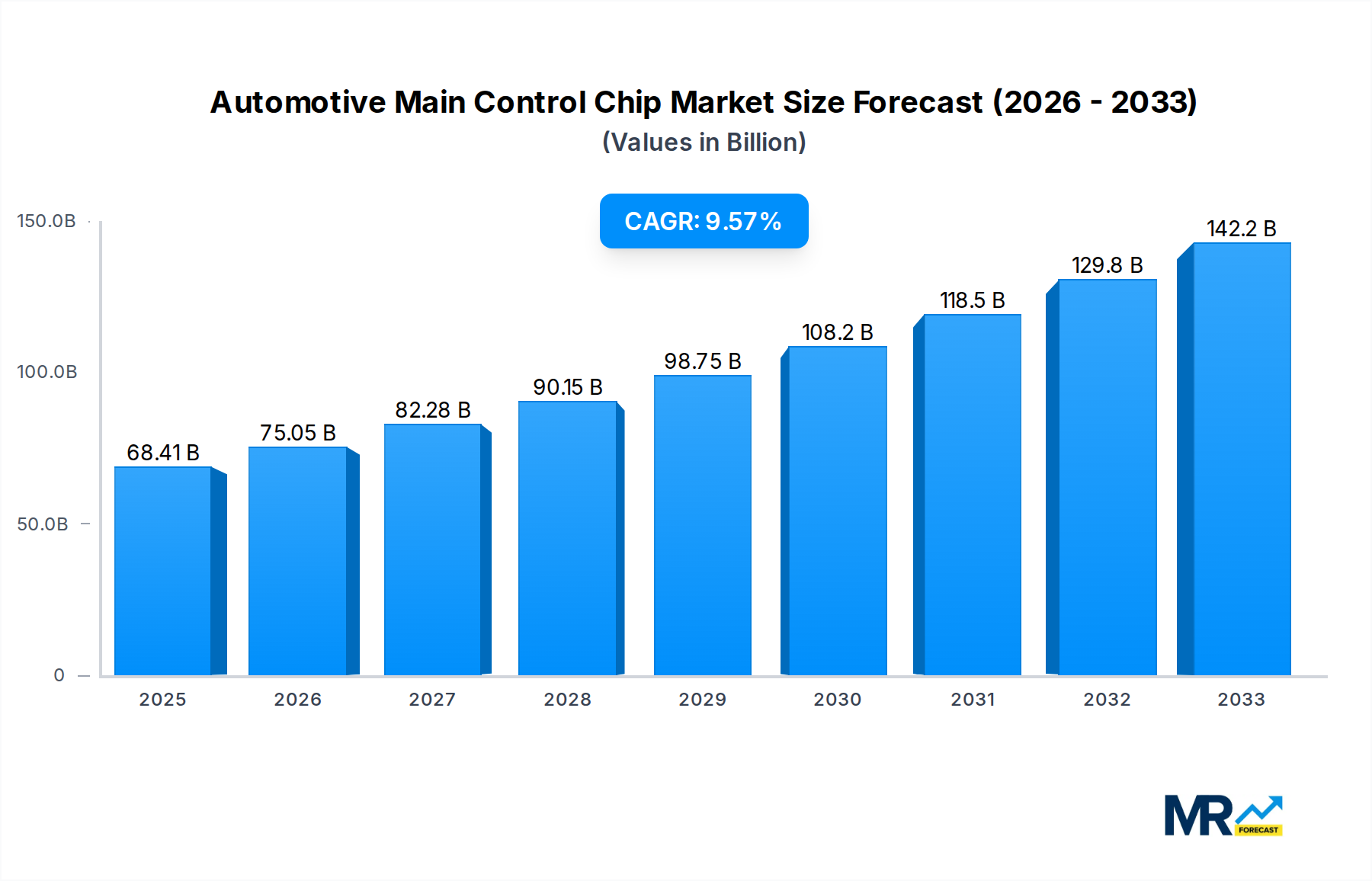

The global automotive main control chip market is projected for substantial growth, reaching an estimated USD 68.41 billion by 2025, with a robust Compound Annual Growth Rate (CAGR) of 9.49% expected to propel it through the forecast period ending in 2033. This expansion is primarily driven by the escalating demand for advanced in-car technologies and the rapid evolution of the automotive industry towards electrification and autonomous driving. Key growth drivers include the increasing sophistication of smart cockpits, which offer enhanced infotainment, connectivity, and user experience features, and the widespread adoption of Advanced Driver-Assistance Systems (ADAS) aimed at improving vehicle safety and driving convenience. The integration of powerful computing chips and dedicated control chips is fundamental to enabling these complex functionalities, making them indispensable components in modern vehicles. The market is segmented into Computing Chip and Control Chip types, with applications spanning Smart Cockpit, ADAS, and other emerging automotive systems.

The competitive landscape is characterized by the presence of major global players such as Infineon, NXP, Renesas, STMicroelectronics, Texas Instruments, Samsung Electronics, and Qualcomm, alongside emerging innovators like Beijing Horizon Robotics Technology and Black Sesame Technologies. These companies are heavily investing in research and development to deliver next-generation semiconductor solutions that meet the stringent performance, safety, and power efficiency requirements of the automotive sector. Emerging trends like the development of highly integrated system-on-chips (SoCs) and the increasing focus on cybersecurity within vehicles are shaping product roadmaps. However, the market faces certain restraints, including the high cost of R&D for advanced semiconductor technologies, the complexities of automotive supply chains, and evolving regulatory frameworks that necessitate continuous adaptation. Despite these challenges, the transformative nature of automotive technology ensures a dynamic and promising future for the main control chip market.

This report offers a comprehensive analysis of the global Automotive Main Control Chip market, delving into its intricate dynamics from 2019 to 2033. With a Base Year of 2025, the report provides granular insights for the Estimated Year of 2025 and projects future trajectories through a detailed Forecast Period of 2025-2033, building upon the Historical Period of 2019-2024. The market is experiencing an unprecedented surge, projected to exceed USD 50 billion by the end of the forecast period, driven by an insatiable demand for advanced automotive features.

XXX Automotive Main Control Chip Trends are rapidly evolving, reflecting the profound transformation underway in the automotive industry. The proliferation of connected and autonomous vehicles is fundamentally reshaping the demand for sophisticated semiconductor solutions. In the Base Year of 2025, the market is characterized by a significant shift towards high-performance computing chips designed to process vast amounts of sensor data, enabling advanced driver-assistance systems (ADAS) and paving the way for fully autonomous driving. Simultaneously, the demand for specialized control chips that manage everything from powertrain efficiency to in-car infotainment is also escalating. The Smart Cockpit segment, in particular, is emerging as a major trendsetter, with consumers expecting increasingly immersive and personalized digital experiences within their vehicles. This trend necessitates advanced chips capable of powering high-resolution displays, seamless connectivity, and sophisticated user interfaces. The ADAS segment, while already a significant driver, continues to expand with the integration of more complex functionalities like advanced sensor fusion, predictive braking, and sophisticated navigation systems. The projected market size, anticipated to reach well over USD 40 billion in the forecast period, underscores the critical role of these chips in realizing the automotive vision of the future. By 2033, we anticipate a market value potentially exceeding USD 70 billion, indicating a compound annual growth rate (CAGR) of over 15%. This explosive growth is driven by the increasing complexity of vehicle electronics, the growing adoption of electric vehicles (EVs) which often feature more advanced digital architectures, and the relentless pursuit of enhanced safety, comfort, and entertainment features. The integration of artificial intelligence (AI) and machine learning (ML) capabilities directly onto these main control chips is also becoming a defining trend, enabling real-time decision-making and predictive functionalities that are crucial for advanced automotive applications. Furthermore, the ongoing miniaturization and increased power efficiency of these chips are critical enablers for their widespread adoption across various vehicle segments, from entry-level cars to luxury autonomous vehicles. The increasing regulatory push for enhanced vehicle safety and emissions reduction further bolsters the demand for these sophisticated control units.

The automotive main control chip market is experiencing robust growth fueled by a confluence of powerful drivers. Foremost among these is the accelerating adoption of advanced driver-assistance systems (ADAS). Features such as adaptive cruise control, lane-keeping assist, automatic emergency braking, and surround-view cameras are becoming standard in new vehicles, directly increasing the demand for sophisticated processing capabilities. The global push towards autonomous driving technology is an even more significant catalyst, requiring immense computational power to process data from multiple sensors (cameras, LiDAR, radar) and make real-time driving decisions. As the industry moves towards higher levels of autonomy, the complexity and processing needs of these main control chips will only intensify. Furthermore, the ever-increasing consumer demand for in-car connectivity and smart cockpit experiences is a major driving force. Infotainment systems are evolving into comprehensive digital hubs, supporting advanced navigation, entertainment streaming, voice assistants, and seamless smartphone integration. This necessitates powerful processors capable of handling high-resolution displays, complex graphics, and multiple applications simultaneously. The growth of the electric vehicle (EV) market also plays a crucial role. EVs typically feature more advanced electronic architectures compared to their internal combustion engine counterparts, often incorporating dedicated domain controllers for battery management, powertrain control, and advanced charging functionalities. This intricate integration of electronics within EVs directly translates to higher demand for specialized and powerful main control chips. The ongoing trend of software-defined vehicles, where functionalities are increasingly determined by software rather than hardware, also means that the central computing power provided by these chips is becoming paramount for over-the-air updates, feature enhancements, and overall vehicle intelligence.

Despite the promising growth trajectory, the automotive main control chip market faces several significant challenges and restraints. The complex and lengthy automotive qualification process is a major hurdle. Semiconductor components intended for automotive use must meet extremely stringent reliability, safety, and performance standards, often requiring years of rigorous testing and validation. This extended development cycle can slow down the introduction of new chip technologies. Supply chain volatility and geopolitical tensions have also emerged as critical concerns. The automotive industry has been heavily impacted by chip shortages in recent years, exacerbated by factors such as increased demand from other sectors, manufacturing disruptions, and trade disputes. This has led to production delays and increased component costs. The rising cost of advanced semiconductor manufacturing poses another restraint. The development and production of leading-edge chips require substantial capital investment in advanced fabrication facilities and research and development. This can make it challenging for smaller players to compete and can lead to higher chip prices, potentially impacting the affordability of advanced automotive features. Cybersecurity threats represent a growing challenge. As vehicles become more connected and reliant on software, they become more vulnerable to cyberattacks. Main control chips must be designed with robust security features to protect against unauthorized access and malicious activities, adding complexity and cost to chip development. Finally, the rapid pace of technological innovation can create obsolescence risks. The automotive industry often has longer product lifecycles than consumer electronics, meaning that chips designed for a particular vehicle model may become outdated before the vehicle reaches the end of its production run, necessitating careful planning and foresight in chip selection.

The ADAS segment is poised to be a dominant force in the automotive main control chip market, both in terms of value and technological advancement. The increasing focus on vehicle safety, driven by regulatory mandates and consumer demand, is the primary propeller for ADAS adoption. As of the Base Year 2025, the market for ADAS chips is estimated to be over USD 15 billion, with projections indicating it will surpass USD 30 billion by 2033. This segment encompasses a wide range of functionalities, from basic parking assistance to sophisticated highway driving assist systems. The core of ADAS lies in the main control chips that act as the brain, processing data from various sensors such as cameras, radar, and LiDAR.

The automotive main control chip industry is experiencing a surge in growth catalysts. The relentless pursuit of enhanced vehicle safety and the increasing adoption of ADAS are paramount, driven by regulatory mandates and consumer demand. The dawn of autonomous driving technology represents a seismic shift, necessitating powerful processors for real-time decision-making. Furthermore, the proliferation of connected car features and sophisticated smart cockpits is transforming the in-cabin experience, demanding more advanced infotainment and HMI solutions. The rapid expansion of the electric vehicle (EV) market also contributes significantly, as EVs typically incorporate more complex electronic architectures and dedicated control units for battery management and powertrain optimization.

This report provides an all-encompassing analysis of the Automotive Main Control Chip market, offering deep insights into its current state and future potential. It meticulously examines the technological advancements, market trends, and evolving consumer demands that are reshaping the automotive landscape. The report delves into the intricate interplay of driving forces, such as the burgeoning ADAS and autonomous driving sectors, alongside the ever-growing consumer appetite for connected and intelligent in-car experiences. Furthermore, it critically assesses the significant challenges and restraints that market participants must navigate, including supply chain complexities and the rigorous automotive qualification processes. With detailed market segmentation, regional analysis, and a comprehensive overview of leading players and their strategic developments, this report equips stakeholders with the knowledge necessary to make informed decisions in this dynamic and rapidly expanding market. The projected market value, exceeding USD 50 billion by the end of the forecast period, underscores the immense opportunities within this critical segment of the automotive industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.1% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.1%.

Key companies in the market include Infineon, NXP, Renesas, STMicroelectronics, Microchip, Texas Instruments, Samsung Electronics, Nuvoton, Silicon Labs, CEC Huada, ON Semiconductor, ROHM, Qualcomm, Intel, Nvidia, Mobileye, MediaTek, Gigadevice Semiconductor, Beijing Horizon Robotics Technology, Telechips, Black Sesame Technologies, Hisilicon, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive Main Control Chip," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Main Control Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.