1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive LED Devices?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Automotive LED Devices

Automotive LED DevicesAutomotive LED Devices by Type (In-car LED Devices, Outdoor LED Devices, World Automotive LED Devices Production ), by Application (Passenger Car, Commercial Vehicle, World Automotive LED Devices Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The global Automotive LED Devices market is poised for significant expansion, projected to reach an estimated value of USD XXX million by 2025, with a robust Compound Annual Growth Rate (CAGR) of XX% anticipated from 2025 to 2033. This growth is primarily fueled by the escalating demand for enhanced vehicle safety features, superior illumination capabilities, and the increasing integration of advanced lighting technologies in both passenger and commercial vehicles. The shift towards energy-efficient and long-lasting LED solutions over traditional lighting systems presents a substantial opportunity for market players. Furthermore, stringent automotive safety regulations worldwide are compelling manufacturers to adopt more sophisticated lighting systems, thereby driving the adoption of automotive LED devices. Innovations in adaptive lighting, matrix LED headlights, and interior ambient lighting are also contributing to this upward trajectory, offering consumers a more personalized and functional driving experience.

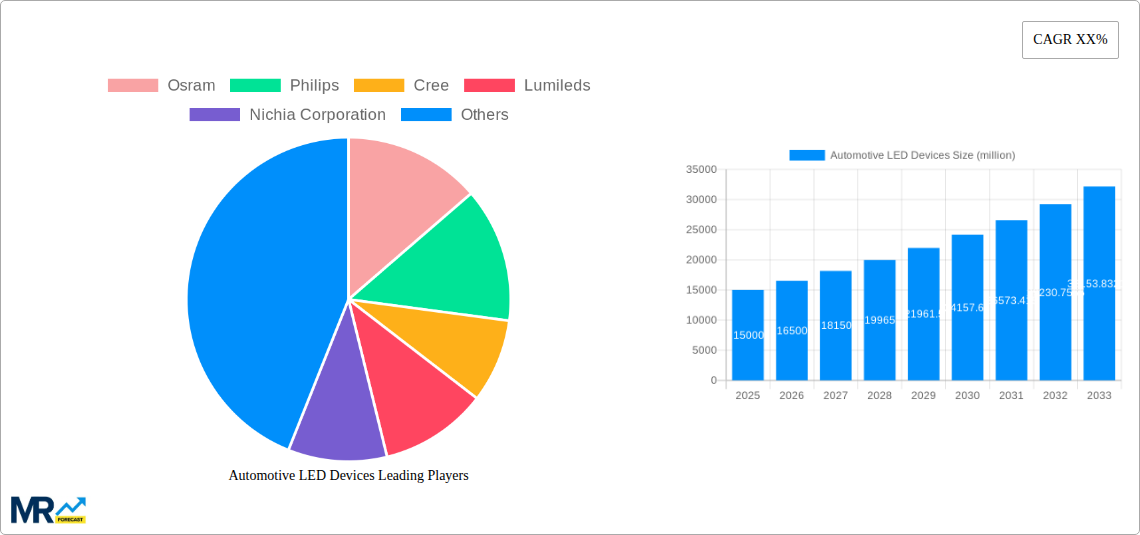

The market is segmented into In-car LED Devices and Outdoor LED Devices, with applications spanning Passenger Cars and Commercial Vehicles. While In-car LED Devices cater to interior illumination, dashboard displays, and other cabin lighting needs, Outdoor LED Devices, encompassing headlights, taillights, and signaling systems, are experiencing a surge in demand due to advancements in exterior lighting technology and safety mandates. Key market drivers include the increasing production of automobiles globally, the growing adoption of electric and hybrid vehicles which often feature advanced LED lighting for aesthetic and functional purposes, and the continuous innovation in LED technology leading to brighter, more durable, and cost-effective solutions. However, the market may face certain restraints such as the initial high cost of advanced LED systems and the complexity of integration, though these are expected to diminish with technological advancements and economies of scale. Prominent companies like Osram, Philips, Cree, Lumileds, and Samsung are at the forefront, investing heavily in research and development to maintain a competitive edge in this dynamic landscape.

Here is a report description on Automotive LED Devices, incorporating your specified details:

The global automotive LED devices market is experiencing a transformative surge, driven by an escalating demand for enhanced safety, fuel efficiency, and sophisticated aesthetic design in vehicles. The study period, spanning from 2019 to 2033, with a base year of 2025, is witnessing a significant evolution from traditional lighting solutions to advanced LED technologies. In the historical period (2019-2024), early adoption focused on premium segments, but the forecast period (2025-2033) indicates a widespread penetration across all vehicle types. The estimated production for 2025 is projected to reach hundreds of millions of units, a figure expected to witness consistent double-digit growth throughout the forecast. This growth is underpinned by the inherent advantages of LEDs, including their longevity, reduced energy consumption, and superior illumination quality, which directly contribute to improved driver visibility and reduced accident rates. Furthermore, the increasing trend of automotive personalization and the desire for distinctive visual signatures are pushing manufacturers to incorporate advanced LED features like adaptive front-lighting systems (AFS), matrix beam headlights, and dynamic turn signals. The integration of LEDs is not confined to exterior lighting; interior cabin lighting is also witnessing a revolution, with ambient lighting, customizable mood lighting, and advanced cockpit displays becoming increasingly prevalent, enhancing the overall passenger experience. The proliferation of electric vehicles (EVs) also plays a crucial role, as their design flexibility and power management systems readily accommodate the integration of energy-efficient LED lighting. The market is also seeing a shift towards intelligent lighting solutions, where LEDs are synchronized with vehicle sensors and external data, enabling features such as adaptive lighting that adjusts beam patterns based on road conditions, traffic, and pedestrian detection. This synergistic integration of hardware and software is redefining automotive illumination, moving beyond mere visibility to active safety and intelligent driver assistance.

Several potent forces are propelling the expansion of the automotive LED devices market. Foremost among these is the relentless pursuit of enhanced vehicle safety. LEDs offer superior brightness and faster response times compared to traditional incandescent bulbs, providing drivers with better visibility in challenging conditions like fog, rain, and darkness. This improved illumination directly translates to reduced reaction times and a lower incidence of accidents. Secondly, the increasing stringency of global automotive regulations mandating improved safety features and fuel efficiency is a significant catalyst. LEDs consume considerably less energy than conventional lighting, contributing to overall fuel economy and, consequently, helping manufacturers meet emission standards. The burgeoning electric vehicle sector is also a major driver; EVs, with their inherent design flexibility and emphasis on energy conservation, are natural adopters of energy-efficient LED lighting. Furthermore, the growing consumer demand for advanced automotive features, including customizable ambient lighting, dynamic turn signals, and sophisticated headlight designs, is pushing manufacturers to invest heavily in LED technology. The aesthetic appeal and customization possibilities offered by LEDs allow for unique brand identities and enhanced user experiences, making them a key differentiator in a competitive market.

Despite the robust growth trajectory, the automotive LED devices market encounters certain challenges and restraints. A primary hurdle is the higher initial cost of LED components compared to traditional lighting solutions, which can impact the overall vehicle price, especially in entry-level segments. While prices are decreasing, this remains a factor for cost-conscious manufacturers and consumers. Another significant challenge is the complexity of integration and thermal management. LEDs generate heat, and managing this heat effectively within the confined spaces of a vehicle is crucial for their longevity and performance. This requires sophisticated thermal management systems, adding to design complexity and cost. Stringent performance and reliability standards in the automotive industry also pose a challenge. LED devices must withstand extreme temperature fluctuations, vibrations, and prolonged operational cycles, demanding rigorous testing and high-quality manufacturing processes. Furthermore, the rapid pace of technological advancement in LED technology can lead to obsolescence concerns for existing designs and necessitate continuous investment in research and development for manufacturers. Supply chain disruptions and the availability of raw materials, particularly specialized semiconductors and phosphors, can also present temporary restraints, impacting production volumes and pricing.

World Automotive LED Devices Production and the Passenger Car application segment are poised to exhibit significant dominance within the global Automotive LED Devices market during the study period (2019-2033), with the base year of 2025 serving as a pivotal point for estimating future trends.

Dominating Segments and Regions:

World Automotive LED Devices Production: This segment, encompassing the overall global manufacturing output of automotive LED devices, is expected to lead the market by volume. The estimated production in 2025 is projected to be in the hundreds of millions of units, a figure that will see substantial expansion throughout the forecast period (2025-2033). This overarching dominance is a direct reflection of the widespread adoption of LED technology across all automotive applications and regions. The continuous drive for innovation and cost reduction in LED manufacturing, coupled with the increasing production of vehicles globally, underpins this segment's leadership. Companies like Osram, Philips, Cree, Lumileds, Nichia Corporation, and Samsung are major contributors to this global production, alongside emerging players from Asia. The sheer scale of vehicle manufacturing, particularly in Asia-Pacific, North America, and Europe, ensures that the total production volume of automotive LED devices remains a leading market indicator.

Application: Passenger Car: Within the application segments, Passenger Cars are expected to be the largest revenue generator and volume driver. In 2025, the demand for LED devices in passenger cars is estimated to be in the hundreds of millions of units. This dominance is attributed to several factors:

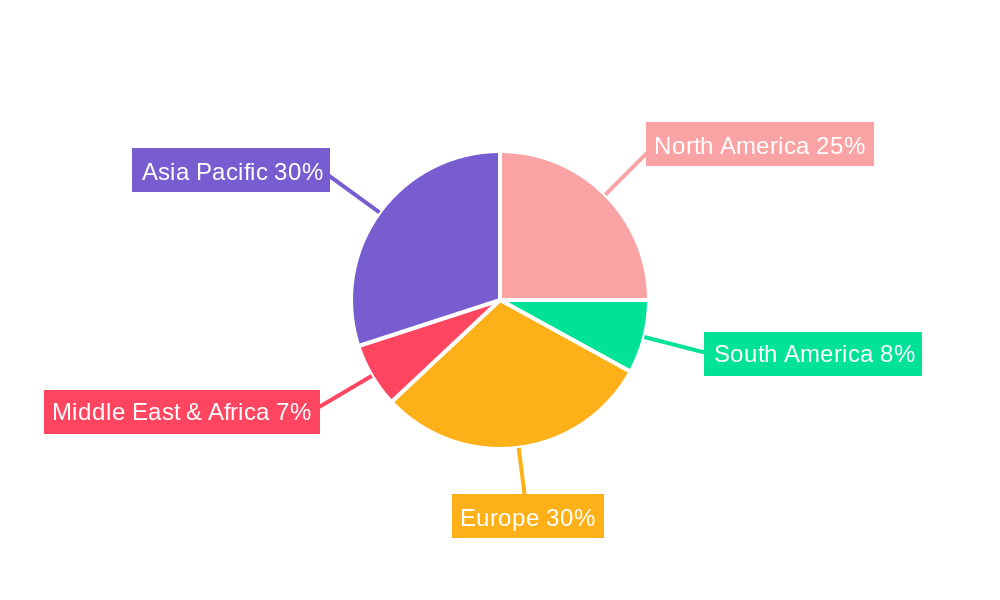

Key Regions/Countries:

The synergistic growth of high production volumes in the World Automotive LED Devices Production segment, coupled with the immense demand from the Passenger Car application, primarily driven by leading automotive manufacturing hubs in Asia-Pacific, Europe, and North America, will solidify their dominant positions in the market.

The automotive LED devices industry is propelled by several key growth catalysts. The unwavering focus on enhancing vehicle safety through improved visibility and advanced driver-assistance systems (ADAS) is a primary driver. The increasing adoption of electric vehicles, which benefit from the energy efficiency and design flexibility of LEDs, further fuels demand. Moreover, escalating consumer preferences for sophisticated interior and exterior lighting aesthetics, coupled with the decreasing cost of LED technology, are making these advanced lighting solutions more accessible across vehicle segments. Regulatory mandates for fuel efficiency and reduced emissions also indirectly promote LED adoption due to their lower power consumption.

This comprehensive report on Automotive LED Devices offers an in-depth analysis of the market dynamics from 2019 to 2033, with 2025 as the base year for detailed estimations. It meticulously covers key segments including In-car LED Devices and Outdoor LED Devices, and analyzes production and application trends across Passenger Cars and Commercial Vehicles. The report delves into the intricate driving forces, challenges, and restraints shaping the industry, providing actionable insights. It highlights key regions and segments poised for significant growth, alongside crucial industry developments and a detailed overview of leading players. The report aims to equip stakeholders with a thorough understanding of market trends, opportunities, and the competitive landscape for informed strategic decision-making.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Osram, Philips, Cree, Lumileds, Nichia Corporation, Koito Manufacturing Co., Ltd., Shenzhen Jufei Optoelectronics Co., Ltd., Samsung, Everlight Electronics, Seoul Semiconductor, GE Lighting, Valeo, Hasco VISION Technology Co., Ltd., Magneti Marelli, Stanley, Changzhou Xingyu Automotive Lighting Systems Co., Ltd., Varroc Lighting Systems, Nanning Liaowang AUTOMOTIVE Lamp Co., Ltd., .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive LED Devices," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive LED Devices, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.