1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Intelligent Diagnostic Tools?

The projected CAGR is approximately XX%.

Automotive Intelligent Diagnostic Tools

Automotive Intelligent Diagnostic ToolsAutomotive Intelligent Diagnostic Tools by Type (Diagnostic Platforms, Professional Diagnostics, DIY Diagnostics, World Automotive Intelligent Diagnostic Tools Production ), by Application (Passenger Vehicle, Light Commercial Vehicle, Heavy Commercial Vehicle, World Automotive Intelligent Diagnostic Tools Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

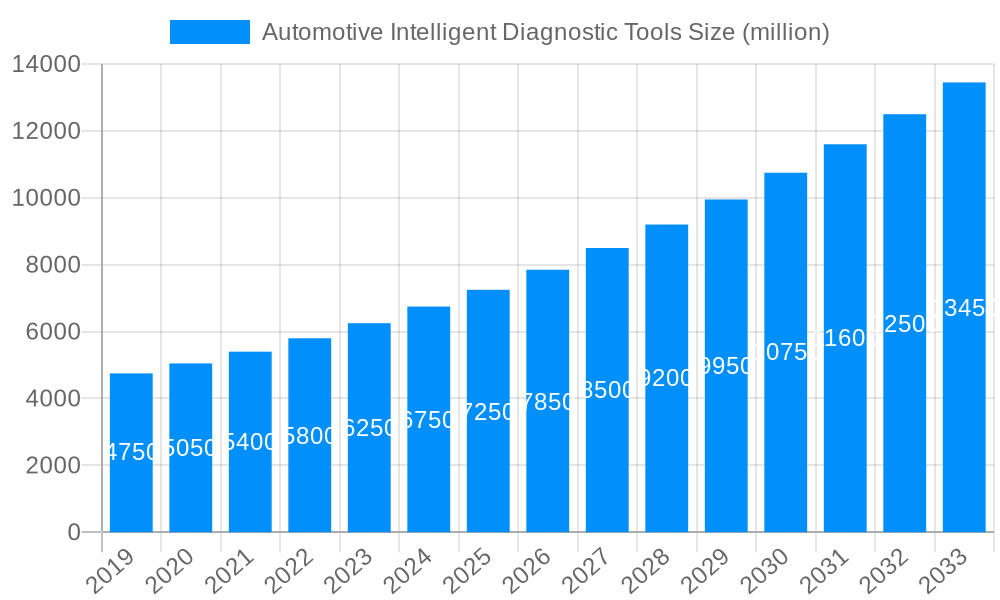

The global Automotive Intelligent Diagnostic Tools market is projected for substantial growth, estimated to reach approximately $7,500 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of around 8.5% anticipated throughout the forecast period extending to 2033. This expansion is primarily fueled by the increasing complexity of modern vehicles, the rapid adoption of advanced automotive technologies such as ADAS (Advanced Driver-Assistance Systems) and electric powertrains, and the growing demand for sophisticated diagnostic solutions. The rising emphasis on vehicle safety, emissions compliance, and efficient maintenance further bolsters market demand. The prevalence of the "right to repair" movement and increasing consumer awareness regarding vehicle health are also significant drivers, pushing the need for accurate and accessible diagnostic tools for both professional mechanics and informed vehicle owners.

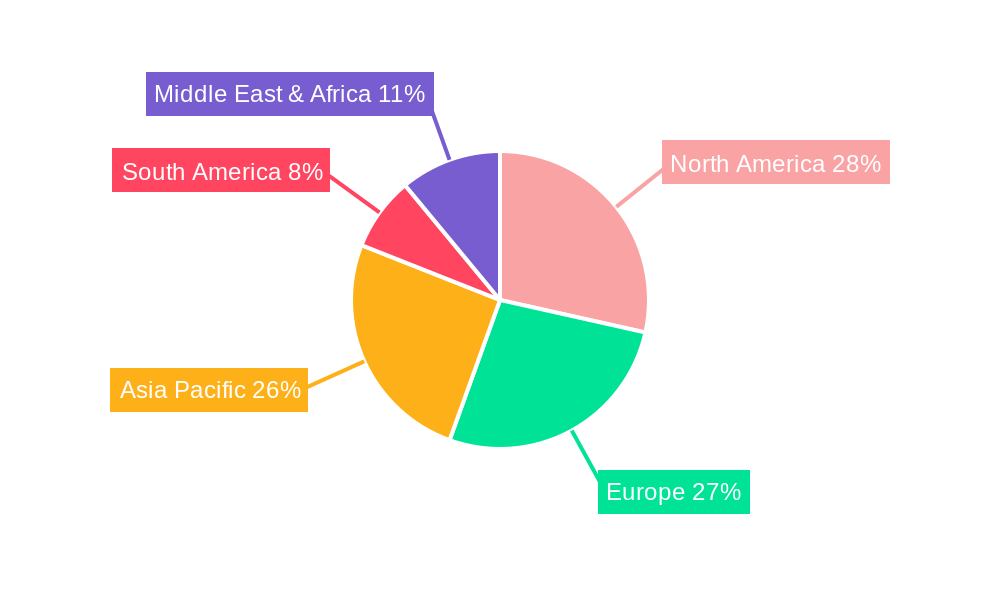

The market segmentation reveals a dynamic landscape. Within diagnostic platforms, professional diagnostics are expected to dominate, owing to their advanced capabilities and crucial role in repair shops. However, DIY diagnostics are poised for significant growth as sophisticated, user-friendly tools become more accessible to the average car owner. Application-wise, passenger vehicles represent the largest segment, given their sheer volume on global roads. Light and heavy commercial vehicles also present substantial opportunities, driven by fleet management needs and the imperative for minimal downtime. Geographically, North America and Europe are leading markets due to their established automotive repair infrastructure and high vehicle parc. However, the Asia Pacific region, particularly China and India, is anticipated to witness the fastest growth, driven by burgeoning automotive production, increasing disposable incomes, and a rapidly expanding vehicle fleet. Key restraints include the high initial cost of some advanced diagnostic equipment and the need for continuous software updates, which can pose challenges for smaller repair shops.

Here's a unique report description on Automotive Intelligent Diagnostic Tools, incorporating your specified elements:

The global automotive intelligent diagnostic tools market is poised for significant expansion, driven by an accelerating technological evolution within the automotive industry. During the study period of 2019-2033, with a base year of 2025, the market is expected to witness a substantial compound annual growth rate (CAGR). This growth is underpinned by the increasing complexity of vehicle electronics, the proliferation of Advanced Driver-Assistance Systems (ADAS), and the burgeoning demand for connected car services. As vehicles become more sophisticated, traditional diagnostic methods are rapidly becoming obsolete, necessitating the adoption of intelligent tools capable of deciphering intricate software and hardware interdependencies. The estimated production volume of automotive intelligent diagnostic tools in 2025 is projected to reach 25.5 million units, a figure anticipated to surge by the end of the forecast period in 2033. This upward trajectory is further fueled by stringent emission regulations and evolving safety standards that mandate more precise and frequent vehicle health monitoring. The shift towards electric vehicles (EVs) and hybrid technologies also presents a unique set of diagnostic challenges and opportunities, requiring specialized tools that can effectively assess battery health, electric motor performance, and integrated power management systems. Furthermore, the increasing adoption of cloud-based diagnostic platforms and artificial intelligence (AI) driven predictive maintenance solutions is revolutionizing how vehicle issues are identified and resolved, moving from reactive repairs to proactive problem prevention. The market's trajectory is also influenced by the growing aftermarket demand for advanced diagnostic capabilities, as vehicle owners and independent repair shops seek to keep pace with dealership-level technology. The historical period from 2019-2024 laid the groundwork for this expansion, marked by initial investments in software development and early adoption of connected diagnostics. The estimated production in the base year of 2025 will serve as a crucial benchmark for future growth projections.

The automotive intelligent diagnostic tools market is propelled by a confluence of powerful driving forces. Foremost among these is the escalating technological sophistication of modern vehicles. The integration of complex electronic control units (ECUs), sophisticated sensor networks, and advanced software platforms for functions ranging from infotainment to autonomous driving creates a diagnostic landscape that demands intelligent, software-driven solutions. The rapid adoption of Advanced Driver-Assistance Systems (ADAS) like adaptive cruise control, lane-keeping assist, and automatic emergency braking necessitates specialized diagnostic tools to calibrate, troubleshoot, and maintain these safety-critical systems. Furthermore, the global push towards electrification and the increasing market share of electric vehicles (EVs) and hybrid electric vehicles (HEVs) introduce entirely new diagnostic paradigms, focusing on battery management systems, electric powertrain components, and high-voltage systems. Stringent government regulations concerning vehicle emissions and safety standards also play a pivotal role, compelling manufacturers and repair shops to invest in diagnostic tools that can accurately assess compliance and ensure vehicle performance meets regulatory requirements. The growing trend of "right to repair" initiatives and the increasing consumer demand for transparency and efficiency in vehicle maintenance are also fueling the adoption of advanced diagnostic tools by independent repair shops and DIY enthusiasts. Finally, the burgeoning aftermarket sector, eager to access dealership-level diagnostic capabilities, contributes significantly to the market's expansion.

Despite the robust growth prospects, the automotive intelligent diagnostic tools market faces several significant challenges and restraints that could temper its trajectory. A primary hurdle is the escalating cost of developing and updating these sophisticated tools. The rapid pace of automotive innovation, particularly in software and AI, necessitates continuous research and development, leading to higher product prices that can be a barrier for smaller repair shops and individual technicians. The fragmentation of the automotive market, with numerous vehicle manufacturers and diverse proprietary diagnostic protocols, complicates the development of universal diagnostic solutions, often requiring specialized tools for specific brands or platforms. Cybersecurity concerns also loom large; as diagnostic tools become increasingly connected and reliant on software updates, they become potential targets for cyberattacks, threatening data integrity and vehicle security. The need for continuous training and upskilling of technicians to effectively utilize these advanced tools presents another challenge, as the complexity of intelligent diagnostics requires a more technically proficient workforce. Furthermore, the rapid obsolescence of existing diagnostic hardware and software due to frequent vehicle model updates creates an ongoing investment burden for users, limiting widespread adoption in some segments. The global supply chain disruptions, which have impacted various industries, can also affect the availability of key components and the timely delivery of these diagnostic solutions.

The North America region, particularly the United States, is projected to dominate the automotive intelligent diagnostic tools market. This dominance is attributed to several interconnected factors. The region boasts the highest adoption rate of advanced automotive technologies, including a significant concentration of vehicles equipped with ADAS features and a burgeoning EV market. The strong regulatory environment, emphasizing vehicle safety and emissions, further necessitates the widespread use of sophisticated diagnostic equipment. Furthermore, North America has a well-established and technologically advanced aftermarket service sector, with independent repair shops actively investing in state-of-the-art tools to compete with dealerships. The high disposable income and consumer willingness to spend on vehicle maintenance and performance also contribute to the market's strength.

Within the segments, Professional Diagnostics is expected to be the leading segment in terms of both market share and growth. This is directly driven by the increasing complexity of modern vehicles, which often require specialized knowledge and equipment beyond the capabilities of basic DIY tools. Professional diagnostic platforms are essential for dealerships, independent repair shops, and fleet maintenance operations to accurately identify and resolve issues in passenger vehicles, light commercial vehicles, and heavy commercial vehicles. The need for efficient and precise troubleshooting, coupled with the growing demand for software updates and recalibrations for ADAS and other advanced systems, makes professional diagnostic tools indispensable.

World Automotive Intelligent Diagnostic Tools Production will also be a key segment to watch, as the manufacturing hubs for these sophisticated devices are concentrated in regions with strong electronics and automotive manufacturing capabilities. Countries like China, which is a major global manufacturing base for automotive components and electronics, are expected to play a significant role in the production volume. The availability of skilled labor, advanced manufacturing infrastructure, and government support for technological innovation positions these regions to be critical players in meeting the global demand. The estimated production of 25.5 million units in 2025 signifies the scale of this manufacturing segment. The interplay between technological innovation in North America and manufacturing prowess in regions like Asia-Pacific will shape the global landscape of automotive intelligent diagnostic tools.

The growth of the automotive intelligent diagnostic tools industry is significantly catalyzed by the accelerating pace of technological advancements in vehicles. The widespread integration of sophisticated software and hardware, including ADAS, autonomous driving features, and electric powertrains, creates a constant need for advanced diagnostic solutions. The increasing interconnectedness of vehicles and the rise of IoT in automotive applications further fuel this demand, requiring tools that can monitor and diagnose networked systems. Additionally, stringent government regulations regarding vehicle emissions, safety, and mandatory diagnostics are a powerful growth catalyst. The growing aftermarket for vehicle servicing and the "right to repair" movement empower independent workshops to invest in sophisticated tools, expanding the market beyond dealerships.

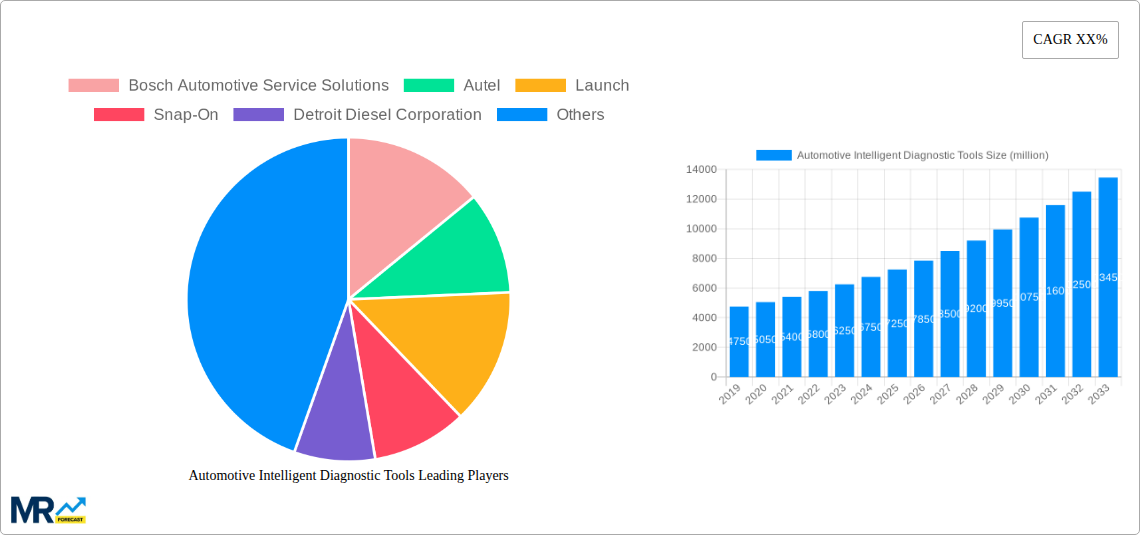

This comprehensive report provides an in-depth analysis of the global automotive intelligent diagnostic tools market, offering valuable insights for stakeholders across the automotive ecosystem. The study delves into market segmentation by Type (Diagnostic Platforms, Professional Diagnostics, DIY Diagnostics), Application (Passenger Vehicle, Light Commercial Vehicle, Heavy Commercial Vehicle), and World Automotive Intelligent Diagnostic Tools Production, analyzing the dynamics and growth potential of each. It meticulously examines the industry developments and trends from the historical period of 2019-2024, establishing a robust foundation for the forecast period of 2025-2033. The report highlights key market drivers, such as the increasing complexity of vehicle electronics and the proliferation of ADAS, while also addressing critical challenges like cybersecurity and the need for skilled technicians. Detailed analysis of leading players, including Bosch Automotive Service Solutions, Autel, and Snap-On, provides a competitive landscape overview. With detailed market sizing and projections, the report aims to equip businesses with the strategic intelligence needed to navigate this dynamic and rapidly evolving sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Bosch Automotive Service Solutions, Autel, Launch, Snap-On, Detroit Diesel Corporation, ANCEL, OTC Tools, Innova Electronics, Vector, AVL Ditest, MAHLE, Danlaw, Hella Gutmann, Konnwei, FOXWELL, AUTOOL, Topdon, BlueDriver, Autodiag Technology, Scangauge, Geotab, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive Intelligent Diagnostic Tools," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Intelligent Diagnostic Tools, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.