1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Instrument Meter?

The projected CAGR is approximately 7.1%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Automotive Instrument Meter

Automotive Instrument MeterAutomotive Instrument Meter by Type (Analogue Instrument Meter, Digital Instrument Meter, Others), by Application (Passenger Cars, Commercial Vehicles), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

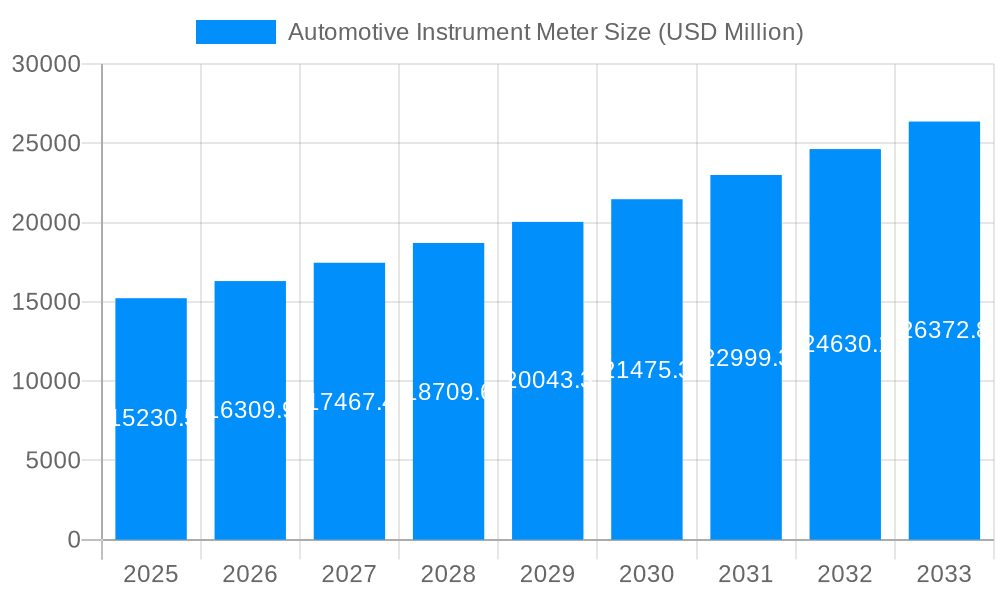

The global automotive instrument meter market is poised for robust growth, projected to reach a significant valuation by 2033, driven by a steady Compound Annual Growth Rate (CAGR) of 7.1%. This expansion is fueled by the increasing demand for advanced vehicle features and sophisticated driver information systems. The market is segmented by type into Analogue Instrument Meters, Digital Instrument Meters, and Others. While analogue meters retain a presence, the trend is overwhelmingly towards digital instrument clusters, offering enhanced functionality, customization, and integration with modern automotive electronics. The "Others" category likely encompasses hybrid solutions and emerging technologies.

Application-wise, the market is primarily driven by Passenger Cars and Commercial Vehicles. The passenger car segment benefits from consumer expectations for premium features and enhanced user experience, while commercial vehicles are increasingly equipped with advanced telematics and driver monitoring systems, further boosting demand for sophisticated instrument clusters. Key market players like Bosch, Denso, and Nippon Seiki are at the forefront, investing in R&D to develop next-generation digital clusters that integrate with advanced driver-assistance systems (ADAS) and infotainment platforms. Regional dynamics indicate a strong presence and growth potential in Asia Pacific, particularly China and Japan, owing to their massive automotive manufacturing bases and rapid adoption of new technologies. North America and Europe also represent significant markets, driven by stringent safety regulations and a high consumer preference for advanced in-car technology. The market's growth trajectory suggests a continued shift towards fully digital and highly integrated instrument meter solutions, with innovation in display technology and connectivity being paramount.

The projected market size of $15,230.5 million (in value units of millions) as of 2025 is expected to witness substantial growth over the forecast period. This upward trend is supported by the inherent demand for advanced vehicle diagnostics, driver safety features, and a more immersive in-car experience. The increasing complexity of modern vehicles, with integrated ADAS and connectivity features, necessitates sophisticated instrument clusters capable of displaying a wide array of information clearly and intuitively. This complexity also presents opportunities for innovation in user interface design and data visualization. While the market is generally robust, potential restraints could include the high cost of advanced digital instrument clusters, which might slow adoption in price-sensitive segments or regions. However, economies of scale and technological advancements are expected to mitigate these concerns over time. Emerging trends point towards augmented reality (AR) integration in instrument meters, providing drivers with even more contextual and intuitive information, further solidifying the market's growth potential and its critical role in the evolving automotive landscape.

This report offers an in-depth analysis of the global Automotive Instrument Meter market, providing a thorough understanding of its current landscape and future trajectory. The study encompasses a detailed examination of market trends, driving forces, challenges, and regional dynamics across the Study Period of 2019-2033, with a Base Year of 2025 and an Estimated Year also set at 2025, followed by a robust Forecast Period from 2025-2033. The Historical Period, from 2019-2024, is also meticulously reviewed. The report delves into the market size, projected to reach several million units, segmented by type (Analogue, Digital, and Others) and application (Passenger Cars, Commercial Vehicles, and Industry). Key players, including Bosch, Denso, Nippon Seiki, and Yazaki, are profiled with their contributions and strategies highlighted. Furthermore, significant technological advancements and market developments are identified and analyzed to offer actionable insights for stakeholders. This comprehensive report is designed to equip industry participants with the knowledge needed to navigate the evolving Automotive Instrument Meter sector and capitalize on emerging opportunities.

The global Automotive Instrument Meter market is undergoing a profound transformation, driven by an escalating demand for advanced in-cabin technologies and enhanced driver experiences. XXX The historical period from 2019-2024 witnessed a gradual shift from purely functional analog displays to more sophisticated digital interfaces, reflecting the increasing integration of infotainment and connectivity features within vehicles. As we move through the Base Year of 2025 and into the Forecast Period of 2025-2033, the dominance of Digital Instrument Meters is expected to accelerate significantly. This trend is primarily fueled by the automotive industry's pursuit of greater customization, real-time data delivery, and the seamless integration of advanced driver-assistance systems (ADAS). Consumers are increasingly seeking personalized driving environments, where instrument clusters can adapt to their preferences, display critical safety information intuitively, and offer a rich media experience. The rise of autonomous driving technologies further accentuates this trend, necessitating advanced displays capable of conveying complex operational status and predictive information to the driver. Analogue meters, while still holding a niche in certain luxury or classic vehicle segments, are projected to see a declining market share. The "Others" category, which likely encompasses hybrid displays and emerging concepts, is anticipated to witness moderate growth as manufacturers experiment with innovative display solutions. The Passenger Cars segment will continue to be the primary volume driver, given its larger production numbers and a quicker adoption rate of new technologies. However, Commercial Vehicles are also expected to see an uptick in digital instrument adoption, driven by the need for enhanced fleet management, driver productivity tools, and improved safety features in demanding operational environments. The industry segment's influence will remain relatively smaller compared to the automotive sectors. The market's overall growth trajectory is robust, with projected unit sales in the millions, underscoring the critical role instrument meters play in modern vehicle design and functionality.

The automotive instrument meter market is experiencing significant momentum driven by a confluence of technological advancements and evolving consumer expectations. The relentless pursuit of enhanced driver experience and safety is a primary catalyst. As vehicles become more sophisticated with the integration of advanced driver-assistance systems (ADAS), connected car technologies, and advanced infotainment, the instrument cluster has evolved from a simple display of speed and RPM to a central hub of information. This evolution necessitates the adoption of digital instrument meters that can present complex data in an intuitive, customizable, and visually engaging manner. The increasing focus on vehicle personalization allows drivers to tailor their display preferences, further boosting the demand for digital solutions. Furthermore, the rapid development and increasing affordability of display technologies, such as high-resolution LCDs and OLED panels, are making advanced instrument clusters a more viable option for a wider range of vehicle segments. The global shift towards electric vehicles (EVs) also plays a crucial role. EVs require different types of information to be displayed, such as battery status, charging levels, and range optimization, which are best conveyed through dynamic digital interfaces. The competitive landscape among automakers, striving to differentiate their offerings with cutting-edge in-cabin technology, further accelerates the adoption of advanced instrument meters.

Despite the promising growth trajectory, the automotive instrument meter market faces several challenges and restraints that could impede its full potential. One of the most significant hurdles is the high cost associated with advanced digital instrument clusters. The sophisticated hardware, including high-resolution displays, powerful processors, and complex software, can substantially increase the overall cost of a vehicle, making it a premium feature rather than a standard offering, especially in entry-level segments. This cost sensitivity can limit the adoption rate, particularly in price-sensitive markets. Furthermore, the complexity of integrating these advanced systems into existing vehicle architectures presents a considerable challenge for automakers and suppliers. Ensuring seamless communication between various ECUs (Electronic Control Units), software compatibility, and cybersecurity measures requires substantial investment in research and development and rigorous testing procedures. The evolving regulatory landscape, particularly concerning data privacy and cybersecurity, adds another layer of complexity. Manufacturers must ensure their instrument meter systems comply with increasingly stringent regulations, which can necessitate costly redesigns and updates. The rapid pace of technological change also poses a challenge. Keeping up with the latest advancements in display technology, processing power, and software functionalities requires continuous innovation, which can be resource-intensive. Finally, the potential for driver distraction due to overly complex or information-rich displays is a growing concern that needs careful consideration in the design and implementation of automotive instrument meters.

The Digital Instrument Meter segment, particularly within the Passenger Cars application, is poised to dominate the global Automotive Instrument Meter market throughout the Study Period of 2019-2033, with a strong emphasis on key regions like Asia Pacific, particularly China, and North America.

Dominance of Digital Instrument Meters: The shift from traditional analogue displays to sophisticated digital instrument clusters is a defining trend. This segment's dominance is driven by the increasing demand for advanced features such as customizable layouts, real-time data visualization for ADAS (Advanced Driver-Assistance Systems), integrated navigation, and enhanced infotainment connectivity. As technology costs decrease and computational power increases, digital clusters become more accessible across vehicle segments, moving beyond luxury vehicles into mainstream passenger cars. The ability to dynamically display critical information like battery status, charging levels, and range optimization further fuels their adoption in the growing electric vehicle market, a significant sub-segment within passenger cars.

Passenger Cars as the Primary Application: Passenger cars represent the largest and most dynamic application segment for automotive instrument meters. Their sheer volume of production globally, coupled with a quicker adoption cycle for new technologies, makes them the primary driver of market growth. Consumers in this segment are increasingly prioritizing in-cabin experience, seeking modern, tech-forward features that enhance comfort, convenience, and safety. The trend towards digitalization is directly reflected in the demand for advanced digital instrument clusters within passenger vehicles.

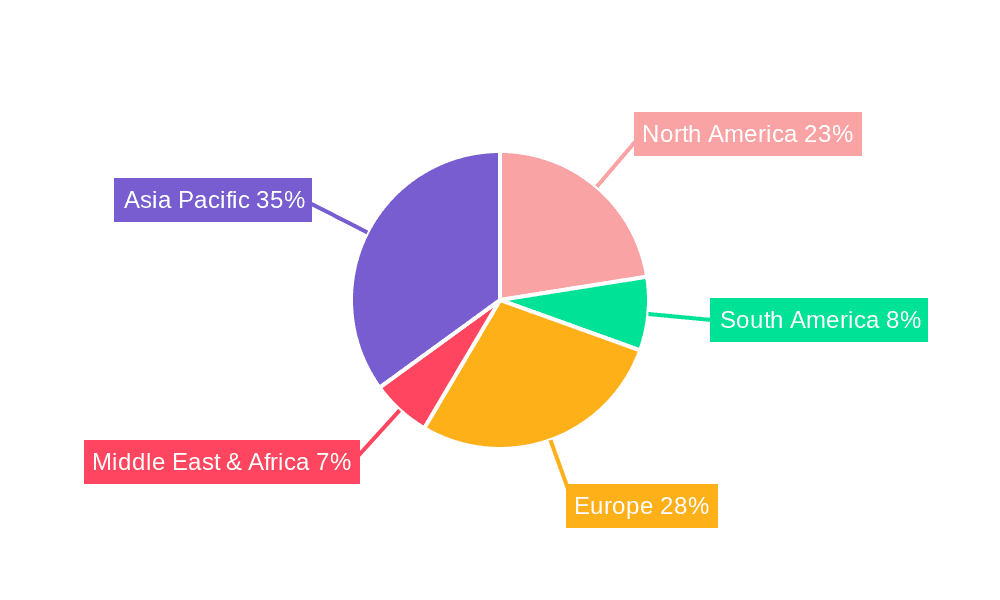

Asia Pacific (Especially China) as a Dominant Region: The Asia Pacific region, spearheaded by China, is expected to lead the automotive instrument meter market. China's position as the world's largest automotive market, coupled with its aggressive push towards electric vehicle adoption and technological innovation, makes it a key growth engine. The presence of major Chinese automotive manufacturers and a robust ecosystem of automotive component suppliers, including companies like Dongfeng Motor Parts And Components Group and Shanghai INESA Auto Electronics System, significantly contributes to this regional dominance. Government initiatives promoting smart mobility and the rapid urbanization of developing economies within the region further bolster demand for advanced automotive technologies, including sophisticated instrument clusters. The region also benefits from strong manufacturing capabilities and a large consumer base receptive to new technological trends.

North America as a Strong Contributor: North America, particularly the United States, also represents a significant market for automotive instrument meters. The region has a high consumer propensity for advanced vehicle features and a strong presence of luxury and premium automotive brands that have historically been early adopters of sophisticated in-cabin technologies. The ongoing development and integration of autonomous driving features, which require advanced display capabilities, are also a major factor driving demand for digital instrument clusters in this region. The robust aftermarket for vehicle upgrades and the focus on safety features further contribute to the market's strength in North America. The presence of global automotive giants like Bosch and Magneti Marelli, with significant operations in the region, also solidifies its importance.

The synergy between the expanding digital instrument meter segment, the colossal passenger car market, and the dynamic growth in key regions like Asia Pacific and North America creates a powerful force that will shape the future of the automotive instrument meter industry. The "Others" segment within types and "Commercial Vehicles" within applications will see steady growth but are unlikely to match the dominance of digital instrument meters in passenger cars in the foreseeable future.

The automotive instrument meter industry is fueled by several key growth catalysts. The accelerating adoption of Advanced Driver-Assistance Systems (ADAS) and the looming advent of autonomous driving necessitate sophisticated displays that can convey complex safety information intuitively, driving the demand for advanced digital instrument clusters. The global surge in Electric Vehicle (EV) production introduces new display requirements, such as real-time battery status and range optimization, which are best met by digital solutions. Furthermore, the increasing consumer desire for personalized in-cabin experiences, seamless connectivity, and integrated infotainment systems empowers the instrument cluster to become a central interface, boosting demand for its advanced functionalities. Lastly, the continuous innovation in display technologies, leading to more cost-effective and higher-resolution screens, makes these advanced features accessible to a wider range of vehicle segments.

This report provides a granular and exhaustive examination of the global Automotive Instrument Meter market. It offers critical insights into the market dynamics, including key trends, driving forces, and challenges that will shape the industry landscape. The report meticulously analyzes market segmentation by type (Analogue, Digital, and Others) and application (Passenger Cars, Commercial Vehicles, and Industry), providing precise market size projections in millions of units. Regionally, the report highlights the dominant markets and identifies emerging opportunities. With a comprehensive study period spanning from 2019 to 2033, including a detailed analysis of the historical period (2019-2024), base year (2025), and forecast period (2025-2033), this report equips stakeholders with actionable intelligence for strategic decision-making. It delves into the leading players and their contributions, as well as significant technological developments, ensuring a complete understanding of the sector's evolution.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.1% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 7.1%.

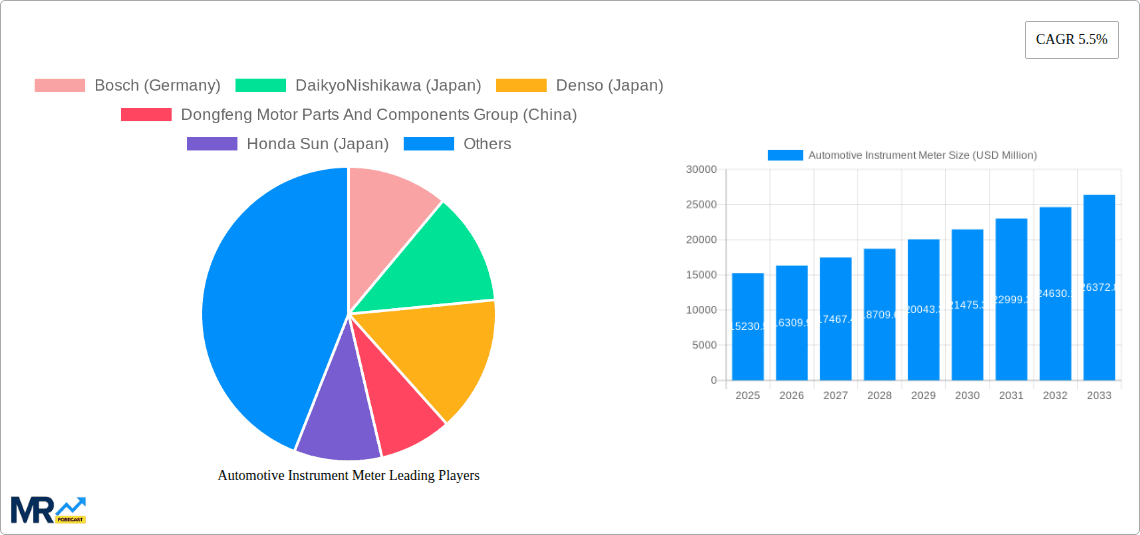

Key companies in the market include Bosch (Germany), DaikyoNishikawa (Japan), Denso (Japan), Dongfeng Motor Parts And Components Group (China), Honda Sun (Japan), Dongguan Jeco Electronics (Japan), Magneti Marelli (Italy), Mitsubishi Electric (Japan), Nippon Seiki (Japan), S&T Motiv (Korea), Shanghai INESA Auto Electronics System (China), Unick (Korea), Yazaki (Japan), .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive Instrument Meter," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Instrument Meter, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.