1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Gear Shifter?

The projected CAGR is approximately 9.3%.

Automotive Gear Shifter

Automotive Gear ShifterAutomotive Gear Shifter by Type (Mechanical Gear Shifter, Electronic Gear Shifter, World Automotive Gear Shifter Production ), by Application (Passenger Vehicle, Commercial Vehicle, World Automotive Gear Shifter Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

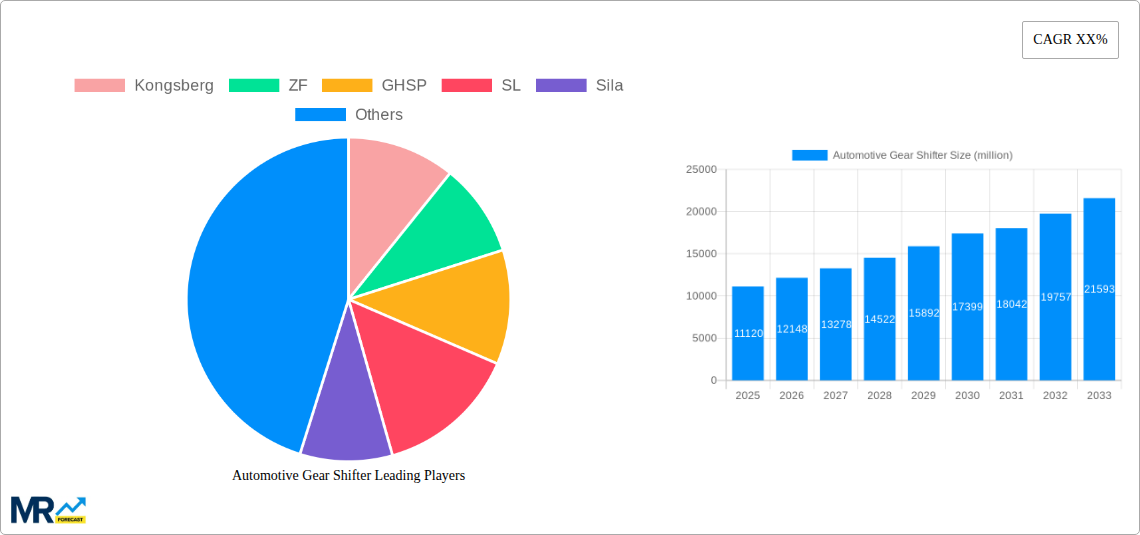

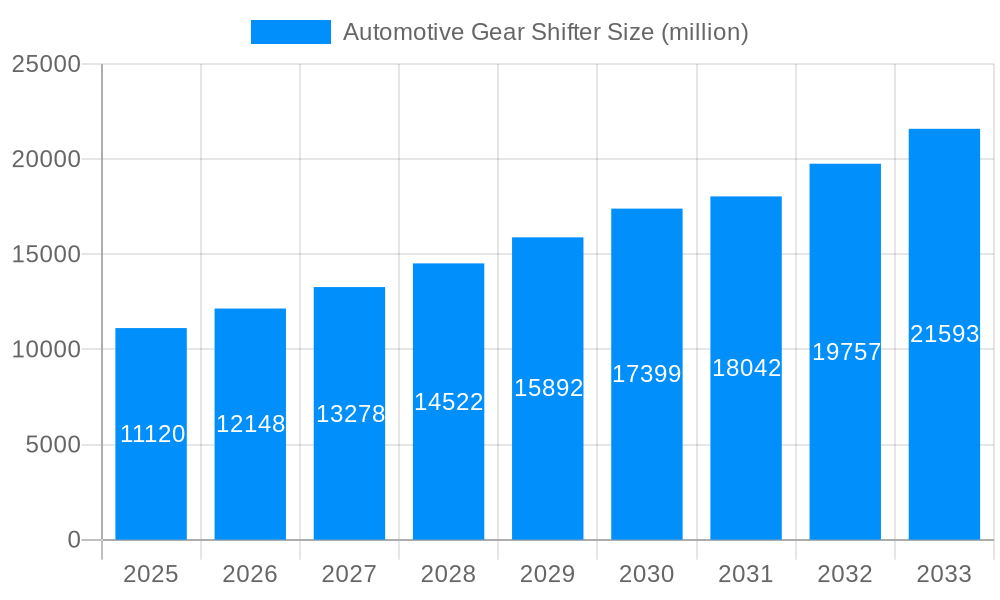

The global Automotive Gear Shifter market is poised for significant expansion, projected to reach an estimated value of $11.12 billion by 2025. This robust growth trajectory is fueled by a Compound Annual Growth Rate (CAGR) of 9.3% throughout the forecast period of 2025-2033. A primary driver for this expansion is the increasing adoption of advanced driver-assistance systems (ADAS) and autonomous driving technologies, which necessitate sophisticated and highly responsive gear shifting mechanisms. Furthermore, the growing global demand for passenger and commercial vehicles, particularly in emerging economies, directly translates into a higher volume of gear shifter production. Technological advancements, such as the shift towards electronic gear shifters offering enhanced convenience, safety, and fuel efficiency, are also a key contributor to market dynamism. The integration of these advanced systems aligns with evolving consumer preferences for more digitized and intuitive in-car experiences, pushing manufacturers to invest in innovative gear shifter solutions.

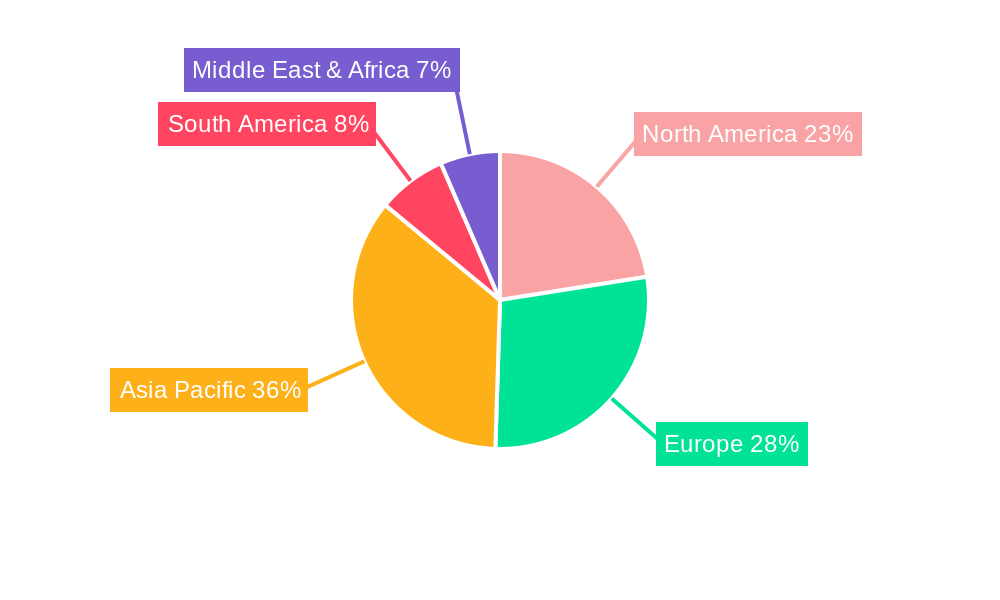

The market segmentation reveals a clear trend towards Electronic Gear Shifters, which are expected to capture a substantial market share due to their superior performance and integration capabilities with modern vehicle architectures. While Mechanical Gear Shifters will continue to hold a presence, particularly in cost-sensitive segments and certain commercial vehicle applications, the future clearly leans towards electronic solutions. Geographically, the Asia Pacific region, led by China, is anticipated to dominate the market, driven by its massive automotive manufacturing base and burgeoning consumer market. North America and Europe also represent significant markets, influenced by stringent safety regulations and a high adoption rate of advanced automotive technologies. Key players like ZF, Kongsberg, and GHSP are at the forefront of innovation, investing heavily in research and development to deliver next-generation gear shifting solutions that cater to the evolving demands of the global automotive industry.

This report offers a comprehensive analysis of the global automotive gear shifter market, spanning a critical study period from 2019 to 2033. With the Base Year and Estimated Year both set as 2025, the report meticulously examines the market's trajectory through its Historical Period (2019-2024) and projects its future landscape during the extensive Forecast Period (2025-2033). The analysis delves into intricate details, quantifying the market in terms of billions of units, providing a clear understanding of its scale and economic significance. The report segments the market by Type, encompassing both traditional Mechanical Gear Shifters and the increasingly dominant Electronic Gear Shifters, and by Application, detailing the demand from Passenger Vehicles and Commercial Vehicles. Furthermore, it provides insights into World Automotive Gear Shifter Production, offering a global perspective on manufacturing capabilities and output. The report is an indispensable resource for stakeholders seeking to understand the current dynamics, identify emerging trends, and strategize for future growth within this dynamic and technologically evolving sector.

The automotive gear shifter market is undergoing a profound transformation driven by the relentless pace of technological innovation and shifting consumer preferences. Over the study period of 2019-2033, a distinct trend towards sophisticated and user-friendly interfaces is evident. The transition from purely mechanical systems to electronic and even electromechanical actuators signifies a paradigm shift, catering to the demands of modern vehicle architectures. This evolution is not merely about aesthetics; it's deeply intertwined with advancements in vehicle safety, fuel efficiency, and autonomous driving capabilities. The increasing integration of advanced driver-assistance systems (ADAS) necessitates seamless communication between the shifter and the vehicle's central control unit, enabling features like automatic parking and predictive shifting. The proliferation of electric vehicles (EVs) has also become a significant influencer. EVs, often lacking traditional multi-speed transmissions, are adopting minimalist, often rotary or push-button, electronic shifters that are more akin to a selection of drive modes rather than a complex mechanical linkage. This shift is reshaping the manufacturing landscape, favoring companies with expertise in mechatronics and software integration. Furthermore, the pursuit of enhanced user experience is pushing the boundaries of ergonomic design, with shifters becoming more intuitive and less obtrusive within the cabin. The "by-wire" technology, where mechanical linkages are replaced by electrical signals, is gaining traction, offering greater design flexibility and weight reduction. Consumer demand for premium interiors is also influencing shifter design, with a growing emphasis on materials, haptic feedback, and customizable lighting. The consolidation of the automotive supply chain and the increasing focus on sustainability are also playing crucial roles, encouraging suppliers to develop more efficient, lightweight, and environmentally friendly gear shifter solutions. The market is witnessing a bifurcation, with high-end vehicles embracing cutting-edge electronic systems and some entry-level segments exploring cost-effective, yet still modernized, mechanical solutions. The underlying driver for these trends is the continuous effort to optimize vehicle performance, enhance driver convenience, and prepare for the autonomous future of mobility.

The automotive gear shifter market is propelled by a confluence of powerful forces, fundamentally reshaping its trajectory. The most significant catalyst is the global surge in vehicle production, particularly in emerging economies, which directly translates to increased demand for gear shifters. This expansion is further fueled by the growing middle class in these regions, leading to a greater adoption of personal mobility solutions. Concurrently, the relentless pursuit of fuel efficiency and reduced emissions by automotive manufacturers worldwide is a major driving force. Modern gear shifters, especially electronic variants, are crucial in optimizing transmission performance, contributing to better fuel economy and lower CO2 outputs. The advent and rapid integration of electric and hybrid vehicles represent another monumental driving force. These powertrains, with their unique operational requirements, necessitate innovative shifter designs that differ significantly from traditional internal combustion engine vehicles, often leading to the adoption of electronic or even push-button selectors. The increasing adoption of advanced driver-assistance systems (ADAS) and autonomous driving technologies also plays a pivotal role. These sophisticated systems require precise and reliable communication with the powertrain, and advanced gear shifters are integral to this interconnected ecosystem. Furthermore, the evolving consumer expectations for enhanced comfort, convenience, and sophisticated in-cabin experiences are pushing manufacturers to develop more ergonomic, intuitive, and aesthetically pleasing gear shifters. The drive towards vehicle weight reduction, aiming to improve overall performance and fuel efficiency, also favors the adoption of lightweight electronic components and the elimination of bulky mechanical linkages. Finally, evolving regulatory landscapes, mandating stricter emission standards and safety features, indirectly influence the demand for advanced gear shifter technologies that can contribute to compliance.

Despite its robust growth prospects, the automotive gear shifter market faces several significant challenges and restraints that could temper its expansion. One of the primary hurdles is the high cost associated with research and development (R&D) for advanced electronic and electromechanical gear shifting systems. The development of sophisticated software, intricate hardware, and rigorous testing procedures requires substantial investment, which can be a deterrent for smaller players and a considerable expense for larger ones. Furthermore, the increasing complexity of electronic shifters leads to potential issues related to reliability and durability, especially in harsh automotive environments. Ensuring consistent performance over the lifespan of a vehicle, across varying temperatures and vibrations, is a constant engineering challenge. The global automotive industry is also susceptible to geopolitical uncertainties, supply chain disruptions, and fluctuating raw material prices. Any instability in these areas can directly impact the production costs and availability of essential components for gear shifters, leading to price volatility and production delays. The evolving nature of vehicle powertrains, particularly the rapid transition towards electric vehicles, presents a unique challenge. While EVs are creating new opportunities for electronic shifters, the decline in traditional internal combustion engine vehicle production could lead to a contraction in the market for certain types of mechanical gear shifters. This necessitates adaptation and a strategic shift in product portfolios. Moreover, stringent regulatory compliance across different regions for safety and emissions standards adds another layer of complexity and cost to the development and manufacturing processes. The integration of new technologies also requires significant workforce retraining and the acquisition of new skill sets within manufacturing facilities, which can be a slow and expensive process. Finally, the intense competition within the automotive supply chain can lead to price pressures, squeezing profit margins for gear shifter manufacturers.

The global automotive gear shifter market is poised for significant growth, with certain regions and segments expected to lead this expansion.

Dominant Segments:

Key Dominant Regions/Countries:

Asia-Pacific: This region is unequivocally set to dominate the global automotive gear shifter market, driven by its position as the world's largest automotive manufacturing hub and a rapidly expanding consumer base.

Europe: Remains a strong and significant market for automotive gear shifters, characterized by its established automotive industry, high adoption rates of advanced technologies, and stringent emission regulations.

The dominance of the Asia-Pacific region, particularly China, is attributed to its massive production volumes, rapid adoption of EVs, and a burgeoning domestic market. Simultaneously, the electronic gear shifter segment's ascendancy is driven by the global shift towards electrification and the increasing sophistication of vehicle technology.

The automotive gear shifter industry is experiencing robust growth fueled by several key catalysts. The accelerating global adoption of electric and hybrid vehicles is a primary driver, as these powertrains necessitate entirely new generations of electronic shifting mechanisms. Furthermore, the continuous advancement in autonomous driving and ADAS technologies demands more sophisticated and integrated electronic control systems, with the gear shifter playing a crucial role in seamless operation. The increasing consumer preference for advanced in-cabin technology, intuitive interfaces, and premium aesthetics also pushes manufacturers to innovate in shifter design and functionality. The ongoing expansion of the global automotive market, particularly in emerging economies, translates directly into higher unit sales of vehicles and, consequently, gear shifters.

This report provides an in-depth and comprehensive analysis of the global automotive gear shifter market, offering stakeholders an unparalleled understanding of its current landscape and future trajectory. The report meticulously dissects the market by product type, application, and geographic region, utilizing data spanning the study period of 2019-2033, with a sharp focus on the Base Year (2025) and the Forecast Period (2025-2033). Beyond quantitative market sizing in billions of units, the report delves into critical trends, driving forces, and challenges, offering strategic insights for market participants. It identifies key regions and segments poised for dominance, providing a roadmap for future investment and development. The report also profiles leading players and highlights significant industry developments, ensuring a holistic and actionable perspective for businesses operating within or looking to enter this dynamic sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.3% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 9.3%.

Key companies in the market include Kongsberg, ZF, GHSP, SL, Sila, Ficosa, Fuji Kiko, Kostal, DURA, Tokai Rika, Ningbo Gaofa, Chongqing Downwind, Nanjing Aolin, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive Gear Shifter," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Gear Shifter, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.