1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Fuel Cell System Parts?

The projected CAGR is approximately 4.9%.

Automotive Fuel Cell System Parts

Automotive Fuel Cell System PartsAutomotive Fuel Cell System Parts by Type (Monitoring and Improving Part, Inputs (Hydrogen and Oxygen) Part, Outputs (Electricity, Water, and Heat) Part), by Application (Passenger Cars, Commercial Vehicles), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

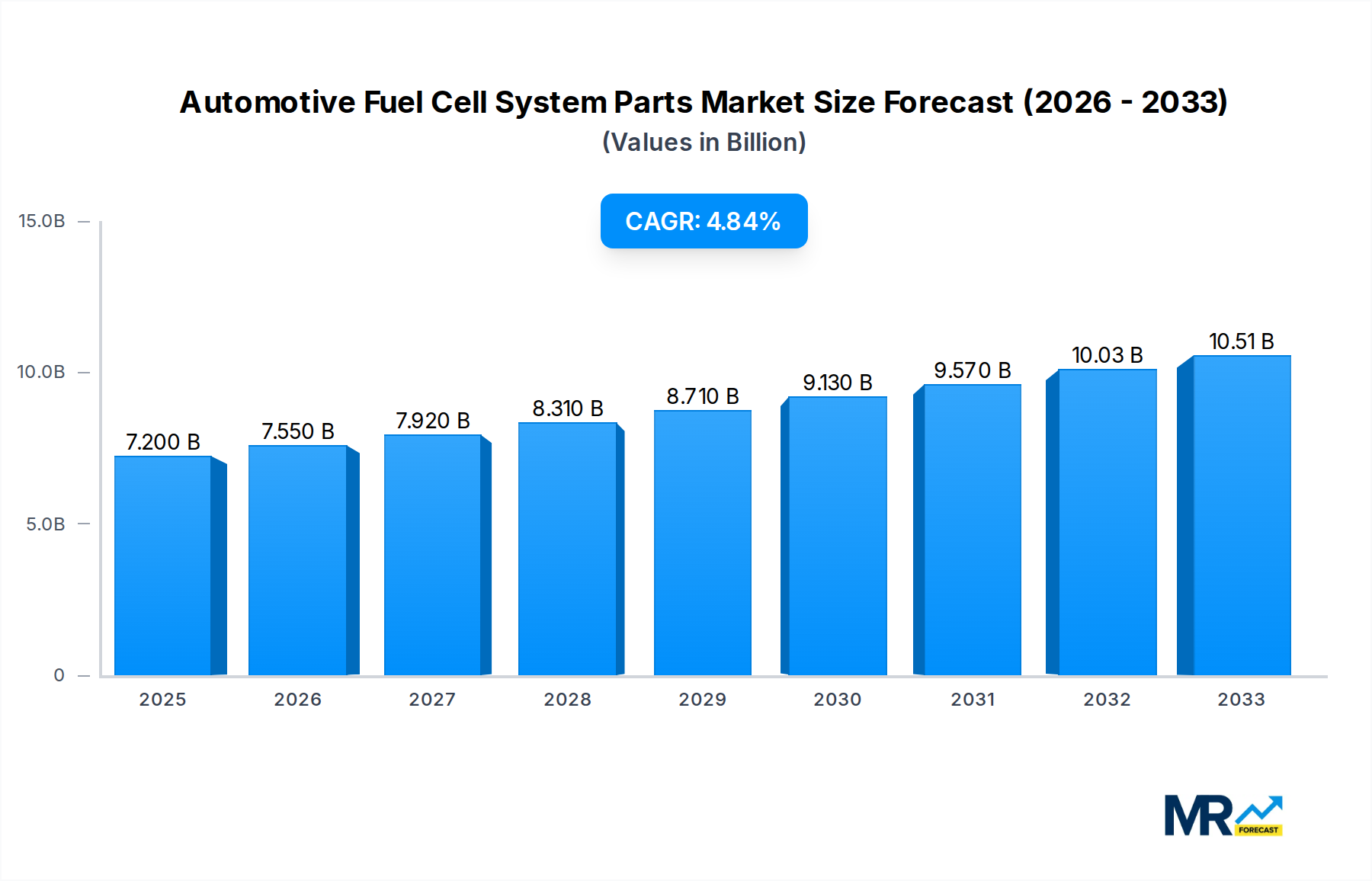

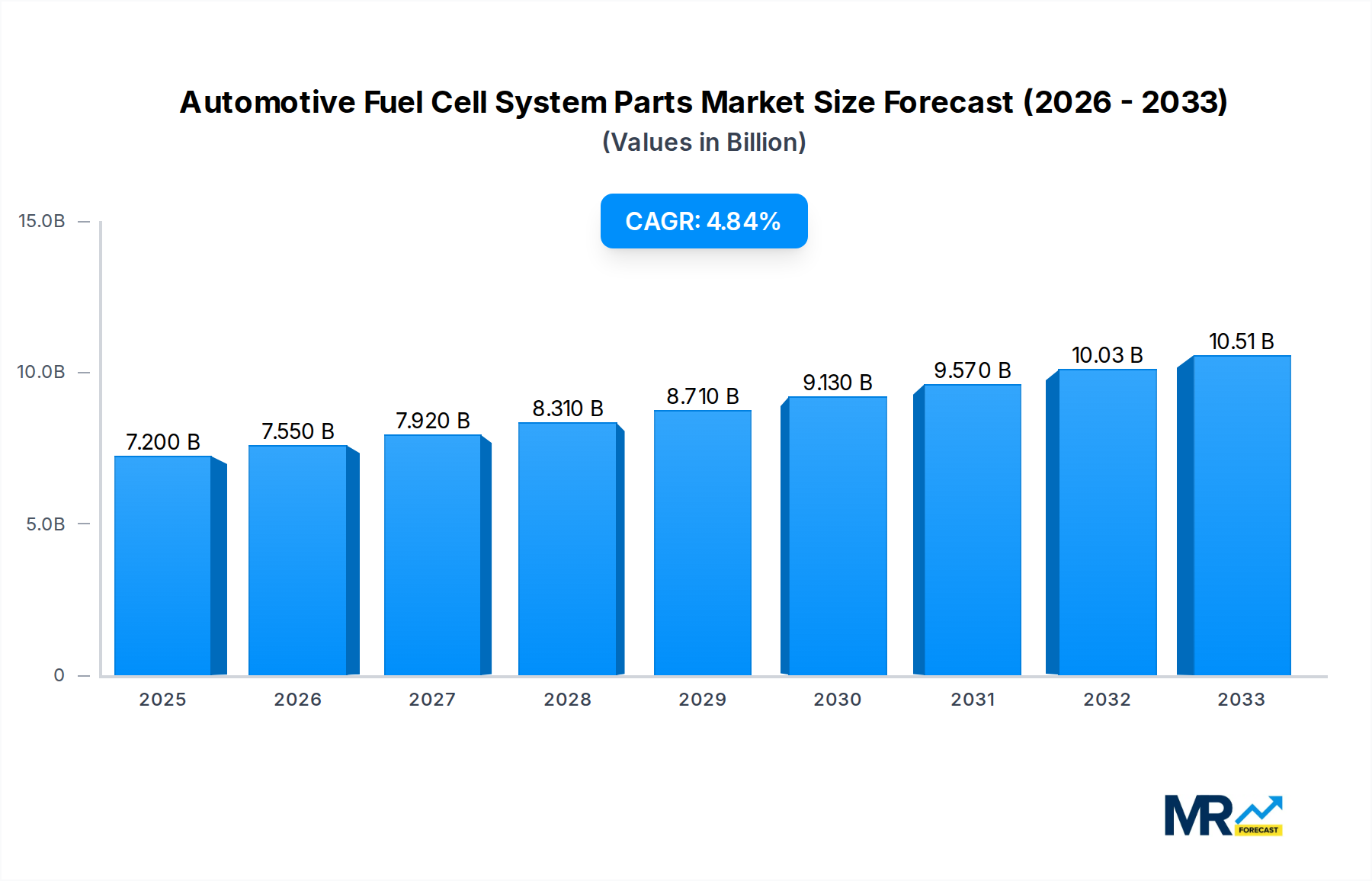

The Automotive Fuel Cell System Parts market is poised for significant expansion, with a current valuation of approximately $6.89 billion. This robust growth is projected to continue at a Compound Annual Growth Rate (CAGR) of 4.9% throughout the forecast period, reaching an estimated value of over $10 billion by 2033. This upward trajectory is primarily fueled by the accelerating adoption of fuel cell electric vehicles (FCEVs) driven by stringent emission regulations, government incentives, and a growing consumer demand for sustainable transportation solutions. Key market drivers include advancements in fuel cell technology, leading to improved efficiency and durability, as well as the expanding charging infrastructure for hydrogen refueling. The market is segmented into critical components: Monitoring and Improving Parts, Inputs (Hydrogen and Oxygen) Parts, and Outputs (Electricity, Water, and Heat) Parts. These segments are crucial for the efficient functioning and performance optimization of fuel cell systems in vehicles.

The application landscape for automotive fuel cell system parts is dominated by Passenger Cars, reflecting the burgeoning interest in hydrogen-powered personal mobility. Commercial Vehicles are also emerging as a significant application area, driven by the need for zero-emission long-haul transportation and reduced operational costs. Leading companies such as Toyota Industries, Parker-Hannifin, and Magneti Marelli are at the forefront of innovation and supply, contributing to the market's dynamic nature. However, the market faces certain restraints, including the high cost of fuel cell systems, limited availability of hydrogen refueling stations, and challenges in hydrogen production and storage. Despite these hurdles, the overarching trend towards decarbonization and the inherent advantages of fuel cell technology in terms of range and fast refueling times position the Automotive Fuel Cell System Parts market for sustained and substantial growth in the coming years.

Here's a unique report description for Automotive Fuel Cell System Parts, incorporating your specified elements:

XXX represents the burgeoning global automotive fuel cell system parts market, poised for significant expansion in the coming years. The market, valued in the billions, is undergoing a dynamic transformation driven by technological advancements and a growing imperative for sustainable mobility solutions. During the historical period of 2019-2024, the sector witnessed steady but nascent growth, largely confined to niche applications and early adopters. However, the base year of 2025 marks a pivotal point, with the market set to accelerate its trajectory throughout the forecast period of 2025-2033. Key market insights reveal a profound shift in investor confidence and manufacturing capabilities, with investments in the billions being channeled into research, development, and scaled production of critical fuel cell components. The emphasis is shifting from basic componentry to sophisticated, integrated systems designed for enhanced efficiency, durability, and cost-effectiveness. This evolution is underscored by the increasing demand for specialized parts that manage hydrogen and oxygen inputs with precision, as well as those that effectively process electricity, water, and heat outputs. The study period of 2019-2033 encapsulates this entire journey, from early exploration to widespread market penetration. A critical observation is the increasing modularity and standardization of fuel cell parts, facilitating easier integration into diverse vehicle platforms. Furthermore, the market is experiencing innovation in materials science, leading to lighter, more robust, and cost-efficient components. The projected growth in the billions is a testament to the industry's commitment to overcoming previous hurdles and realizing the full potential of hydrogen-powered transportation. The estimated year of 2025 signifies the dawn of a new era for automotive fuel cell system parts, characterized by technological maturity and commercial viability.

The automotive fuel cell system parts market is experiencing an unprecedented surge driven by a confluence of potent forces. Foremost among these is the global commitment to decarbonization and the urgent need to mitigate climate change. Governments worldwide are implementing stringent emission regulations and offering substantial incentives for zero-emission vehicles, directly fueling the demand for fuel cell technologies. This regulatory push is complemented by a burgeoning consumer awareness and preference for environmentally friendly transportation, creating a pull for vehicles powered by fuel cells. The rapid advancements in fuel cell technology itself are another significant propellant. Breakthroughs in membrane electrode assemblies (MEAs), bipolar plates, and balance of plant components are enhancing efficiency, extending lifespan, and reducing the overall cost of fuel cell systems, making them increasingly competitive with traditional internal combustion engines and battery electric vehicles. Furthermore, the diversification of hydrogen production methods, including the development of green hydrogen derived from renewable energy sources, is addressing concerns about the sustainability of the entire fuel cell ecosystem. The growing interest from major automotive manufacturers in developing and deploying fuel cell vehicles, particularly for commercial applications where range and rapid refueling are critical, is a substantial market driver.

Despite the optimistic outlook, the automotive fuel cell system parts market faces several formidable challenges and restraints that could temper its growth trajectory. The most significant hurdle remains the high cost of fuel cell components, particularly platinum-group metals used in catalysts, which can significantly increase the overall price of fuel cell vehicles. While efforts are underway to reduce platinum loading and explore alternative materials, cost parity with internal combustion engine vehicles and battery electric vehicles remains an elusive goal. The nascent hydrogen refueling infrastructure is another critical bottleneck. The limited availability and geographical dispersion of hydrogen fueling stations across many regions make widespread consumer adoption of fuel cell vehicles impractical and inconvenient. This lack of infrastructure creates a "chicken and the egg" problem, where manufacturers are hesitant to produce more vehicles without adequate refueling options, and infrastructure providers are reluctant to invest heavily without a guaranteed customer base. Safety concerns and public perception surrounding the storage and handling of hydrogen also present a restraint, although significant advancements in hydrogen tank technology and safety protocols are continuously being made. Finally, the long-term durability and maintenance costs of fuel cell systems, while improving, are still areas requiring further demonstration and consumer reassurance.

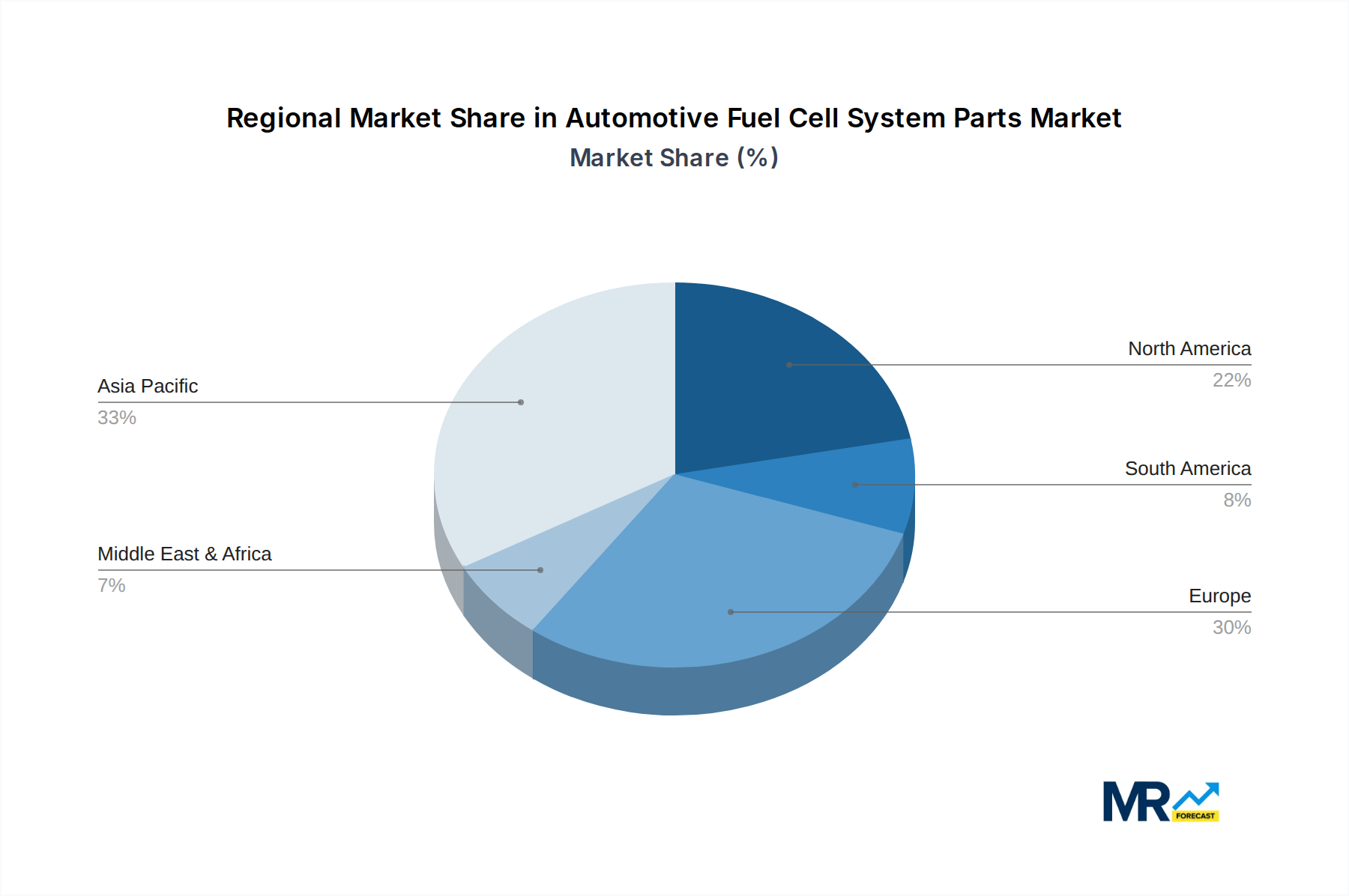

The automotive fuel cell system parts market is poised for dominance by Asia and North America, with specific segments within these regions exhibiting remarkable growth.

Within the broader market, the Inputs (Hydrogen and Oxygen) Part segment is expected to witness substantial growth across both regions. This encompasses a wide array of components essential for delivering and managing hydrogen and oxygen to the fuel cell stack, including:

The increasing focus on optimizing the core fuel cell reactions necessitates continuous innovation and scaling of production for these input-related parts. Manufacturers are investing in developing lighter, more durable, and cost-effective solutions to meet the growing demand from vehicle manufacturers. The anticipated market value in the billions for these specialized components underscores their critical role in enabling the widespread adoption of fuel cell technology. The development of advanced materials and manufacturing processes for these parts will be a key differentiator for market leaders.

Several factors are acting as significant growth catalysts for the automotive fuel cell system parts industry. The intensifying global focus on sustainability and emission reduction, coupled with supportive government policies and subsidies, provides a strong regulatory push. Technological advancements leading to improved fuel cell efficiency, durability, and reduced manufacturing costs are making fuel cell systems more economically viable. The growing demand for zero-emission commercial vehicles, where fuel cells offer a compelling range and refueling advantage, is a major catalyst. Furthermore, increasing investments from major automotive OEMs in developing and deploying fuel cell vehicles, alongside the expansion of hydrogen infrastructure initiatives, are creating a positive feedback loop, driving innovation and market expansion.

This comprehensive report delves into the intricate landscape of the automotive fuel cell system parts market, projected to reach billions in value. It meticulously analyzes the historical trajectory from 2019-2024, establishing a baseline for future growth. The base year of 2025 serves as a critical juncture, with the forecast period extending to 2033, meticulously charting the market's expansion. The report provides an in-depth examination of key market insights, highlighting transformative trends and technological advancements. It explores the driving forces, including stringent emission regulations and growing environmental consciousness, that are propelling the industry forward. Conversely, it also addresses the significant challenges and restraints, such as high component costs and nascent infrastructure, that the market must overcome. Furthermore, the report identifies dominant regions and segments, offering a detailed analysis of their strategic importance and growth potential. Key players and their contributions are highlighted, alongside significant developments that are shaping the future of automotive fuel cell technology. This report offers a holistic view, empowering stakeholders with the knowledge to navigate this dynamic and evolving market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.9% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4.9%.

Key companies in the market include Toyota Industries (Japan), Parker-Hannifin (USA), Magneti Marelli (Italy), NOK (Japan), Sensata Technologies (USA), Modine Manufacturing (USA), Aisan Industry (Japan), Sejong Industrial (Korea), Asahi Kasei (Japan), Fukui Byora (Japan), .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive Fuel Cell System Parts," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Fuel Cell System Parts, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.