1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Fatigue Testing?

The projected CAGR is approximately 4.5%.

Automotive Fatigue Testing

Automotive Fatigue TestingAutomotive Fatigue Testing by Type (Regular Testing, Extreme Testing), by Application (Passenger Car, Commercial Vehicle), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

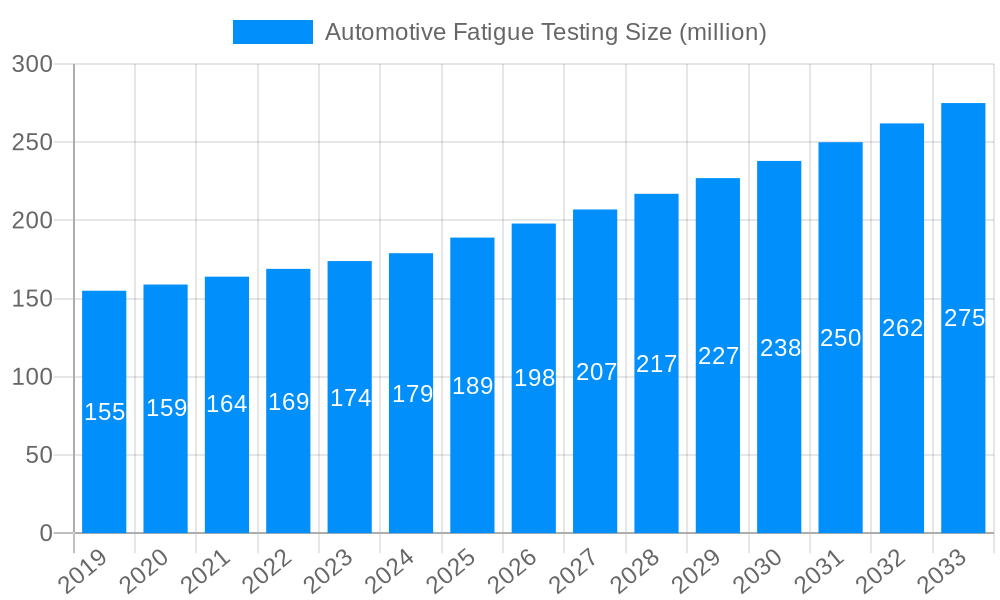

The global automotive fatigue testing market is poised for robust expansion, projected to reach an estimated USD 189 million by 2025, with a healthy Compound Annual Growth Rate (CAGR) of 4.5% anticipated through 2033. This sustained growth is primarily fueled by the escalating demand for enhanced vehicle durability, safety, and performance. Stringent automotive safety regulations worldwide are compelling manufacturers to invest heavily in rigorous testing protocols to ensure their vehicles can withstand prolonged stress and strain under diverse operating conditions. Furthermore, the continuous innovation in vehicle design, including the adoption of lighter materials and complex powertrains, necessitates advanced fatigue testing methodologies to validate structural integrity and predict lifespan. The market's expansion is further bolstered by the increasing complexity of vehicle electronic systems and the growing trend of electrification, which introduce new failure modes and require specialized fatigue testing solutions.

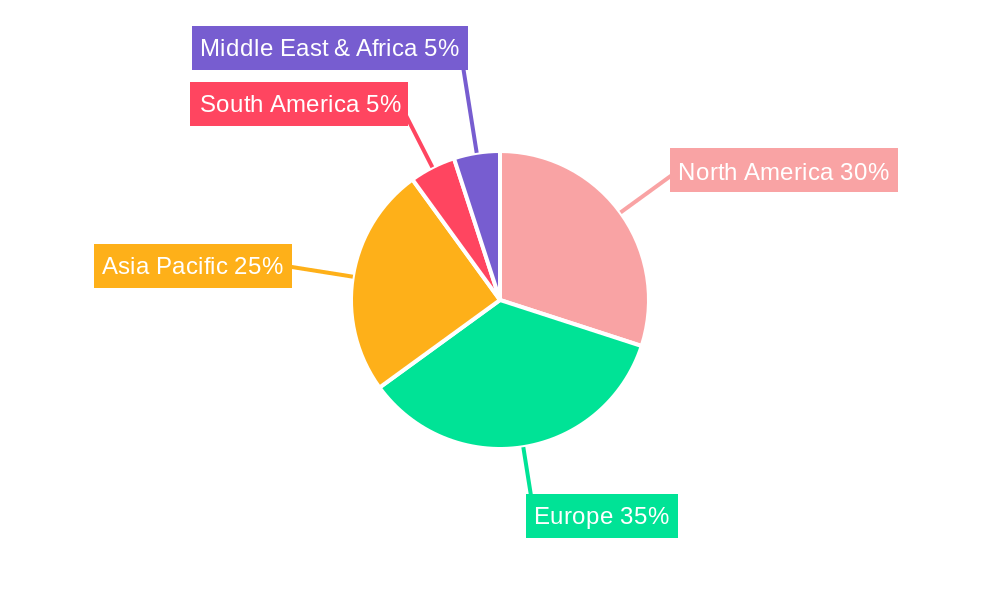

The automotive fatigue testing landscape is characterized by a dynamic interplay of evolving technologies and market demands. Key trends include the increasing adoption of simulation and digital twins to complement physical testing, offering cost efficiencies and faster design iterations. The integration of artificial intelligence and machine learning for predictive maintenance and optimized test cycle development is also gaining traction. While the market benefits from strong drivers, certain restraints are present. High upfront investment costs for sophisticated testing equipment and the need for skilled personnel can pose a challenge, particularly for smaller manufacturers. However, the growing outsourcing of testing services to specialized third-party providers is mitigating these barriers. The market is segmented by type into Regular Testing and Extreme Testing, with applications spanning Passenger Cars and Commercial Vehicles, each presenting unique testing requirements and growth opportunities. Geographically, North America and Europe currently dominate the market due to their established automotive industries and stringent safety standards, with Asia Pacific emerging as a high-growth region driven by its expanding automotive production and increasing focus on quality.

This comprehensive report delves into the dynamic landscape of Automotive Fatigue Testing, offering an in-depth analysis of market trends, driving forces, challenges, and future growth prospects. Spanning a study period from 2019 to 2033, with a focus on the base and estimated year of 2025, the report meticulously examines the historical period (2019-2024) to provide a robust foundation for forecasting the market's trajectory through the forecast period of 2025-2033.

The automotive fatigue testing market is undergoing a profound transformation driven by an insatiable demand for enhanced vehicle reliability, durability, and safety. In the historical period from 2019 to 2024, the market witnessed steady growth as manufacturers increasingly recognized the critical role of fatigue testing in preventing costly recalls and ensuring customer satisfaction. The advent of advanced simulation techniques and digital twins has begun to augment traditional physical testing, allowing for more efficient identification of potential failure points early in the development cycle. The increasing complexity of vehicle architectures, incorporating sophisticated electronics and lightweight materials, further necessitates rigorous fatigue assessment to validate their long-term performance under diverse operational stresses. The ongoing shift towards electric vehicles (EVs) and autonomous driving systems presents a unique set of fatigue challenges. Battery packs, high-voltage powertrains, and advanced sensor arrays require specialized testing protocols to ensure their resilience against vibrations, thermal cycling, and mechanical stresses encountered in real-world driving conditions. This evolution is leading to a greater adoption of extreme testing scenarios to replicate the demanding operational environments anticipated for these next-generation vehicles. Moreover, stricter regulatory mandates concerning vehicle safety and emissions are indirectly fueling the need for more comprehensive and sophisticated fatigue testing methodologies, pushing the boundaries of current testing capabilities. The market is also experiencing a growing emphasis on sustainability, with a focus on testing components and systems that contribute to fuel efficiency and reduced environmental impact. This includes evaluating the fatigue life of lightweight components and powertrain elements designed to optimize energy consumption. The overall trend points towards a market that is becoming more sophisticated, data-driven, and aligned with the evolving demands of the automotive industry, including the substantial global production volumes, which are projected to reach millions of units annually across various vehicle segments.

The projected market size in the millions of units for automotive components and vehicles undergoing fatigue testing is substantial and growing. For instance, considering the annual production of passenger cars alone, which runs into tens of millions globally, even a small percentage undergoing advanced fatigue testing translates to a significant volume. Similarly, commercial vehicles, although produced in lower volumes than passenger cars, often demand more intensive fatigue testing due to their rugged operational requirements and longer service life expectations, potentially representing millions of units tested annually. The burgeoning electric vehicle segment, while still growing, is rapidly expanding its share of this testing volume, with millions of battery systems and electric drivetrains slated for rigorous fatigue evaluation. This increasing demand for robust and reliable vehicles across all segments, from everyday passenger cars to heavy-duty commercial trucks and specialized industrial applications, directly translates into a massive volume of components and systems that require comprehensive fatigue testing to meet stringent industry standards and consumer expectations.

The automotive fatigue testing market is being propelled by a confluence of powerful forces, each contributing to its sustained growth and evolution. Foremost among these is the unwavering commitment of automotive manufacturers to enhance vehicle safety and reliability. With the ever-increasing complexity of modern vehicles, integrating advanced electronics, novel materials, and sophisticated powertrains, the need to guarantee long-term durability and prevent catastrophic failures has never been more paramount. This drive for excellence is further amplified by stringent governmental regulations and evolving consumer expectations, where a history of recalls or performance issues can significantly damage brand reputation and market share. The burgeoning electric vehicle (EV) revolution is a significant catalyst, introducing new components like battery packs, electric motors, and power electronics that require specialized fatigue testing to ensure their longevity and performance under demanding operating conditions. Furthermore, the widespread adoption of advanced driver-assistance systems (ADAS) and the development of autonomous driving technologies necessitate rigorous testing of sensors, actuators, and control units to ensure their unwavering reliability in all environmental scenarios. The increasing globalization of the automotive supply chain also plays a crucial role, demanding standardized testing protocols to ensure component quality and compatibility across different regions and suppliers. The pursuit of lightweighting strategies to improve fuel efficiency and reduce emissions necessitates testing the fatigue performance of new composite materials and advanced alloys, ensuring they can withstand the rigors of daily use over their intended lifespan.

Despite the robust growth trajectory, the automotive fatigue testing sector is not without its hurdles. One of the most significant challenges is the escalating cost associated with advanced testing equipment and facilities. Developing and maintaining state-of-the-art fatigue testing rigs, particularly those capable of simulating extreme environmental conditions or high-cycle loads, requires substantial capital investment. This financial burden can be particularly challenging for smaller and medium-sized enterprises (SMEs) within the supply chain. Another restraint is the increasing complexity and diversity of vehicle architectures. As vehicles become more integrated and feature an array of interconnected systems, replicating all potential fatigue scenarios in a test environment becomes increasingly intricate and time-consuming. The rapid pace of technological innovation in the automotive industry also poses a challenge. New materials, software-driven functionalities, and evolving powertrain designs necessitate continuous adaptation and development of new testing methodologies, which can be a resource-intensive process. The global semiconductor shortage and supply chain disruptions experienced in recent years have also impacted the availability of testing equipment and components, indirectly affecting the pace of fatigue testing. Furthermore, the need for highly skilled personnel with expertise in advanced simulation, data analysis, and specialized testing techniques creates a talent acquisition challenge for many organizations. The pressure to reduce development timelines while maintaining or improving testing rigor also presents a constant balancing act for manufacturers.

The Passenger Car segment, across several key regions, is poised to dominate the automotive fatigue testing market in terms of volume and strategic importance.

Dominant Regions and Countries:

Dominant Segment: Passenger Car

While Commercial Vehicles also represent a significant and growing segment, particularly in terms of the intensity of testing required due to their demanding operational environments, the sheer volume of Passenger Car production and the breadth of its technological adoption ensure its leading position in the automotive fatigue testing market.

Several key factors are acting as significant growth catalysts for the automotive fatigue testing industry. The accelerating adoption of electric vehicles (EVs) is a major driver, introducing new components like battery packs and electric drivetrains that require specialized and robust fatigue testing to ensure their longevity and performance. The increasing integration of advanced driver-assistance systems (ADAS) and the pursuit of autonomous driving capabilities necessitate rigorous testing of sensors, actuators, and associated electronics to guarantee their reliability under all conditions. Furthermore, a growing emphasis on lightweighting strategies, utilizing advanced materials like composites and high-strength alloys, demands comprehensive fatigue analysis to ensure these components can withstand operational stresses. Stricter safety regulations and evolving consumer expectations for vehicle durability and longevity are also compelling manufacturers to invest more in comprehensive fatigue testing throughout the product development lifecycle.

This report offers a comprehensive overview of the automotive fatigue testing market, providing invaluable insights for stakeholders across the industry. It delves into the intricate details of market segmentation, meticulously analyzing trends and growth drivers within different testing types such as Regular Testing and Extreme Testing, and across various applications including Passenger Car and Commercial Vehicle. The report forecasts market dynamics from 2025 to 2033, building upon a thorough analysis of the historical period (2019-2024) and establishing 2025 as the base and estimated year. Beyond market sizing and projections, it explores the critical technological advancements, regulatory influences, and evolving consumer demands that are shaping the future of automotive durability and reliability. The report identifies key players, highlights their strategic initiatives, and examines significant developments, offering a holistic understanding of the competitive landscape and future opportunities within this vital sector of the automotive industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.5% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4.5%.

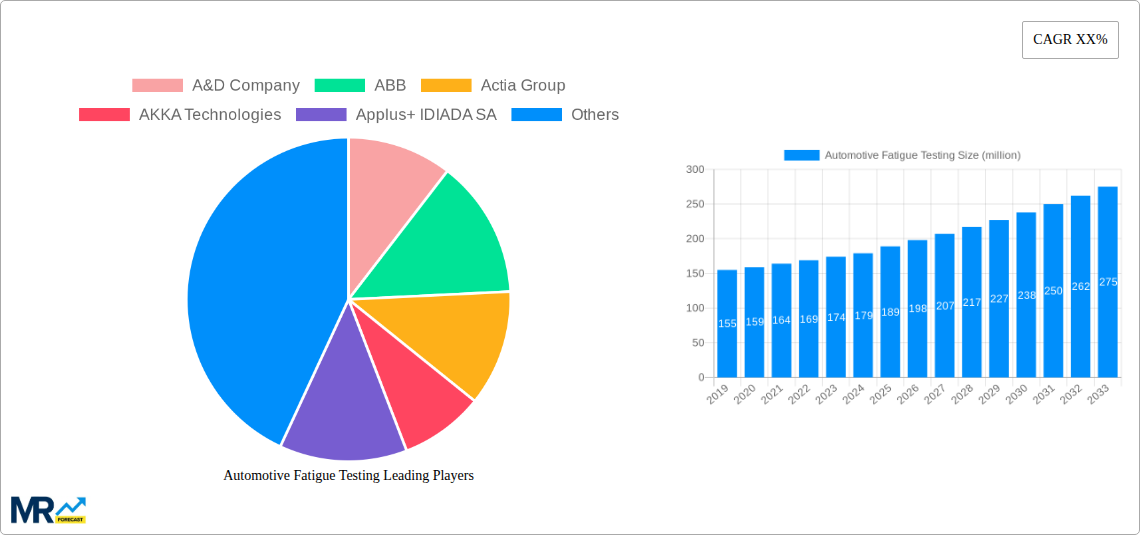

Key companies in the market include A&D Company, ABB, Actia Group, AKKA Technologies, Applus+ IDIADA SA, ATESTEO GmbH, ATS Automation Tooling Systems, AVL Powertrain Engineering, Continental AG, Cosworth, Delphi Technologies, FEV Europe GmbH, Honeywell International, HORIBA MIRA, IAV Automotive Engineering, Intertek Group, Mustang Advanced Engineering, Redviking Group, Ricardo, Robert Bosch GmbH, SGS SA, Siemens, Softing AG, ThyssenKrupp System Engineering GmbH, Vector Informatik GmbH, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A.

Yes, the market keyword associated with the report is "Automotive Fatigue Testing," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Fatigue Testing, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.