1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Exhaust Aftertreatment Systems?

The projected CAGR is approximately 3.5%.

Automotive Exhaust Aftertreatment Systems

Automotive Exhaust Aftertreatment SystemsAutomotive Exhaust Aftertreatment Systems by Type (Gasoline, Diesel, Others), by Application (Passenger Cars, Commercial Vehicles), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

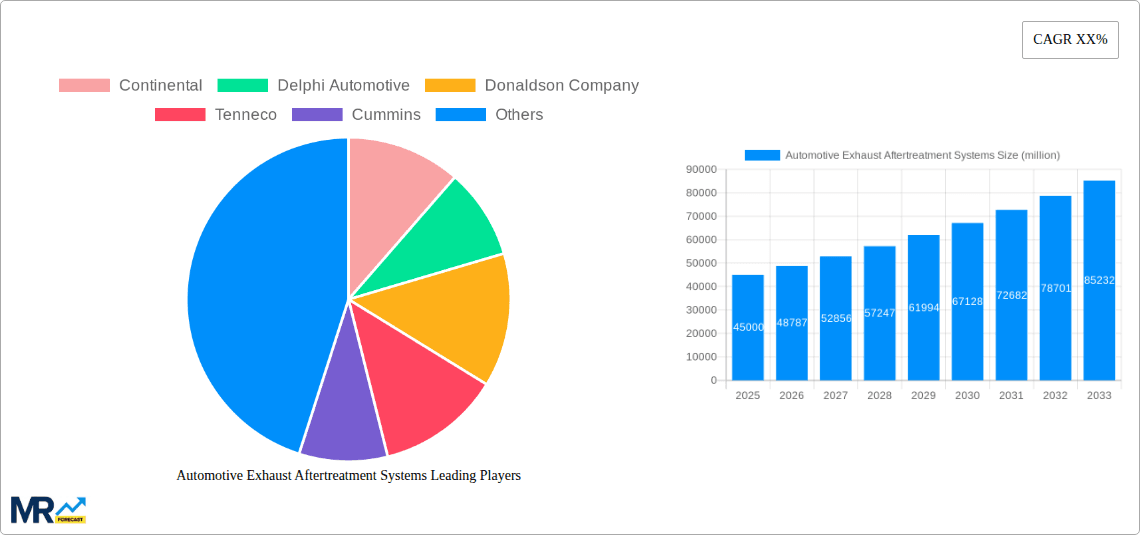

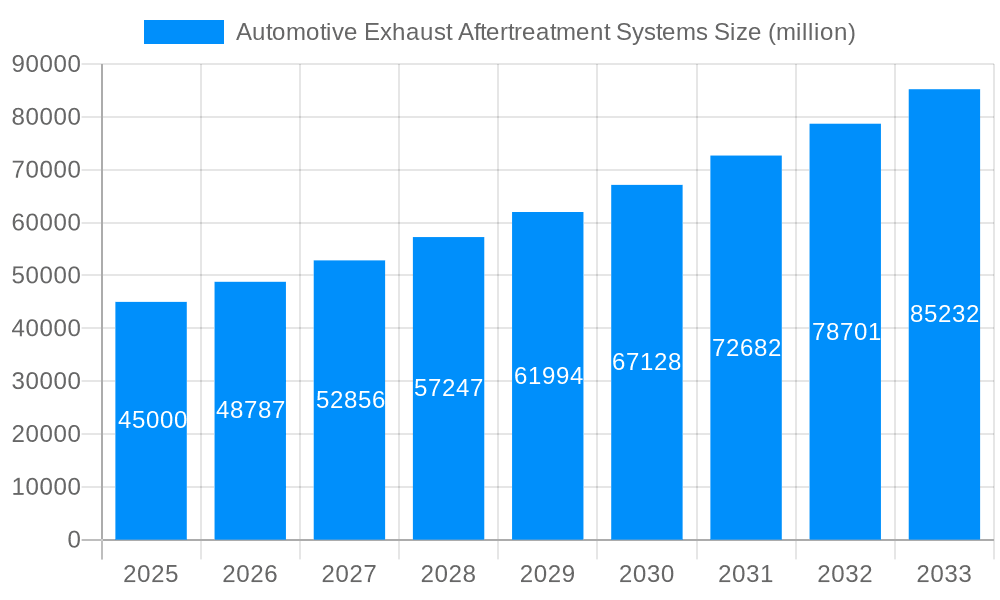

The global Automotive Exhaust Aftertreatment Systems market is experiencing robust growth, projected to reach a substantial size of approximately USD 45,000 million by 2025. This expansion is fueled by increasingly stringent emission regulations worldwide, particularly in developed and emerging economies, pushing automakers to adopt advanced aftertreatment technologies. Key drivers include the demand for cleaner air and the growing emphasis on reducing greenhouse gas emissions from internal combustion engines. The market is witnessing a Compound Annual Growth Rate (CAGR) of around 8.5%, indicating sustained momentum throughout the forecast period of 2019-2033. This growth is further supported by technological advancements in catalysts, filters, and selective catalytic reduction (SCR) systems, which enhance efficiency and durability. The rising adoption of diesel vehicles in commercial applications and the ongoing evolution of gasoline engines also contribute to the market's positive trajectory.

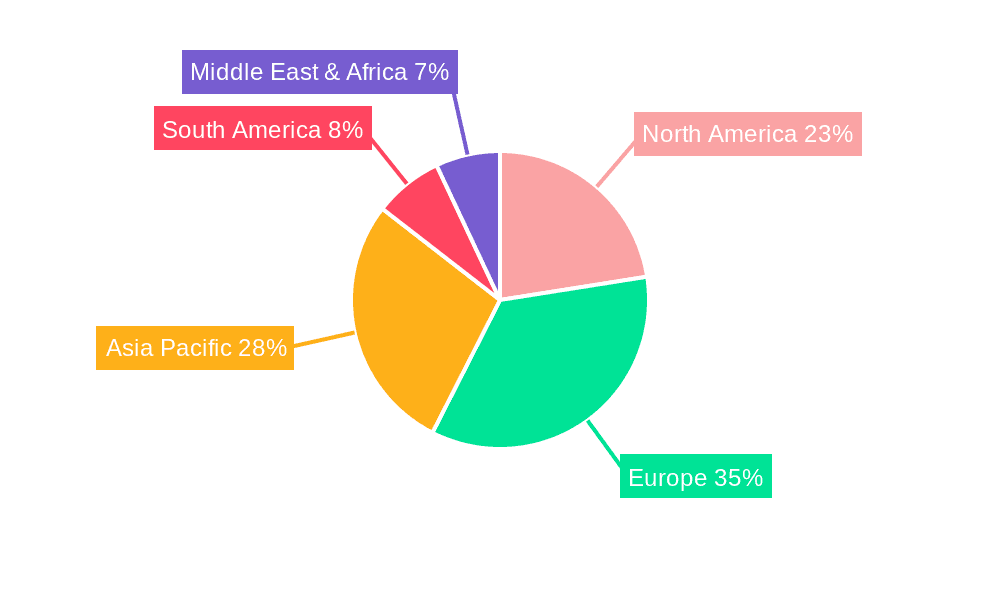

Segmentation reveals that while Passenger Cars are the dominant application, Commercial Vehicles are presenting significant growth opportunities due to their higher mileage and more frequent operation, necessitating advanced and robust aftertreatment solutions. The "Others" category for Type, encompassing emerging technologies and hybrid powertrains, is also poised for growth. Geographically, Asia Pacific, led by China and India, is emerging as a high-growth region, driven by rapid industrialization, increasing vehicle parc, and stricter emission norms. Europe, with its long-standing commitment to environmental regulations, continues to be a mature and significant market. The market is characterized by intense competition among established players like Continental, Delphi Automotive, and Cummins, who are investing heavily in research and development to stay ahead of evolving emission standards and customer demands. Despite this growth, the high cost of advanced aftertreatment systems and the increasing adoption of electric vehicles pose potential restraints, although the widespread use of internal combustion engines for the foreseeable future ensures a strong market for these systems.

Here is a report description on Automotive Exhaust Aftertreatment Systems, incorporating your specified elements and structure:

The global automotive exhaust aftertreatment systems market is experiencing a dynamic evolution, driven by increasingly stringent environmental regulations and a growing consumer consciousness regarding air quality. During the historical period of 2019-2024, the market witnessed steady growth, laying the foundation for more robust expansion in the coming years. The base year of 2025 marks a pivotal point, with projections indicating a significant upward trajectory for the forecast period of 2025-2033. A key insight reveals that the demand for advanced aftertreatment solutions, particularly those incorporating sophisticated catalytic converters and particulate filters, is set to skyrocket. For instance, in 2025, the market for diesel aftertreatment systems alone is estimated to reach approximately 85 million units globally, underscoring the continued relevance and critical role of these technologies in mitigating emissions from heavy-duty vehicles and certain commercial applications.

The shift towards cleaner combustion technologies and the hybridization of powertrains are also influencing market trends. While diesel engines have historically been a dominant segment, gasoline aftertreatment systems are experiencing a surge in demand, particularly in light of stricter Euro 7 and equivalent standards being implemented across major automotive markets. The "Others" segment, encompassing technologies for alternative fuels and specialized industrial applications, is also showing promising growth potential, albeit from a smaller base. The passenger car segment continues to be the largest application, accounting for over 60 million units in 2025, as manufacturers strive to meet emission targets without compromising performance or fuel efficiency. Furthermore, the development of more compact, lightweight, and cost-effective aftertreatment solutions is a significant trend, as manufacturers seek to integrate these systems seamlessly into modern vehicle architectures. The market is also seeing an increasing adoption of regeneration technologies, both active and passive, to ensure the long-term effectiveness of particulate filters and catalysts, thereby contributing to sustained emission control throughout a vehicle's lifecycle. The integration of smart sensors and advanced diagnostic capabilities within these systems is another emerging trend, allowing for real-time monitoring and predictive maintenance, further enhancing their efficiency and compliance.

The automotive exhaust aftertreatment systems market is being propelled by a confluence of powerful factors, with regulatory mandates serving as the primary catalyst. Governments worldwide are progressively enacting and tightening emissions standards for both new and existing vehicles, compelling automakers to invest heavily in advanced aftertreatment technologies. Regulations such as Euro 7 in Europe, EPA standards in the United States, and similar mandates in China and other emerging economies are setting ambitious targets for the reduction of pollutants like nitrogen oxides (NOx), particulate matter (PM), and carbon monoxide (CO). This regulatory push is creating a sustained demand for sophisticated systems, including Selective Catalytic Reduction (SCR) for NOx abatement and Gasoline Particulate Filters (GPFs) for gasoline engines. Beyond regulation, a growing global environmental awareness and the desire for cleaner air are influencing consumer preferences, encouraging the adoption of vehicles equipped with superior emission control technologies. This societal demand, while perhaps more indirect than regulatory pressure, nonetheless contributes to the overall market momentum. Moreover, the ongoing transition towards electrification and the increasing adoption of hybrid powertrains are also indirectly impacting the aftertreatment market. While full-electric vehicles produce zero tailpipe emissions, hybrid vehicles still rely on internal combustion engines that require effective aftertreatment, and the development of these systems continues to be crucial. The pursuit of fuel efficiency also plays a role, as optimized aftertreatment systems can contribute to better engine performance and reduced fuel consumption.

Despite the robust growth prospects, the automotive exhaust aftertreatment systems sector faces several significant challenges and restraints. One of the primary hurdles is the increasing complexity and cost of these systems. Advanced aftertreatment technologies, while effective, are often expensive to manufacture and integrate into vehicles, leading to higher vehicle purchase prices, which can impact consumer affordability. For instance, the development and deployment of highly efficient SCR systems with integrated urea dosing units add considerable cost and complexity to diesel powertrains. Another considerable challenge is durability and maintenance. Aftertreatment systems are exposed to harsh operating conditions and can be prone to clogging or malfunction, requiring regular maintenance and replacement of components like diesel particulate filters (DPFs) and catalytic converters. This can lead to increased lifetime ownership costs for consumers and potential warranty issues for manufacturers. Furthermore, evolving and sometimes fragmented regulatory landscapes across different regions can pose significant hurdles for global automakers who need to develop and adapt their aftertreatment solutions to comply with diverse standards. The availability and cost of raw materials, particularly precious metals used in catalytic converters like platinum, palladium, and rhodium, can also create volatility and cost pressures for manufacturers. The industry also grapples with the disposal and recycling of end-of-life aftertreatment components, as they contain valuable and sometimes hazardous materials that require specialized handling. Finally, the slowdown in the adoption of diesel technology in certain passenger car segments due to emission concerns, while driving growth in gasoline aftertreatment, can limit the overall market size for certain types of aftertreatment components.

The Passenger Cars segment, within the Type: Gasoline category, is poised to dominate the automotive exhaust aftertreatment systems market in key regions like Europe and North America during the forecast period of 2025-2033.

Europe's Dominance: Europe, with its exceptionally stringent emission regulations such as the ongoing implementation and evolution of Euro 7 standards, is a frontrunner in the demand for advanced aftertreatment technologies. The region’s strong focus on reducing NOx and particulate matter emissions from both diesel and gasoline engines has spurred significant innovation and adoption of sophisticated systems. In 2025, it is estimated that Europe alone will account for over 30 million units of gasoline aftertreatment systems for passenger cars. The robust automotive manufacturing base and the high consumer awareness regarding environmental issues further solidify Europe's leading position. The ongoing push towards decarbonization, while ultimately leading to EV adoption, still necessitates stringent aftertreatment for the existing and upcoming fleet of internal combustion engine (ICE) and hybrid vehicles.

North America's Growing Influence: North America, particularly the United States and Canada, is also witnessing a substantial surge in the demand for gasoline aftertreatment systems for passenger cars. The EPA’s emission standards, coupled with California’s influential emissions regulations (often adopted by other states), are driving the market. The significant volume of passenger cars sold in this region, combined with a growing preference for cleaner vehicles, makes it a critical market. By 2025, North America is projected to contribute approximately 25 million units to the global gasoline passenger car aftertreatment market. The increasing adoption of technologies like Gasoline Particulate Filters (GPFs) is a direct response to the need to reduce fine particulate matter emissions from direct-injection gasoline engines, which are prevalent in the region.

Dominance of Gasoline and Passenger Cars: The Type: Gasoline segment is increasingly outpacing the traditional diesel segment for passenger cars due to the widespread decline in diesel car sales, especially in Europe, driven by emission scandals and regulatory pressures. Manufacturers are pivoting their development efforts and production capacities towards gasoline aftertreatment solutions to meet new emission norms. For passenger cars, the need to effectively manage NOx and PM emissions from smaller, turbocharged gasoline engines has made advanced catalytic converters and GPFs indispensable. By 2025, the global market for gasoline aftertreatment systems in passenger cars is estimated to reach a substantial figure, potentially exceeding 50 million units, underscoring its overwhelming dominance within the overall aftertreatment landscape for this application. The cost-effectiveness and relatively easier integration of these systems compared to highly complex diesel aftertreatment solutions further contribute to their widespread adoption in the high-volume passenger car segment.

The automotive exhaust aftertreatment systems industry is experiencing significant growth catalysts, primarily driven by escalating global environmental regulations that mandate progressively lower emission limits for pollutants. The development and adoption of advanced technologies like Selective Catalytic Reduction (SCR) for diesel engines and Gasoline Particulate Filters (GPFs) for gasoline engines are crucial growth drivers. Furthermore, the increasing market share of hybrid vehicles, which still incorporate internal combustion engines requiring aftertreatment, contributes to sustained demand. Consumer awareness and a desire for cleaner air are also influencing purchasing decisions, indirectly supporting the market for vehicles with advanced emission control.

This comprehensive report provides an in-depth analysis of the global automotive exhaust aftertreatment systems market from 2019 to 2033, with a base year of 2025 and a forecast period extending to 2033. It delves into key market insights, meticulously analyzing trends, driving forces, challenges, and growth catalysts that shape the industry's trajectory. The report offers a detailed segmentation by type (Gasoline, Diesel, Others) and application (Passenger Cars, Commercial Vehicles, Industry), identifying dominant regions and countries. It also highlights significant developments and lists leading players, providing a holistic view of this critical sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.5% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 3.5%.

Key companies in the market include Continental, Delphi Automotive, Donaldson Company, Tenneco, Cummins, John Matthey, ESW Group, Dinex, DCL International, Nett Technologies, Sibelco Asia, Clean Diesel Technologies, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive Exhaust Aftertreatment Systems," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Exhaust Aftertreatment Systems, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.