1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Competition Tyre?

The projected CAGR is approximately 8.26%.

Automotive Competition Tyre

Automotive Competition TyreAutomotive Competition Tyre by Type (18-inch, 15-inch, 13-inch, Others, World Automotive Competition Tyre Production ), by Application (Grand Tourer, Touring, Formula, Rally, Others, World Automotive Competition Tyre Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

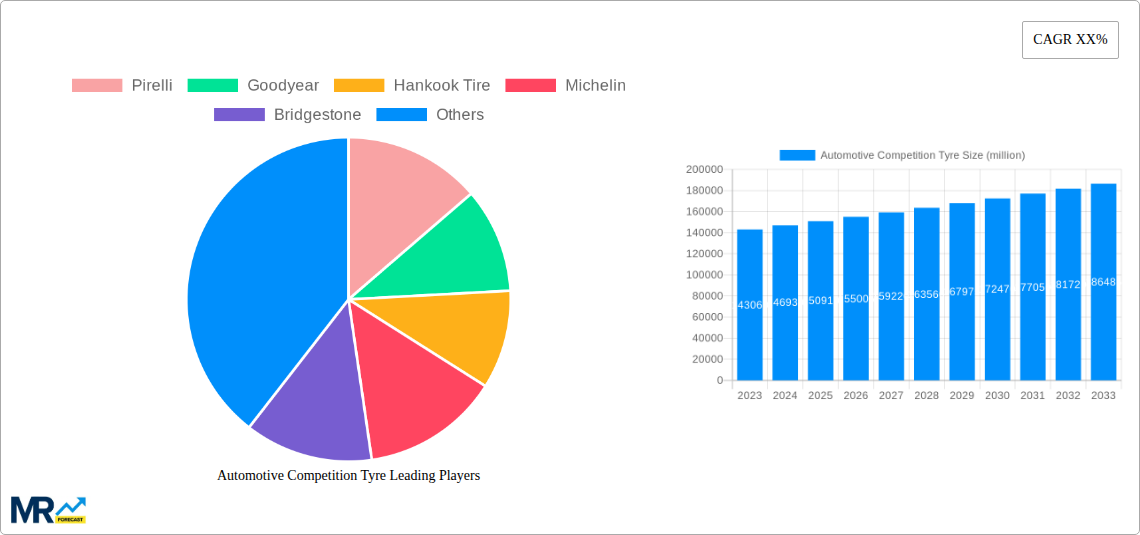

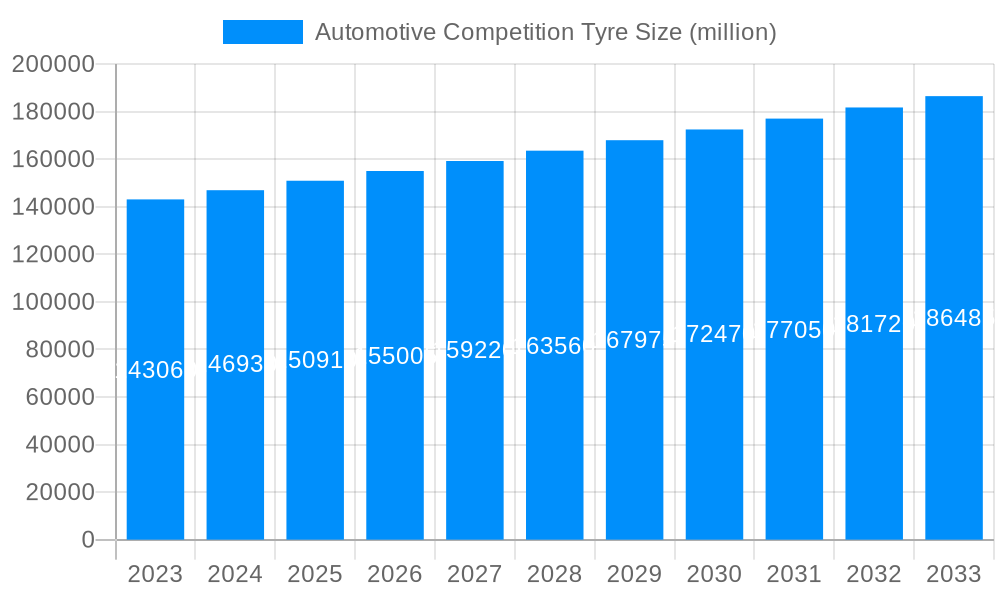

The global automotive competition tyre market is projected to reach a substantial valuation, driven by the adrenaline-fueled world of motorsports and the increasing demand for high-performance vehicles. With a current market size of $143.06 billion in 2023, the industry is expected to witness a steady expansion, growing at a Compound Annual Growth Rate (CAGR) of 3.4% from 2023 to 2033. This growth is underpinned by several key factors. The sheer passion and investment in professional racing circuits, from Formula 1 to endurance events, consistently fuels the need for specialized, cutting-edge competition tyres. Furthermore, the burgeoning trend of track days, amateur racing, and performance tuning among automotive enthusiasts creates a significant secondary market. As consumers increasingly seek enhanced driving dynamics and on-track capabilities in their personal vehicles, the demand for competition-grade tyres, even for road use, is on the rise. Leading tyre manufacturers are continuously investing in research and development to produce lighter, more durable, and grippier tyres, pushing the boundaries of what's possible in tyre technology. This innovation directly benefits the competition segment, driving adoption and market value.

The market is segmented across various tyre types, with 18-inch, 15-inch, and 13-inch dominating due to their prevalence in major racing disciplines. However, the "Others" category, encompassing specialized sizes for unique racing applications and emerging series, also shows potential for growth. The application landscape is dominated by Grand Tourer and Touring segments, reflecting the broad appeal of performance driving beyond dedicated race tracks. Formula and Rally racing, while niche, represent highly specialized and technologically advanced segments that drive innovation. Geographically, Asia Pacific, particularly China and Japan, is emerging as a significant growth engine, fueled by a rapidly expanding automotive sector and a growing interest in performance driving. North America and Europe remain mature yet robust markets, driven by established racing leagues and a strong culture of automotive enthusiasm. Key players like Pirelli, Goodyear, Michelin, and Bridgestone are at the forefront, constantly innovating and strategizing to capture market share in this dynamic and competitive arena.

Here's a report description for Automotive Competition Tyres, incorporating your specific requests for structure, content, and word counts:

This comprehensive report delves into the intricate dynamics of the global automotive competition tyre market, offering an in-depth analysis from the historical period of 2019-2024 through to a projected future extending to 2033. With the base and estimated year set at 2025, the study provides a robust framework for understanding past performance, current market standing, and future growth trajectories. The market, projected to reach values in the billions of USD across its forecast period, is shaped by evolving technological advancements, shifting consumer preferences, and the ever-increasing performance demands of motorsport.

This report will dissect the market across various critical segments, including tyre types such as 18-inch, 15-inch, 13-inch, and Others, providing granular insights into their respective market shares and growth potential. Furthermore, the analysis will extend to the diverse applications of competition tyres, categorised into Grand Tourer, Touring, Formula, Rally, and Others, highlighting the specific demands and innovations within each application. The World Automotive Competition Tyre Production figures will be a central focus, offering a quantitative overview of global manufacturing output and capacity. Industry developments will be tracked meticulously, providing context for the market's evolution.

Companies such as Pirelli, Goodyear, Hankook Tire, Michelin, Bridgestone, and Yokohama are key players whose strategies, innovations, and market positioning are thoroughly examined. This report is an essential resource for tyre manufacturers, motorsport organisations, automotive manufacturers, investors, and industry analysts seeking to navigate and capitalize on the burgeoning opportunities within the global automotive competition tyre sector.

The automotive competition tyre market is characterized by a relentless pursuit of enhanced performance, durability, and efficiency, driving a wave of innovative trends. XXX [Insert Key Market Insights Here]. For instance, the increasing sophistication of Formula racing demands ultra-lightweight yet incredibly robust tyres capable of withstanding extreme G-forces and temperatures, leading to advancements in compound technologies and structural designs. The burgeoning popularity of Grand Tourer (GT) racing and endurance events has spurred the development of tyres offering a delicate balance between outright grip for blistering lap times and longevity to endure hundreds of competitive kilometres. This necessitates advanced rubber formulations that can degrade predictably, providing consistent performance throughout a stint. Furthermore, the niche but passionate Rally segment continually pushes the boundaries of tyre construction, requiring unparalleled resistance to punctures and impacts from varied and unpredictable terrains. The integration of smart tyre technology, embedding sensors to monitor pressure, temperature, and wear in real-time, is another significant trend, offering teams invaluable data for strategic decision-making and performance optimization. This technological integration is not just confined to elite motorsport but is also filtering down into semi-professional and even high-performance amateur racing, democratizing access to advanced performance monitoring. The environmental consciousness within the automotive industry is also beginning to influence competition tyre development, with a growing interest in sustainable materials and manufacturing processes, aiming to reduce the carbon footprint without compromising on performance. This is leading to research into bio-based compounds and recycled materials, representing a long-term shift in the industry's approach to sustainability. The constant evolution of vehicle dynamics and chassis design also necessitates a corresponding evolution in tyre technology, creating a symbiotic relationship where advancements in one directly fuel innovation in the other. The increasing global reach of motorsport, particularly in emerging markets, is also a trend to watch, as it opens up new avenues for market growth and demand for specialized competition tyres tailored to local racing conditions and regulations. The competitive landscape is increasingly globalized, with manufacturers vying for dominance across diverse racing series and geographical territories, making a nuanced understanding of regional preferences and regulatory frameworks crucial for success.

Several powerful forces are propelling the global automotive competition tyre market forward, fueled by the inherent demand for superior performance and the expanding reach of motorsport. The unwavering passion for speed and technological excellence within professional motorsport categories like Formula, WEC, and GT racing serves as a primary driver. As automotive manufacturers pour billions into racing programs to hone their engineering prowess and brand image, the demand for cutting-edge tyres that can unlock maximum performance from their vehicles escalates. This constant push for milliseconds on the track directly translates into significant investment in research and development by tyre manufacturers, leading to continuous innovation in rubber compounds, tread patterns, and structural designs. Beyond the pinnacle of motorsport, the growing popularity of track days, amateur racing leagues, and enthusiast-driven events for Grand Tourer and Touring cars is creating a substantial secondary market. This expanding participation base requires a diverse range of competition-grade tyres that offer a balance of performance, durability, and accessibility. Furthermore, the increasing emphasis on driver development and driver training programs, often conducted on circuits, also contributes to the demand for tyres that provide predictable grip and feedback, allowing drivers to hone their skills safely and effectively. The technological spillover from Formula 1 and other top-tier series into lower racing categories and eventually into high-performance road-legal tyres also acts as a significant catalyst, creating a ripple effect of innovation and demand across the entire automotive ecosystem. The global expansion of automotive manufacturing and the increasing disposable income in emerging economies are also indirectly driving this market, as more individuals are able to participate in or follow motorsport. The inherent competitive nature of the automotive industry, where performance metrics are paramount, ensures that tyre technology will remain a critical area of focus and investment for years to come. The symbiotic relationship between automotive engineers and tyre specialists is crucial, as advancements in vehicle aerodynamics and power output necessitate equally advanced tyre solutions to translate that potential into tangible performance gains on the track.

Despite the robust growth potential, the automotive competition tyre market faces several significant challenges and restraints that can temper its expansion. One of the most prominent challenges is the intense cost associated with research and development. Creating cutting-edge competition tyres requires substantial investment in specialized materials, sophisticated testing equipment, and highly skilled personnel. This can create a barrier to entry for smaller players and place significant financial pressure on established manufacturers, particularly during economic downturns. The highly cyclical nature of motorsport itself can also be a restraint. Sponsorship budgets, regulatory changes, and the overall economic health of the automotive industry can directly impact the number of racing series, the level of competition, and consequently, the demand for specialized tyres. Furthermore, stringent homologation and regulatory requirements imposed by motorsport governing bodies can limit innovation. While these regulations ensure fairness and safety, they can also stifle the introduction of truly disruptive technologies if they don't fit within the established frameworks. Environmental concerns and sustainability pressures are also emerging as a restraint. The production and disposal of traditional rubber compounds can have an environmental impact, and there is increasing demand for greener alternatives. Developing sustainable competition tyres that can match the performance of conventional ones without significant cost increases presents a considerable technical hurdle. The limited addressable market for hyper-specialized tyres in niche racing categories can also be a restraint. While Formula 1 tyres garner significant attention, the volumes for extremely specialized tyres in very specific racing disciplines might not be as large as for broader applications. Supply chain disruptions, raw material price volatility, and geopolitical instability can also impact production costs and availability, posing further challenges to consistent market growth. The reliance on specific raw materials, some of which are subject to global commodity price fluctuations, adds another layer of uncertainty to cost management and pricing strategies.

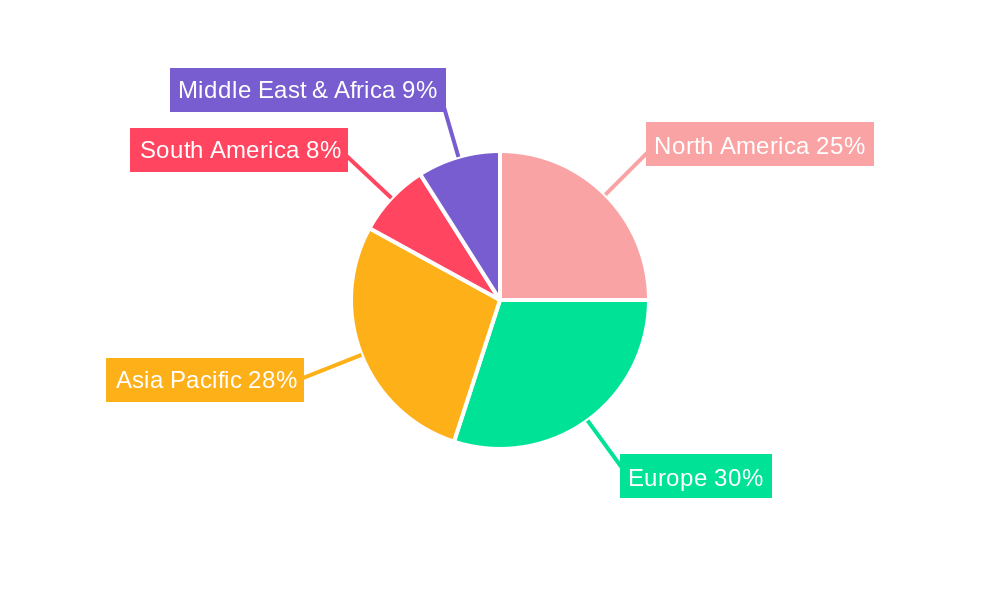

The global automotive competition tyre market is characterized by a dynamic interplay between key regions and specific product segments that consistently demonstrate dominance. Examining the Type segment, 18-inch tyres are poised to be a significant market dominator. This dominance stems from their widespread application across a multitude of popular racing disciplines, including GT racing, many forms of touring car championships, and increasingly, in high-performance club racing and track day events globally. The versatility and performance characteristics of 18-inch wheels and corresponding tyres make them a standard choice for a vast array of vehicles seeking competitive edge. The continued evolution of GT car designs and the popularity of these series, particularly in Europe and North America, solidify the 18-inch segment's leading position. The Application segment that will likely dominate is Grand Tourer (GT) and Touring. These categories represent a substantial portion of motorsport participation and viewership worldwide. The growth of series like the GT World Challenge, DTM, and various national touring car championships directly translates into a massive demand for specialised competition tyres. These tyres need to offer a sophisticated blend of grip, durability, and predictability to suit the diverse demands of endurance racing, sprint races, and varied track conditions. The substantial investment by automotive manufacturers in GT and touring car programs further amplifies the importance of this segment.

Geographically, Europe is expected to remain a dominant region, driven by its rich motorsport heritage and the presence of numerous high-profile racing series like Formula 1, WEC, and various national GT and touring car championships. The established automotive industry infrastructure, coupled with a strong enthusiast base, underpins this regional dominance. North America, particularly the United States, also represents a significant and growing market, fueled by the popularity of NASCAR, IndyCar, and IMSA sports car racing. The increasing investment in motorsport infrastructure and the growing participation in track day events contribute to its market strength. The Asia-Pacific region, with its rapidly expanding automotive market and growing interest in motorsport, presents a crucial area for future growth and potential dominance. While perhaps not yet at the same volume as Europe or North America, countries like Japan, China, and South Korea are witnessing increased investment in racing and automotive performance, indicating a strong future trajectory. The World Automotive Competition Tyre Production figures are directly influenced by these regional demands. The concentration of major tyre manufacturers with strong R&D capabilities in these dominant regions further reinforces their market leadership. The sheer volume of racing events, from professional championships to amateur club racing, across these key regions creates a consistent and substantial demand for various types and applications of competition tyres. The trend towards larger wheel sizes in performance vehicles, both on the road and on the track, further solidifies the dominance of the 18-inch tyre segment. The continuous evolution of vehicle technology, requiring more specialized tyre solutions, will continue to drive innovation and demand within these key segments and regions, making them the focal points for market analysis and strategic investment in the coming years.

Several key growth catalysts are propelling the automotive competition tyre industry forward. The increasing global participation in motorsport and track day events is a fundamental driver, expanding the customer base beyond professional racing. Furthermore, the relentless pursuit of technological advancements and performance enhancement by automotive manufacturers in their road-going vehicles, often validated through motorsport, fuels demand for cutting-edge tyre solutions. The spillover of technologies developed for elite racing series into more accessible categories also broadens the market appeal and adoption of advanced tyre features.

This report offers a comprehensive overview of the automotive competition tyre market, extending beyond a simple market size projection. It delves into the intricate details of World Automotive Competition Tyre Production by examining manufacturing capacities and key production hubs. The analysis includes a detailed breakdown of the market by Type, including the significant 18-inch, 15-inch, and 13-inch segments, as well as 'Others', providing granular insights into each category's market share and growth potential. Furthermore, the report scrutinizes the market across diverse Application segments such as Grand Tourer, Touring, Formula, Rally, and Others, highlighting the unique demands and innovations prevalent in each. The Industry Developments section meticulously tracks significant advancements, technological breakthroughs, and regulatory changes impacting the sector. This holistic approach ensures that stakeholders gain a profound understanding of the market's past, present, and future landscape.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.26% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 8.26%.

Key companies in the market include Pirelli, Goodyear, Hankook Tire, Michelin, Bridgestone, Yokohama, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive Competition Tyre," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Competition Tyre, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.