1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Carbon Fiber Composites Parts?

The projected CAGR is approximately 12%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Automotive Carbon Fiber Composites Parts

Automotive Carbon Fiber Composites PartsAutomotive Carbon Fiber Composites Parts by Type (Brake Discs, Brake Pads, Battery Housing, Mirror Housing, Chassis, Pillars, Other), by Application (OEM, Aftermarket), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

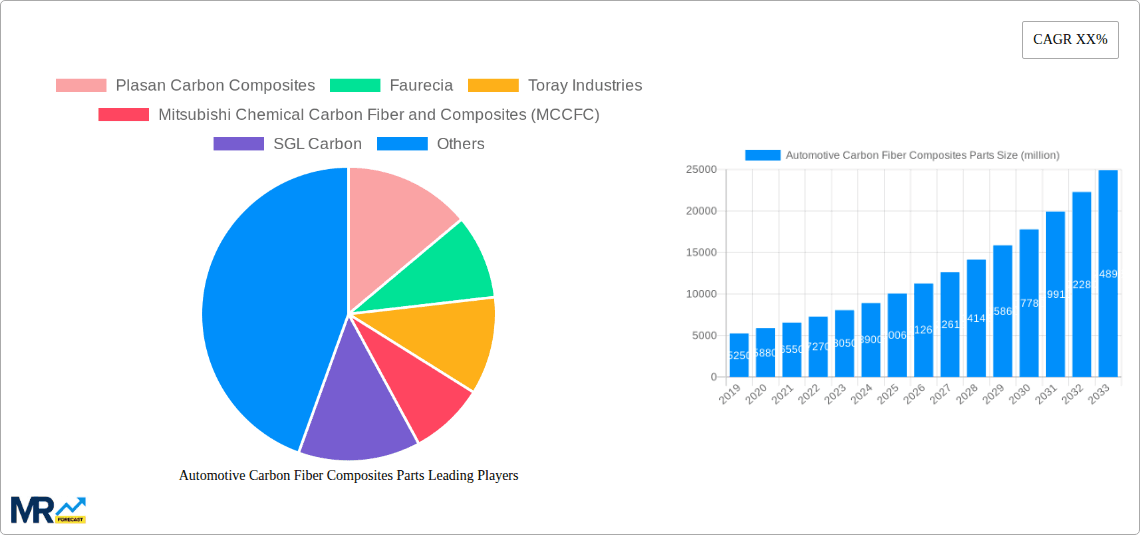

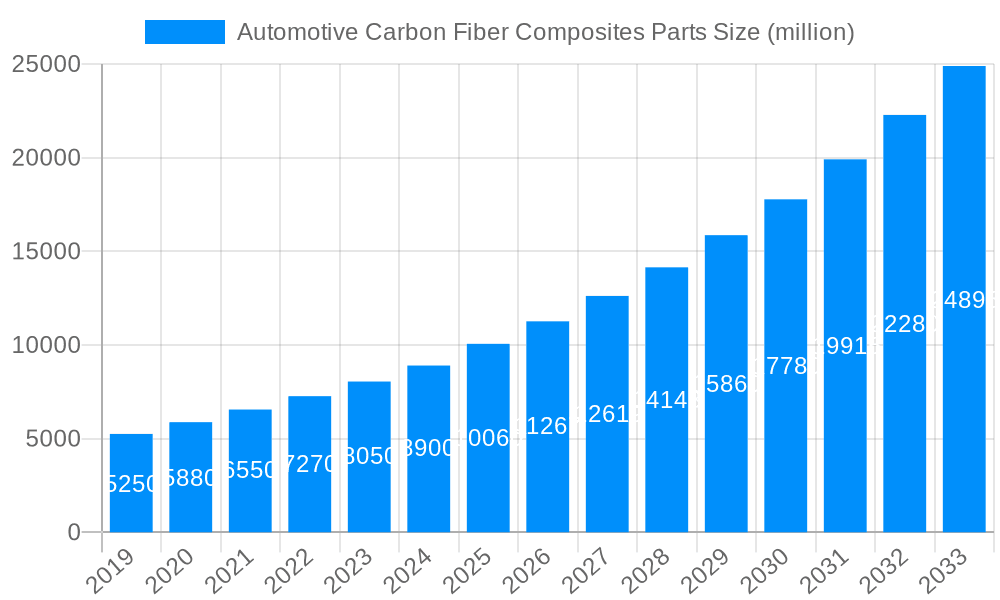

The global Automotive Carbon Fiber Composites Parts market is poised for substantial growth, projected to reach an estimated $10.06 billion by 2025, with a remarkable Compound Annual Growth Rate (CAGR) of 12% expected to drive its expansion throughout the forecast period of 2025-2033. This robust expansion is primarily fueled by the automotive industry's relentless pursuit of lightweighting solutions to enhance fuel efficiency, reduce emissions, and improve overall vehicle performance. The increasing adoption of advanced materials like carbon fiber composites in structural components, such as chassis, pillars, and battery housings for electric vehicles (EVs), is a significant driver. Furthermore, the growing demand for high-performance vehicles and the stringent regulatory landscape pushing for lower CO2 emissions are propelling the market forward. Innovations in manufacturing processes and the declining cost of carbon fiber production are also contributing to wider adoption across various vehicle segments.

The market’s growth trajectory is further shaped by distinct trends and segment dynamics. The OEM segment is anticipated to maintain its dominance, driven by long-term supply agreements and the integration of carbon fiber composites in new vehicle platforms. Simultaneously, the aftermarket segment is expected to witness significant growth as consumers seek to upgrade existing vehicles for improved performance and aesthetics. Key product segments, including brake discs and pads, are experiencing increased adoption due to their superior performance characteristics. Geographically, Asia Pacific is emerging as a pivotal region, driven by the burgeoning automotive manufacturing hubs in China and India, coupled with significant investments in R&D and technological advancements. While the high cost of carbon fiber and complex manufacturing processes remain as restraints, ongoing technological advancements and economies of scale are gradually mitigating these challenges, paving the way for a highly dynamic and promising market.

Here is a unique report description on Automotive Carbon Fiber Composites Parts, incorporating your specified elements:

The automotive carbon fiber composites parts market is experiencing a significant upward trajectory, projected to witness substantial growth over the study period of 2019-2033. With a base year of 2025 serving as a pivotal point, the market is estimated to reach a valuation of XXX billion USD by 2025, with robust expansion expected throughout the forecast period of 2025-2033. This surge is underpinned by a confluence of factors, primarily driven by the relentless pursuit of vehicle lightweighting to enhance fuel efficiency and reduce emissions. Automakers are increasingly embracing carbon fiber composites as a superior alternative to traditional metals, particularly in performance vehicles, electric vehicles (EVs), and luxury segments. The historical performance from 2019-2024 laid the groundwork for this accelerated growth, characterized by a gradual but steady integration of these advanced materials.

The burgeoning EV sector is a particularly potent catalyst, as battery weight is a critical concern for range and performance. Carbon fiber's exceptional strength-to-weight ratio makes it ideal for constructing lightweight yet robust battery housings, contributing directly to improved vehicle dynamics and energy efficiency. Beyond battery components, the application spectrum is broadening significantly. From intricate Mirror Housing and structural Chassis components to high-performance Brake Discs and Brake Pads, the adoption of carbon fiber is expanding across various vehicle systems. This widespread integration, facilitated by advancements in manufacturing technologies and a growing understanding of material properties, is reshaping automotive design and engineering paradigms. The market's evolution is not merely about replacing existing parts; it's about enabling entirely new design possibilities and performance benchmarks, ultimately pushing the boundaries of what is achievable in automotive engineering. The increasing demand for customized and high-performance solutions further fuels the market, as carbon fiber offers unparalleled design flexibility.

The automotive carbon fiber composites parts market is being propelled forward by a powerful synergy of technological advancements, stringent regulatory landscapes, and evolving consumer preferences. The global push towards sustainability and reduced environmental impact is a primary driver, with governments worldwide implementing stricter emissions standards. Carbon fiber's inherent lightweight properties directly contribute to enhanced fuel efficiency in internal combustion engine vehicles and increased range in electric vehicles, making it an indispensable material for meeting these regulatory demands. Furthermore, the inherent strength and stiffness of carbon fiber composites translate to improved vehicle safety and performance. This is particularly appealing in the high-performance and luxury vehicle segments, where enhanced driving dynamics and superior structural integrity are paramount.

The continuous innovation in manufacturing processes, including advancements in automated fiber placement, resin transfer molding, and additive manufacturing for composites, has significantly reduced production costs and lead times, making carbon fiber more accessible for mass production. This technological evolution is democratizing the use of these advanced materials, enabling their integration into a wider array of vehicle models and segments. The growing interest in lightweight construction for improved handling, acceleration, and braking further solidifies carbon fiber's position. As the cost-effectiveness of carbon fiber production continues to improve, its adoption will likely permeate into mid-range and even some budget-conscious vehicle segments, further accelerating market expansion.

Despite the robust growth trajectory, the automotive carbon fiber composites parts market faces several significant challenges and restraints that could temper its full potential. The primary hurdle remains the cost of raw materials and manufacturing. While advancements are being made, the production of carbon fiber itself and the intricate processes involved in creating composite parts are still considerably more expensive than those for traditional materials like steel and aluminum. This cost differential can be a deterrent for mass-market vehicle manufacturers, limiting its widespread adoption to higher-end and performance-oriented vehicles.

Another significant concern is the complex repairability of carbon fiber components. Unlike metal parts that can be easily repaired or replaced, damaged carbon fiber parts often require specialized expertise and equipment for repair, or outright replacement, which can be costly and time-consuming for consumers and repair shops. This lack of widespread repair infrastructure can create hesitancy in adoption. Furthermore, the recycling and end-of-life management of carbon fiber composites present a growing environmental challenge. While efforts are underway to develop effective recycling methods, current processes can be energy-intensive and may not always yield high-quality recycled materials, leading to concerns about the long-term sustainability of widespread carbon fiber usage. The initial capital investment required for tooling and manufacturing facilities equipped to handle carbon fiber composites can also be a significant barrier for smaller automotive manufacturers or suppliers looking to transition to these materials.

The OEM application segment is poised to dominate the automotive carbon fiber composites parts market, driven by the inherent design and engineering integration required at the vehicle manufacturing stage. Automakers are increasingly specifying carbon fiber components for their new vehicle platforms, particularly in the pursuit of lightweighting for fuel efficiency and performance. This proactive integration at the design phase ensures that the full benefits of carbon fiber – its strength, stiffness, and design flexibility – are realized from the outset. The Chassis segment, in particular, represents a substantial area of dominance within the OEM application. The development of full carbon fiber monocoque chassis or significant chassis reinforcements using composites offers unparalleled improvements in structural rigidity, weight reduction, and overall vehicle dynamics. This allows for enhanced handling, improved crashworthiness, and the potential for novel vehicle architectures, especially crucial for the development of electric vehicles where battery integration and weight distribution are critical.

Furthermore, the Battery Housing segment is experiencing explosive growth within the OEM application, directly fueled by the burgeoning electric vehicle market. The need for lightweight, strong, and thermally managed battery enclosures makes carbon fiber composites an ideal solution. Their ability to be molded into complex shapes also facilitates efficient battery pack design and integration. The Application in Chassis components extends beyond the primary structure to include elements like subframes, suspension components, and driveline parts, where weight savings directly translate to improved performance and efficiency.

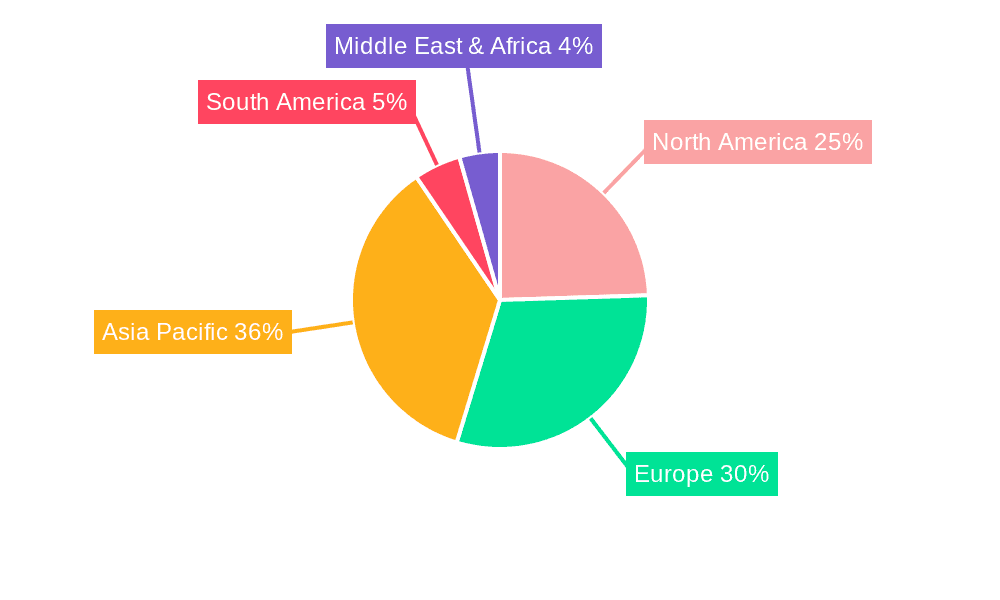

Geographically, North America and Europe are anticipated to lead the market, primarily due to the strong presence of premium and performance vehicle manufacturers, alongside stringent environmental regulations pushing for lightweighting solutions. The high concentration of R&D centers and a forward-thinking approach to adopting advanced materials in these regions further solidify their dominance.

Dominant Segments:

Key Regions:

The OEM application, especially for chassis and battery housings, coupled with the leadership of North America and Europe, paints a clear picture of where the market's most significant value and volume will be generated. The continuous innovation in these areas by leading manufacturers will ensure sustained demand and market dominance.

The growth of the automotive carbon fiber composites parts industry is significantly accelerated by several key catalysts. The relentless pursuit of vehicle lightweighting to meet fuel efficiency standards and reduce emissions is a paramount driver. Furthermore, the burgeoning electric vehicle (EV) market necessitates lightweight battery enclosures for extended range. Advancements in manufacturing technologies, such as automation and improved resin systems, are reducing costs and increasing production scalability. Finally, the growing consumer demand for high-performance vehicles with superior handling and dynamics further fuels the adoption of these advanced materials.

This comprehensive report offers an in-depth analysis of the automotive carbon fiber composites parts market, spanning the study period of 2019-2033. It provides a detailed outlook on market trends, growth drivers, and key challenges, with a base year of 2025 and an estimated market valuation of XXX billion USD for 2025. The report delves into the critical factors propelling the industry forward, including the relentless demand for lightweighting, the exponential growth of the electric vehicle sector, and continuous advancements in manufacturing technologies. It also meticulously examines the restraints, such as high costs and repairability issues. Furthermore, the report highlights the dominant market segments and regions, with a particular focus on the OEM application for chassis and battery housings, and the leading roles of North America and Europe. The report includes a thorough list of key players and significant developments that have shaped and will continue to influence the market landscape.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 12%.

Key companies in the market include Plasan Carbon Composites, Faurecia, Toray Industries, Mitsubishi Chemical Carbon Fiber and Composites (MCCFC), SGL Carbon, Composite Resources, Hexcel Corporation, TEIJIN LIMITED, CPC SRL, Mubea, HP Composites, Cotesa, Sparco, Formaplex, Bucci Composites, CBS Composites, Cobra Advanced Composites, TOPKEY Excellence In Composites, Action Composite Technology Limited, Zhongfu Shenying Carbon Fiber Xining, HengruiGroup, Martec Composite, Gigantex Corporation, CF Composite, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Automotive Carbon Fiber Composites Parts," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automotive Carbon Fiber Composites Parts, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.