1. What is the projected Compound Annual Growth Rate (CAGR) of the Automobile Clutch?

The projected CAGR is approximately 3.9%.

Automobile Clutch

Automobile ClutchAutomobile Clutch by Type (Dry Clutch, Wet Clutch), by Application (Passenger Vehicles, Commercial Vehicles), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

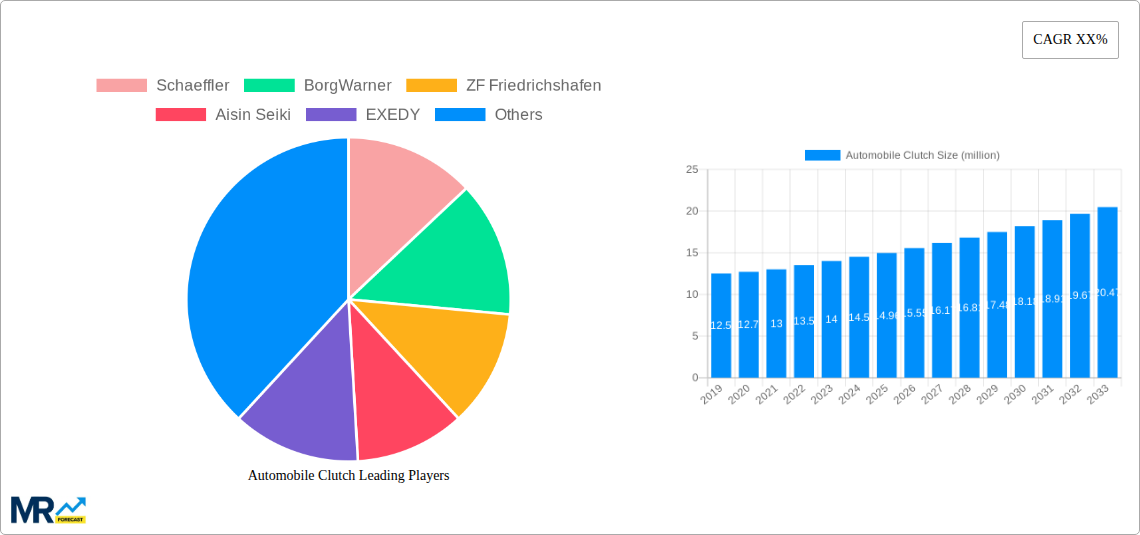

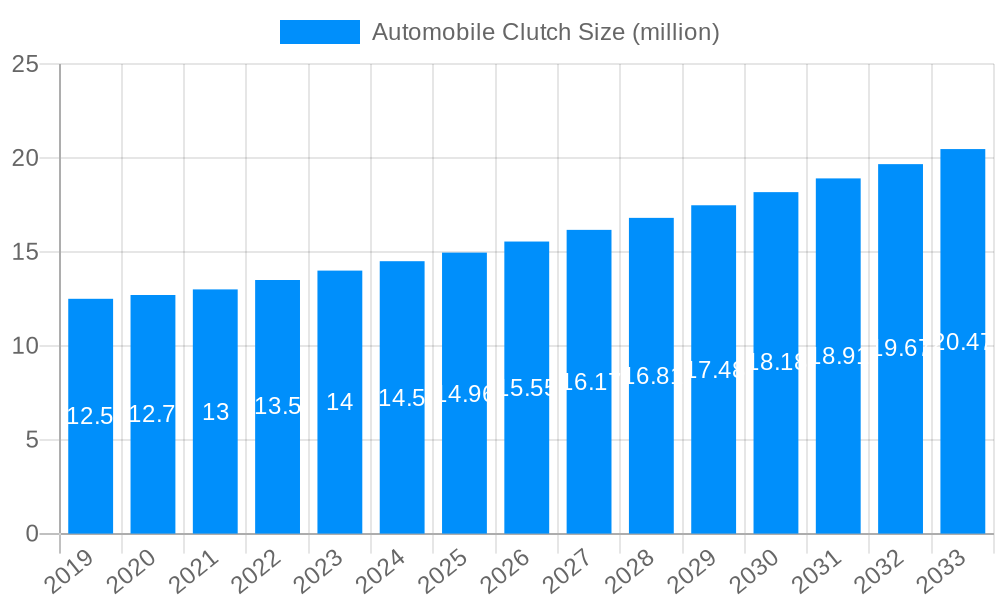

The global automobile clutch market is projected to reach a substantial valuation, estimated at approximately $14.96 billion by 2025, with a steady Compound Annual Growth Rate (CAGR) of 3.9% anticipated to drive its expansion through 2033. This growth trajectory is underpinned by several key factors. The increasing global vehicle production, particularly in emerging economies, directly fuels demand for clutch systems. Furthermore, the continuous evolution of automotive technology, including advancements in transmission systems and the integration of smarter clutch functionalities, contributes to market vitality. The rising consumer preference for enhanced driving comfort and performance, which modern clutch designs readily address, also plays a significant role. Additionally, the aftermarket segment, driven by regular maintenance and replacement needs, represents a consistent revenue stream for clutch manufacturers and suppliers. The market is characterized by a strong emphasis on innovation, with companies actively investing in research and development to introduce more efficient, durable, and cost-effective clutch solutions, including those catering to evolving powertrain technologies.

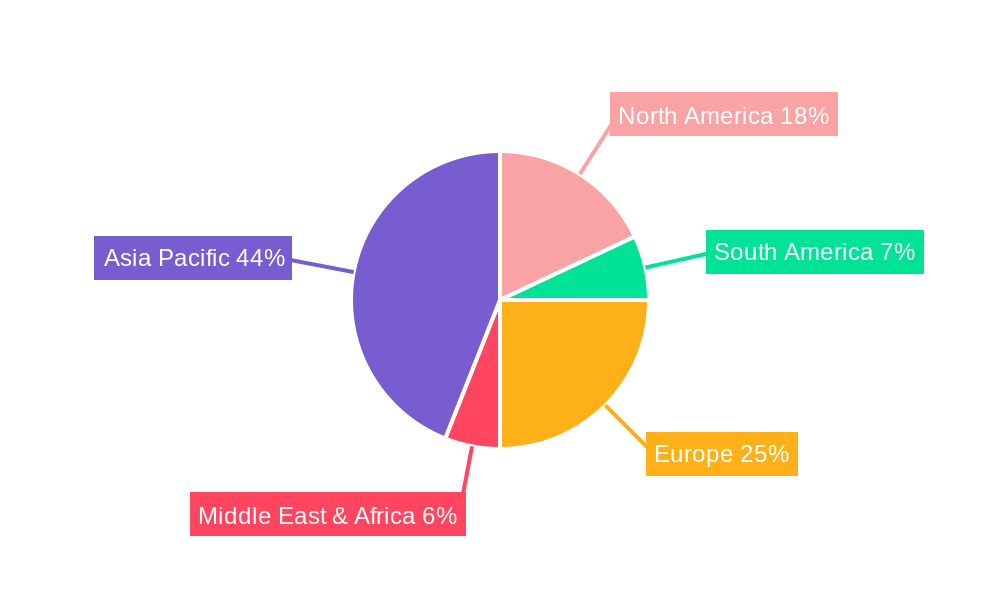

The market is segmented by clutch type into Dry Clutch and Wet Clutch, with applications spanning both Passenger Vehicles and Commercial Vehicles. Dry clutches, commonly found in manual transmissions, continue to hold a significant share due to their cost-effectiveness and widespread adoption in many vehicle segments. However, wet clutches are gaining prominence, especially in automatic and dual-clutch transmission systems, offering smoother engagement, better heat dissipation, and enhanced performance, particularly in high-torque applications and performance vehicles. Geographically, the Asia Pacific region, led by China and India, is expected to be a dominant force due to its massive vehicle production and burgeoning automotive industry. North America and Europe also represent substantial markets, driven by a large existing vehicle parc, stringent emission standards necessitating efficient powertrain components, and the presence of leading automotive manufacturers and aftermarket service providers. The Middle East & Africa and South America present emerging growth opportunities, albeit with varying paces of adoption and market maturity.

Here is a unique report description for the Automobile Clutch market, incorporating your specified elements:

This in-depth report delves into the global automobile clutch market, providing a holistic view of its present landscape, historical trajectory, and future projections. Spanning the study period of 2019 to 2033, with a base year of 2025 and an estimated year also of 2025, the report meticulously analyzes the market's dynamics, segmented by clutch type, vehicle application, and key industry developments. We offer an exhaustive forecast for the forecast period of 2025-2033, building upon the insights garnered from the historical period of 2019-2024. This research aims to equip stakeholders with critical market intelligence, enabling informed strategic decision-making in this vital automotive component sector.

The global automobile clutch market is poised for significant evolution, driven by a complex interplay of technological advancements, evolving consumer preferences, and stringent regulatory landscapes. The market, projected to be valued in the hundreds of billions of dollars by 2025, is witnessing a steady shift towards more sophisticated and efficient clutch systems. A key trend is the increasing integration of advanced clutch technologies in both passenger and commercial vehicles, aimed at enhancing fuel efficiency, reducing emissions, and improving drivability. The burgeoning demand for automatic and semi-automatic transmission systems, while traditionally requiring more complex clutch mechanisms, is a major driver. Furthermore, the growing adoption of hybrid and electric vehicles (EVs) presents a dual-edged trend. While EVs, in their purest form, do not inherently require traditional clutches, the development of hybrid powertrains often necessitates advanced clutch solutions for seamless power management between the electric motor and internal combustion engine. Consequently, the market is experiencing a bifurcation, with a continued demand for robust and reliable dry and wet clutch systems in conventional powertrains, alongside a growing segment focused on specialized clutch solutions for hybrid architectures. The aftermarket segment also remains a crucial contributor, driven by replacement needs and the increasing average age of vehicle fleets worldwide. Understanding these nuanced trends is paramount for stakeholders navigating the competitive automotive clutch landscape. The market is also characterized by a growing emphasis on lightweight materials and reduced friction, contributing to overall vehicle performance and sustainability goals. The increasing complexity of modern vehicle powertrains necessitates advanced clutch control systems that can adapt to diverse driving conditions and optimize power delivery, further fueling innovation in this sector. The proliferation of advanced driver-assistance systems (ADAS) and the eventual push towards autonomous driving will also necessitate sophisticated clutch actuation and control strategies. The aftermarket, fueled by the global vehicle parc, will continue to be a substantial revenue stream, with a focus on high-quality replacement parts and innovative solutions for older vehicle models.

Several potent forces are collectively driving the growth and transformation of the global automobile clutch market. The ever-increasing global vehicle production, particularly in emerging economies, forms the bedrock of demand for clutches. As more vehicles are manufactured, the direct correlation with the need for clutch systems, both for new installations and subsequent replacements, becomes evident. Consumer preference for enhanced driving comfort and convenience is a significant catalyst, propelling the adoption of automatic and dual-clutch transmission (DCT) systems, which inherently rely on sophisticated clutch technology. This demand is not limited to passenger vehicles; commercial vehicles are also increasingly benefiting from automated manual transmissions (AMTs) and DCTs, leading to improved operational efficiency and driver fatigue reduction. Furthermore, stringent government regulations concerning fuel economy and emissions are indirectly bolstering the market. Manufacturers are compelled to develop lighter, more efficient clutches that contribute to overall vehicle fuel efficiency, thus meeting regulatory targets. This pursuit of efficiency also extends to the development of wet clutches with improved lubrication and reduced drag, as well as advanced friction materials that optimize torque transfer and minimize energy loss. The growing aftermarket segment, driven by the global vehicle parc and the need for timely replacements, also plays a crucial role. As vehicles age, the demand for replacement clutches steadily increases, providing a consistent revenue stream for market players. The increasing complexity of modern vehicle powertrains, including the integration of hybrid technologies, further necessitates the development of specialized and advanced clutch solutions, creating new avenues for growth and innovation within the market.

Despite the robust growth drivers, the automobile clutch market is not without its impediments. The most significant challenge stems from the accelerating transition towards fully electric vehicles (EVs). As EVs gain market share, the demand for traditional clutch systems in pure electric configurations diminishes significantly. While hybrid vehicles still necessitate clutches, their eventual displacement by battery-electric powertrains poses a long-term threat to the established clutch market. The intense price competition among manufacturers, coupled with the commoditization of certain clutch components, puts considerable pressure on profit margins. This is particularly true in the aftermarket segment, where cost-effectiveness is a primary concern for consumers. Volatility in raw material prices, such as steel, iron, and specialized friction materials, can impact production costs and subsequently affect pricing strategies. Geopolitical uncertainties and supply chain disruptions, as evidenced in recent years, can also lead to production delays and increased costs. Furthermore, the intricate nature of clutch system development and manufacturing requires substantial investment in research and development (R&D) to keep pace with evolving vehicle technologies. The high cost associated with R&D, coupled with the need for specialized manufacturing processes, can be a barrier for smaller players. The increasing complexity of vehicle electronics and control systems also demands seamless integration of clutch actuation, which requires significant engineering expertise and can be a point of contention during development. Lastly, the long product development cycles in the automotive industry mean that adapting to rapid technological shifts, such as the acceleration of EV adoption, can be a protracted process.

The global automobile clutch market is characterized by regional dominance and segment supremacy, with distinct patterns shaping its landscape.

Dominant Segments:

Application: Passenger Vehicles: This segment consistently commands the largest share of the automobile clutch market. The sheer volume of passenger vehicle production globally, coupled with the increasing demand for convenience features like automatic transmissions, fuels this dominance. As per our analysis, the passenger vehicle segment is projected to contribute over seventy percent of the global market revenue in 2025, with continued strong performance through the forecast period. This is further amplified by the growing middle class in developing nations, leading to increased passenger car ownership.

Type: Dry Clutch: Dry clutches remain the predominant type of clutch used in the majority of passenger vehicles and a significant portion of commercial vehicles due to their cost-effectiveness, simplicity, and efficiency in many applications. Their widespread adoption in manual and automated manual transmissions ensures their continued market leadership. In 2025, dry clutches are estimated to hold a market share of approximately sixty-five percent of the total clutch market value.

Dominant Regions/Countries:

Asia Pacific: This region is the undisputed leader in the global automobile clutch market, driven by its status as the world's manufacturing hub for automobiles. Countries like China, Japan, South Korea, and India are not only major producers of vehicles but also significant consumers of clutches. The burgeoning automotive industry in these nations, fueled by growing disposable incomes and increasing urbanization, translates into a massive demand for all types of clutches. Asia Pacific's market share is projected to be around forty-five percent in 2025, with a robust compound annual growth rate (CAGR) expected throughout the forecast period.

Europe: Europe, with its strong automotive manufacturing base and stringent emission standards, also represents a significant market for automobile clutches. The region is a leader in the adoption of advanced technologies, including DCTs and specialized clutches for hybrid powertrains. Europe is anticipated to hold a market share of approximately twenty-five percent in 2025.

The dominance of passenger vehicles and dry clutches, coupled with the manufacturing and consumption power of the Asia Pacific region, particularly China, forms the core of the global automobile clutch market's current and projected future. The increasing adoption of dual-clutch transmissions in passenger cars is also expected to drive significant growth within the dry clutch segment.

The automobile clutch industry is experiencing robust growth fueled by several key catalysts. The escalating global demand for vehicles, especially in emerging economies, directly translates to increased clutch production and consumption. Furthermore, the rising consumer preference for automated and semi-automatic transmissions, which necessitate advanced clutch systems, is a significant growth propeller. This trend is further amplified by the continuous drive for improved fuel efficiency and reduced emissions, pushing manufacturers to innovate and develop more efficient clutch technologies. The burgeoning aftermarket segment, driven by the increasing vehicle parc and replacement needs, also provides a stable and consistent revenue stream. The ongoing development of hybrid powertrains, which still incorporate clutch mechanisms for power management, offers a crucial bridge during the transition to full electrification.

This comprehensive report provides an exhaustive analysis of the global automobile clutch market, delving into its intricate workings from 2019 to 2033. With 2025 serving as both the base and estimated year, the report offers detailed projections for the forecast period of 2025-2033, building upon insights from the historical period of 2019-2024. It meticulously examines market segmentation by clutch type (Dry Clutch, Wet Clutch) and application (Passenger Vehicles, Commercial Vehicles), alongside significant industry developments. The report identifies key market drivers, including the growing global vehicle parc and the shift towards automated transmissions, while also addressing critical challenges such as the rise of electric vehicles and intense market competition. Regional analysis highlights the dominance of Asia Pacific, particularly China, in both production and consumption. Leading players and their strategic initiatives are thoroughly investigated. This report offers invaluable market intelligence for all stakeholders, enabling strategic planning and decision-making within this dynamic automotive component sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.9% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 3.9%.

Key companies in the market include Schaeffler, BorgWarner, ZF Friedrichshafen, Aisin Seiki, EXEDY, FTE Automotive, AMS Automotive, Valeo, Setco Automotive, Bosch, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Automobile Clutch," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Automobile Clutch, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.