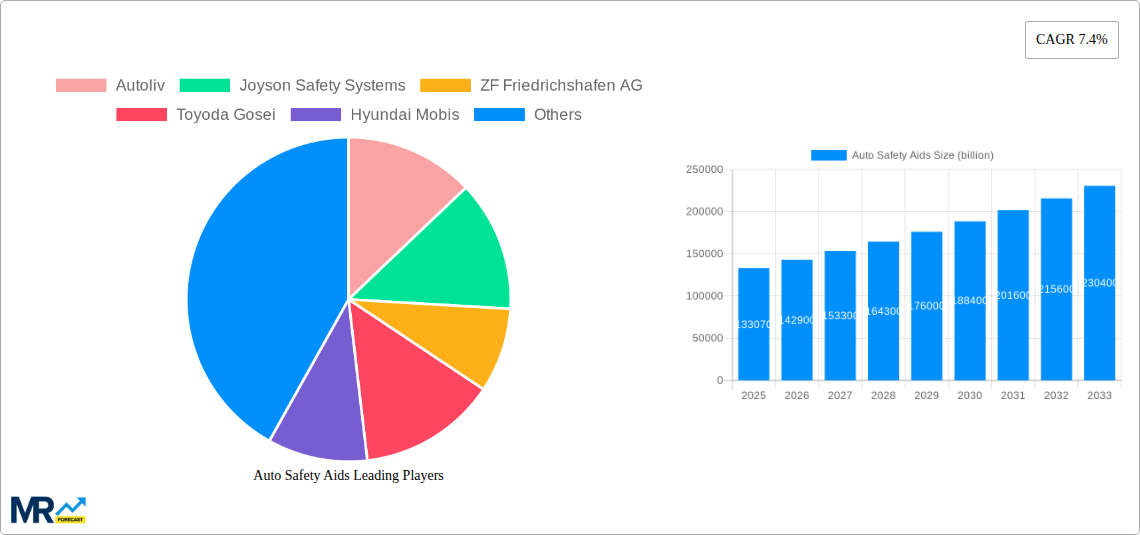

1. What is the projected Compound Annual Growth Rate (CAGR) of the Auto Safety Aids?

The projected CAGR is approximately 7.4%.

Auto Safety Aids

Auto Safety AidsAuto Safety Aids by Type (Seat Belts, Airbag, Anti-lock Brake System, High Brake Lamp), by Application (Car, Bus, Truck, Special Purpose Vehicle), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

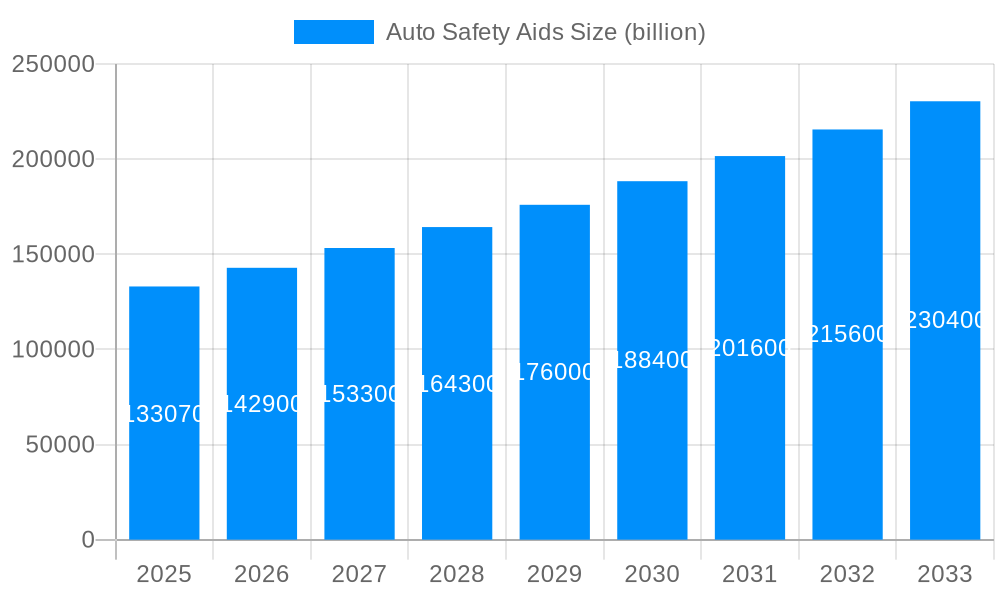

The global Auto Safety Aids market is poised for robust growth, projected to reach USD 133.07 billion by 2025, with a compound annual growth rate (CAGR) of 7.4% expected to drive the market through 2033. This significant expansion is fueled by a confluence of factors, including increasingly stringent government regulations mandating advanced safety features in vehicles, a growing consumer awareness and demand for enhanced vehicle safety, and the relentless innovation in automotive technology. The rising adoption of sophisticated safety systems like airbags, anti-lock braking systems (ABS), and high brake lamps is a direct response to these pressures, aiming to reduce road fatalities and injuries. Furthermore, the burgeoning automotive industry, particularly in emerging economies, and the increasing production of passenger cars, buses, and trucks are creating a larger addressable market for these essential safety components. The drive towards semi-autonomous and autonomous driving technologies also necessitates more advanced and integrated safety aid systems, further propelling market expansion.

The market is segmented into key product types such as Seat Belts, Airbag, Anti-lock Brake System, and High Brake Lamp, catering to diverse applications across Cars, Buses, Trucks, and Special Purpose Vehicles. Geographically, the Asia Pacific region, led by China and India, is anticipated to witness the fastest growth due to its massive automotive production and a rapidly expanding middle class with a growing preference for safer vehicles. North America and Europe, established automotive markets with mature safety regulations and high consumer spending on vehicle features, will continue to be significant revenue contributors. Key industry players like Autoliv, Joyson Safety Systems, and ZF Friedrichshafen AG are actively investing in research and development to introduce next-generation safety technologies, focusing on lightweight materials, enhanced sensor integration, and intelligent warning systems. Challenges, such as the high cost of advanced safety systems and potential consumer resistance due to price sensitivity, are being addressed through technological advancements that improve cost-effectiveness and wider integration across vehicle segments.

This comprehensive report delves into the intricate dynamics of the global Auto Safety Aids market, offering a detailed analysis of its growth trajectory, key drivers, prevailing challenges, and future outlook. Spanning a study period from 2019 to 2033, with a base year of 2025, the report provides in-depth insights into the market's performance during the historical period (2019-2024) and projects its evolution through the forecast period (2025-2033). The analysis incorporates crucial market intelligence, including an estimated market size of $150 billion in 2025, and anticipates a significant expansion reaching an estimated $280 billion by 2033.

The global Auto Safety Aids market is currently experiencing a robust expansion driven by a confluence of factors, most notably the increasing adoption of advanced safety technologies and stringent government regulations mandating their integration in vehicles. The market size, estimated at $150 billion in 2025, is poised for substantial growth, projected to reach $280 billion by 2033. This upward trend is underpinned by a growing consumer awareness of vehicle safety and a rising demand for features that enhance occupant protection. The evolution of automotive technology, particularly the integration of Artificial Intelligence (AI) and sensor technologies, is paving the way for more sophisticated safety systems. For instance, advancements in airbag technology, from traditional frontal airbags to sophisticated multi-stage deployment systems and side-curtain airbags, are becoming standard. Similarly, the anti-lock braking system (ABS) has evolved into electronic stability control (ESC) and further into advanced driver-assistance systems (ADAS) that preemptively mitigate accident risks. The passenger car segment is currently the largest contributor to the market revenue, driven by high production volumes and an increasing emphasis on premium safety features in new vehicle models. However, the commercial vehicle segment, including buses and trucks, is also witnessing accelerated growth as safety regulations become more comprehensive across all vehicle types. The "high brake lamp" segment, while seemingly a basic safety feature, is also benefiting from technological advancements, with integrated LED and intelligent lighting systems improving visibility and signaling. The industry is also observing a trend towards the integration of these safety aids into a cohesive safety ecosystem within the vehicle, where different systems communicate and collaborate to provide holistic protection. This interconnectedness, coupled with the increasing sophistication of automotive electronics, is a defining characteristic of the current market landscape. Furthermore, the growing interest in autonomous driving technologies, while not directly an "aid" in the traditional sense, necessitates and drives the development of highly advanced sensing and control systems that are intrinsically linked to safety. The aftermarket segment for safety aids is also expanding, offering consumers an avenue to retrofit older vehicles with enhanced safety features, further contributing to the overall market valuation. The increasing focus on pedestrian safety, with systems designed to detect and alert drivers to pedestrians, is another emerging trend that will significantly shape the future of the auto safety aids market. The overarching narrative for auto safety aids is one of continuous innovation, driven by both regulatory pressures and the proactive pursuit of enhanced vehicle security and occupant well-being.

The Auto Safety Aids market is propelled by a powerful synergy of evolving regulatory frameworks, escalating consumer demand for enhanced safety, and rapid technological advancements. Governments worldwide are increasingly implementing stringent safety standards, mandating the inclusion of critical safety features like airbags and ABS in new vehicles. This regulatory push creates a consistent and growing demand for these safety components. Simultaneously, heightened consumer awareness regarding the importance of vehicle safety, fueled by media coverage of accidents and the availability of safety ratings, is compelling manufacturers to prioritize and integrate advanced safety systems. Consumers are no longer viewing safety features as optional add-ons but as essential requirements, willing to invest in vehicles equipped with the latest protective technologies. Furthermore, the relentless pace of technological innovation is a significant driver. The integration of sophisticated sensors, processors, and software is enabling the development of more intelligent and proactive safety systems. Features like autonomous emergency braking, lane departure warning, and blind-spot monitoring are becoming increasingly common, moving beyond passive protection to active accident prevention. The growing maturity of the automotive industry, particularly in emerging economies, is also contributing to market expansion. As disposable incomes rise, consumers are increasingly able to afford vehicles equipped with advanced safety features. The shift towards electric vehicles (EVs) also plays a role, as EV manufacturers are often at the forefront of adopting and integrating cutting-edge safety technologies, setting new benchmarks for the industry. The overarching trend is a proactive approach to safety, moving from reactive measures to preventative ones, a paradigm shift driven by these fundamental forces.

Despite the robust growth, the Auto Safety Aids market faces several challenges and restraints that could temper its expansion. One of the primary restraints is the cost of implementation. Advanced safety features, while beneficial, significantly increase the manufacturing cost of vehicles. This can be a deterrent for price-sensitive consumers and may limit the adoption of these technologies in entry-level or budget-friendly vehicles, particularly in developing markets. The complexity of integration and the need for rigorous testing and validation of these sophisticated systems also pose significant hurdles. Ensuring the seamless and reliable functioning of interconnected safety systems requires substantial investment in research and development, as well as extensive testing protocols to meet safety and regulatory standards. Cybersecurity concerns are also emerging as a critical challenge. As vehicles become more connected and reliant on software, the risk of cyberattacks that could compromise safety systems is a growing apprehension for both manufacturers and consumers. Ensuring the integrity and security of these systems is paramount and requires continuous vigilance and investment. Standardization and regulatory fragmentation across different regions can also create complexities for global manufacturers. Developing safety systems that meet diverse and sometimes conflicting regulatory requirements adds to development costs and timelines. Furthermore, consumer understanding and perception of the efficacy and necessity of certain advanced safety features can be a barrier. Some consumers may still perceive these as unnecessary gadgets, requiring extensive education and marketing efforts to build trust and awareness. Finally, supply chain disruptions, as witnessed in recent years, can impact the availability and cost of critical components required for the manufacturing of auto safety aids, thereby affecting production volumes and market accessibility.

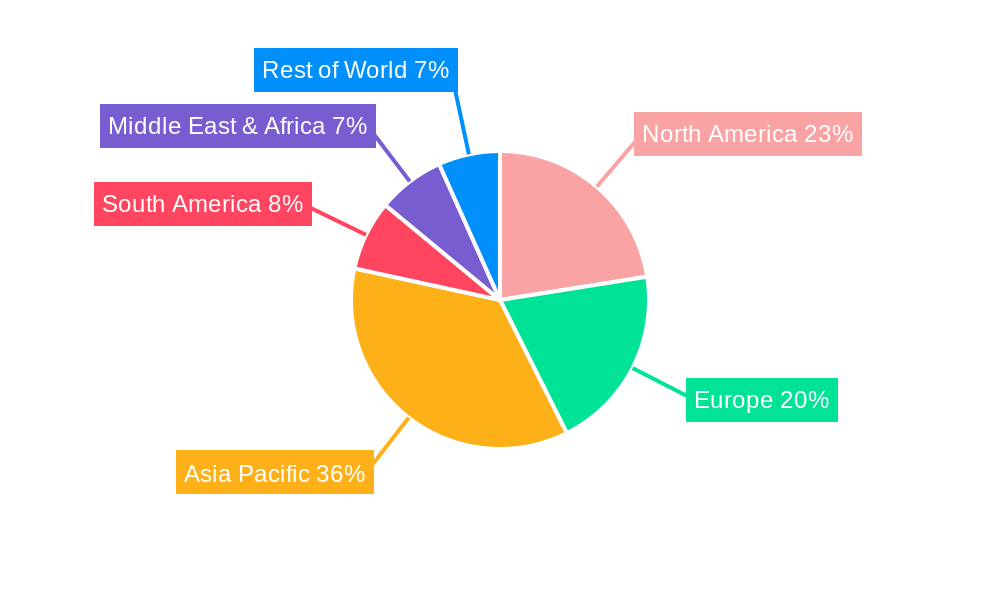

The Asia-Pacific region, driven primarily by China and India, is poised to dominate the Auto Safety Aids market in the coming years, largely due to the burgeoning automotive sector, increasing disposable incomes, and rapidly evolving regulatory landscape. This dominance will be further amplified by the significant demand within the Car segment, which represents the largest application area for safety aids. The sheer volume of passenger car production and sales in these nations, coupled with a growing emphasis on vehicle safety by both government agencies and consumers, positions Asia-Pacific at the forefront.

In terms of Type, Seat Belts are expected to maintain their position as a foundational safety aid, witnessing consistent demand driven by ongoing production and mandatory regulations. However, the Airbag segment is anticipated to experience a more dynamic growth trajectory. This is attributed to the increasing inclusion of multi-stage airbags, side-curtain airbags, and knee airbags as standard or optional features in a wider range of vehicle models. Manufacturers are also focusing on enhancing airbag performance and integrating them with other safety systems for a more comprehensive occupant protection strategy. The market for Anti-lock Brake System (ABS), while already mature, will continue to be a significant contributor, especially with its integration into more advanced braking and stability control systems.

The Car segment is undeniably the largest and fastest-growing application within the Auto Safety Aids market. This is a direct consequence of the global automotive industry's focus on passenger vehicles, which constitute the majority of vehicle production and sales. The increasing consumer preference for personal mobility, coupled with the rising middle class in emerging economies, fuels the demand for cars. Manufacturers are responding to this demand by incorporating a wide array of advanced safety features into their car models to enhance competitiveness and meet consumer expectations.

In contrast, while Bus and Truck segments are crucial for safety, their market share in the Auto Safety Aids sector is comparatively smaller than that of passenger cars. This is primarily due to lower production volumes and a more specialized application base. However, these segments are also witnessing growth, driven by stricter regulations for commercial vehicle safety, particularly in developed economies, and the increasing demand for enhanced driver comfort and fatigue reduction systems. The Special Purpose Vehicle segment, while niche, will also contribute to market growth, especially with the incorporation of advanced safety features in vehicles designed for specific applications like emergency services, construction, and defense.

The dominance of Asia-Pacific, particularly China, in the Auto Safety Aids market is a multifaceted phenomenon. China's position as the world's largest automotive market, coupled with its ambitious targets for vehicle safety enhancements and the rapid development of its domestic automotive industry, makes it a critical region. The Chinese government's proactive approach in mandating safety features and promoting the adoption of advanced technologies, including those related to autonomous driving and ADAS, further solidifies its leading role. India, with its rapidly growing economy and a burgeoning automotive market, presents a significant opportunity for growth. The increasing disposable incomes and a greater awareness of road safety among Indian consumers are driving the demand for safer vehicles. Furthermore, the "Make in India" initiative is encouraging local manufacturing of automotive components, including safety aids.

The Auto Safety Aids industry is experiencing significant growth catalysts, most notably the increasing stringency of global safety regulations that mandate advanced features. The growing consumer awareness and demand for enhanced vehicle safety are also powerful drivers, pushing manufacturers to integrate more protective technologies. Furthermore, rapid advancements in sensor technology, AI, and connectivity are enabling the development of more sophisticated and proactive safety systems, moving beyond passive protection to active accident prevention. The growing adoption of electric vehicles, which often come equipped with the latest safety innovations, also contributes to market expansion.

This report offers a holistic view of the Auto Safety Aids market, encompassing a detailed analysis of its current state and future trajectory. It delves into the critical trends shaping the industry, such as the increasing adoption of intelligent safety systems and the growing emphasis on occupant and pedestrian protection. The report meticulously examines the driving forces, including regulatory mandates and evolving consumer preferences, while also providing a realistic assessment of the challenges and restraints, such as cost implications and cybersecurity risks. Furthermore, it identifies key regions and segments poised for dominant growth, offering valuable insights for strategic decision-making. The comprehensive coverage ensures stakeholders have a deep understanding of the market dynamics, technological advancements, and competitive landscape, empowering them to navigate this evolving sector effectively.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 7.4%.

Key companies in the market include Autoliv, Joyson Safety Systems, ZF Friedrichshafen AG, Toyoda Gosei, Hyundai Mobis, APG, Wanxiang Qianchao, Vie Group, Nihon Plast, S and T Motiv, Jinzhou Jinheng Automotive Safety System, Eastjoylong, Tai Hang Chang Qing, .

The market segments include Type, Application.

The market size is estimated to be USD 133.07 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Auto Safety Aids," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Auto Safety Aids, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.