1. What is the projected Compound Annual Growth Rate (CAGR) of the Auto Parts Manufacturing?

The projected CAGR is approximately 2.21%.

Auto Parts Manufacturing

Auto Parts ManufacturingAuto Parts Manufacturing by Type (Battery, Cooling System, Underbody Component, Automotive Filter, Engine Components, Lighting Component, Others), by Application (OEM, Aftermarket), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

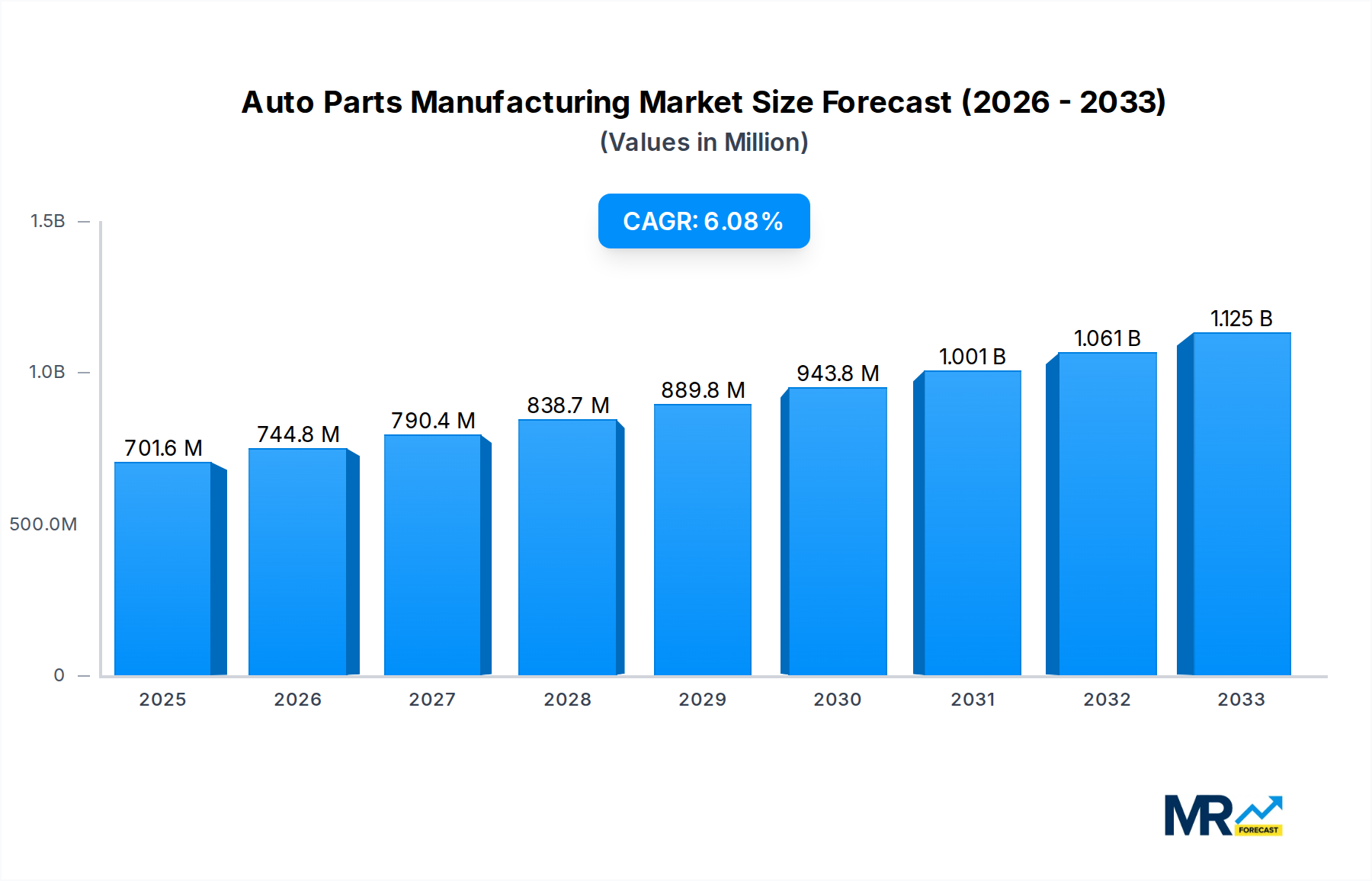

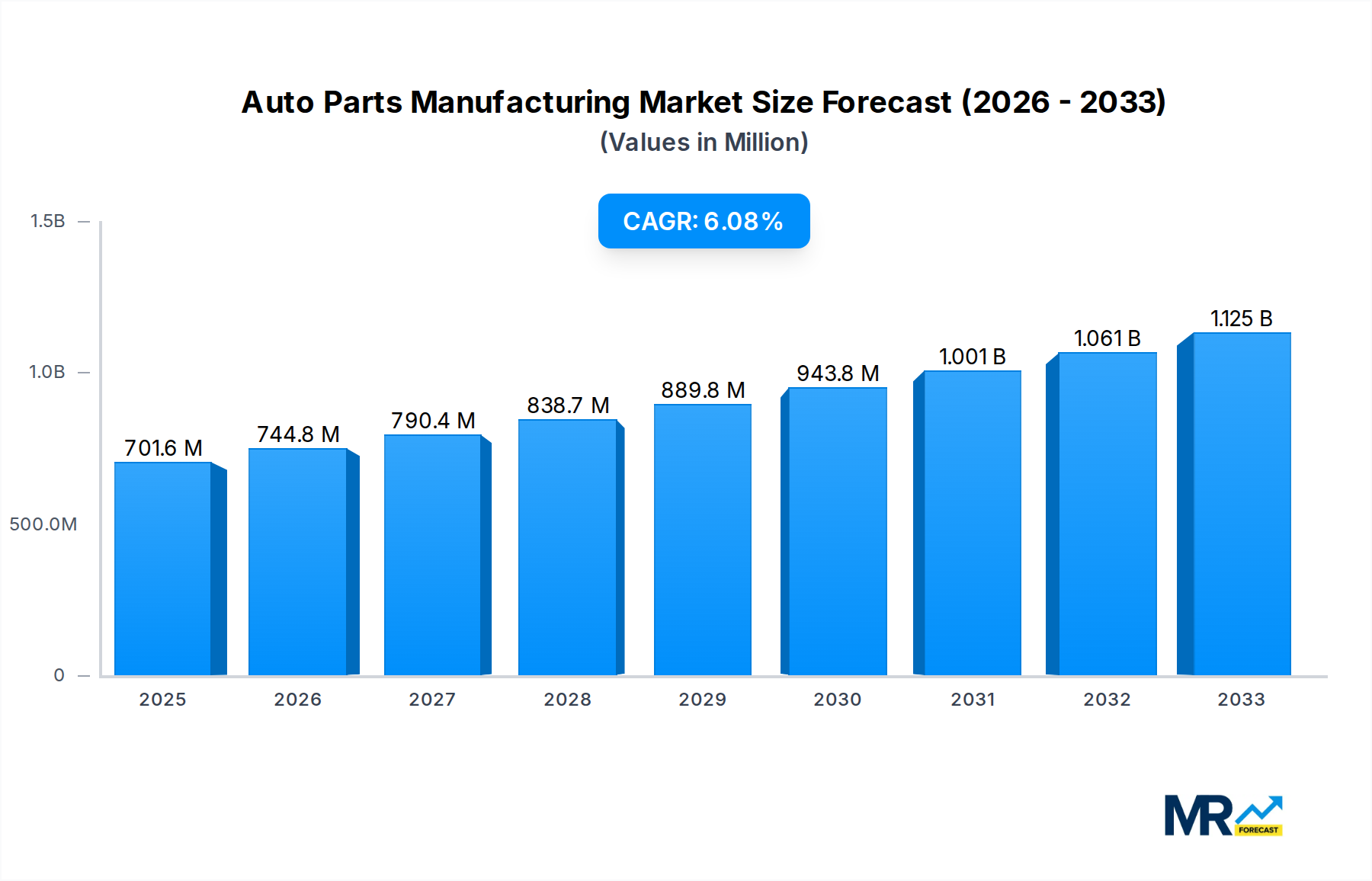

The global Auto Parts Manufacturing market is projected to reach a significant valuation of USD 701.57 billion by 2025, demonstrating robust growth with an estimated Compound Annual Growth Rate (CAGR) of 6.1% through 2033. This expansion is fueled by a dynamic interplay of factors, with the burgeoning demand for electric vehicles (EVs) and their specialized components, such as advanced battery systems and sophisticated cooling mechanisms, emerging as primary drivers. The increasing sophistication of automotive technology, encompassing advanced driver-assistance systems (ADAS) and connected car features, also necessitates a continuous upgrade and replacement of existing parts, thereby stimulating aftermarket sales. Furthermore, stringent regulatory mandates for vehicle safety and emissions are compelling manufacturers to innovate and adopt higher-quality, more efficient components, contributing to market expansion. Emerging economies, particularly in the Asia Pacific region, are witnessing a surge in automotive production and sales, creating substantial opportunities for auto parts manufacturers.

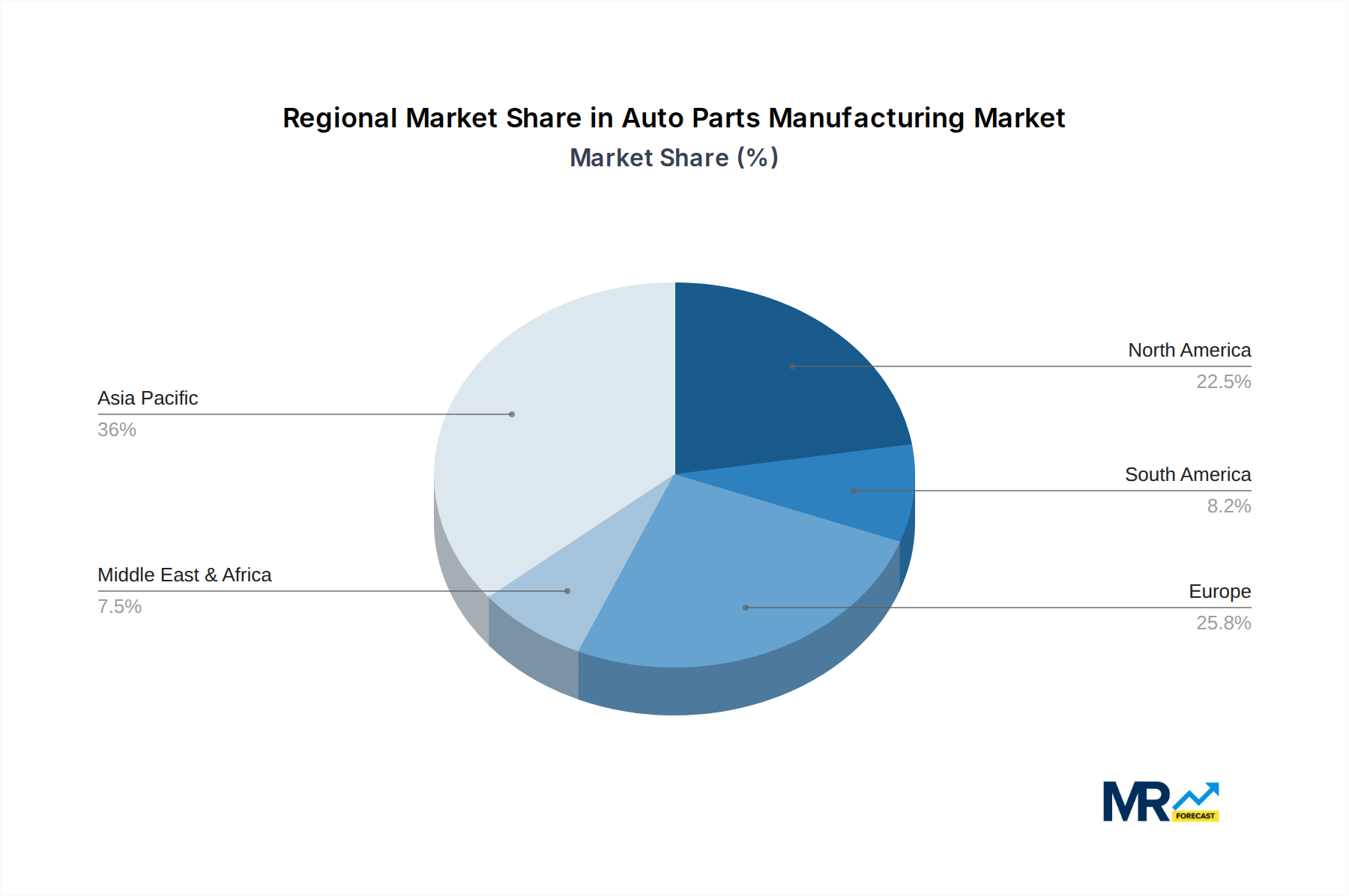

The market is characterized by a diverse segmentation catering to evolving automotive needs. Key segments include Battery components, vital for the growing EV sector, and Cooling Systems, essential for thermal management in both traditional and electric powertrains. Underbody Components, Automotive Filters, Engine Components, and Lighting Components represent established yet continuously evolving segments. The demand is bifurcated between the Original Equipment Manufacturer (OEM) segment, driven by new vehicle production, and the Aftermarket, fueled by vehicle maintenance, repair, and upgrades. Geographically, North America and Europe are mature markets with a strong focus on technological advancements and regulatory compliance, while the Asia Pacific region, led by China and India, is the fastest-growing market due to its massive vehicle parc and expanding manufacturing base. Key industry players like Robert Bosch, Denso, Delphi, and Continental are strategically investing in research and development to capitalize on these trends, particularly in areas like electrification and autonomous driving technologies.

This comprehensive report delves into the intricate world of auto parts manufacturing, offering an in-depth analysis of its present landscape and future trajectory. Spanning a study period from 2019 to 2033, with a specific focus on the base and estimated year of 2025 and a robust forecast period from 2025 to 2033, the report leverages historical data from 2019-2024 to paint a vivid picture of market dynamics. It quantifies market opportunities and challenges in the billions, providing a crucial understanding of the financial scale and potential within this vital industry. The report meticulously examines key industry players, emerging trends, driving forces, and critical challenges, offering actionable insights for stakeholders across the automotive value chain.

The global auto parts manufacturing industry is undergoing a transformative period, driven by a confluence of technological advancements, evolving consumer demands, and stringent regulatory frameworks. The historical period from 2019 to 2024 witnessed significant shifts, particularly the burgeoning impact of electrification and the increasing integration of advanced digital technologies. As we move into the base year of 2025 and the subsequent forecast period through 2033, these trends are poised to accelerate, reshaping the manufacturing processes, product portfolios, and competitive strategies of key players. The market's estimated valuation is in the hundreds of billions, signifying its immense economic importance. A significant trend is the increasing demand for lightweight materials, driven by the need to improve fuel efficiency in internal combustion engine (ICE) vehicles and enhance the range of electric vehicles (EVs). This has led to greater adoption of aluminum alloys, composites, and advanced plastics in components ranging from chassis to engine parts. Furthermore, the proliferation of smart automotive technologies is a dominant force. The integration of sensors, advanced driver-assistance systems (ADAS), and in-car infotainment systems necessitates a sophisticated and interconnected supply chain for electronic components, sensors, and sophisticated control units. This segment alone is experiencing exponential growth, pushing innovation in areas like semiconductors and specialized software.

The shift towards electric mobility is fundamentally altering the landscape of auto parts manufacturing. Traditional engine components are gradually being replaced by electric powertrains, battery systems, and power electronics. Companies that were once heavily reliant on ICE components are now pivoting their investments and R&D efforts towards EV-specific parts, such as battery management systems, electric motors, and charging infrastructure components. This transition is not without its complexities, requiring substantial capital investment and the acquisition of new skill sets. The growing emphasis on sustainability and environmental regulations is another critical trend influencing the industry. Manufacturers are increasingly pressured to adopt greener production methods, reduce waste, and develop parts with a lower environmental footprint. This includes the use of recycled materials, energy-efficient manufacturing processes, and components designed for end-of-life recyclability. The circular economy concept is gaining traction, encouraging a more responsible approach to material sourcing and product lifecycle management.

Moreover, the digitalization of manufacturing processes, often referred to as Industry 4.0, is revolutionizing how auto parts are produced. This involves the implementation of automation, artificial intelligence (AI), big data analytics, and the Internet of Things (IoT) to optimize production efficiency, improve quality control, and enable predictive maintenance. The ability to collect and analyze real-time data from the manufacturing floor allows for greater agility and responsiveness to market demands. The aftermarket segment is also evolving, with an increasing demand for high-quality, reliable replacement parts, particularly as the global vehicle parc ages. However, the rise of counterfeit parts and the growing complexity of vehicles necessitate advanced diagnostic tools and specialized training for aftermarket service providers. The overall market size is projected to continue its upward trajectory, fueled by these multifaceted trends.

The auto parts manufacturing industry is propelled by a dynamic interplay of macro-economic factors, technological advancements, and evolving consumer preferences. The increasing global vehicle production volume remains a fundamental driver. Despite cyclical fluctuations, the underlying trend of growing vehicle ownership, particularly in emerging economies, ensures a consistent demand for a wide array of automotive components. This expanding market size, measured in hundreds of billions, directly translates to increased production needs for both original equipment manufacturers (OEMs) and the aftermarket.

A paramount driving force is the unstoppable momentum of vehicle electrification. The global push towards reducing carbon emissions and the increasing adoption of electric vehicles (EVs) have created a massive new market for batteries, electric motors, power electronics, and related components. This transition is not just a minor shift; it's a fundamental reimagining of the automobile, demanding significant investment and innovation in new product categories. Simultaneously, the rapid advancement and integration of automotive electronics and connectivity are transforming vehicles into sophisticated, data-driven machines. The growing sophistication of Advanced Driver-Assistance Systems (ADAS), autonomous driving technologies, and in-car digital experiences necessitates a surge in demand for sensors, processors, communication modules, and software, further expanding the market for specialized electronic components.

Consumer demand for enhanced safety, comfort, and personalized driving experiences also plays a crucial role. This translates into a higher demand for advanced seating systems, climate control solutions, infotainment units, and adaptive lighting, all of which require specialized manufacturing capabilities. Furthermore, stringent government regulations and emissions standards across the globe are compelling automakers and, consequently, their suppliers, to innovate and produce more fuel-efficient, cleaner, and safer components. This regulatory push acts as a significant catalyst for technological development and market growth in specific segments like emissions control systems and advanced safety features.

Despite the robust growth prospects, the auto parts manufacturing sector faces significant challenges and restraints that can impede its progress. The increasing complexity of vehicle technology presents a substantial hurdle. The integration of sophisticated electronics, autonomous driving features, and advanced powertrains requires manufacturers to continuously invest in R&D, acquire new technical expertise, and adapt their production lines. This complexity also increases the potential for supply chain disruptions and quality control issues, which can be costly to rectify.

The volatility of raw material prices is another critical restraint. Fluctuations in the cost of metals, plastics, rare earth elements, and other essential inputs can significantly impact manufacturing costs and profitability. Geopolitical instability, trade disputes, and global supply chain bottlenecks can exacerbate these price swings, making long-term cost planning challenging for companies operating in the hundreds of billions dollar market. The intense global competition and price pressures from both established players and emerging manufacturers, particularly from low-cost regions, can squeeze profit margins. Automakers are constantly seeking to reduce their sourcing costs, forcing auto parts manufacturers to operate with leaner margins and seek efficiencies across their operations.

The transition to electric vehicles (EVs), while a growth driver, also poses a significant challenge for established manufacturers of traditional internal combustion engine (ICE) components. Re-tooling factories, retraining workforces, and developing new technological capabilities for EV components requires substantial capital investment and a strategic pivot, which can be a daunting task for companies with long-standing expertise in ICE technology. Furthermore, cybersecurity threats are becoming an increasingly relevant concern. With the growing digitalization of manufacturing processes and the interconnectedness of vehicle systems, manufacturers must invest in robust cybersecurity measures to protect their intellectual property, production data, and ultimately, the safety of the vehicles they equip. The threat of cyber-attacks can disrupt operations, compromise sensitive information, and damage brand reputation.

The global auto parts manufacturing market, valued in the hundreds of billions, is characterized by regional dominance and segment leadership driven by economic development, technological adoption, and regulatory landscapes.

Dominant Regions/Countries:

Asia Pacific: This region, led by China, is the undisputed powerhouse in auto parts manufacturing.

Europe: Home to some of the world's leading automotive brands, Europe remains a pivotal region for auto parts manufacturing, particularly in the OEM segment.

North America: Primarily driven by the United States, North America is a major consumer and producer of auto parts.

Dominant Segments:

Engine Components: Despite the shift towards electrification, Engine Components continue to represent a substantial portion of the auto parts manufacturing market due to the vast existing fleet of internal combustion engine vehicles. This segment encompasses a wide range of parts, including pistons, crankshafts, valves, and fuel injection systems. Companies like Robert Bosch and Denso are major players in this historically dominant segment.

Underbody Components: This segment, including parts like chassis, suspension, braking systems, and exhaust systems, is critical for vehicle performance and safety. As vehicles become more sophisticated, there's an increasing demand for advanced materials and precision engineering in these components. ZF TRW and Magna International are significant contributors to this segment.

Battery: This segment is experiencing explosive growth due to the rapid adoption of electric vehicles. The demand for advanced battery technologies, including lithium-ion batteries and their associated components, is a key driver of market expansion. Companies are heavily investing in R&D and manufacturing capabilities for this segment.

Automotive Filter: Essential for maintaining vehicle performance and longevity, the Automotive Filter segment, including air filters, oil filters, and fuel filters, continues to show steady growth. The increasing complexity of engines and emission control systems drives the demand for more efficient and specialized filters.

OEM (Original Equipment Manufacturer): The OEM segment is the largest by volume, as auto parts manufacturers supply components directly to vehicle assembly lines. The growth of the OEM segment is intrinsically linked to global vehicle production volumes and the introduction of new vehicle models.

Aftermarket: The Aftermarket segment, which includes replacement parts sold through independent repair shops and retailers, is also a significant market. An aging global vehicle parc, coupled with the need for regular maintenance and repairs, fuels consistent demand. The aftermarket is also influenced by consumer preference for quality and affordability.

The interplay of these regions and segments, particularly the growing influence of Asia Pacific in both production and consumption, and the burgeoning Battery segment driven by EV adoption, will shape the future landscape of the auto parts manufacturing market.

The auto parts manufacturing industry is fueled by several key growth catalysts. The accelerating global adoption of Electric Vehicles (EVs) is a paramount driver, creating immense demand for batteries, electric powertrains, and associated components. The continuous advancement in automotive technology, particularly in areas like autonomous driving, connectivity, and advanced driver-assistance systems (ADAS), necessitates a surge in demand for sophisticated electronics, sensors, and control units. Furthermore, growing vehicle production volumes, especially in emerging economies, directly translate to increased demand for all types of auto parts. Finally, stringent government regulations mandating improved fuel efficiency and reduced emissions are compelling innovation and driving the demand for advanced and eco-friendly automotive components.

This comprehensive report provides an exhaustive analysis of the auto parts manufacturing market, offering critical insights for strategic decision-making. It meticulously dissects market trends, identifies key growth drivers, and delineates the challenges that stakeholders must navigate. With an estimated market value in the hundreds of billions, the report quantifies opportunities across various segments like Batteries, Engine Components, and Underbody Components, and applications such as OEM and Aftermarket. It leverages historical data from 2019-2024 and provides a robust forecast for 2025-2033, centered around the base year of 2025, enabling stakeholders to understand the market's trajectory and capitalize on emerging opportunities within this dynamic and evolving industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.21% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 2.21%.

Key companies in the market include Robert Bosch, Denso, Delphi, Valeo, Continental, ZF TRW, Magna International, Faurecia, Magneti Marelli, Aisin Seiki, Brembo, Akebono Brake Industry, Hella, ACDelco, .

The market segments include Type, Application.

The market size is estimated to be USD 2302.2 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Auto Parts Manufacturing," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Auto Parts Manufacturing, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.