1. What is the projected Compound Annual Growth Rate (CAGR) of the Atrial Septal Occlusion Device?

The projected CAGR is approximately 10.94%.

Atrial Septal Occlusion Device

Atrial Septal Occlusion DeviceAtrial Septal Occlusion Device by Type (Absorbable, Unabsorbable), by Application (Children, Adult), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

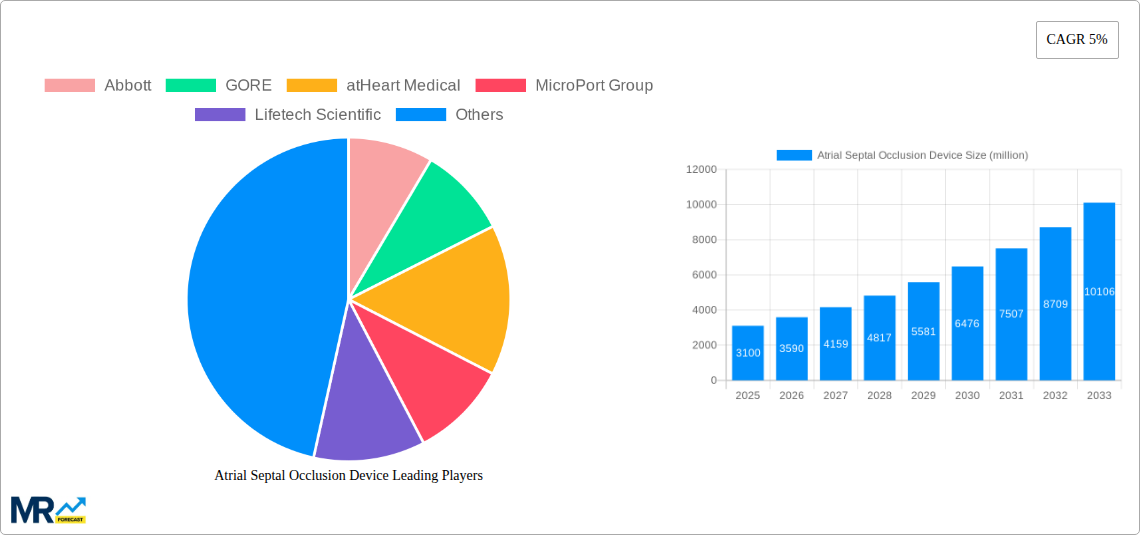

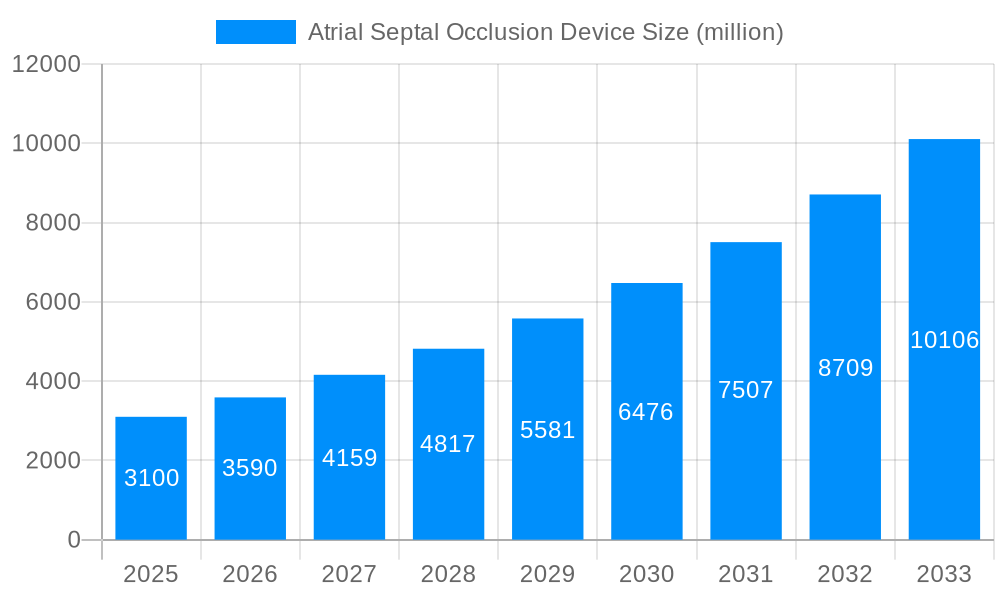

The global Atrial Septal Occlusion Device market is poised for significant expansion, with an estimated market size of approximately $3.1 billion in 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 15.9%, projecting the market to reach substantial figures by 2033. This upward trajectory is primarily fueled by an increasing prevalence of congenital heart defects, specifically atrial septal defects (ASDs), which necessitates effective interventional treatments. Advancements in medical technology, leading to the development of more sophisticated, minimally invasive, and patient-friendly occlusion devices, are also key drivers. These innovations contribute to improved patient outcomes, reduced recovery times, and a lower risk of complications compared to traditional surgical interventions, thereby increasing adoption rates among both pediatric and adult populations. Furthermore, a growing awareness among healthcare professionals and patients regarding the benefits of percutaneous closure procedures over surgery is also propelling market growth.

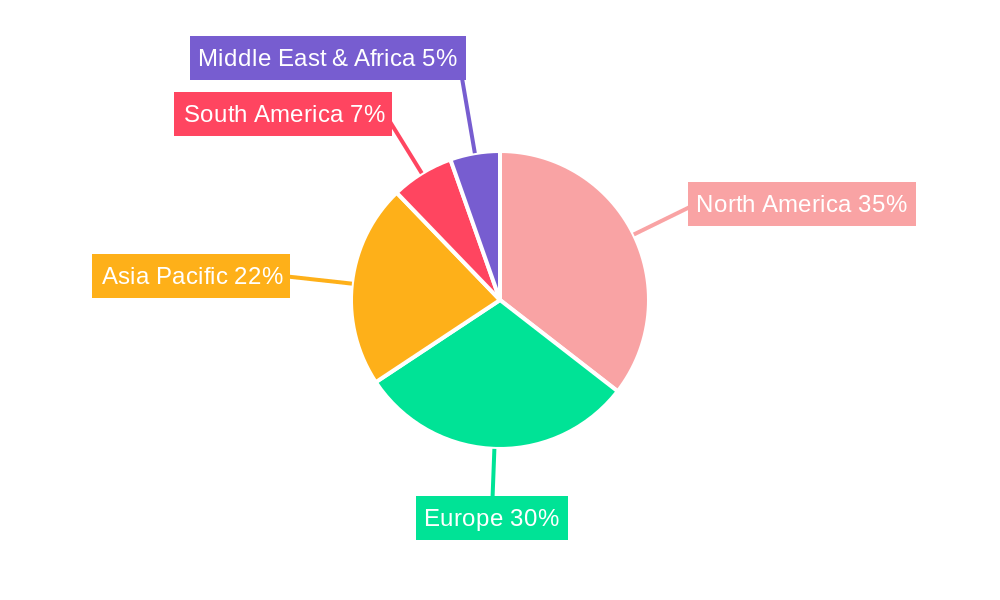

The market segmentation reveals a strong demand across both absorbable and unabsorbable device types, catering to diverse clinical needs and physician preferences. While absorbable devices offer the advantage of eventual dissolution, unabsorbable devices continue to be a mainstay due to their proven efficacy and long-term reliability. The application segment is equally divided between children and adults, reflecting the widespread impact of ASDs across all age groups. Geographically, North America and Europe currently lead the market due to their advanced healthcare infrastructure, high disposable incomes, and early adoption of innovative medical technologies. However, the Asia Pacific region, particularly China and India, is expected to exhibit the fastest growth rate, driven by a large and growing patient pool, improving healthcare access, and increasing investments in medical device manufacturing. Key players like Abbott, GORE, and MicroPort Group are at the forefront, actively engaged in research and development to introduce next-generation devices and expand their market reach.

The global atrial septal occlusion device market is poised for remarkable expansion, projected to surge from an estimated USD 2.1 billion in the base year of 2025 to a substantial USD 4.5 billion by the forecast year of 2033. This represents a compelling compound annual growth rate (CAGR) of approximately 9.5% during the forecast period (2025-2033). The historical period (2019-2024) laid the groundwork for this growth, with steady advancements in device technology and increasing awareness of transcatheter interventions for atrial septal defects (ASDs). The Estimated Year (2025) solidifies this trajectory, reflecting current market momentum and anticipated uptake of innovative solutions.

XXX, the key market insight driving this expansion, lies in the escalating prevalence of congenital heart defects, particularly ASDs, necessitating effective and less invasive treatment options. The shift from traditional open-heart surgery to percutaneous procedures, facilitated by sophisticated occlusion devices, is a cornerstone of this trend. These devices offer reduced recovery times, lower complication rates, and improved patient outcomes, especially for pediatric populations where minimally invasive approaches are paramount. Furthermore, an aging global population contributes to a rise in acquired heart conditions, indirectly increasing the demand for cardiac interventions, including those for secundum ASDs which are more common in adults. The growing emphasis on early diagnosis and intervention in both pediatric and adult cardiology further fuels market penetration. Technological innovations, such as the development of absorbable devices that dissolve over time, are also gaining traction, offering novel solutions for specific patient needs and potentially reducing long-term complications. The increasing healthcare expenditure globally, coupled with favorable reimbursement policies for transcatheter procedures in many developed nations, is also a significant contributor to the market's robust growth. The base year of 2025 serves as a critical benchmark, capturing the current state of adoption and the nascent impact of recent technological advancements. The study period of 2019-2033 encompasses the foundational years of widespread adoption through to the projection of mature market growth, providing a comprehensive view of the forces shaping this vital segment of cardiovascular care.

The atrial septal occlusion device market is experiencing robust growth, propelled by a confluence of powerful driving forces. Foremost among these is the increasing global prevalence of congenital heart defects (CHDs), with atrial septal defects (ASDs) being a significant subset. As diagnostic capabilities improve and awareness among healthcare professionals and the public rises, more cases are identified, leading to a greater demand for effective treatment solutions. Critically, the paradigm shift from open-heart surgery to less invasive transcatheter closure procedures is a major catalyst. These percutaneous techniques, utilizing sophisticated occlusion devices, offer patients numerous advantages, including shorter hospital stays, reduced pain and scarring, faster recovery times, and a lower risk of surgical complications. This patient-centric approach is increasingly favored by both clinicians and patients, especially for pediatric interventions where preserving quality of life and minimizing trauma are paramount. Furthermore, the development of advanced device technologies, such as self-expanding nitinol devices with enhanced flexibility and biocompatibility, alongside the emerging category of absorbable occlusion devices, are continuously expanding the therapeutic armamentarium and addressing unmet clinical needs. The growing incidence of ASDs in adults, often undiagnosed until later in life and associated with increased risks of atrial fibrillation and stroke, also contributes significantly to market expansion, broadening the patient demographic for these devices. The estimated year of 2025 highlights the current momentum driven by these factors, with projections indicating continued acceleration.

Despite the promising growth trajectory, the atrial septal occlusion device market faces several significant challenges and restraints that could temper its expansion. One primary hurdle is the high cost of these advanced devices, which can be a barrier to widespread adoption, particularly in resource-limited healthcare systems or for uninsured patient populations. The complex manufacturing processes and the specialized materials used contribute to these elevated prices, necessitating robust reimbursement frameworks to ensure accessibility. Another significant restraint stems from the need for specialized training and expertise among interventional cardiologists and cardiovascular surgeons to perform transcatheter closure procedures effectively and safely. The learning curve associated with new device designs and techniques can slow down adoption rates and potentially lead to suboptimal outcomes if not managed properly. Potential complications associated with transcatheter closure, although generally lower than surgical risks, still exist. These can include device embolization, residual shunting, arrhythmias, and vascular access site complications. Stringent regulatory approvals and lengthy clinical trial processes for new devices also pose a challenge, extending the time to market and increasing development costs for manufacturers. Furthermore, patient and physician reluctance to deviate from established surgical protocols, especially in regions with a strong tradition of surgical intervention, can also act as a restraint. Addressing these challenges through ongoing training, cost-effectiveness studies, and continued innovation to minimize risks will be crucial for the sustained growth of the atrial septal occlusion device market through the forecast period ending in 2033.

The Adult segment is projected to be the dominant force in the Atrial Septal Occlusion Device market during the forecast period (2025-2033). This dominance is underpinned by several key factors:

Geographically, North America and Europe are expected to lead the market, driven by:

The Unabsorbable segment within the Type category is also anticipated to maintain its leading position, especially in the short to medium term. These devices, typically made from nitinol or other biocompatible metals, have a proven track record of safety and efficacy over decades. Their durability and established performance characteristics make them the go-to option for a wide range of ASDs. However, the Absorbable segment is poised for substantial growth, driven by the potential for devices to degrade and be absorbed by the body over time, eliminating the presence of foreign material and potentially reducing long-term risks of complications. This emerging category represents a significant area of innovation and holds promise for future market expansion.

The atrial septal occlusion device industry is experiencing a surge of growth, propelled by several key catalysts. A primary driver is the increasing global prevalence of congenital heart defects, with ASDs being a significant contributor. Enhanced diagnostic techniques and greater awareness are leading to earlier and more frequent identification of these conditions. Furthermore, the growing preference for minimally invasive transcatheter closure procedures over traditional open-heart surgery is a major growth catalyst. These procedures offer improved patient outcomes, faster recovery, and reduced complications. Continuous technological innovation, including the development of more sophisticated device designs, improved biocompatibility, and the emergence of absorbable occlusion devices, is also fueling market expansion. The rising healthcare expenditure in emerging economies and favorable reimbursement policies in developed nations further support the adoption of these advanced medical devices.

This comprehensive report delves into the dynamic global atrial septal occlusion device market, offering an in-depth analysis of its growth trajectory from the historical period (2019-2024) through to robust projections for the forecast period (2025-2033), with an estimated market value of USD 4.5 billion by 2033. It meticulously examines the key market insights, underpinned by the increasing prevalence of ASDs and the shift towards minimally invasive treatments. The report scrutinizes the driving forces, including technological advancements and rising healthcare expenditure, while also addressing the critical challenges and restraints such as high costs and the need for specialized training. A significant portion is dedicated to identifying the dominant region or country and key segments, such as the Adult application and Unabsorbable device type, that are poised to shape market dynamics. Furthermore, it highlights the crucial growth catalysts and provides a detailed overview of the leading industry players. The report offers valuable insights into significant developments within the sector, presented chronologically. This extensive coverage aims to equip stakeholders with a strategic understanding of the atrial septal occlusion device landscape, enabling informed decision-making and strategic planning.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.94% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 10.94%.

Key companies in the market include Abbott, GORE, atHeart Medical, MicroPort Group, Lifetech Scientific, Occlutech, Lepu Medical Technology, WEGO, ScienTech Medical, Shanghai MicroPort MedBot, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Atrial Septal Occlusion Device," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Atrial Septal Occlusion Device, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.