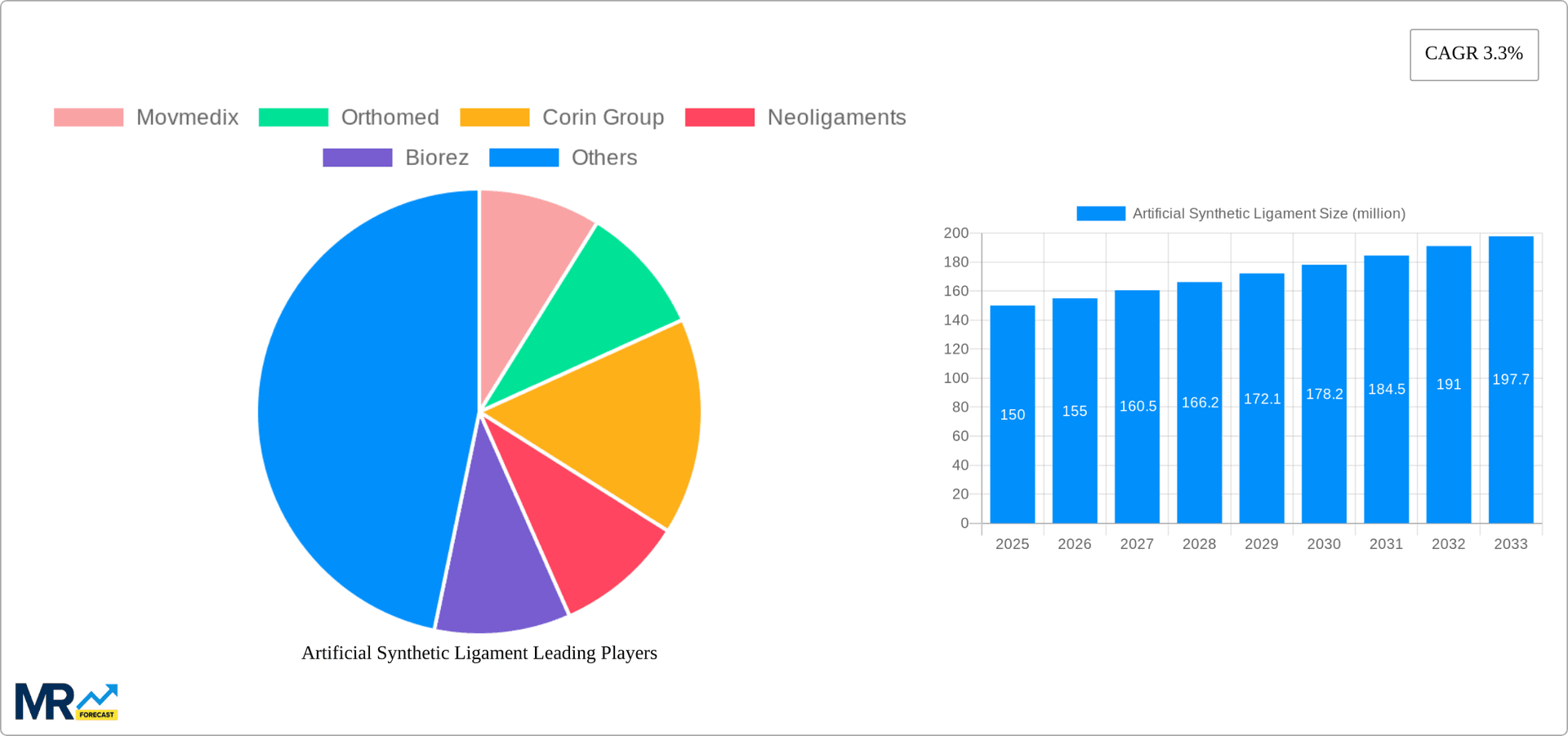

1. What is the projected Compound Annual Growth Rate (CAGR) of the Artificial Synthetic Ligament?

The projected CAGR is approximately 3.3%.

Artificial Synthetic Ligament

Artificial Synthetic LigamentArtificial Synthetic Ligament by Type (Anterior Cruciate Ligament (ACL), Posterior Cruciate Ligament (PCL), Medial Cruciate Ligament (MCL)), by Application (Knee Injuries, Shoulder Injuries, Foot and Ankle Injuries, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

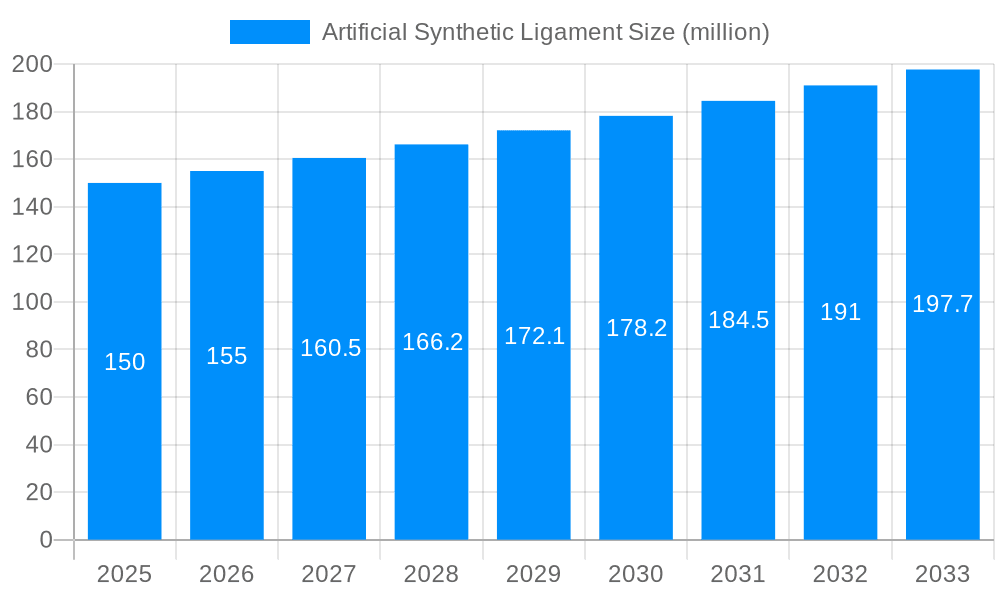

The global artificial synthetic ligament market, valued at $150 million in 2025, is projected to experience steady growth, driven by an increasing prevalence of sports injuries, a rising geriatric population susceptible to ligament tears, and advancements in surgical techniques and biomaterial development. The market's 3.3% CAGR indicates a consistent, albeit moderate, expansion over the forecast period (2025-2033). Key growth drivers include the rising preference for minimally invasive surgical procedures, improved rehabilitation outcomes associated with synthetic ligaments, and increasing healthcare expenditure globally. The anterior cruciate ligament (ACL) segment currently dominates the market due to its high incidence of injury, particularly among athletes. However, growing awareness and improved diagnostic capabilities for other ligament injuries (PCL, MCL) are expected to fuel growth in these segments as well. Geographic analysis reveals that North America and Europe currently hold significant market shares due to established healthcare infrastructure and high adoption rates of advanced medical technologies. However, emerging markets in Asia Pacific, driven by rising disposable incomes and improving healthcare access, are anticipated to contribute significantly to market growth in the coming years. Competition in the market is intense, with a mix of established players and emerging companies focused on innovation and developing superior biocompatible materials. This competitive landscape further accelerates market growth, resulting in continuous improvements in product offerings and pricing.

The market's restraints include the relatively high cost of synthetic ligaments compared to traditional treatments, potential complications associated with surgery and implant failure, and the need for extensive post-operative rehabilitation. Nevertheless, ongoing research into biocompatible materials and minimally invasive techniques is expected to mitigate these limitations. The market segmentation by application (knee injuries, shoulder injuries, foot and ankle injuries) reflects the versatility of synthetic ligaments in addressing a wide range of musculoskeletal injuries, further expanding market opportunities. Over the forecast period, we anticipate a gradual shift towards less invasive surgical techniques and a higher adoption of synthetic ligaments in emerging economies. This, combined with ongoing technological advancements and a growing understanding of the benefits, will contribute to a steady increase in market size and broader accessibility of this crucial medical technology.

The global artificial synthetic ligament market is experiencing robust growth, projected to reach multi-billion dollar valuations by 2033. Driven by an aging population, increasing incidence of sports injuries, and advancements in biomaterial science, the market exhibits a strong upward trajectory. The period between 2019 and 2024 (Historical Period) saw steady expansion, laying the foundation for the accelerated growth anticipated during the forecast period (2025-2033). By the estimated year 2025, the market is expected to surpass several hundred million units, indicating significant market penetration and adoption. Key insights reveal a strong preference for synthetic ligaments over autografts and allografts in specific applications due to factors such as reduced donor site morbidity, shorter recovery times, and consistent mechanical properties. This trend is particularly pronounced in the ACL and PCL segments. Further market segmentation reveals variations in growth rates across different geographical regions, with North America and Europe leading the way in terms of adoption and technological innovation. However, emerging markets in Asia-Pacific are demonstrating rapid expansion fueled by rising disposable incomes and increasing awareness of advanced surgical techniques. The competitive landscape features a mix of established players and emerging innovators, each vying for market share through strategic partnerships, R&D investments, and product diversification. The market's future hinges on ongoing research to enhance biocompatibility, improve long-term durability, and reduce the risk of complications associated with synthetic implants. This includes significant investments in creating ligaments with superior tensile strength and fatigue resistance to better match the natural properties of native tissue.

Several factors contribute to the robust growth of the artificial synthetic ligament market. Firstly, the global rise in sports-related injuries, particularly among younger demographics, significantly fuels demand for effective and reliable ligament reconstruction solutions. This is further exacerbated by the increasing participation in high-impact sports worldwide. Secondly, the limitations of traditional autograft and allograft procedures—such as donor site morbidity, harvesting difficulties, and limited availability—are driving the adoption of synthetic alternatives. Synthetic ligaments offer a consistent and readily available solution, reducing patient wait times and improving surgical efficiency. Thirdly, continuous advancements in biomaterial science are leading to the development of increasingly biocompatible and durable synthetic ligaments. These improvements minimize the risk of rejection, inflammation, and long-term complications, fostering greater confidence among surgeons and patients. Finally, growing awareness among healthcare professionals and patients regarding the benefits of synthetic ligaments, coupled with an increase in minimally invasive surgical techniques, further contributes to market expansion. This heightened awareness, facilitated by medical publications and industry conferences, leads to improved patient outcomes and broader acceptance of synthetic ligament replacement as a viable treatment option.

Despite its considerable potential, the artificial synthetic ligament market faces certain challenges. The high cost of synthetic ligament implants presents a significant barrier to wider adoption, particularly in resource-constrained healthcare settings. Furthermore, concerns regarding the long-term durability and biocompatibility of synthetic materials remain. While improvements have been made, achieving perfect biointegration and preventing degradation over many years continues to be a focus of ongoing research. Another key challenge lies in the potential for complications associated with surgical procedures, such as infection, implant failure, and stiffness. These complications can lead to negative patient outcomes and impact the overall reputation of synthetic ligament technology. The regulatory landscape varies across different regions, introducing complexities and delays in product approvals. Meeting stringent regulatory requirements adds to the cost and time involved in bringing new synthetic ligament products to the market. Finally, the limited availability of trained surgeons specializing in the implantation of synthetic ligaments can act as a restraint on market expansion. Addressing these challenges requires collaboration between researchers, manufacturers, regulatory bodies, and surgeons to ensure the safety and efficacy of synthetic ligaments while making them more accessible.

The Anterior Cruciate Ligament (ACL) segment is expected to dominate the artificial synthetic ligament market due to its high incidence of injury across various demographics and the significant functional limitations associated with ACL tears. The prevalence of ACL injuries, particularly in sports like football, basketball, and skiing, creates a substantial demand for effective reconstructive solutions.

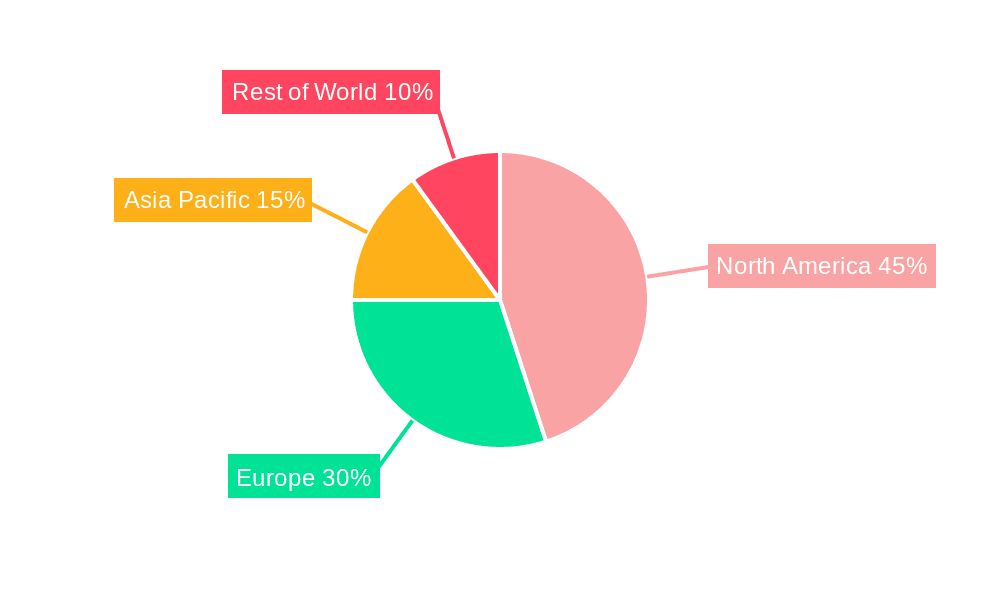

North America and Europe are currently leading the market due to factors such as high healthcare expenditure, advanced healthcare infrastructure, and a greater awareness of advanced surgical techniques. These regions have a high concentration of specialized surgeons and research institutions dedicated to the development and refinement of artificial synthetic ligaments.

Asia-Pacific is poised for significant growth owing to the rapidly expanding healthcare sector, rising disposable incomes, and a growing population participating in sports and physical activities. While currently lagging behind North America and Europe in market size, the region's increasing awareness of minimally invasive procedures and improved access to healthcare services are catalysts for future expansion.

Knee Injuries as an application segment are likely to maintain dominance due to the high prevalence of ACL, PCL, and MCL injuries within this category. The prevalence of knee injuries among sports enthusiasts and the aging population needing knee replacements make this application segment a key driver of market growth.

The substantial unmet medical need in anterior cruciate ligament reconstruction, coupled with technological advancements in biomaterial science, further cements the ACL segment's leading position within the market. The high incidence of ACL injuries necessitates a significant number of reconstruction procedures annually, driving consistent market demand for high-quality synthetic ligament implants.

The artificial synthetic ligament industry is propelled by several key growth catalysts. Technological advancements resulting in improved biocompatibility and durability of synthetic materials are key. This, combined with increasing awareness among healthcare professionals and patients regarding the benefits of synthetic ligaments over traditional approaches, is driving broader adoption. Furthermore, the rising prevalence of sports-related injuries, especially among younger individuals, adds significant fuel to market expansion. Finally, governmental initiatives promoting advanced medical technologies, coupled with the expansion of healthcare infrastructure in developing economies, are further contributing to market growth.

This report provides a comprehensive overview of the artificial synthetic ligament market, encompassing market size and growth projections, key trends, driving factors, challenges, and a detailed competitive landscape analysis. The report further segments the market by ligament type (ACL, PCL, MCL), application (knee, shoulder, foot & ankle), and geographical region, providing granular insights into market dynamics. This in-depth analysis offers valuable information for stakeholders across the value chain, facilitating informed decision-making and strategic planning.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.3% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 3.3%.

Key companies in the market include Movmedix, Orthomed, Corin Group, Neoligaments, Biorez, FH ORTHO, Mathys, Teijin, Exactech, Cousin Biotech, CoreTissue BioEngineering, Shanghai Pine & Power Biotech, Shanghai Ligatech Bioscience, .

The market segments include Type, Application.

The market size is estimated to be USD 150 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Artificial Synthetic Ligament," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Artificial Synthetic Ligament, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.