1. What is the projected Compound Annual Growth Rate (CAGR) of the Artificial Spinal Membrane?

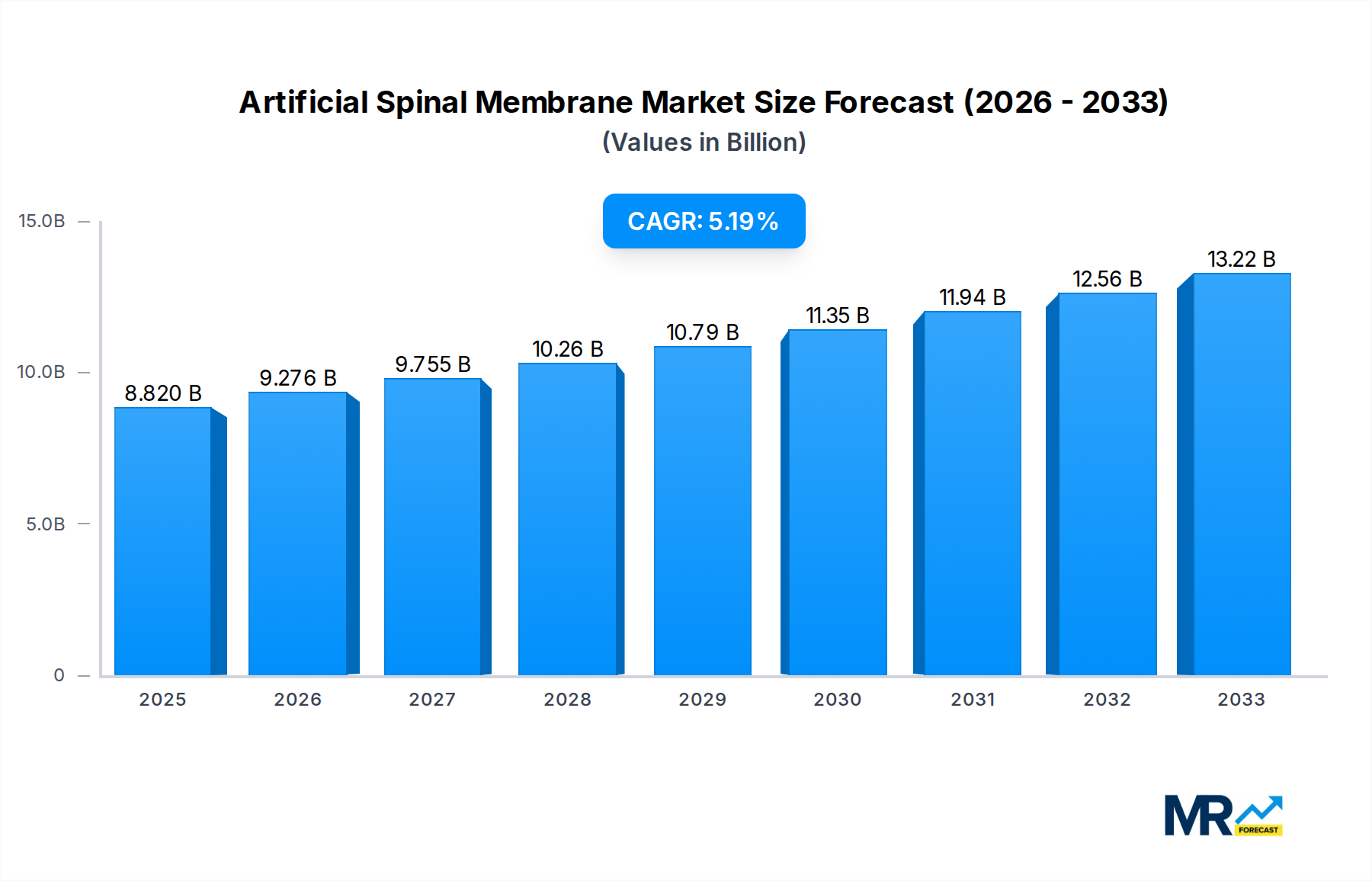

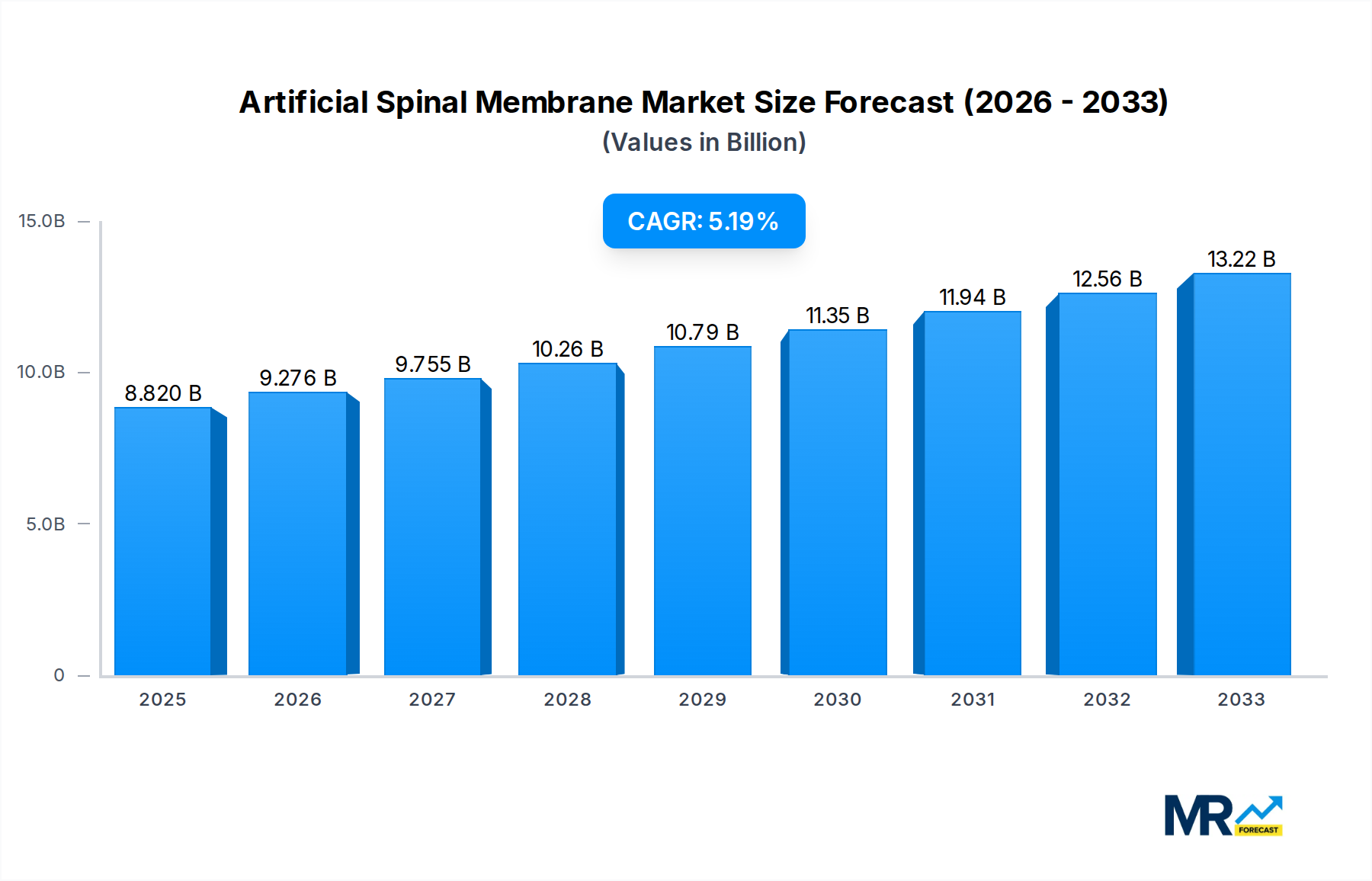

The projected CAGR is approximately 5.04%.

Artificial Spinal Membrane

Artificial Spinal MembraneArtificial Spinal Membrane by Type (Autologous Repair Materials, Allogeneic Repair Materials, World Artificial Spinal Membrane Production ), by Application (Neurosurgery, Spinal Surgery, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The global Artificial Spinal Membrane market is projected to experience robust growth, reaching an estimated value of $8.82 billion by 2025. This expansion is fueled by a Compound Annual Growth Rate (CAGR) of 5.04% over the forecast period of 2025-2033. A significant driver for this market is the increasing prevalence of spinal disorders, including degenerative disc disease, herniated discs, and spinal stenosis, which necessitates advanced surgical interventions. Advances in biomaterials and regenerative medicine are leading to the development of more effective and biocompatible artificial spinal membranes, enhancing surgical outcomes and patient recovery. The growing aging population globally, coupled with a higher incidence of spinal conditions in this demographic, further propels demand for these innovative solutions. Furthermore, rising healthcare expenditure and increasing adoption of minimally invasive surgical techniques contribute to market expansion.

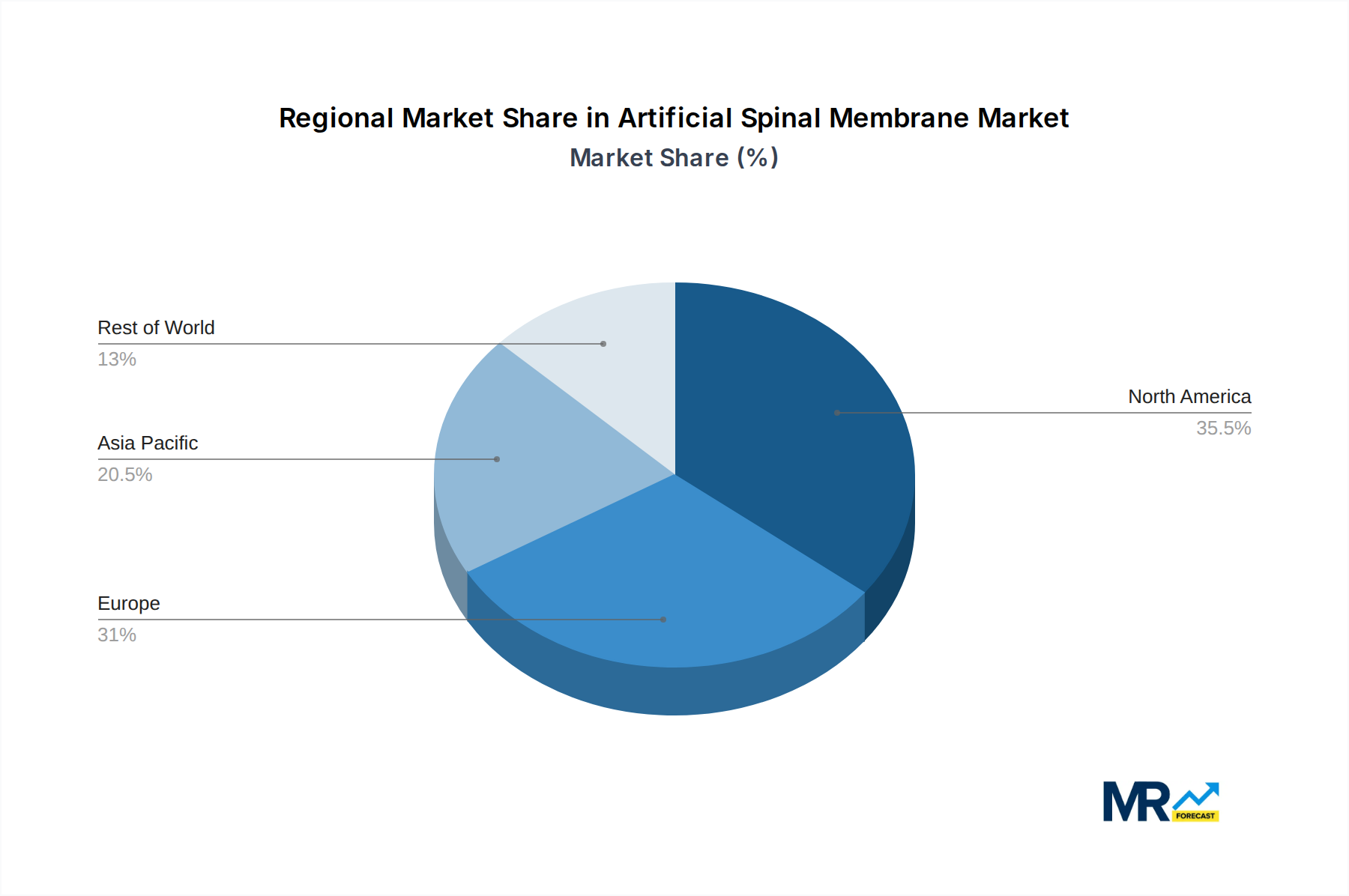

The market segmentation reveals a strong demand across neurosurgery and spinal surgery applications. Autologous repair materials and allogeneic repair materials represent key segments, with ongoing research focused on improving their efficacy and reducing the risk of complications. The competitive landscape is characterized by the presence of prominent global players such as Medtronic, Stryker, and Johnson & Johnson, alongside emerging regional manufacturers, particularly in China and other Asia Pacific countries. These companies are actively engaged in research and development, strategic partnerships, and mergers and acquisitions to strengthen their market position and expand their product portfolios. North America and Europe currently hold significant market share due to advanced healthcare infrastructure and high patient awareness, while the Asia Pacific region is expected to witness the fastest growth, driven by a large patient pool, improving healthcare access, and increasing investment in medical technologies.

The artificial spinal membrane market is poised for substantial expansion, projected to reach an estimated value of USD 3.5 billion by 2025, with robust growth anticipated through the forecast period of 2025-2033. This burgeoning market is characterized by a growing awareness of spinal health issues, an aging global population, and advancements in biomaterials technology. The historical period from 2019 to 2024 witnessed foundational growth, driven by initial research and development and the emergence of early-stage products. As we move into the base year of 2025, the market is entering a more dynamic phase, fueled by increasing clinical adoption and a broader understanding of the benefits offered by these innovative spinal implants.

The demand for artificial spinal membranes is intrinsically linked to the rising incidence of degenerative spinal conditions, such as herniated discs, spinal stenosis, and spondylolisthesis, which often necessitate surgical intervention. The increasing prevalence of these conditions, particularly in developed economies with aging demographics, is a significant driver. Furthermore, technological innovations in the development of biocompatible and bioresorbable materials are expanding the therapeutic potential of artificial spinal membranes. These materials aim to mimic the natural structure and function of the spinal dura mater, facilitating better healing and reducing the risk of complications like cerebrospinal fluid leaks and scar tissue formation.

The market segmentation offers valuable insights. In terms of Type, Autologous Repair Materials, derived from a patient's own tissue, are expected to maintain a significant share due to their inherent biocompatibility and reduced immunogenicity. However, the logistical challenges and costs associated with harvesting autologous tissue may limit their widespread application. Allogeneic Repair Materials, sourced from donors, present a viable alternative with greater availability, though they carry a slightly higher risk of immune rejection. The World Artificial Spinal Membrane Production segment, encompassing both these types, is crucial for understanding the overall supply chain and manufacturing capabilities.

Geographically, North America and Europe currently dominate the market, owing to advanced healthcare infrastructure, higher disposable incomes, and greater investment in R&D. However, the Asia-Pacific region is projected to witness the most rapid growth, driven by a large and aging population, improving healthcare access, and increasing adoption of advanced medical technologies. The application segments of Neurosurgery and Spinal Surgery are the primary beneficiaries, with a smaller but growing application in Other related fields.

The focus on minimally invasive surgical techniques further bolsters the demand for artificial spinal membranes, as these products are often integral to successful outcomes in such procedures. The ability of artificial membranes to provide a robust and protective barrier during complex spinal surgeries contributes to reduced operative time and faster patient recovery. Looking ahead, the period from 2025 to 2033 is anticipated to see sustained growth, with a projected market value that could significantly surpass current estimates if technological breakthroughs and wider market penetration are achieved.

The artificial spinal membrane market is being propelled by a confluence of powerful drivers that are shaping its trajectory through the forecast period of 2025-2033. Foremost among these is the escalating global burden of spinal disorders. An aging population across developed and developing nations contributes significantly to the rise in degenerative conditions like disc herniation and spinal stenosis, which frequently require surgical intervention. This demographic shift directly translates into an increased patient pool seeking effective treatment options, thereby amplifying the demand for advanced biomaterials such as artificial spinal membranes. Furthermore, advancements in biomaterial science and tissue engineering are continuously pushing the boundaries of what is possible. Researchers are developing novel materials that offer enhanced biocompatibility, improved integration with host tissues, and even controlled bioresorption, minimizing long-term complications. These innovations are making artificial spinal membranes more effective and safer, encouraging wider adoption by surgeons. The increasing preference for minimally invasive surgical techniques also plays a crucial role. Artificial spinal membranes are integral to many of these procedures, providing essential protection and facilitating better wound healing while reducing the invasiveness of surgery. This trend towards less traumatic interventions directly benefits the artificial spinal membrane market. Finally, growing investment in research and development by leading medical device companies, including giants like Medtronic, Stryker, and Johnson & Johnson, is fueling innovation and product development, further accelerating market expansion.

Despite the promising outlook, the artificial spinal membrane market faces several significant challenges and restraints that could temper its growth trajectory through the forecast period of 2025-2033. A primary hurdle is the cost associated with these advanced biomaterials and the associated surgical procedures. High production costs for sophisticated materials and the specialized nature of surgeries often lead to elevated healthcare expenses, which can be a barrier to adoption, particularly in price-sensitive markets or for patients with limited insurance coverage. Regulatory approval processes for novel medical devices, including artificial spinal membranes, can be lengthy and complex. Obtaining clearance from bodies like the FDA or EMA requires extensive clinical trials and rigorous data validation, which can delay market entry and increase development costs for manufacturers. While advancements in biomaterials are ongoing, concerns regarding long-term biocompatibility and potential immunogenic responses remain. Although artificial membranes are designed to minimize these risks, ensuring complete and safe integration with the human body over extended periods is an ongoing area of research and vigilance, and any adverse events could lead to public and regulatory scrutiny. Moreover, the availability of established and effective, albeit less advanced, surgical techniques and traditional graft materials presents a form of competition. Surgeons who are accustomed to existing methods may be hesitant to switch to newer, less familiar technologies without substantial evidence of superior outcomes and ease of use. Finally, a lack of widespread physician awareness and training regarding the specific benefits and application nuances of different types of artificial spinal membranes can also limit their uptake in certain surgical settings.

The World Artificial Spinal Membrane Production segment is poised to witness significant dominance shifts and growth across various regions and within specific application segments, painting a dynamic picture for the market between 2019 and 2033.

Key Dominating Segments & Regions:

Spinal Surgery Application: This segment will undoubtedly lead the market in terms of revenue and adoption. Spinal surgery, encompassing procedures for degenerative disc disease, herniated discs, spinal stenosis, and trauma, represents the most substantial application area for artificial spinal membranes. The increasing prevalence of these conditions, coupled with the need for robust dural repair and protection, makes this segment the primary demand driver. The ability of artificial membranes to prevent cerebrospinal fluid leaks and promote optimal healing after complex spinal reconstructions solidifies their indispensability in this field. The growing adoption of minimally invasive spinal surgeries further enhances the appeal of these advanced materials, as they are often critical components in facilitating these less invasive approaches.

North America Region: Historically, North America, particularly the United States, has been a frontrunner in the adoption of advanced medical technologies and has a high prevalence of spinal disorders coupled with a well-developed healthcare infrastructure. The presence of major medical device companies like Medtronic, Stryker, and Johnson & Johnson, with substantial R&D budgets and established distribution networks, further bolsters its dominance. High disposable incomes, robust insurance coverage, and a proactive approach to adopting innovative surgical solutions contribute to a strong market presence.

Asia-Pacific Region: While currently not the largest market, the Asia-Pacific region is projected to be the fastest-growing and will soon rival established markets for World Artificial Spinal Membrane Production. This rapid ascent is driven by several factors:

Allogeneic Repair Materials (Type Segment): While Autologous Repair Materials offer excellent biocompatibility, Allogeneic Repair Materials are likely to gain significant market share in the long run due to their greater availability and scalability. The challenges and costs associated with harvesting autologous tissue make allogeneic options more attractive for widespread clinical use, especially as manufacturing processes for donor-derived materials become more refined and safety protocols are rigorously upheld. The ability to produce these materials in larger batches, adhering to strict quality control measures, positions them for broader market penetration across various regions and for diverse patient needs.

The interplay between these regional and segmental dynamics will define the landscape of World Artificial Spinal Membrane Production, with Asia-Pacific emerging as a critical growth engine and Spinal Surgery as the dominant application, all underpinned by the increasing importance of Allogeneic Repair Materials in meeting global demand.

The artificial spinal membrane industry is fueled by several potent growth catalysts that are expected to drive its expansion through the forecast period of 2025-2033. A primary catalyst is the escalating global prevalence of spinal disorders, directly correlating with aging demographics and sedentary lifestyles, which necessitates effective surgical interventions. Advancements in biomaterial science, leading to the development of highly biocompatible, bioresorbable, and functionally superior artificial membranes, are significantly enhancing treatment efficacy and patient outcomes. Furthermore, the increasing adoption of minimally invasive surgical techniques in spinal procedures directly supports the demand for specialized implants like artificial membranes, which are crucial for successful outcomes in these less invasive approaches. Growing investment in research and development by key players is also a significant growth enabler, fostering innovation and the introduction of next-generation products to the market.

This report offers a comprehensive analysis of the artificial spinal membrane market, meticulously examining trends, drivers, challenges, and future prospects from 2019 to 2033. It delves into the nuances of World Artificial Spinal Membrane Production, including segmentation by Type (Autologous Repair Materials, Allogeneic Repair Materials) and Application (Neurosurgery, Spinal Surgery, Other), providing granular insights into market dynamics. The study employs a robust methodology, with the Base Year at 2025 and a detailed Forecast Period from 2025-2033, building upon a solid foundation from the Historical Period (2019-2024). The report scrutinizes leading players like Medtronic, Stryker, and Johnson & Johnson, alongside emerging regional innovators, detailing their strategies and market positioning. Significant developments and technological advancements are highlighted, alongside regional market analyses, with a particular focus on growth catalysts and the factors propelling the industry forward, ensuring a holistic understanding for stakeholders.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.04% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 5.04%.

Key companies in the market include Maipu Medical, Zhenghai Bio, TianXin Fu Medical Appliance, Guanhao Bio, Bairen Medical, Medtronic, Stryker, Zimmer Biomet, Johnson & Johnson, Integra LifeSciences.

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "Artificial Spinal Membrane," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Artificial Spinal Membrane, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.