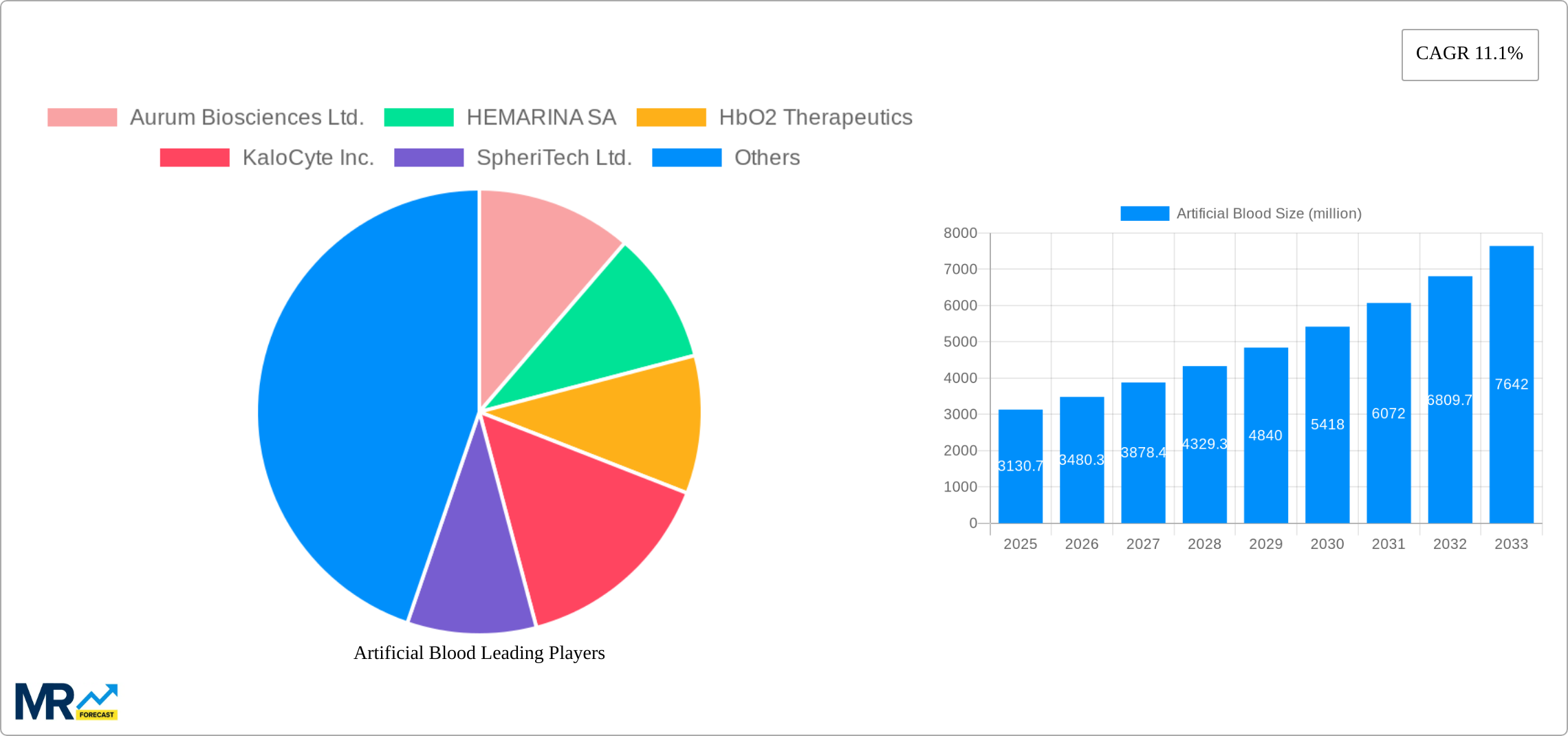

1. What is the projected Compound Annual Growth Rate (CAGR) of the Artificial Blood?

The projected CAGR is approximately 11.1%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Artificial Blood

Artificial BloodArtificial Blood by Type (Human Blood, Synthetic Blood, Animal Blood), by Application (Hemoglobin-Based Oxygen Carriers (HBOCs), Perflurocarbon Emulsions (PFCEs)), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

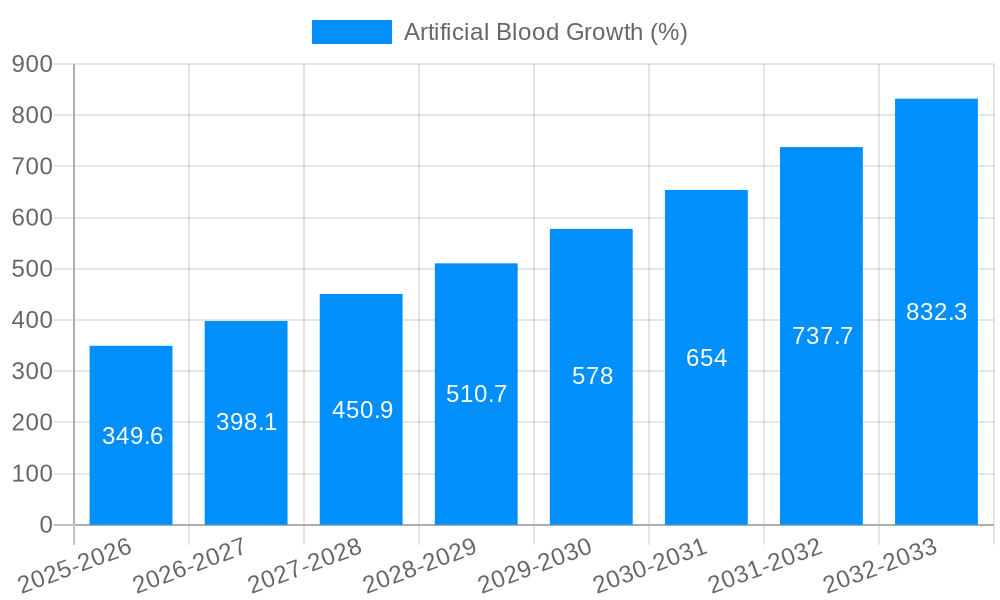

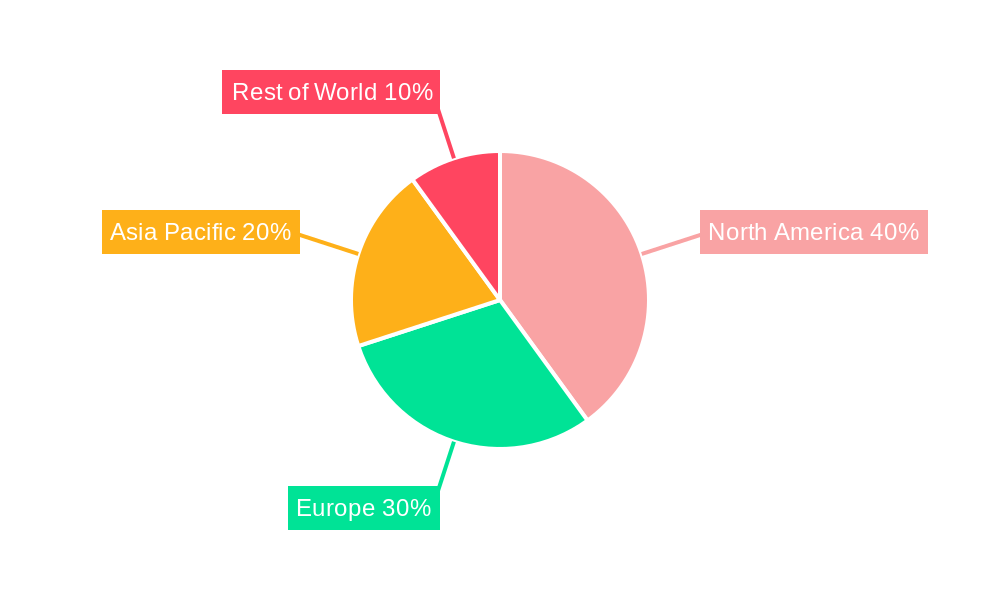

The artificial blood market, valued at $3130.7 million in 2025, is projected to experience robust growth, driven by a compelling CAGR of 11.1% from 2025 to 2033. This expansion is fueled by several key factors. The increasing prevalence of trauma cases and surgical procedures necessitates readily available blood substitutes, particularly in situations where donor blood is scarce or incompatible. Technological advancements in hemoglobin-based oxygen carriers (HBOCs) and perfluorocarbon emulsions (PFCEs) are improving efficacy and safety, further stimulating market growth. Moreover, rising research and development investments focused on overcoming limitations like immunogenicity and cost-effectiveness are paving the way for more widely accepted and accessible artificial blood products. Government initiatives supporting blood research and the development of alternative blood substitutes are also providing significant impetus. The market is segmented by blood type (human, synthetic, animal) and application (HBOCs, PFCEs), with HBOCs currently dominating due to established clinical applications. Regional variations exist, with North America and Europe currently leading market share due to established healthcare infrastructure and high adoption rates, but emerging economies in Asia-Pacific are poised for significant growth due to rapidly expanding healthcare sectors.

Growth is expected to be particularly strong in the development and adoption of synthetic blood alternatives. This segment benefits from overcoming limitations associated with human and animal-derived blood, such as disease transmission risks and ethical concerns. While challenges remain in terms of cost, long-term efficacy, and widespread regulatory approval, ongoing research and development efforts are addressing these issues. The increasing demand for safe and efficient blood substitutes in emergency situations, coupled with the potential for personalized medicine approaches, points toward a promising trajectory for the artificial blood market. This market is expected to benefit from increased private and public funding targeting improved efficacy and safety, ultimately leading to wider adoption across diverse healthcare settings. The competitive landscape is marked by a mix of established players and emerging biotech companies, with intense focus on innovation and expansion into untapped markets.

The artificial blood market is experiencing significant growth, projected to reach multi-billion dollar valuations by 2033. Driven by increasing demand for blood transfusions and the limitations of traditional blood donations, the industry is witnessing considerable innovation across various segments. From 2019 to 2024 (historical period), the market showcased steady growth, laying the groundwork for the explosive expansion predicted in the forecast period (2025-2033). The estimated market value in 2025 stands at a substantial figure in the millions, reflecting the growing acceptance and adoption of artificial blood substitutes. Key market insights point to a preference shift towards safer, readily available, and easily storable alternatives to human blood. This is especially pronounced in regions facing blood shortages and those with stringent regulatory environments. The rising prevalence of chronic diseases requiring frequent transfusions is another major driver. Furthermore, advancements in bioengineering and nanotechnology are continually improving the efficacy and safety profiles of artificial blood products, further fueling market expansion. The increasing investment in research and development by both large pharmaceutical companies and innovative startups is indicative of a promising future for this sector. Competition is fierce, with companies vying for market share through strategic partnerships, acquisitions, and the introduction of novel products with enhanced performance characteristics. The market is also witnessing increased regulatory scrutiny, with authorities focusing on the safety and efficacy of artificial blood products before widespread adoption. This careful monitoring is expected to enhance public trust and contribute to sustainable market growth.

Several factors are driving the remarkable expansion of the artificial blood market. The persistent global shortage of blood donations forms a critical foundation for this growth. Traditional blood donation systems struggle to meet the ever-increasing demands of trauma care, surgical procedures, and the treatment of various blood-related disorders. Artificial blood offers a potential solution to this persistent problem, providing a readily available, easily stored, and potentially safer alternative. Moreover, the rising prevalence of chronic diseases such as cancer, sickle cell anemia, and kidney failure necessitates frequent blood transfusions, thereby driving the need for reliable and readily available substitutes. The inherent risks associated with traditional blood transfusions, including the transmission of infectious diseases and adverse immune reactions, are significant concerns that fuel the demand for safer artificial alternatives. Technological advancements play a vital role, with ongoing research and development leading to the creation of more efficient and biocompatible artificial blood products. The development of hemoglobin-based oxygen carriers (HBOCs) and perfluorocarbon emulsions (PFCEs) with improved oxygen-carrying capacity and reduced side effects represents a significant leap forward. Finally, increasing investment from both public and private sectors is propelling innovation and driving the commercialization of promising artificial blood technologies.

Despite the considerable potential, the artificial blood market faces significant challenges. The high cost of research, development, and manufacturing artificial blood products represents a major barrier to widespread accessibility and affordability. Rigorous regulatory approvals are also a significant hurdle, demanding extensive clinical trials and safety assessments before market entry. The potential for adverse side effects, although minimized with recent advancements, remains a concern, requiring continuous monitoring and refinement of existing technologies. Furthermore, ensuring the long-term stability and efficacy of artificial blood products is crucial for widespread adoption, as degradation over time can compromise their effectiveness. Public perception and acceptance of artificial blood also play a role; overcoming any existing hesitancy or apprehension requires extensive public education and awareness campaigns. Finally, competition from established blood banks and transfusion services creates an additional challenge for artificial blood manufacturers seeking to gain market share. Addressing these challenges effectively is critical for realizing the full potential of artificial blood and achieving its widespread adoption.

The artificial blood market is poised for significant growth across various regions, but certain segments are expected to lead the charge. North America and Europe are anticipated to maintain a dominant market share due to advanced healthcare infrastructure, robust regulatory frameworks, and higher disposable incomes. However, rapidly developing economies in Asia-Pacific are projected to demonstrate exceptional growth rates, driven by rising healthcare expenditure and growing awareness of blood-related diseases.

Dominant Segment: Hemoglobin-Based Oxygen Carriers (HBOCs) are projected to dominate the market due to their superior oxygen-carrying capacity and relative ease of production compared to other substitutes. This segment's share is expected to surpass several million units by 2033.

Market Drivers by Region:

The success of HBOCs hinges on ongoing advancements in reducing side effects and improving long-term stability. Further research in this area is crucial to maintain the segment’s dominance and drive overall market growth. The projected increase in demand for readily available, safe, and effective alternatives to human blood, combined with technological advancements, ensures that the HBOC segment will remain a key driver of market expansion over the forecast period.

Several key factors are accelerating the growth of the artificial blood industry. These include the ever-increasing demand for blood transfusions worldwide, driven by a rising global population and escalating rates of trauma and chronic diseases. Technological breakthroughs in bioengineering and nanotechnology are leading to more effective and safer artificial blood products with improved oxygen-carrying capacity and reduced side effects. Furthermore, substantial investments from both public and private sectors are funding research, development, and the commercialization of innovative artificial blood substitutes. This concerted effort is translating into a steady stream of new products and improvements to existing technologies. The rising awareness among healthcare professionals and the public regarding the limitations of traditional blood donation systems is further fueling demand.

This report provides a comprehensive overview of the artificial blood market, encompassing market size and growth projections, detailed segmentation analysis, in-depth profiles of key players, and a thorough examination of the industry's driving forces, challenges, and future outlook. The study period (2019-2033) covers both historical performance and future forecasts, providing valuable insights into market trends and dynamics. The detailed analysis helps stakeholders make informed business decisions and capitalize on the opportunities within this rapidly evolving sector. The report highlights the significant potential of artificial blood to address critical global healthcare challenges, such as blood shortages and the risks associated with traditional blood transfusions.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 11.1% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 11.1%.

Key companies in the market include Aurum Biosciences Ltd., HEMARINA SA, HbO2 Therapeutics, KaloCyte Inc., SpheriTech Ltd., NuvOx Pharma, .

The market segments include Type, Application.

The market size is estimated to be USD 3130.7 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Artificial Blood," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Artificial Blood, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.