1. What is the projected Compound Annual Growth Rate (CAGR) of the Antibody Drug Conjugate Therapeutics?

The projected CAGR is approximately 24.74%.

Antibody Drug Conjugate Therapeutics

Antibody Drug Conjugate TherapeuticsAntibody Drug Conjugate Therapeutics by Type (/> Mmunomedics Technology, Immunogen Technology, Seattle Genetics Technology, Others), by Application (/> Lymphoma, Leukemia, Multiple Myeloma, Skin Cancer, Colon Cancer, Glioblastoma, Pancreatic Cancer, Prostate Cancer, Solid Tumor, Breast Cancer), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

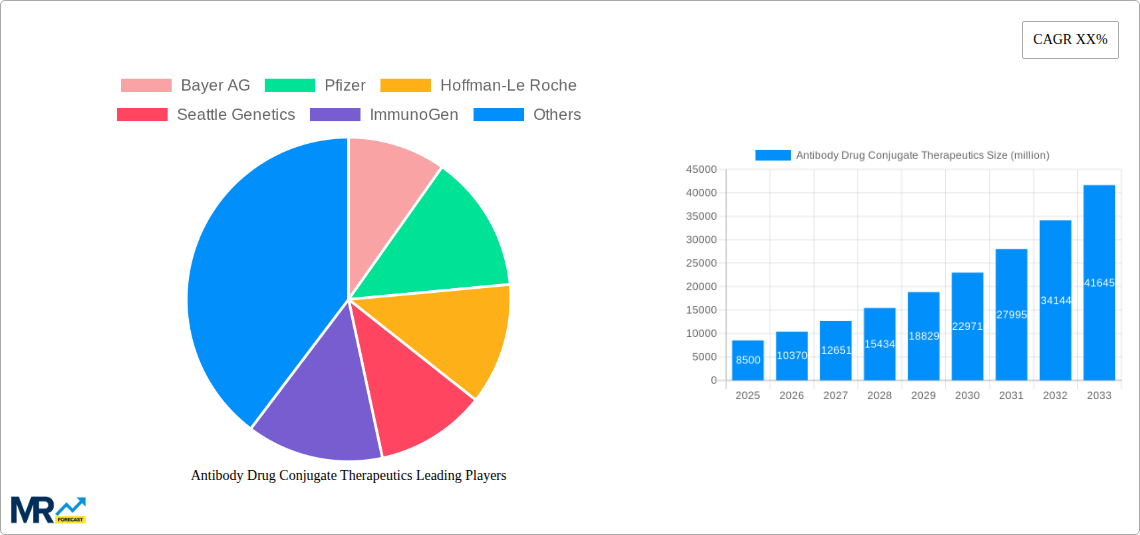

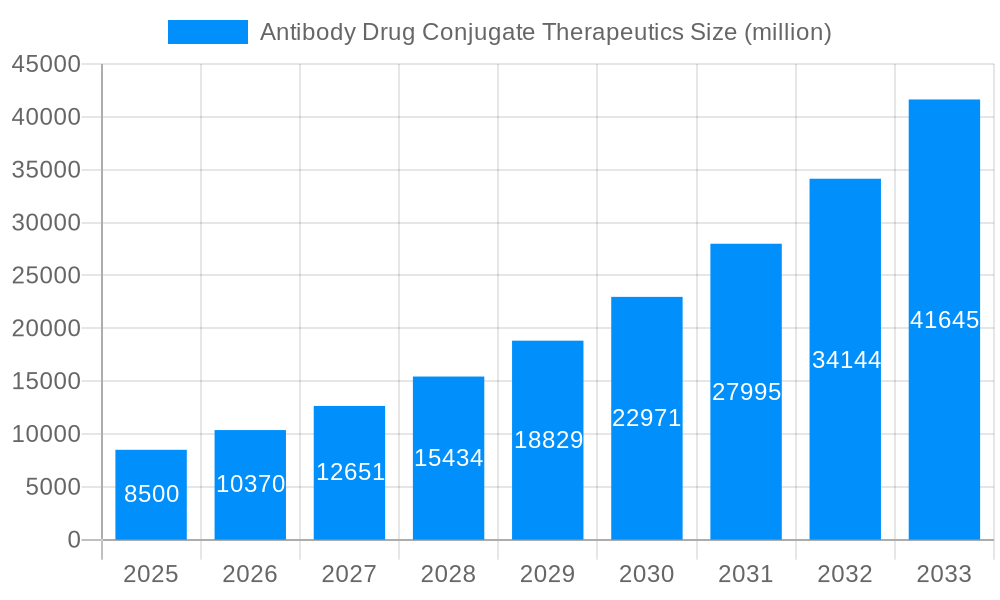

The Antibody Drug Conjugate (ADC) therapeutics market is poised for substantial expansion, driven by the increasing global cancer burden and the demonstrated efficacy of ADCs in precision oncology. The market, valued at $23 billion in the base year of 2024, is projected to grow at a Compound Annual Growth Rate (CAGR) of 24.74%. This robust growth is underpinned by continuous technological advancements in ADC design, leading to enhanced therapeutic profiles and reduced side effects. A burgeoning pipeline of investigational ADCs and increased pharmaceutical R&D investments are further fueling this upward trajectory. Key growth catalysts include the rising incidence of hematological and solid tumors, coupled with a critical need for novel treatment modalities with improved patient outcomes.

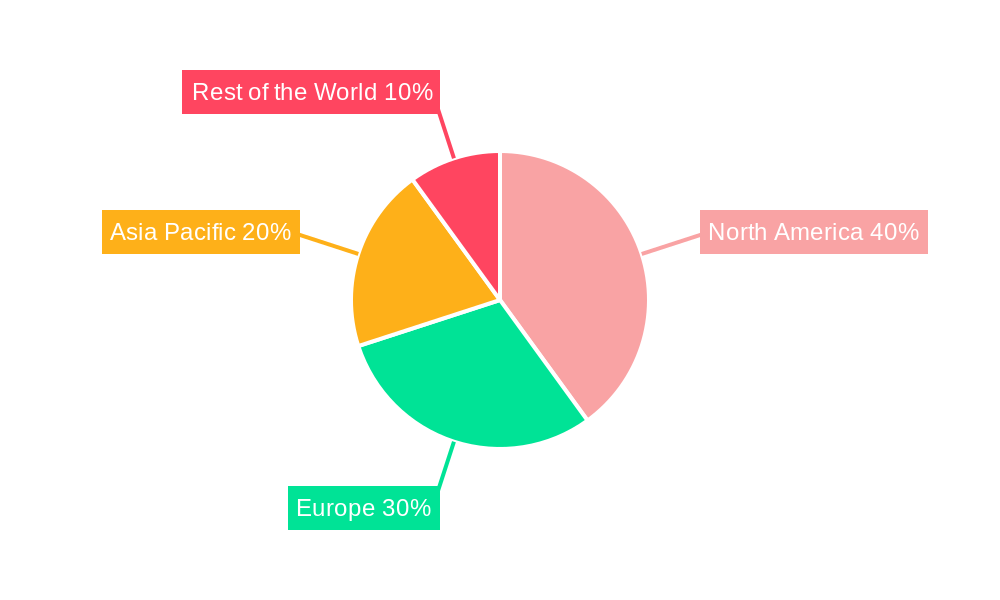

Despite significant progress, the ADC therapeutics market encounters certain obstacles. The high cost of ADC development and manufacturing, alongside the intricate nature of clinical trials, presents considerable challenges. While technological innovations are mitigating potential immunogenicity and toxicity concerns, these remain areas requiring ongoing attention. Nevertheless, strategic research into next-generation payload technologies, advanced linker chemistries, and the expansion of ADC applications into solid tumor treatment are anticipated to drive considerable market growth. Leading entities such as Bayer AG, Pfizer, Roche, and Seattle Genetics are at the forefront of innovation, actively developing and commercializing novel ADC therapies. Market segmentation is primarily based on cancer type, ADC modality, and geographical region, with North America currently leading market share due to substantial healthcare investments and well-established infrastructure.

The Antibody Drug Conjugate (ADC) therapeutics market is experiencing explosive growth, projected to reach multi-billion dollar valuations by 2033. Driven by an increasing prevalence of cancer and a rising demand for targeted therapies, the market witnessed significant expansion during the historical period (2019-2024). The estimated market value in 2025 stands at a substantial figure, reflecting the continued adoption of ADCs across various cancer types. Key market insights reveal a shift towards more sophisticated ADC designs, incorporating improved linker technologies and payloads to enhance efficacy and reduce toxicity. The success of several recently approved ADCs has further fueled investment and innovation in the sector. This is complemented by ongoing clinical trials exploring novel ADC candidates targeting a wider range of cancers, including those with limited treatment options. The forecast period (2025-2033) promises further growth, fueled by technological advancements, expanded clinical applications, and increased market penetration in emerging economies. The competition among established pharmaceutical giants and emerging biotech companies is intensifying, leading to a dynamic market landscape characterized by strategic collaborations, mergers, and acquisitions. A significant portion of the growth is attributed to the development and approval of ADCs with improved safety profiles and targeted delivery mechanisms. These improvements are reducing off-target effects, thereby enhancing patient outcomes and overall market acceptance. Furthermore, the rising prevalence of hematological malignancies and solid tumors is directly impacting demand. Continued research and development are expected to lead to new ADC modalities, potentially impacting the treatment landscape for various diseases beyond oncology in the coming years.

The ADC therapeutics market's remarkable growth is driven by several converging factors. Firstly, the increasing incidence of cancer globally fuels the demand for effective and targeted therapies. ADCs offer a significant advantage over traditional chemotherapy by selectively delivering cytotoxic payloads to cancer cells, minimizing harm to healthy tissues. Secondly, significant advancements in ADC technology have led to improved drug-to-antibody ratios (DAR), enhancing efficacy and reducing side effects. This includes the development of novel linkers and payloads tailored to specific cancer types and tumor microenvironments. Thirdly, the successful launches of several ADCs have demonstrated their clinical efficacy and market viability, encouraging further investment in R&D and expanding market adoption. Finally, the ongoing research and development efforts are exploring new ADC candidates targeting previously untreatable cancers, broadening the market's therapeutic potential. Strategic collaborations between large pharmaceutical companies and smaller biotech firms are accelerating the pace of innovation, facilitating quicker development timelines and broader access to advanced technologies. This collaborative approach is essential for navigating the complexities involved in ADC development, leading to faster and more efficient drug delivery into the market.

Despite the substantial progress, several challenges hinder the widespread adoption of ADC therapeutics. The high cost of developing and manufacturing ADCs presents a significant barrier, particularly in resource-constrained healthcare settings. The complexities involved in conjugating antibodies with cytotoxic payloads require advanced manufacturing capabilities, resulting in high production costs. Furthermore, the potential for immunogenicity and the occurrence of adverse events such as hypersensitivity reactions, hepatotoxicity and nephrotoxicity, remain significant concerns. Regulatory hurdles related to the development and approval of new ADCs can prolong the timeline from discovery to market launch, affecting the overall profitability. The heterogeneity of cancer cells and the development of drug resistance represent significant challenges in achieving long-term efficacy, particularly in solid tumor settings. Ensuring equitable access to ADC therapies in both developed and developing countries remains a considerable challenge, especially given the substantial cost of treatment.

North America: This region is expected to maintain its dominant position due to high healthcare expenditure, advanced infrastructure for clinical trials, and early adoption of innovative therapies. The presence of major pharmaceutical companies and a strong regulatory framework further strengthens its market leadership.

Europe: The European market shows strong growth potential, driven by a rising incidence of cancer and increasing investment in healthcare infrastructure. Stringent regulatory standards and a robust healthcare system contribute to the market's expansion.

Asia Pacific: Rapid economic growth, rising healthcare spending, and an increasing prevalence of cancer are driving market growth in this region. However, regulatory challenges and infrastructure limitations might hinder market penetration to some extent.

Segments: The hematological malignancies segment is currently leading due to the successful launch of several ADCs specifically targeting these cancers. However, significant advancements in ADC technology are expanding the application of ADCs in solid tumors, presenting a promising growth area. The increased focus on developing next-generation ADCs tailored to specific tumor types and with improved efficacy and safety profiles will further drive segment-specific growth. This will involve innovative linker chemistries, novel payloads, and improved antibody targeting mechanisms. The continued success in clinical trials, with the approval of new ADCs against previously difficult-to-treat solid tumors, will influence the market share distribution across various cancer types and treatment segments.

The ADC industry is propelled by continuous innovation in ADC design and delivery, including the exploration of novel payloads, linkers, and antibody engineering strategies to enhance efficacy and reduce toxicity. Simultaneously, the expansion of clinical trials into diverse cancer indications is driving further development and potential market expansion. The increased collaboration between pharmaceutical companies and biotech firms accelerates the pace of development and market entry for novel ADCs.

This report provides a comprehensive analysis of the Antibody Drug Conjugate (ADC) therapeutics market, covering market size, growth drivers, challenges, key players, and future trends. The detailed analysis of the key segments, regional markets, and competitive landscape offers valuable insights for stakeholders involved in the ADC sector. The inclusion of historical data, current market estimations, and future forecasts provides a complete picture of the industry’s evolution and growth potential. This report serves as an essential resource for companies, investors, and researchers seeking a thorough understanding of this rapidly growing therapeutic area.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 24.74% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 24.74%.

Key companies in the market include Bayer AG, Pfizer, Hoffman-Le Roche, Seattle Genetics, ImmunoGen, Genentech, Synthon Holding, Sanofi, Genmab, Amgen, Novartis, Eli Lilly.

The market segments include Type, Application.

The market size is estimated to be USD 23 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Antibody Drug Conjugate Therapeutics," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Antibody Drug Conjugate Therapeutics, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.