1. What is the projected Compound Annual Growth Rate (CAGR) of the Amorphous Metal Core Transformer?

The projected CAGR is approximately XX%.

Amorphous Metal Core Transformer

Amorphous Metal Core TransformerAmorphous Metal Core Transformer by Type (Oil-Immersed Amorphous Core Transformers, Dry-Type Amorphous Core Transformers, World Amorphous Metal Core Transformer Production ), by Application (Factory, Building, Utility Companies, Others, World Amorphous Metal Core Transformer Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

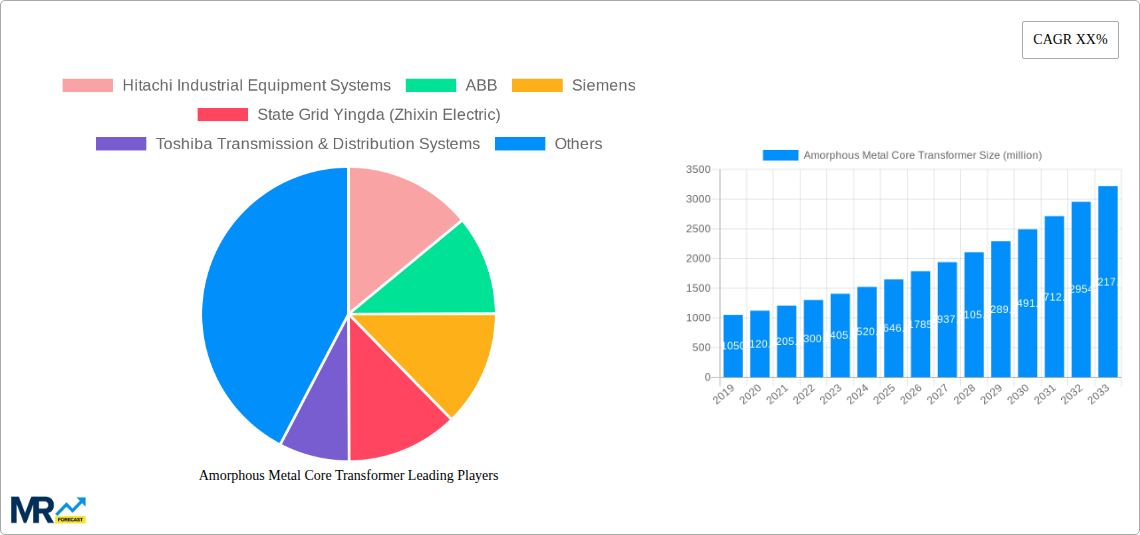

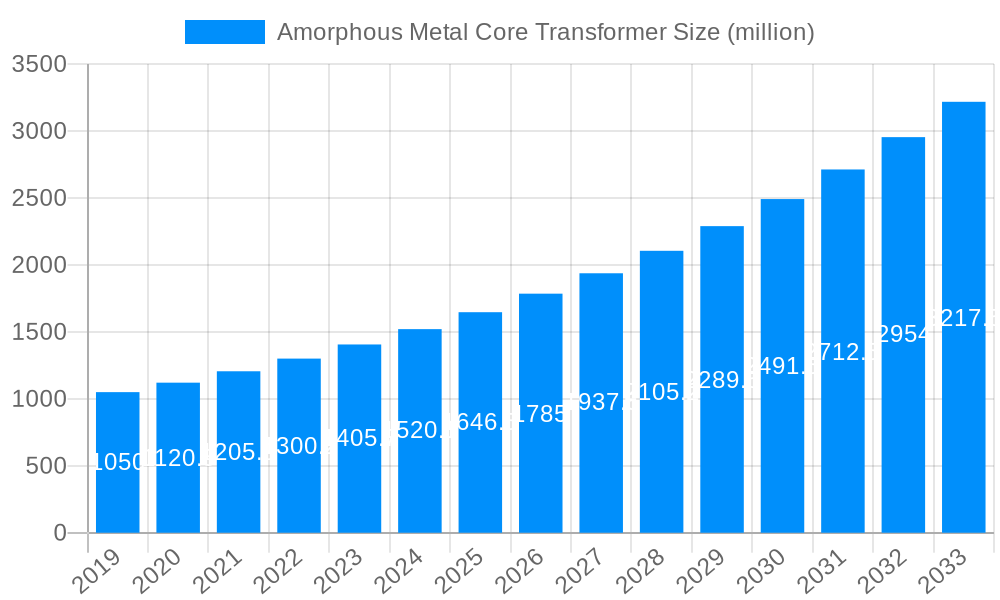

The global Amorphous Metal Core Transformer market is poised for substantial growth, projected to reach USD 1646.5 million by 2025. This expansion is driven by the increasing demand for energy-efficient electrical equipment, stringent government regulations promoting energy conservation, and the superior magnetic properties of amorphous materials, such as lower core losses and higher efficiency compared to traditional silicon steel transformers. The transformer industry is witnessing a significant shift towards these advanced technologies, particularly in applications where energy savings translate directly to operational cost reductions. Key segments like Oil-Immersed Amorphous Core Transformers and Dry-Type Amorphous Core Transformers are expected to see robust demand. The widespread adoption in factory settings, modern buildings requiring high energy efficiency, and utility companies aiming to minimize transmission losses are significant contributors to market acceleration.

The market's upward trajectory is further bolstered by technological advancements in amorphous core manufacturing and transformer design, leading to improved performance and reliability. Key players like Hitachi Industrial Equipment Systems, ABB, and Siemens are actively investing in research and development to expand their product portfolios and cater to the evolving needs of the global energy infrastructure. While the market demonstrates a promising Compound Annual Growth Rate (CAGR) of approximately 8-10% (estimated based on typical market growth for advanced electrical components and the provided market size), challenges such as the relatively higher initial cost of amorphous core transformers compared to conventional ones, and the availability of raw materials for amorphous alloys, could pose moderate restraints. However, the long-term operational cost savings and environmental benefits are increasingly outweighing these initial concerns, paving the way for widespread adoption across North America, Europe, and particularly the Asia Pacific region, which is expected to lead in consumption due to its rapid industrialization and infrastructure development.

The global amorphous metal core transformer market is poised for substantial growth, projected to reach several million units in production volume by the end of the study period in 2033. This upward trajectory is underpinned by a confluence of factors, including escalating energy demands, a global push towards energy efficiency, and stringent environmental regulations. As the world grapples with the imperative to reduce carbon footprints and optimize energy consumption, amorphous metal core transformers are emerging as a critical technology. Their inherent superior energy efficiency, translating to lower no-load losses compared to traditional silicon steel cores, makes them an attractive proposition for a wide array of applications, from industrial facilities to utility grids and commercial buildings. The market’s evolution is also being shaped by significant advancements in material science and manufacturing processes, leading to improved performance characteristics and cost-effectiveness. This report delves into the intricate dynamics of this market, analyzing trends across various segments and applications.

The base year of 2025 presents a pivotal moment, with the market already exhibiting strong momentum. The forecast period from 2025 to 2033 is expected to witness an accelerated adoption rate as more industries and utilities recognize the long-term economic and environmental benefits. The historical period from 2019 to 2024 has laid the groundwork, showcasing the initial penetration and growing acceptance of amorphous core technology. Key market insights indicate a growing preference for oil-immersed amorphous core transformers due to their robustness and suitability for outdoor and high-capacity applications. However, dry-type amorphous core transformers are also gaining traction, particularly in sensitive environments where fire safety and environmental concerns are paramount. The ongoing research and development efforts are focused on further enhancing the performance of amorphous cores, including increasing their saturation flux density and improving their mechanical properties, which will undoubtedly fuel market expansion. The increasing global electricity consumption, coupled with the need for reliable and efficient power distribution, solidifies the strategic importance of amorphous metal core transformers in the coming decade.

The surge in demand for amorphous metal core transformers is primarily driven by the overarching global imperative for energy efficiency and sustainability. As nations across the world set ambitious targets for reducing greenhouse gas emissions and energy consumption, transformers that minimize energy losses become indispensable. Amorphous metal cores, with their significantly lower no-load losses compared to conventional silicon steel cores, offer a tangible solution to this challenge. This translates into substantial operational cost savings for end-users over the lifespan of the transformer, making them a compelling investment. Furthermore, the increasing integration of renewable energy sources into power grids necessitates highly efficient and responsive power transmission and distribution equipment. Amorphous core transformers are well-suited to handle the fluctuations and complexities associated with renewable energy, contributing to grid stability and reliability. The growing awareness among industrial consumers and utility providers about the economic and environmental advantages of these advanced transformers is a key propellant.

Moreover, the development and refinement of amorphous metal alloys and manufacturing techniques have made these transformers more accessible and competitive. Initially, the higher cost of amorphous materials posed a barrier to widespread adoption. However, economies of scale, coupled with technological advancements that optimize production processes, have helped bridge this gap. This makes amorphous core transformers a viable and increasingly preferred option for a broader spectrum of projects. The continuous push for grid modernization and upgrades, particularly in developing economies, also presents a significant growth avenue. As existing infrastructure is replaced and expanded, there is a growing opportunity to incorporate more energy-efficient technologies, with amorphous core transformers leading the charge in this transition. The synergy between regulatory support for energy-efficient technologies and the inherent performance benefits of amorphous cores creates a powerful momentum for market growth.

Despite the promising growth trajectory, the amorphous metal core transformer market is not without its challenges and restraints. A significant hurdle remains the initial cost premium associated with amorphous metal alloys compared to traditional silicon steel. While the operational savings over the transformer's lifetime are substantial, the upfront investment can be a deterrent, especially for smaller utilities or businesses with limited capital budgets. This cost factor can slow down the adoption rate in price-sensitive markets or for standard applications where the efficiency gains are less critical. Another challenge lies in the manufacturing complexity and specialized expertise required for producing amorphous metal cores. The intricate process of rapidly cooling molten metal to form amorphous structures demands sophisticated equipment and highly skilled personnel, which can limit the number of manufacturers capable of producing these cores and, consequently, impact supply chain dynamics and lead times.

Furthermore, the brittle nature of amorphous alloys can present a challenge during handling and transportation. Unlike the more ductile silicon steel, amorphous metals can be more susceptible to damage if not handled with extreme care. This necessitates specialized packaging and logistics, potentially adding to the overall cost and complexity of deployment. The availability of raw materials, particularly critical elements like iron, nickel, and cobalt, can also be a concern, with potential supply chain disruptions and price volatility impacting production costs and availability. While technological advancements are continuously improving the mechanical properties of amorphous alloys, ongoing research and development are crucial to address these limitations fully. The lack of widespread standardization for amorphous core transformers in some regions can also create uncertainty for buyers and designers, hindering widespread adoption. Overcoming these challenges will be crucial for unlocking the full market potential of amorphous metal core transformers.

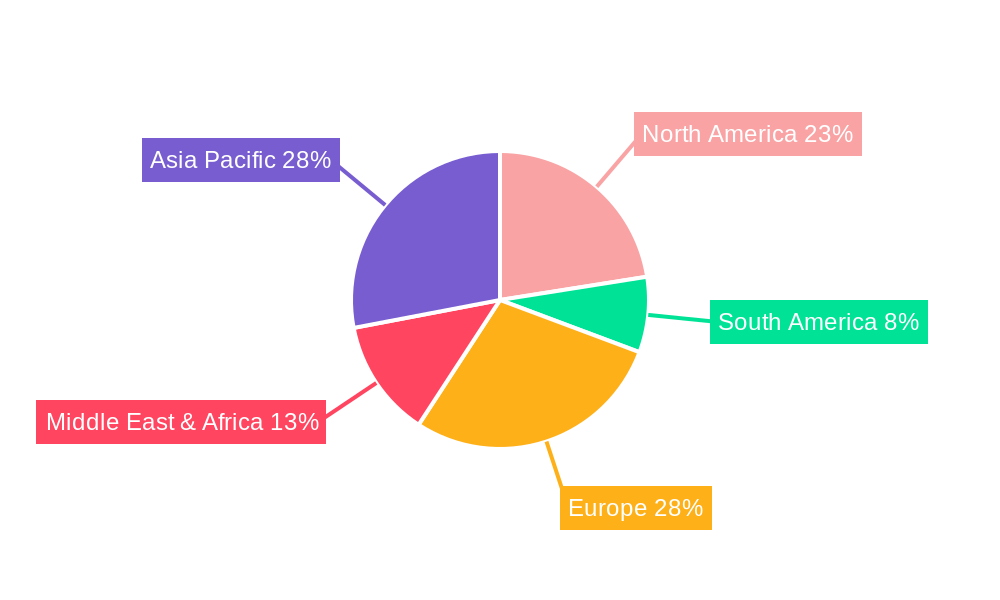

The global amorphous metal core transformer market is experiencing dynamic shifts, with certain regions and segments poised to lead the growth in the coming years. The Asia-Pacific region, particularly China, is expected to be a dominant force in both production and consumption. This dominance is fueled by several converging factors:

Within the Type segment, Oil-Immersed Amorphous Core Transformers are anticipated to continue their reign as the most dominant category, especially in high-capacity applications such as utility substations and industrial power distribution. Their inherent advantages in cooling and insulation make them ideal for demanding environments. However, Dry-Type Amorphous Core Transformers are experiencing a remarkable surge in demand, particularly in applications where environmental sensitivity and safety are paramount. This includes:

In terms of Application, the Utility Companies segment will remain a cornerstone of the amorphous metal core transformer market. The sheer scale of electricity generation, transmission, and distribution managed by utility companies necessitates a vast number of transformers, and the drive for efficiency in this sector directly translates to increased adoption of amorphous core technology. They are crucial for minimizing energy losses across the entire grid, contributing to a more sustainable and cost-effective power supply. The Factory segment is also a significant contributor, driven by industrial electrification and the need for energy-efficient power solutions to reduce operational costs and environmental impact. As manufacturing processes become more sophisticated and energy-intensive, the demand for high-performance, efficient transformers like those with amorphous cores will continue to grow. The Building segment, encompassing commercial and residential structures, is witnessing an increasing trend towards smart building technologies and energy-efficient infrastructure, further boosting the demand for amorphous core transformers, especially the dry-type variants.

The amorphous metal core transformer industry is being propelled by several key growth catalysts. The escalating global focus on energy conservation and environmental protection, driven by international agreements and national policies, is a primary driver. Amorphous cores significantly reduce no-load losses, leading to substantial energy savings and a lower carbon footprint, making them a preferred choice for utilities and industries aiming for sustainability. Furthermore, the increasing demand for electricity, fueled by industrial growth, urbanization, and the electrification of transportation, necessitates efficient power transmission and distribution infrastructure. The technological advancements in amorphous alloy composition and manufacturing processes are leading to improved performance and cost-effectiveness, making these transformers more competitive. Lastly, government incentives and regulations promoting energy-efficient equipment are creating a favorable market environment for their adoption.

This comprehensive report offers an in-depth analysis of the global amorphous metal core transformer market, providing critical insights for stakeholders. It delves into market sizing and forecasting for the Study Period 2019-2033, with a focus on the Base Year 2025 and the Forecast Period 2025-2033. The report meticulously examines key market trends, identifying the driving forces behind market expansion, such as the imperative for energy efficiency and the increasing global electricity demand. It also addresses the challenges and restraints, including cost considerations and manufacturing complexities, that may influence market dynamics. Detailed regional analysis, particularly focusing on the dominance of the Asia-Pacific region and specific countries like China, is provided. Furthermore, the report highlights significant developments, identifies leading players, and explores the growth catalysts that are shaping the future of this vital sector. The comprehensive coverage ensures a thorough understanding of the market landscape, enabling informed strategic decision-making.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Hitachi Industrial Equipment Systems, ABB, Siemens, State Grid Yingda (Zhixin Electric), Toshiba Transmission & Distribution Systems, CG Global, CREAT, Sunten, Yangdong Electric, TBEA, Eaglerise, TATUNG, Henan Longxiang Electrical, Howard Industries, Powerstar, .

The market segments include Type, Application.

The market size is estimated to be USD 1646.5 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Amorphous Metal Core Transformer," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Amorphous Metal Core Transformer, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.