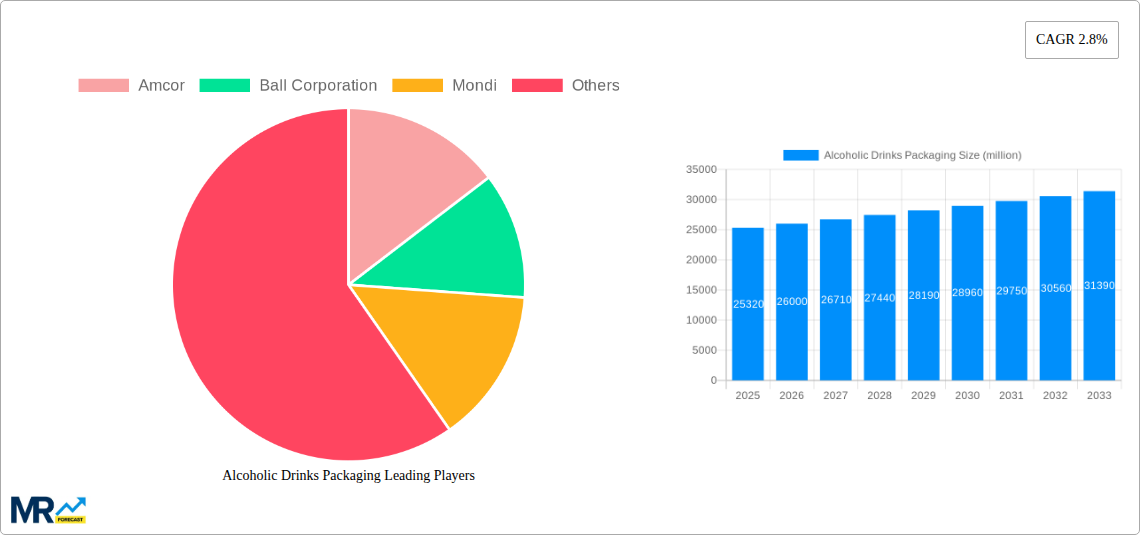

1. What is the projected Compound Annual Growth Rate (CAGR) of the Alcoholic Drinks Packaging?

The projected CAGR is approximately 2.8%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Alcoholic Drinks Packaging

Alcoholic Drinks PackagingAlcoholic Drinks Packaging by Type (Plastic, Metal, Glass, Others), by Application (Beer, Spirits, Wine, Ready-to-drink, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

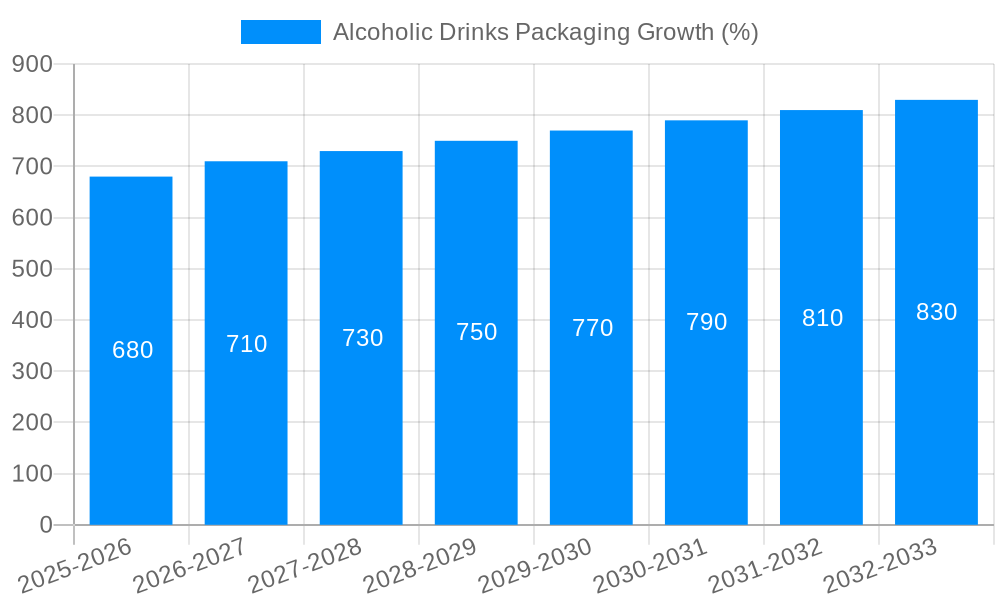

The alcoholic drinks packaging market, currently valued at $25,320 million (2025), is projected to experience steady growth, exhibiting a Compound Annual Growth Rate (CAGR) of 2.8% from 2025 to 2033. This growth is fueled by several key factors. The increasing demand for premium and craft alcoholic beverages, coupled with a rising consumer preference for convenient and sustainable packaging solutions, is driving market expansion. Furthermore, innovations in packaging materials, such as lightweight and recyclable options, are contributing to this positive trend. The rising popularity of e-commerce and direct-to-consumer (DTC) sales models also necessitates robust and protective packaging, further boosting market demand. Major players like Amcor, Ball Corporation, Mondi, Saint Gobain, Tetra Laval, Crown Holdings, Krones AG, and Sidel are actively shaping the market landscape through strategic partnerships, acquisitions, and product diversification. The competitive landscape is characterized by intense innovation and a focus on meeting diverse consumer needs and preferences across different alcoholic beverage categories (e.g., beer, wine, spirits).

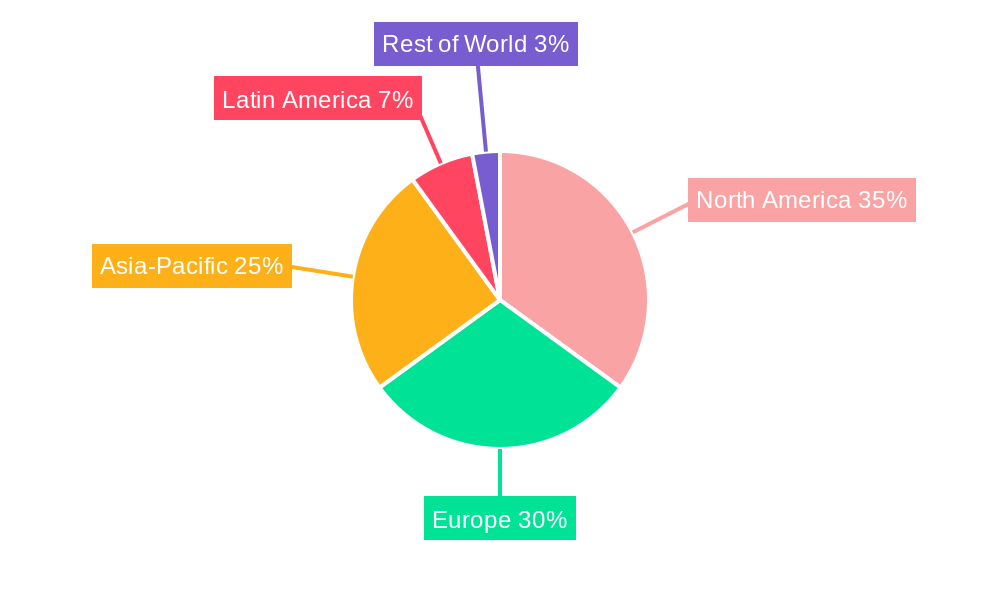

The market segmentation, while not explicitly detailed, is likely diverse, encompassing various packaging types (glass bottles, cans, flexible pouches, etc.) and materials (glass, aluminum, plastic, paperboard). Geographical variations in consumer preferences and regulatory frameworks will also significantly influence regional market growth. While specific regional data is unavailable, it is reasonable to expect North America and Europe to maintain significant market shares, driven by established alcoholic beverage industries and high per capita consumption. Emerging markets in Asia-Pacific and Latin America are expected to demonstrate considerable growth potential, driven by increasing disposable incomes and changing consumption patterns. However, potential restraints such as fluctuating raw material prices and evolving environmental regulations might pose challenges to market expansion in the coming years. Nevertheless, the overall outlook remains positive, with the market poised for sustained growth through 2033.

The alcoholic drinks packaging market, valued at over 500 million units in 2024, is experiencing a dynamic shift driven by evolving consumer preferences and technological advancements. The historical period (2019-2024) witnessed a steady growth trajectory, primarily fueled by the increasing demand for premium and craft alcoholic beverages. Consumers are increasingly drawn to sustainable packaging options, leading to a surge in demand for eco-friendly materials like recycled glass, aluminum, and biodegradable plastics. This trend is further amplified by stringent environmental regulations imposed globally. Simultaneously, the industry is witnessing a rise in innovative packaging formats, including sleek cans, unique bottle shapes, and sophisticated closures, all aimed at enhancing the shelf appeal and consumer experience. The demand for convenience and portability has also led to growth in ready-to-drink (RTD) formats packaged in smaller, more convenient sizes. The estimated year (2025) shows a significant increase in the market size, and the forecast period (2025-2033) projects continued expansion, driven by factors such as rising disposable incomes, particularly in emerging markets, and an increased focus on personalization and brand storytelling through packaging design. The market is becoming increasingly segmented, with specific packaging solutions tailored to different alcoholic beverage types, from wine and beer to spirits and ready-to-drink cocktails. This trend necessitates manufacturers to adapt quickly to evolving consumer demands and technological advancements. The competition in the alcoholic drinks packaging sector is intense, with major players constantly innovating to maintain their market share.

Several key factors are propelling the growth of the alcoholic drinks packaging market. Firstly, the escalating demand for premium and craft alcoholic beverages is a major driver. Consumers are willing to pay more for high-quality products, and sophisticated packaging plays a crucial role in communicating this premium positioning. Secondly, the increasing focus on sustainability is significantly influencing packaging choices. Consumers are actively seeking environmentally friendly options, prompting manufacturers to invest in eco-conscious materials and processes. Thirdly, the rise of e-commerce and online alcohol sales has spurred the demand for robust and tamper-evident packaging solutions to ensure product safety during transit. Finally, the growing popularity of ready-to-drink (RTD) alcoholic beverages, which are often packaged in smaller, more portable formats, contributes to the market's expansion. These trends, coupled with technological advancements in packaging materials and manufacturing processes, are collectively driving the market forward, creating a highly dynamic and competitive environment.

Despite the positive growth outlook, the alcoholic drinks packaging market faces several challenges. Fluctuating raw material prices, particularly for plastics and metals, pose a significant threat to profitability. Stringent regulations regarding the use of certain materials and the increasing focus on sustainability add complexity and cost to the manufacturing process. Maintaining brand consistency and ensuring product integrity across diverse packaging formats and distribution channels also presents a challenge. Furthermore, the need for constant innovation to stay ahead of the competition in terms of design and functionality necessitates significant investments in research and development. The pressure to reduce packaging waste and improve recyclability continues to intensify, placing additional pressure on manufacturers to adopt sustainable practices. Finally, managing the complexities of global supply chains and geopolitical uncertainties further adds to the challenges faced by companies operating in this sector.

The alcoholic drinks packaging market displays significant regional variations. North America and Europe currently dominate the market owing to high consumption levels and strong consumer preference for premium and sustainable packaging. However, Asia-Pacific is showing promising growth potential driven by a burgeoning middle class and increasing alcohol consumption. Within segments, glass bottles continue to hold a significant market share, particularly in the premium wine and spirits categories. However, aluminum cans are experiencing rapid growth due to their lightweight, recyclable nature, and suitability for RTD beverages. Other notable segments include flexible packaging (pouches and bags), used increasingly for convenience and cost-effectiveness, and cartons for wine and other alcoholic beverages.

The market is segmented based on materials (glass, metal, plastic, paperboard, others), product type (wine, beer, spirits, RTD), and packaging type (bottles, cans, pouches, cartons, etc.). The choice of packaging significantly impacts the brand's image and consumer appeal, necessitating a careful balance between sustainability, cost, and functionality.

The alcoholic drinks packaging industry is experiencing significant growth fueled by several key factors. The rising demand for premium and craft alcoholic beverages drives the need for attractive and functional packaging. The increased adoption of sustainable packaging materials and eco-friendly manufacturing practices further fuels this growth. E-commerce growth, increasing disposable incomes in emerging markets, and the rising popularity of ready-to-drink beverages are also significant catalysts. Innovation in packaging design, enhanced functionality, and the introduction of tamper-evident packaging further contribute to the market expansion.

This report provides a comprehensive analysis of the alcoholic drinks packaging market, covering historical data (2019-2024), the estimated year (2025), and a forecast for the period 2025-2033. It delves into key trends, driving forces, challenges, and regional variations, offering insights into the leading players and significant market developments. The report provides valuable information for businesses operating in this dynamic sector, facilitating strategic decision-making and aiding in understanding market opportunities. The comprehensive data and insights contained within will enable stakeholders to develop informed strategies for navigating the evolving landscape of alcoholic drinks packaging.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 2.8% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 2.8%.

Key companies in the market include Amcor, Ball Corporation, Mondi, Ball Corporation, Amcor, Saint Gobain, Tetra Laval, Crown Holdings, Krones AG, Sidel, .

The market segments include Type, Application.

The market size is estimated to be USD 25320 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Alcoholic Drinks Packaging," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Alcoholic Drinks Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.