1. What is the projected Compound Annual Growth Rate (CAGR) of the Airplane Seats?

The projected CAGR is approximately XX%.

Airplane Seats

Airplane SeatsAirplane Seats by Type (First Class Seat, Business Class Seat, Economy Class Seat, Other), by Application (Commercial Aircraft, Military Aircraf, Private Aircraf, World Airplane Seats Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

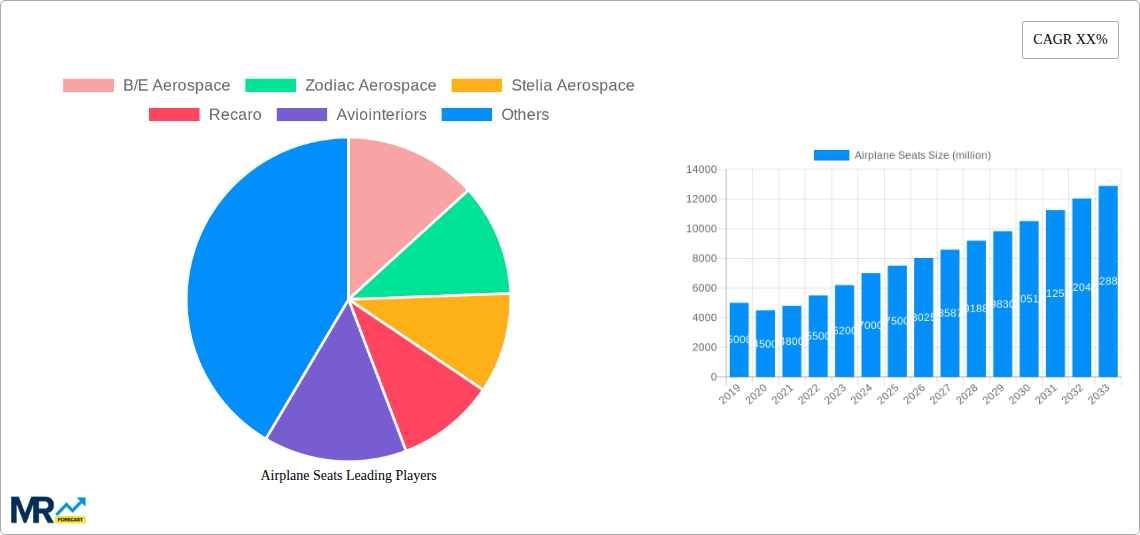

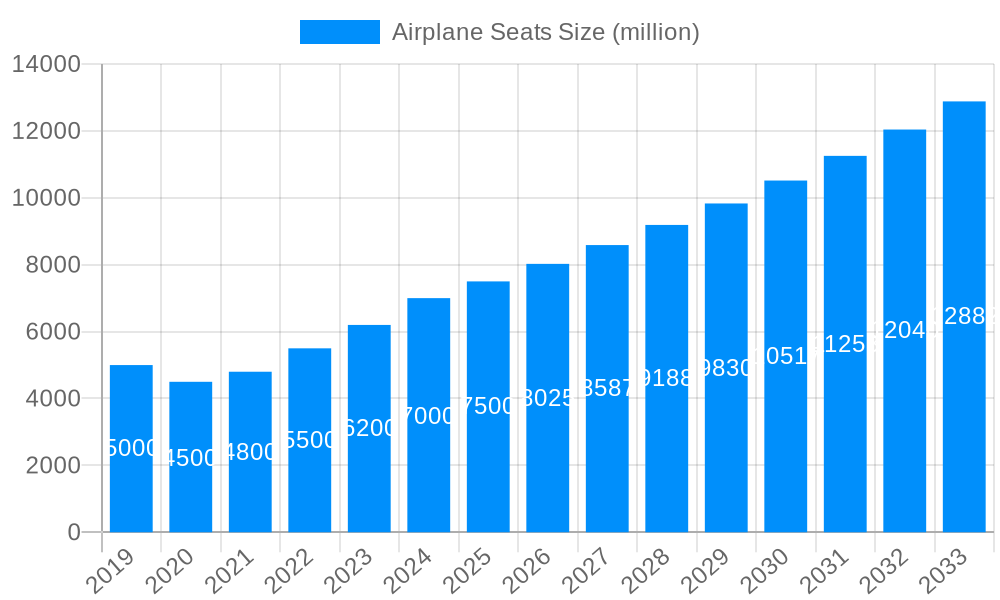

The global airplane seats market is poised for significant expansion, projected to reach an estimated USD 7,500 million by 2025, growing at a robust Compound Annual Growth Rate (CAGR) of 6.5% through 2033. This substantial growth is underpinned by a confluence of factors, including the sustained recovery and expansion of global air travel following recent disruptions, increasing demand for enhanced passenger comfort and premium cabin experiences, and the ongoing modernization of airline fleets with more fuel-efficient and technologically advanced aircraft. The market is witnessing a dynamic shift towards lighter, more ergonomic seat designs that optimize cabin space and reduce aircraft weight, contributing to operational efficiencies for airlines. Furthermore, the rising disposable incomes in emerging economies and the growing trend of budget-conscious travel are driving demand for economy class seats, which constitute the largest segment by volume.

Key growth drivers for the airplane seats market include the substantial backlog of aircraft orders from major manufacturers like Boeing and Airbus, necessitating a consistent supply of new seating solutions. The increasing integration of smart technologies, such as in-flight entertainment systems, USB charging ports, and advanced lighting, is also a significant trend, catering to evolving passenger expectations. However, the market faces certain restraints, including the high capital expenditure associated with seat development and manufacturing, stringent regulatory requirements and certification processes, and the potential for economic downturns to impact airline profitability and consequently, fleet expansion plans. Despite these challenges, the industry is actively pursuing innovation, with a focus on sustainable materials and manufacturing processes, aiming to reduce environmental impact while meeting the burgeoning demand for air travel. The competitive landscape is characterized by the presence of established global players and a growing number of specialized manufacturers, all vying for market share through product differentiation, technological advancements, and strategic partnerships.

This report offers a deep dive into the global airplane seats market, meticulously analyzing historical performance, current dynamics, and future projections. Spanning the Study Period of 2019-2033, with a Base Year and Estimated Year of 2025, and a Forecast Period from 2025-2033, it builds upon the Historical Period of 2019-2024 to provide actionable insights. The analysis encompasses a wide spectrum of seat types, applications, and leading manufacturers, projecting market values in the millions unit.

XXX The global airplane seats market is poised for significant evolution, driven by a confluence of technological advancements, passenger expectations, and airline operational strategies. Over the Study Period (2019-2033), a discernible trend towards enhanced passenger comfort and premium cabin experiences is projected to gain further momentum, particularly within the First Class Seat and Business Class Seat segments. This is not merely about luxury; it's a strategic imperative for airlines seeking to differentiate their offerings and capture higher yields in an increasingly competitive landscape. The demand for reconfigurable and modular seat designs is also on the rise, allowing airlines greater flexibility to adapt cabin layouts to suit changing route demands and passenger preferences. Lightweight materials and innovative ergonomics are paramount, directly impacting fuel efficiency and passenger well-being. In the Economy Class Seat segment, while cost-effectiveness remains a primary concern, there's a growing emphasis on maximizing passenger space through intelligent design and the integration of in-flight entertainment (IFE) and connectivity solutions. The "premium economy" concept continues to mature, bridging the gap between traditional economy and business class, creating a distinct market segment with unique design requirements. The Other category, encompassing specialized seating for military or private aircraft, will witness niche but crucial developments driven by specific operational needs and advanced customization. The overarching trend across all segments is the integration of smart technologies, from personalized lighting and climate control to advanced safety features and biometric integration. The market will also see a continued focus on sustainability, with manufacturers exploring eco-friendly materials and manufacturing processes to reduce the environmental footprint of aircraft seating. The growth of long-haul travel, coupled with the increasing prevalence of wide-body aircraft, will further bolster the demand for sophisticated and comfortable seating solutions. Airlines are increasingly viewing their cabin interiors as a key competitive differentiator, investing heavily in bespoke seat designs that enhance brand identity and passenger satisfaction.

The airplane seats market is being propelled by a powerful set of interconnected drivers. Firstly, the robust recovery and projected growth in global air travel, particularly in the Commercial Aircraft segment, forms the bedrock of this expansion. As passenger traffic steadily climbs post-pandemic, the demand for new aircraft and, consequently, new seating solutions, will naturally surge. Airlines are actively investing in fleet modernization and expansion to cater to this resurgence, creating a substantial order book for seat manufacturers. Secondly, the escalating passenger demand for enhanced comfort and personalized experiences is a critical impetus. Passengers, especially on long-haul flights, are willing to pay a premium for seats that offer superior ergonomics, greater legroom, advanced recline capabilities, and integrated entertainment and connectivity options. This is particularly evident in the First Class Seat and Business Class Seat markets, where airlines compete intensely to offer the most luxurious and productive travel environments. Thirdly, airlines' strategic focus on cabin differentiation and revenue generation plays a pivotal role. Innovative seating designs can significantly influence passenger choice and contribute to higher yields. The introduction of premium economy cabins and the continuous upgrading of business and first-class suites are direct manifestations of this strategy. Furthermore, technological advancements in materials science and manufacturing processes are enabling the development of lighter, stronger, and more durable seats. This not only contributes to fuel efficiency for airlines but also allows for more complex and sophisticated design features. Finally, the ongoing efforts towards sustainability and fuel efficiency are driving innovation in seat design, encouraging the use of lighter materials and optimized structures, thereby indirectly fueling market growth through the development of next-generation seating solutions.

Despite the optimistic outlook, the airplane seats market faces several significant challenges and restraints that could temper its growth trajectory. A primary concern is the stringent regulatory environment and complex certification processes associated with aircraft interiors. Ensuring compliance with safety standards, fire retardancy, and structural integrity demands substantial investment in research, development, and testing, which can be time-consuming and costly for manufacturers. Furthermore, the volatile nature of the aerospace industry, susceptible to global economic downturns, geopolitical instability, and unforeseen events such as pandemics, can lead to significant fluctuations in aircraft orders and, consequently, seat demand. The high capital expenditure required for research, development, and manufacturing of advanced seating solutions can also act as a restraint, particularly for smaller or emerging players. Intense competition among established manufacturers and the increasing complexity of supply chains can put pressure on profit margins. Additionally, rising raw material costs and supply chain disruptions, as experienced in recent years, can impact production schedules and increase manufacturing expenses. The ever-evolving passenger expectations and the need for continuous innovation necessitate ongoing investment in R&D, posing a challenge to maintain competitiveness and profitability. Moreover, the long product development cycles in the aerospace industry, coupled with the substantial lead times for aircraft delivery, mean that market shifts can be slow to materialize, and manufacturers must anticipate future trends with a high degree of accuracy. The increasing focus on sustainability also presents a challenge, requiring significant investment in developing and implementing eco-friendly materials and manufacturing practices, which may not always be cost-effective in the short term.

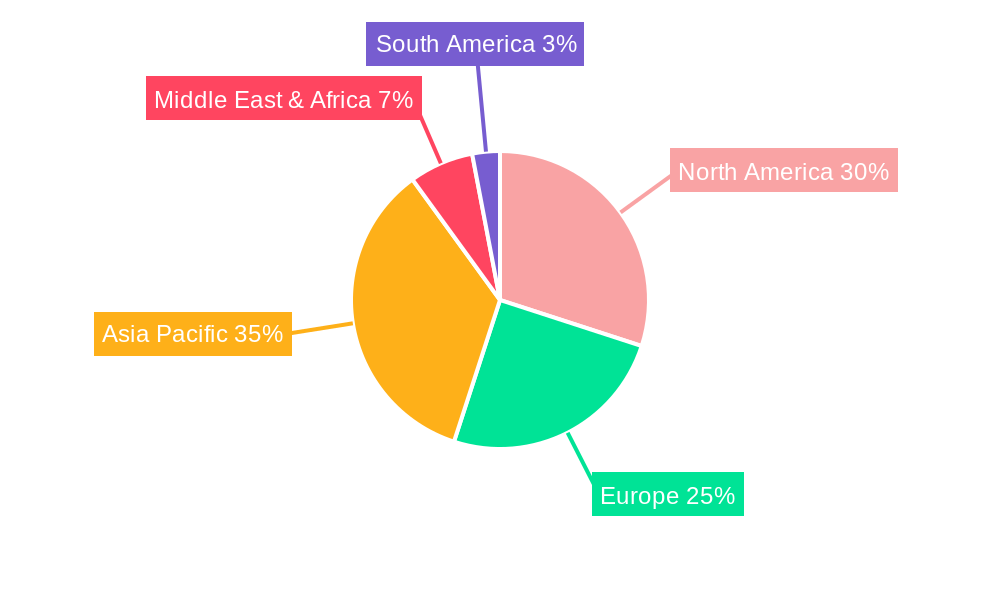

The global airplane seats market is characterized by a dynamic interplay between regional manufacturing strengths and dominant product segments. In terms of regional dominance, North America, particularly the United States, is a key powerhouse. This is driven by the presence of major aircraft manufacturers like Boeing, which necessitate a robust domestic supply chain for aircraft interiors, including seats. The region boasts a high concentration of leading seat manufacturers and a significant installed base of commercial aircraft, fueling ongoing demand for retrofits and new installations. The sheer volume of Commercial Aircraft operations in North America, catering to extensive domestic and international routes, underpins the demand for a vast quantity of Economy Class Seats. However, North America also leads in the adoption of premium cabin configurations due to a strong propensity for business travel and the presence of airlines catering to affluent travelers, thus supporting substantial demand for First Class Seats and Business Class Seats.

Following closely is Europe, home to Airbus, another global aviation giant, and a significant number of prominent airplane seat manufacturers like Zodiac Aerospace, Stelia Aerospace, and Recaro. European airlines are renowned for their focus on cabin innovation and passenger experience, driving demand for advanced and aesthetically pleasing seating solutions across all classes. The European market demonstrates a strong emphasis on sophisticated Business Class Seat designs, often featuring lie-flat capabilities and enhanced privacy. Furthermore, the growing "premium economy" segment is a significant contributor to the European market's growth.

Asia-Pacific is emerging as a rapidly growing and potentially dominant region. Fueled by burgeoning economies, a rapidly expanding middle class, and increasing outbound tourism, the demand for air travel, particularly in the Commercial Aircraft segment, is experiencing unprecedented growth. Countries like China, India, and Southeast Asian nations are witnessing significant fleet expansions by their national carriers, translating into substantial orders for new aircraft and, consequently, airplane seats. The emphasis in this region is currently on increasing the overall capacity with a strong demand for Economy Class Seats, but there is a discernible shift towards upgrading cabin experiences with a growing interest in premium offerings as disposable incomes rise. The region's increasing participation in aircraft manufacturing and assembly, such as the C919 in China, will further solidify its position.

While Commercial Aircraft represent the largest application segment globally due to sheer volume, the Private Aircraft segment, though smaller in scale, commands significant value. The demand for highly customized and luxurious First Class Seat configurations in private jets drives substantial revenue for specialized manufacturers. Similarly, the Military Aircraft segment, while not always publicly reported, involves specialized seating solutions with unique safety and operational requirements, contributing a niche but vital demand.

In terms of seat type dominance, Economy Class Seats constitute the largest share of the market by volume due to the overwhelming number of economy class passengers on commercial flights. However, the Business Class Seat segment is a significant value driver, offering higher margins due to its premium features and customization options. The relentless pursuit of passenger comfort and operational efficiency will continue to shape the trends across all these segments.

Several key catalysts are poised to accelerate growth within the airplane seats industry. The sustained recovery and projected expansion of global air travel volume are fundamental. Airlines are investing in fleet modernization and expansion, directly translating into increased demand for new aircraft seating. Furthermore, the growing passenger inclination towards enhanced comfort and personalized in-flight experiences, particularly in premium cabins, fuels innovation and upgrades. The development and adoption of lightweight, durable, and sustainable materials contribute to fuel efficiency, a crucial factor for airlines, while also enabling more innovative seat designs. The continuous evolution of in-flight entertainment (IFE) and connectivity solutions necessitates integrated seating designs, further driving market demand.

This report provides an exhaustive analysis of the global airplane seats market, offering invaluable insights for stakeholders. It meticulously examines the Type of seats including First Class Seat, Business Class Seat, Economy Class Seat, and Other, as well as their Application across Commercial Aircraft, Military Aircraft, and Private Aircraft. The report delves into market dynamics across the Historical Period (2019-2024), the Base Year and Estimated Year (2025), and projects future trends through the Forecast Period (2025-2033), all within the broader Study Period (2019-2033). It quantifies market values in the millions unit, providing a clear financial perspective. Furthermore, the report identifies the Leading Players in the industry, details Significant Developments, and analyzes key trends, driving forces, challenges, and dominant market regions and segments, offering a holistic understanding of this critical aerospace sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include B/E Aerospace, Zodiac Aerospace, Stelia Aerospace, Recaro, Aviointeriors, Thompson Aero, Geven, Acro Aircraft Seating, ZIM Flugsitz, PAC, Haeco, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Airplane Seats," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Airplane Seats, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.