1. What is the projected Compound Annual Growth Rate (CAGR) of the Aircraft Global Positioning Systems?

The projected CAGR is approximately XX%.

Aircraft Global Positioning Systems

Aircraft Global Positioning SystemsAircraft Global Positioning Systems by Type (Portable GPS, Fixed GPS, World Aircraft Global Positioning Systems Production ), by Application (Military Aircrafts, Civil Aircrafts, World Aircraft Global Positioning Systems Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

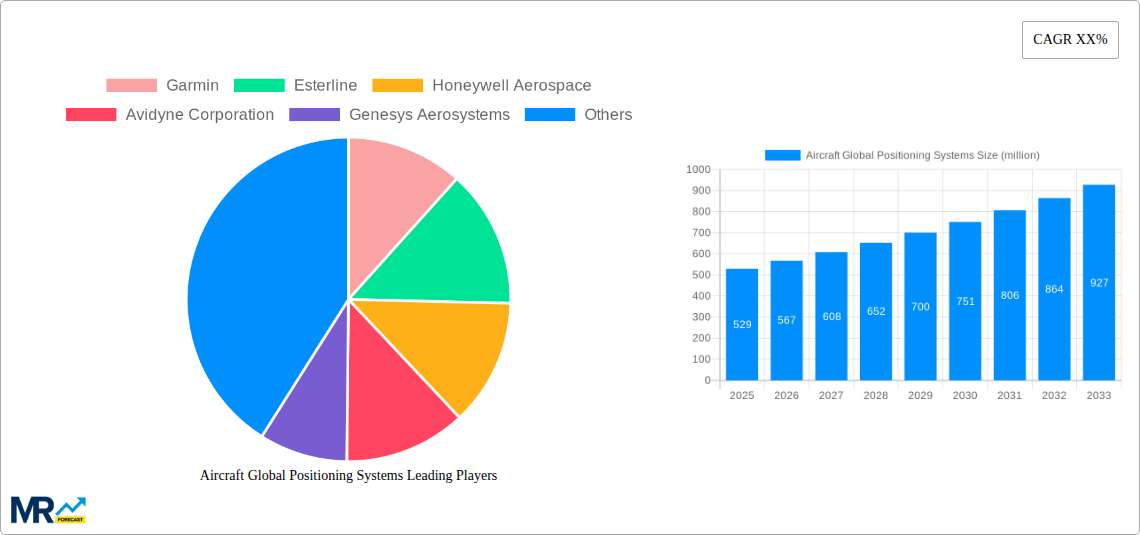

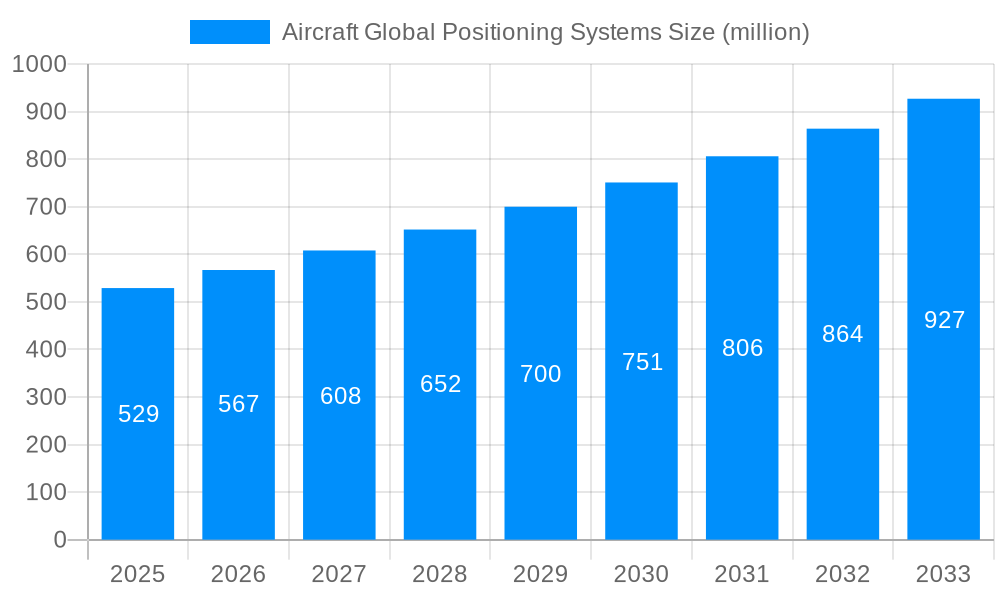

The global Aircraft Global Positioning Systems (GPS) market is poised for robust expansion, projected to reach a substantial market size of $529 million by 2025. This growth is underpinned by an estimated Compound Annual Growth Rate (CAGR) of 7.5% from 2019 to 2033, indicating sustained momentum in the adoption of advanced navigation technologies across both military and civil aviation sectors. Key drivers fueling this expansion include the increasing demand for enhanced flight safety and efficiency, the continuous technological advancements in GPS accuracy and functionality, and the growing integration of sophisticated avionics systems in new aircraft production. Furthermore, the evolving regulatory landscape mandating the use of precise navigation systems for air traffic management and the rising defense spending globally are significant catalysts. The market is segmented into Portable GPS and Fixed GPS, with Portable GPS likely experiencing higher adoption rates in the short to medium term due to its flexibility and cost-effectiveness for retrofitting older aircraft and for specialized applications.

The competitive landscape for Aircraft GPS is characterized by the presence of established aerospace giants and specialized avionics providers, including Garmin, Honeywell Aerospace, and Esterline. These companies are actively engaged in research and development to introduce next-generation GPS solutions with improved capabilities such as enhanced signal reception, anti-jamming features, and seamless integration with other flight management systems. Emerging trends such as the development of multi-constellation receivers (supporting GPS, GLONASS, Galileo, and BeiDou) and the incorporation of AI for predictive navigation are set to further shape market dynamics. However, the market is not without its restraints, including the high cost of initial implementation for some advanced systems, the complexity of integration with existing legacy aircraft, and potential cybersecurity vulnerabilities associated with connected navigation systems. Despite these challenges, the overarching trend towards increased automation and connectivity in aviation, coupled with the inherent need for reliable positioning data, ensures a positive outlook for the Aircraft GPS market.

The global aircraft GPS market is projected to witness a robust expansion, driven by an increasing demand for enhanced navigation, safety, and operational efficiency across both military and civil aviation sectors. During the study period of 2019-2033, with a base year of 2025, the market is expected to surge. The World Aircraft Global Positioning Systems Production segment, encompassing both fixed and portable GPS units, is anticipated to be a significant contributor. In 2025, the estimated production volume of aircraft GPS units is expected to reach an impressive 5.2 million units. This figure is projected to grow steadily throughout the forecast period, reaching approximately 7.8 million units by 2033. The historical period from 2019-2024 laid the foundation for this growth, characterized by gradual technological advancements and increasing adoption rates, especially in emerging aviation markets. The integration of GPS into advanced avionics systems has become a standard, moving beyond basic navigation to encompass sophisticated functionalities like precision approaches, terrain avoidance, and enhanced situational awareness for pilots. The increasing complexity of air traffic management and the need for reduced separation minima further necessitate reliable and precise positioning data, making GPS an indispensable component of modern aircraft. Furthermore, the rise of unmanned aerial vehicles (UAVs) and the expansion of commercial spaceflights are opening up new avenues for GPS application, contributing to the overall market dynamism. The shift towards digital cockpits and the increasing reliance on data-driven decision-making in aviation are also fueling the demand for sophisticated GPS solutions. The market is observing a continuous evolution, with manufacturers focusing on miniaturization, improved accuracy, enhanced security features, and greater interoperability with other avionic systems. The emphasis on global navigation satellite system (GNSS) integrity and the development of augmented systems to improve GPS performance in challenging environments are also key trends shaping the market landscape.

Several compelling factors are driving the expansion of the aircraft global positioning systems market. Foremost among these is the relentless pursuit of enhanced aviation safety. GPS technology provides highly accurate and reliable positional data, which is critical for preventing mid-air collisions, navigating in adverse weather conditions, and executing precision landings. The increasing stringency of aviation regulations globally also mandates the use of advanced navigation systems, directly benefiting the GPS market. Furthermore, the growing complexity of air traffic management systems, particularly in densely populated airspaces, demands precise and real-time location information, which GPS readily provides. The operational efficiency gains offered by GPS are also a significant driver. By enabling more direct flight paths, optimized fuel consumption, and reduced flight times, GPS contributes to cost savings for airlines and operators. The burgeoning unmanned aerial vehicle (UAV) sector, encompassing everything from commercial drones for delivery and surveillance to advanced military reconnaissance platforms, represents a substantial growth area for GPS. These systems are heavily reliant on accurate GPS for autonomous navigation and mission execution. Moreover, the ongoing modernization of military aircraft fleets worldwide, with a focus on incorporating advanced navigation and targeting capabilities, is a consistent and significant demand generator for sophisticated GPS solutions. The continuous evolution of GPS technology, leading to more compact, power-efficient, and feature-rich devices, further stimulates adoption across all aircraft types, from small general aviation planes to large commercial airliners and specialized military platforms.

Despite the promising growth trajectory, the aircraft global positioning systems market faces certain challenges and restraints that could temper its expansion. One of the primary concerns is the vulnerability of GPS signals to interference and jamming. While advancements in anti-jamming technologies are being made, the susceptibility to deliberate or accidental signal disruption remains a potential risk, especially in sensitive military applications or congested airspace. The cost of integrating and maintaining advanced GPS systems can also be a barrier, particularly for smaller aircraft operators or in developing economies where budget constraints are more pronounced. The need for regular software updates, calibration, and potential hardware upgrades to ensure optimal performance and compliance with evolving regulations adds to the overall cost of ownership. Furthermore, the reliance on a global network of satellites means that system downtime, even if infrequent, can have significant implications for aviation operations. The development and implementation of alternative or complementary navigation systems, while offering redundancy, also represent a competitive landscape that GPS providers must navigate. Ensuring the cybersecurity of GPS data and the systems that process it is another crucial aspect that requires continuous vigilance and investment. The increasing complexity of these systems can also lead to a demand for highly specialized technical expertise for installation, maintenance, and troubleshooting, which may not always be readily available. Finally, the potential for signal degradation in certain geographical areas or due to atmospheric conditions, while often mitigated by augmentation systems, can still pose limitations in specific operational scenarios.

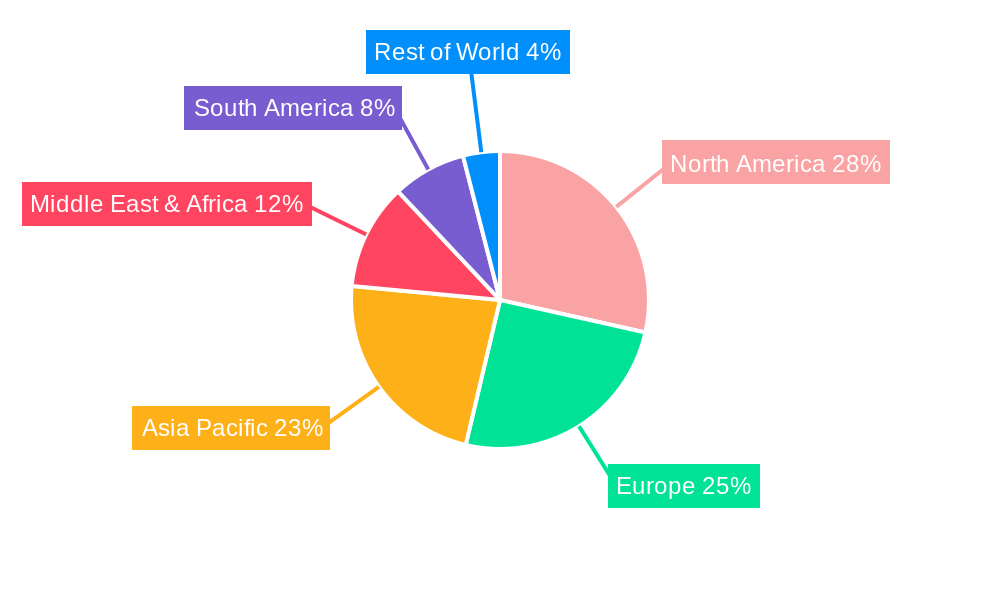

The North America region is anticipated to hold a significant share and potentially dominate the aircraft global positioning systems market throughout the study period (2019-2033), with its peak influence expected around the base year of 2025. This dominance is attributed to a confluence of factors including the presence of a mature aviation industry, substantial investments in defense and aerospace, and stringent regulatory frameworks that promote the adoption of advanced avionics.

Within North America, the United States stands out as a key country driving this dominance. Its expansive airspace, coupled with a large fleet of both civil and military aircraft, creates a consistent demand for advanced GPS solutions. The U.S. Department of Defense is a major consumer of sophisticated GPS technology for its global operations, including precision-guided munitions, navigation, and intelligence, surveillance, and reconnaissance (ISR) missions. This demand fuels innovation and drives the market for high-performance GPS receivers and integrated systems.

On the civil aviation front, North America boasts a high concentration of commercial airlines and general aviation operators. The continuous fleet modernization programs by major airlines, aiming to improve fuel efficiency, safety, and passenger experience, invariably include upgrades to navigation systems, with GPS being a central component. The Federal Aviation Administration (FAA) has been at the forefront of implementing advanced air traffic management systems, such as NextGen, which heavily relies on precise GPS data for enhanced surveillance and efficiency. This regulatory push encourages the adoption of certified GPS equipment across all civil aircraft.

Among the segments, Fixed GPS is expected to be the dominant category, particularly within the North American market. This is driven by the integration of GPS into new aircraft builds and the retrofitting of existing fleets.

While Portable GPS units also play a crucial role, especially in general aviation, flight training, and as backup systems, their market share is typically smaller compared to fixed installations in larger commercial and military aircraft. The total estimated World Aircraft Global Positioning Systems Production in 2025 is expected to be around 5.2 million units, with Fixed GPS representing a substantial portion of this volume, especially in North America. The continuous advancements in miniaturization and accuracy of fixed GPS technology will further solidify its leading position in the market.

The aircraft global positioning systems industry is experiencing a significant growth spurt fueled by several key catalysts. The relentless drive towards enhanced aviation safety, underscored by stringent regulatory mandates and a desire to minimize accidents, is a primary driver. The increasing adoption of performance-based navigation (PBN) and required navigation performance (RNP) procedures, which rely heavily on accurate GPS data for more efficient and safe flight paths, is another major catalyst. Furthermore, the burgeoning unmanned aerial vehicle (UAV) market, encompassing both commercial and military applications, represents a vast and rapidly expanding segment for GPS integration. The modernization of military aviation fleets globally, with a focus on advanced navigation and targeting capabilities, also provides a consistent and significant demand impetus.

This comprehensive report delves deep into the global aircraft global positioning systems market, providing an in-depth analysis of its trajectory from 2019 to 2033, with a specific focus on the base year of 2025. It meticulously examines key market insights, including the estimated World Aircraft Global Positioning Systems Production volume, projected to reach 5.2 million units in 2025 and climb to 7.8 million units by 2033. The report details the driving forces behind this growth, such as enhanced safety regulations and the burgeoning UAV sector, while also addressing significant challenges like signal interference and integration costs. It identifies dominant regions and segments, with North America and the Fixed GPS segment expected to lead the market. Furthermore, the report highlights crucial growth catalysts and provides an exhaustive list of leading players and their significant recent developments. This comprehensive coverage ensures stakeholders gain a holistic understanding of the market's present state and future potential.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Garmin, Esterline, Honeywell Aerospace, Avidyne Corporation, Genesys Aerosystems, Dynon Avionics, FreeFlight Systems, Innovative Solutions and Support, .

The market segments include Type, Application.

The market size is estimated to be USD 529 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Aircraft Global Positioning Systems," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Aircraft Global Positioning Systems, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.