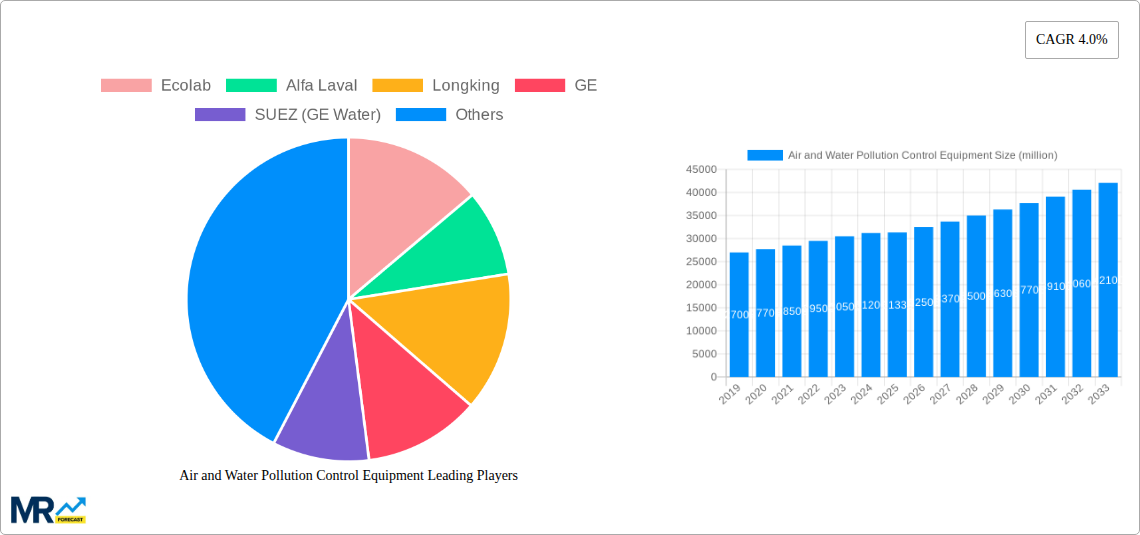

1. What is the projected Compound Annual Growth Rate (CAGR) of the Air and Water Pollution Control Equipment?

The projected CAGR is approximately 4.0%.

Air and Water Pollution Control Equipment

Air and Water Pollution Control EquipmentAir and Water Pollution Control Equipment by Type (Air Pollution Control Equipment, Water Pollution Control Equipment), by Application (Oil and Gas, Mining and Metallurgy, Chemical, Power Generation, Municipal, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

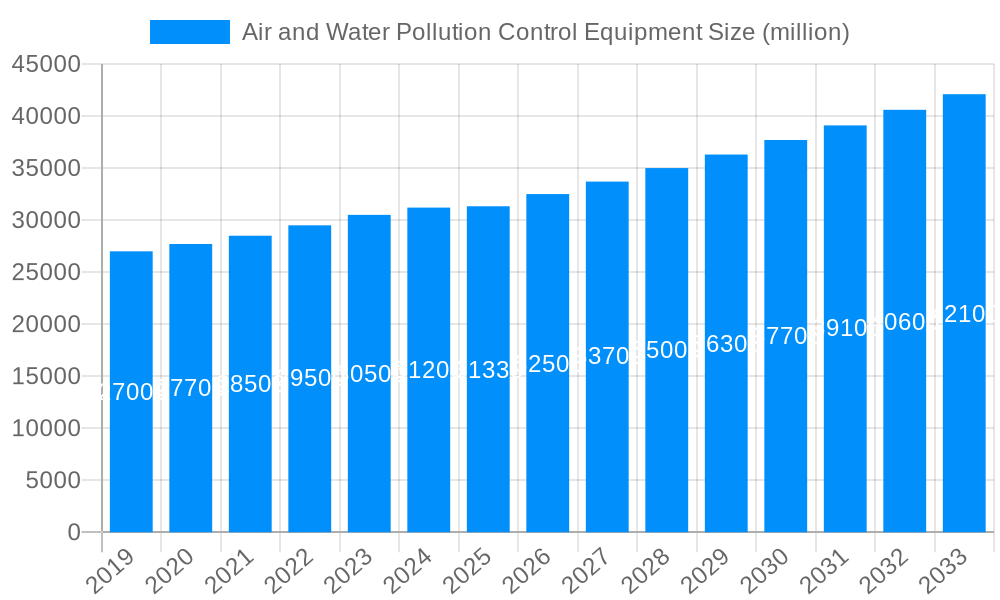

The global Air and Water Pollution Control Equipment market is poised for robust growth, projected to reach approximately $31,330 million by 2025, with a Compound Annual Growth Rate (CAGR) of 4.0% anticipated through 2033. This expansion is fundamentally driven by increasingly stringent environmental regulations worldwide, a growing awareness of the detrimental health and ecological impacts of pollution, and a significant push towards sustainable industrial practices across key sectors. The Oil and Gas, Mining and Metallurgy, Chemical, and Power Generation industries, in particular, are major contributors to this market, as they face intense pressure to mitigate their environmental footprints. Municipal sectors also represent a substantial segment, investing heavily in wastewater treatment and air quality management. The ongoing technological advancements in pollution control equipment, including more efficient filtration systems, advanced scrubbers, and sophisticated monitoring technologies, are further bolstering market demand. Furthermore, the increasing emphasis on circular economy principles and resource recovery from waste streams will create new opportunities for market players.

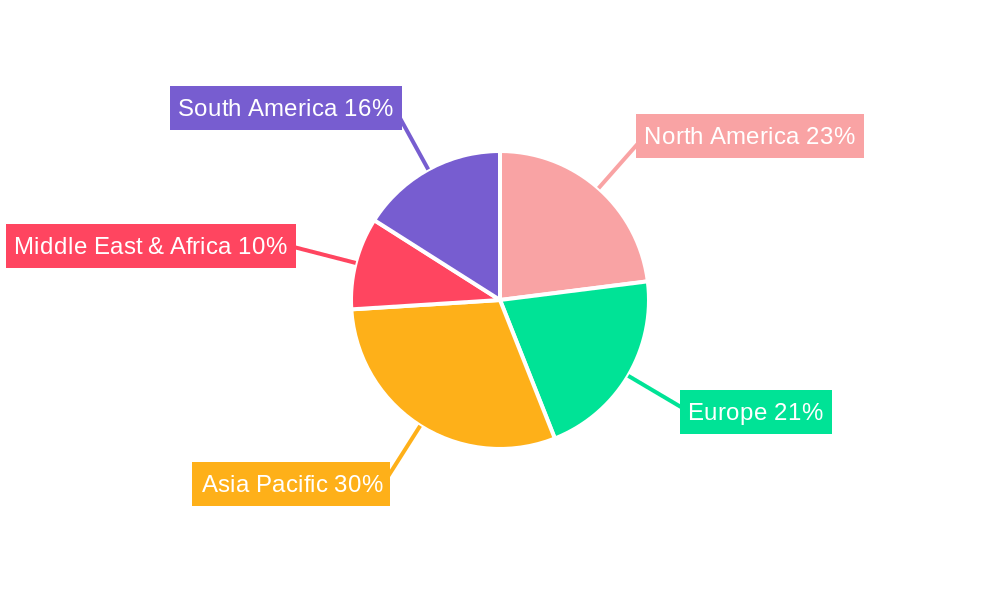

Despite the positive outlook, the market faces certain restraints. High initial capital investment for advanced pollution control systems can be a significant barrier, especially for small and medium-sized enterprises. The operational complexity and maintenance requirements of some advanced technologies also pose challenges. However, the long-term benefits of reduced environmental penalties, improved public health, and enhanced corporate social responsibility are increasingly outweighing these initial concerns. Geographically, Asia Pacific is expected to be a dominant region due to rapid industrialization and a growing focus on environmental protection in countries like China and India. North America and Europe are also significant markets, driven by mature environmental policies and continuous technological innovation. The market landscape is competitive, featuring established players like Ecolab, GE, SUEZ, and Veolia, alongside emerging regional manufacturers, all vying for market share through product innovation, strategic partnerships, and a focus on cost-effective solutions.

Here is a comprehensive report description on Air and Water Pollution Control Equipment, incorporating your specified details and structure:

The global market for Air and Water Pollution Control Equipment is poised for substantial growth, driven by an intensifying focus on environmental sustainability and increasingly stringent regulatory frameworks worldwide. The study period, spanning from 2019 to 2033, with a base and estimated year of 2025 and a forecast period from 2025 to 2033, highlights a dynamic evolution in this sector. During the historical period of 2019-2024, the market witnessed steady expansion as industries began to acknowledge the critical need for pollution abatement. Projections for the base year 2025 indicate a market valuation in the billions of dollars, reflecting the ongoing investments in advanced pollution control technologies.

The trend towards Water Pollution Control Equipment is particularly pronounced, fueled by growing concerns over water scarcity and the contamination of freshwater resources. Industries such as Municipal, Oil & Gas, and Chemical are leading the charge in adopting sophisticated wastewater treatment solutions. This includes membrane filtration, advanced oxidation processes, and biological treatment systems designed to remove a wider spectrum of pollutants, from heavy metals and persistent organic pollutants to microplastics. The market size for water treatment equipment is anticipated to reach several tens of millions by 2025, with significant contributions from regions investing heavily in water infrastructure and recycling initiatives. Simultaneously, the Air Pollution Control Equipment segment is also experiencing robust demand. Power Generation and Mining & Metallurgy sectors, historically significant contributors to air emissions, are increasingly adopting technologies like flue gas desulfurization (FGD), selective catalytic reduction (SCR), and advanced particulate matter filters. The global market for air pollution control equipment is expected to be valued in the hundreds of millions in 2025, driven by stricter air quality standards aimed at reducing greenhouse gas emissions and improving public health. The rise of smart monitoring and control systems, integrating IoT and AI, is also a key trend, enabling real-time performance optimization and predictive maintenance for pollution control assets. Furthermore, the "Others" application segment, encompassing diverse industries like food and beverage, and pharmaceuticals, is also demonstrating consistent growth as these sectors face growing scrutiny regarding their environmental footprint. The cumulative market value for both air and water pollution control equipment is projected to ascend significantly throughout the forecast period, signifying a critical shift towards cleaner industrial practices.

The escalating global demand for Air and Water Pollution Control Equipment is underpinned by a confluence of powerful drivers. Foremost among these is the increasing stringency of environmental regulations enacted by governments worldwide. These regulations, aimed at curbing harmful emissions into the atmosphere and water bodies, mandate industries to invest in state-of-the-art pollution abatement technologies. This regulatory push is particularly evident in developed economies and is gradually extending its influence to emerging markets, creating a broad and consistent demand across sectors. Public awareness and concern regarding environmental degradation and its impact on human health are also playing a pivotal role. Growing pressure from environmental advocacy groups and the general public compels corporations to adopt more sustainable practices and demonstrate their commitment to environmental stewardship. This societal shift influences corporate social responsibility (CSR) initiatives and brand reputation, making pollution control an increasingly strategic imperative. Technological advancements are another significant catalyst. Innovations in materials science, process engineering, and digital technologies are leading to the development of more efficient, cost-effective, and compact pollution control solutions. This includes advancements in areas like advanced oxidation processes for water treatment and novel catalyst technologies for air emission control, which promise higher removal efficiencies and lower operating costs. The economic benefits derived from pollution control, such as resource recovery and improved operational efficiency, are also contributing to market growth. For instance, advanced water treatment systems can facilitate water recycling, reducing reliance on fresh water sources and lowering operational expenses. Similarly, optimized air pollution control can lead to better fuel efficiency and reduced waste generation, presenting a compelling business case for investment.

Despite the robust growth trajectory, the Air and Water Pollution Control Equipment market faces several formidable challenges and restraints that could impede its full potential. A primary concern is the high initial capital expenditure associated with the installation of advanced pollution control systems. For many small and medium-sized enterprises (SMEs), especially in emerging economies, the substantial upfront investment required for cutting-edge equipment can be a significant barrier to adoption, even with the long-term operational benefits. This financial constraint can lead to a slower pace of technological deployment in sectors where margins are tight. Another notable challenge is the complexity of regulatory compliance and enforcement. While regulations are a driving force, the fragmented nature of environmental laws across different regions and countries can create confusion and increase the burden of compliance for multinational corporations. Inconsistent enforcement mechanisms can also lead to a lack of level playing field, where companies in less stringent regions may have a competitive cost advantage. Operational and maintenance costs represent another significant restraint. Pollution control equipment requires regular maintenance, skilled personnel for operation, and the consumption of chemicals or energy, all of which contribute to ongoing operational expenses. For some industries, particularly those with fluctuating production cycles, managing these consistent costs can be a financial challenge. Technological obsolescence and the need for continuous upgrades also pose a challenge. As environmental standards evolve and new pollutants are identified, existing equipment may become outdated, necessitating further investment in retrofits or replacements. This necessitates a long-term strategic planning approach from businesses, which may not always be feasible. Furthermore, public perception and acceptance of certain technologies, particularly those involving large-scale infrastructure, can sometimes be a hurdle. Concerns about noise pollution, visual impact, or the disposal of by-products from pollution control processes can lead to project delays and increased public opposition. The availability of skilled labor to operate and maintain advanced pollution control systems is also a growing concern in some regions, potentially hindering widespread adoption.

The global Air and Water Pollution Control Equipment market is characterized by regional variations in demand, driven by a combination of regulatory landscapes, industrial activity, and environmental priorities. While several regions are experiencing significant growth, Asia Pacific, particularly China and India, is projected to emerge as a dominant force in this market. The rapid industrialization, coupled with a substantial increase in manufacturing output across sectors like Power Generation, Mining and Metallurgy, and Chemical, has led to escalating pollution levels. This, in turn, has prompted governments in these countries to implement and enforce more stringent environmental policies. For instance, China's ambitious "Blue Sky" initiative and India's focus on improving air quality in major cities and its commitment to wastewater treatment have significantly boosted the demand for both air and water pollution control equipment. The sheer volume of industrial operations in these nations, coupled with a growing middle class that is increasingly vocal about environmental concerns, makes them prime markets.

Within this region, the Power Generation segment is a major contributor to the demand for air pollution control equipment. The reliance on fossil fuels for energy generation necessitates advanced technologies like Flue Gas Desulfurization (FGD), Selective Catalytic Reduction (SCR) for NOx control, and Electrostatic Precipitators (ESPs) for particulate matter removal. The market size for these specific air pollution control solutions in the Power Generation sector in Asia Pacific is estimated to be in the hundreds of millions in 2025. Simultaneously, the Municipal segment for water pollution control is also experiencing a surge due to increased investments in sewage treatment plants and wastewater recycling facilities, driven by population growth and water scarcity concerns. The market for water treatment equipment serving municipal needs in this region is also expected to reach tens of millions in 2025.

Another key region exhibiting strong market dominance is North America, driven by well-established environmental regulations and a strong emphasis on technological innovation. The United States, in particular, has a mature market for both air and water pollution control technologies, with significant investments in the Oil & Gas, Chemical, and Power Generation sectors. The increasing focus on methane emission reduction in the Oil & Gas industry and stringent wastewater discharge limits are driving demand for specialized equipment. The market for advanced water treatment technologies in North America is estimated to be in the tens of millions in 2025.

When considering specific segments, Water Pollution Control Equipment is set to experience substantial growth globally, often outpacing the air pollution control segment in certain regions due to the critical need for water resource management. The Municipal segment within water pollution control is a consistently strong performer due to ongoing infrastructure development and public health concerns. In the air pollution control sphere, the Power Generation segment, while facing a transition towards cleaner energy sources, continues to be a significant market due to the existing installed base and the need for retrofitting older plants with advanced emission control technologies. The Oil & Gas sector, despite its volatile nature, presents consistent demand for both air and water pollution control solutions, especially with the growing emphasis on reducing fugitive emissions and treating produced water.

Several key factors are acting as significant growth catalysts for the Air and Water Pollution Control Equipment industry. The most prominent is the increasing global imperative for sustainable development and the integration of Circular Economy principles, pushing industries to minimize waste and maximize resource efficiency. Secondly, ongoing advancements in nanotechnology and advanced materials science are enabling the development of more effective and durable filtration media and catalytic converters, enhancing the performance and lifespan of pollution control devices. The growing adoption of smart technologies, including IoT sensors, AI-driven analytics, and cloud-based monitoring systems, is revolutionizing how pollution control equipment is operated and maintained, leading to optimized performance and reduced downtime. Finally, increased public awareness and demand for cleaner environments, coupled with growing corporate social responsibility commitments, are creating a favorable market environment for pollution control solutions.

This report provides an exhaustive analysis of the Air and Water Pollution Control Equipment market, offering a detailed understanding of the landscape from 2019 to 2033. It delves into the intricate interplay of market dynamics, meticulously dissecting the driving forces and challenges that shape this vital industry. The report offers in-depth segmentation analysis across key types, applications, and industry developments, providing granular insights into market penetration and growth potential. With a focus on the base year 2025 and a comprehensive forecast period extending to 2033, it equips stakeholders with actionable intelligence for strategic decision-making. The report also features a detailed profiling of leading players, highlighting their technological innovations and market strategies. Furthermore, it explores significant regional contributions and emerging trends, ensuring a holistic view of the market's evolution and future trajectory, offering a valuable resource for industry participants, investors, and policymakers alike.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.0% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 4.0%.

Key companies in the market include Ecolab, Alfa Laval, Longking, GE, SUEZ (GE Water), GEA, FLSmidth, Evoqua Water, AAF International, Sumitomo, Foster Wheeler, Feida, Balcke-Dürr, Xylem, Babcock & Wilcox, Ducon Technologies, Wartsila, SPC, Yara Marine Technologies, Dürr AG, Veolia, Sinoma, KC Cottrell, Fives, CECO Environmental, Tianjie Group, HUBER Group, Hamon, Thermax, SHENGYUN, BHEL, Pall Corporation, Jiulong, JOHN ZINK COMPANY, .

The market segments include Type, Application.

The market size is estimated to be USD 31330 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Air and Water Pollution Control Equipment," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Air and Water Pollution Control Equipment, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.