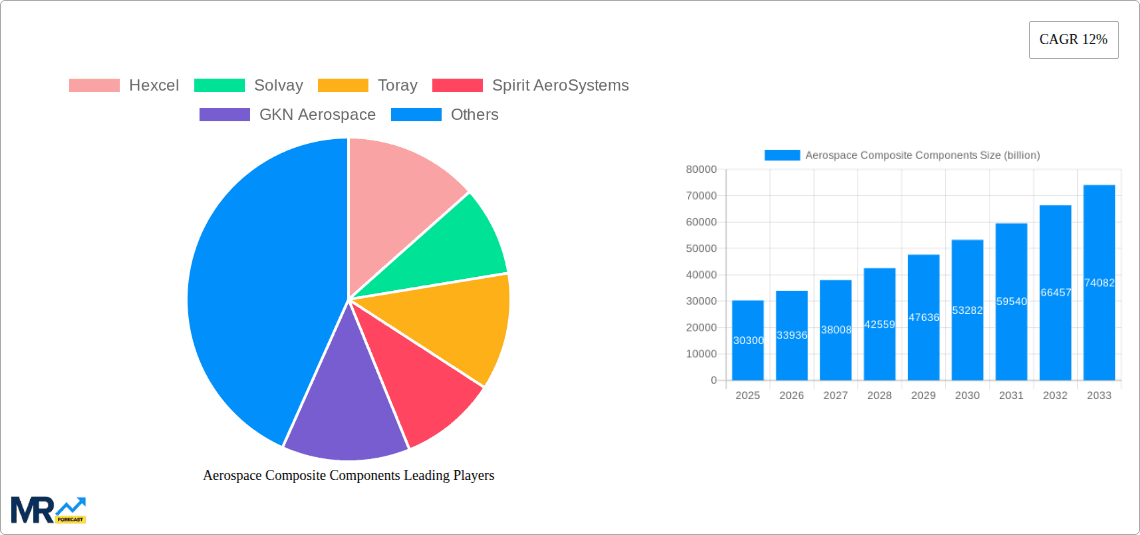

1. What is the projected Compound Annual Growth Rate (CAGR) of the Aerospace Composite Components?

The projected CAGR is approximately 12%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Aerospace Composite Components

Aerospace Composite ComponentsAerospace Composite Components by Type (Components, Aerostructures), by Application (Military Aircraft, Civilian Aircraft, Spacecraft, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

The global Aerospace Composite Components market is poised for significant expansion, projected to reach an estimated USD 30.3 billion in 2025, and demonstrating a robust Compound Annual Growth Rate (CAGR) of 12% during the forecast period of 2025-2033. This impressive growth trajectory is underpinned by a confluence of compelling market drivers. The escalating demand for lighter, more fuel-efficient aircraft across both commercial and military sectors is a primary catalyst. Advanced composite materials offer substantial weight savings compared to traditional metallic components, directly translating into reduced fuel consumption, lower operational costs, and a diminished environmental footprint. Furthermore, the continuous innovation in composite material science, leading to enhanced strength, durability, and performance characteristics, is further propelling market adoption. The increasing production rates of next-generation aircraft programs, coupled with the growing MRO (Maintenance, Repair, and Overhaul) activities for existing fleets, are also contributing to sustained market demand.

Key trends shaping the Aerospace Composite Components landscape include the increasing utilization of carbon fiber reinforced polymers (CFRP) for primary and secondary structures, driven by their superior strength-to-weight ratio. Automation in manufacturing processes, such as automated fiber placement and out-of-autoclave curing, is enhancing production efficiency and reducing costs, making composites more accessible. The growing emphasis on sustainable aviation, including the development of eco-friendly composite materials and advanced recycling techniques, presents a significant future growth avenue. While the market is experiencing a dynamic expansion, potential restraints such as the high initial cost of composite manufacturing equipment, complex repair procedures for composite structures, and the availability of skilled labor could pose challenges. However, the relentless pursuit of technological advancements and the strong economic imperative for fuel efficiency are expected to outweigh these limitations, ensuring a bright future for the aerospace composite components market.

This comprehensive report offers an in-depth analysis of the global Aerospace Composite Components market, forecasting its trajectory from 2019 to 2033. With the Base Year of 2025 and an Estimated Year also of 2025, the Forecast Period spans 2025-2033, building upon insights gleaned from the Historical Period of 2019-2024. The report delves into market valuations expected to reach hundreds of billions of dollars by 2025, providing a granular view of component types, aerostructures, and applications across military, civilian, and space sectors. It meticulously examines the technological advancements, evolving regulatory landscapes, and geopolitical influences that shape this dynamic industry. Furthermore, the report provides actionable intelligence on key regional players, emerging technologies, and strategic imperatives for stakeholders to navigate this rapidly expanding market and capitalize on its immense potential.

The global Aerospace Composite Components market is poised for extraordinary growth, with projections indicating a valuation that will soar into the hundreds of billions of dollars by 2025. This upward trajectory is underpinned by a confluence of factors, including the relentless pursuit of lighter, stronger, and more fuel-efficient aircraft designs. XXX highlights the increasing adoption of advanced composite materials, such as carbon fiber reinforced polymers (CFRPs) and ceramic matrix composites (CMCs), as a fundamental trend. These materials offer superior strength-to-weight ratios, corrosion resistance, and fatigue life compared to traditional metallic alloys, making them indispensable for next-generation aerospace platforms. The report forecasts a significant expansion in the production of composite aerostructures, including wings, fuselage sections, and empennages, as manufacturers increasingly integrate these advanced materials into their primary structures. The demand for composite components is also being propelled by the burgeoning commercial aviation sector, driven by the need to replace aging fleets with more fuel-efficient aircraft, thereby reducing operational costs and environmental impact. Furthermore, the defense sector's continuous innovation in stealth technology, unmanned aerial vehicles (UAVs), and advanced combat aircraft necessitates the use of lightweight and high-performance composite solutions. The space industry, with its ambitious missions and the growing satellite constellations, is also a significant contributor to this market growth. The study will meticulously analyze the nuanced shifts in material preferences, manufacturing techniques, and application-specific demands across these diverse segments. The increasing complexity of aircraft designs, coupled with stringent regulatory requirements for safety and performance, further accentuates the critical role of advanced composite components in shaping the future of aerospace. The market's expansion will be characterized by a steady increase in the average composite content per aircraft, alongside the development of novel composite applications for critical sub-assemblies and interior components.

Several potent forces are collectively driving the remarkable expansion of the Aerospace Composite Components market. Foremost among these is the insatiable demand for enhanced fuel efficiency across all aerospace applications. As airlines and defense agencies grapple with rising fuel costs and increasing environmental regulations, the imperative to reduce aircraft weight has become paramount. Advanced composite materials, with their inherent lightweight properties, offer a direct pathway to achieving significant weight reductions, translating into substantial fuel savings and a smaller carbon footprint. This pursuit of efficiency is particularly pronounced in the civilian aircraft segment, where operational economics heavily influence fleet modernization decisions. Furthermore, the military sector's continuous drive for superior performance in its platforms, including increased maneuverability, extended range, and enhanced stealth capabilities, necessitates the adoption of high-strength, low-weight composite materials. The development of advanced composite manufacturing technologies, such as automated fiber placement and out-of-autoclave curing, is also a significant driver, enabling more cost-effective and scalable production of complex composite parts. This technological advancement is critical for meeting the increasing production rates of new aircraft programs. The growing complexity of modern aircraft designs, featuring more integrated systems and aerodynamic surfaces, further favors the use of composites, which can be molded into intricate shapes with greater ease than metals. The long-term sustainability goals for the aviation industry, pushing for reduced emissions and noise pollution, also indirectly fuel the demand for lighter, more efficient aircraft, and thus composite components.

Despite the robust growth trajectory, the Aerospace Composite Components market is not without its inherent challenges and restraints. A primary concern revolves around the high cost of raw materials and complex manufacturing processes associated with advanced composites. The specialized nature of materials like carbon fiber and the intricate curing cycles required for their integration can contribute to a higher initial investment compared to traditional metallic components. This can be a particular restraint for smaller players or in cost-sensitive applications. Another significant challenge lies in the repair and maintenance of composite structures. While composites offer superior durability in many aspects, their repair can be more complex and require specialized expertise and equipment, potentially leading to higher lifecycle costs. The certification and qualification processes for composite components in aerospace are also notoriously stringent and time-consuming. Ensuring the long-term structural integrity, damage tolerance, and fire resistance of composite parts under various operating conditions requires extensive testing and validation, which can slow down the adoption of new materials and designs. Furthermore, the availability of skilled labor with expertise in composite manufacturing and repair remains a critical bottleneck for the industry's continued growth. The recyclability and end-of-life management of composite materials present an emerging environmental challenge that the industry is actively addressing. Finally, while technological advancements are reducing production costs, the initial capital expenditure for advanced composite manufacturing facilities can be a substantial barrier to entry for new companies, limiting market competition in certain areas.

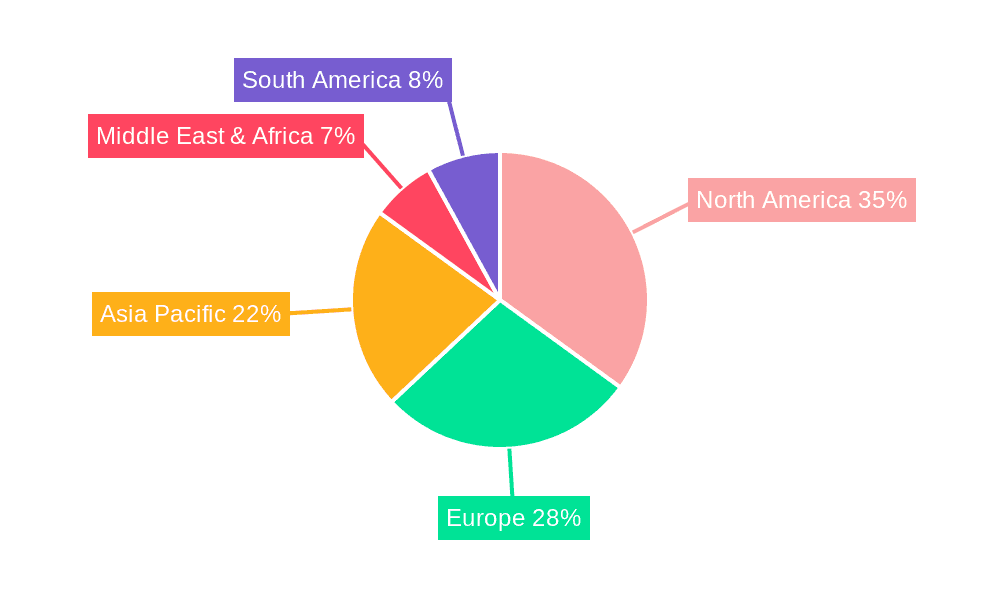

The Aerostructures segment, particularly for Civilian Aircraft, is poised to dominate the global Aerospace Composite Components market. This dominance will be primarily driven by the North America region and the rapidly growing Asia Pacific region.

North America: As the historical hub of aerospace innovation and manufacturing, North America, led by countries like the United States, will continue to exert significant influence. The presence of major aircraft manufacturers such as Boeing, along with key composite material suppliers like Hexcel and Collins Aerospace, forms a robust ecosystem. The demand for new commercial aircraft, driven by fleet modernization and expanding air travel, fuels the need for large-scale composite aerostructures such as wings, fuselage sections, and tail assemblies. The region also benefits from a strong defense sector, further contributing to the demand for advanced composite components in military aircraft. The established infrastructure, skilled workforce, and extensive research and development capabilities in composite technology solidify North America's leading position. The extensive network of tier-1 and tier-2 suppliers integrated within the North American aerospace supply chain ensures efficient production and innovation in aerostructures.

Asia Pacific: The Asia Pacific region, with China at the forefront, is emerging as a powerhouse in the aerospace composite components market. Rapid economic growth, increasing air travel demand, and substantial government investments in domestic aerospace manufacturing are key drivers. Countries like China are actively developing their indigenous aircraft programs, requiring vast quantities of composite aerostructures. The increasing presence of large-scale manufacturing facilities, coupled with a growing skilled workforce, makes this region a critical manufacturing hub. Companies such as Chengdu ALD Aviation Manufacturing, Jialiqi Advanced Composites Technology, and Jiangsu Maixinlin Aviation Science and Technology are increasingly contributing to the global supply chain. The cost-competitiveness and burgeoning production capacity in this region are attracting global manufacturers and facilitating the growth of composite aerostructures for both civilian and military applications. The growing number of airlines operating within the region further amplifies the demand for new aircraft and, consequently, their composite components.

Aerostructures will see the highest growth due to their integral role in aircraft design and performance. The increasing trend towards larger, more fuel-efficient aircraft necessitates the extensive use of lightweight composite materials for primary structural components. The development of advanced composite manufacturing techniques enables the production of complex, integrated aerostructures that offer superior aerodynamic performance and structural integrity. The constant need for fleet renewal in the civilian aircraft sector, driven by passenger demand and environmental regulations, directly translates into a sustained and escalating demand for new composite aerostructures.

The Aerospace Composite Components industry is being invigorated by several potent growth catalysts. The relentless pursuit of fuel efficiency in commercial aviation, driven by cost considerations and environmental mandates, is a primary driver. This leads to increased demand for lightweight composite materials in airframes and engines. The ongoing modernization of military fleets, with a focus on advanced capabilities and stealth technology, also fuels the adoption of high-performance composite components. Furthermore, advancements in composite manufacturing technologies, such as automated fiber placement and additive manufacturing, are enhancing production efficiency and reducing costs, making composites more accessible. The burgeoning space sector, with its ambitious exploration and satellite deployment programs, presents a significant new avenue for composite material applications.

This report provides an exhaustive examination of the Aerospace Composite Components market, offering critical insights into market dynamics, technological advancements, and future opportunities. It meticulously analyzes market valuations expected to reach hundreds of billions by 2025, breaking down segment contributions and regional influences. The study delves into the inherent growth catalysts, such as the drive for fuel efficiency and performance enhancements, while also addressing the significant challenges like material costs and complex manufacturing processes. By examining leading players and significant developments, this report equips stakeholders with the knowledge to navigate this evolving landscape and make informed strategic decisions for long-term success in the aerospace composite components industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 12%.

Key companies in the market include Hexcel, Solvay, Toray, Spirit AeroSystems, GKN Aerospace, Mitsubishi Heavy Industries, Northrop Grumman, Aernnova Aerospace, Saertex, FACC, Safran, General Atomics, Kaman Aerospace, Collins Aerospace, Chengdu ALD Aviation Manufacturing, Jialiqi Advanced Composites Technology, Jiangsu Maixinlin Aviation Science and Technology.

The market segments include Type, Application.

The market size is estimated to be USD 30.3 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Aerospace Composite Components," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Aerospace Composite Components, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.