1. What is the projected Compound Annual Growth Rate (CAGR) of the Aerospace Actuation System?

The projected CAGR is approximately 6.9%.

Aerospace Actuation System

Aerospace Actuation SystemAerospace Actuation System by Application (/> Commercial Aviation, Military Aviation), by Type (/> Flight Control System, Utility Actuation, Auxiliary Control), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

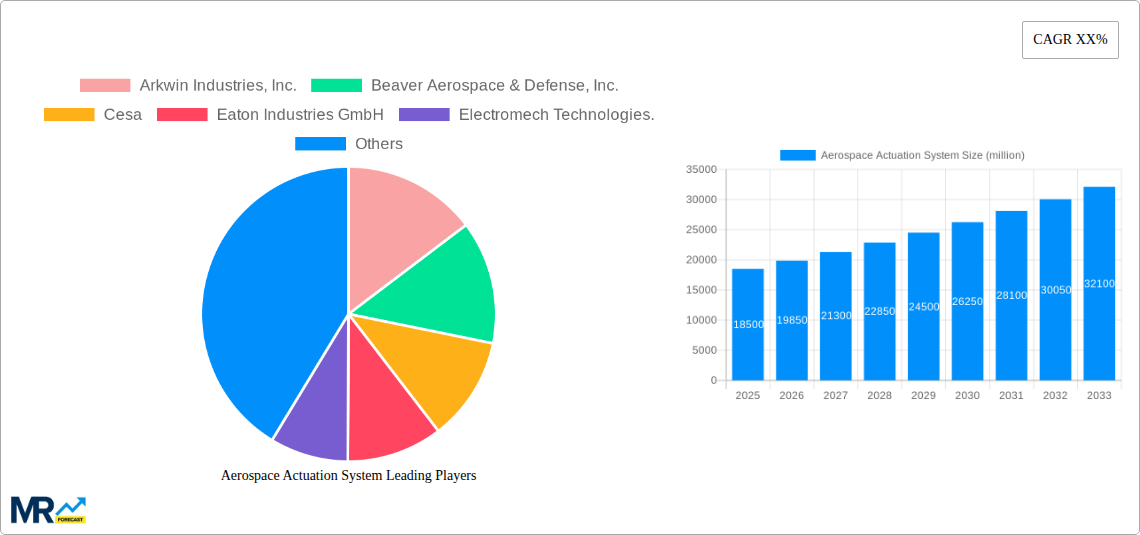

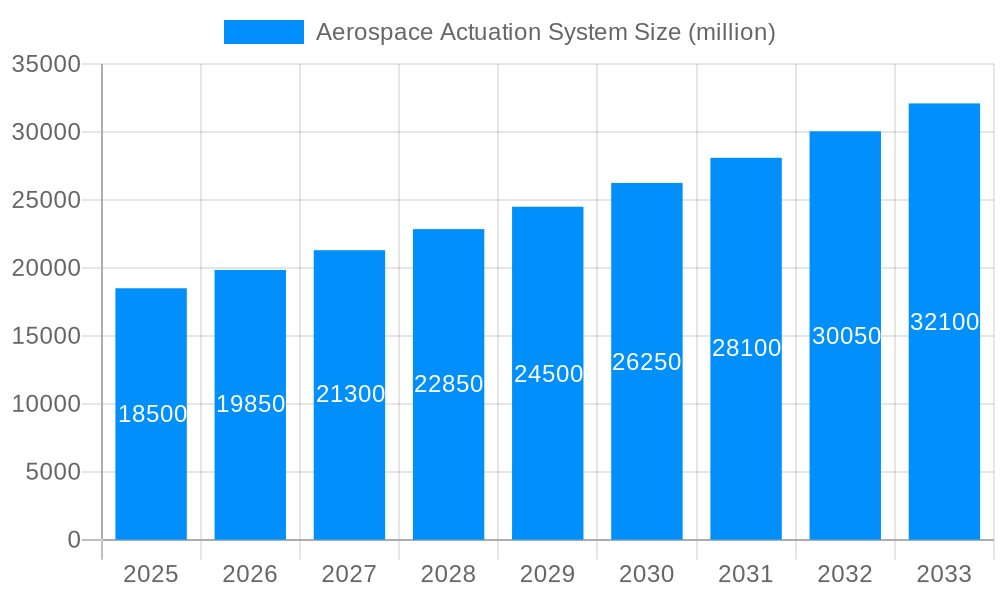

The global Aerospace Actuation System market is projected to reach a market size of 577.1 million by 2025, with a compound annual growth rate (CAGR) of 6.9% from 2025 to 2033. This growth is driven by increasing demand for new commercial and military aircraft, fueled by rising air travel and defense spending. Technological advancements in fly-by-wire systems and the development of more electric aircraft (MEA) necessitate advanced, precise, and reliable actuation systems. Aircraft modernization and fleet replacement also contribute to sustained demand.

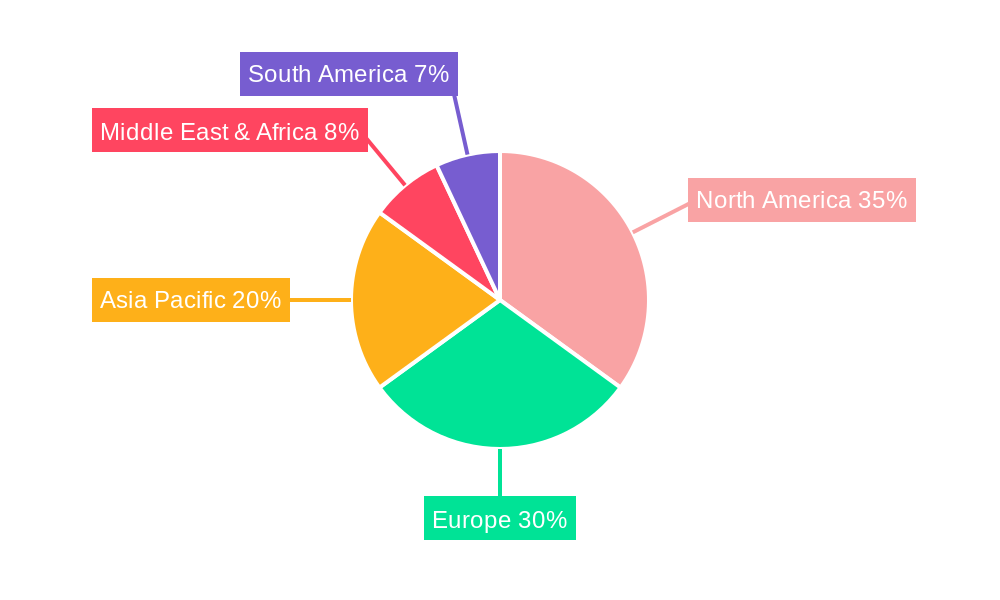

The market is segmented by application into Commercial Aviation and Military Aviation, with Commercial Aviation anticipated to lead due to expanding global air passenger and cargo traffic. By type, the segments are Flight Control Systems and Utility Actuation, both vital for aircraft operation and safety. Innovations in electric and hydraulic actuation are enhancing flight control systems. Key industry players, including Honeywell International Inc., Moog Inc., and PARKER HANNIFIN CORP., are investing in R&D to offer novel solutions. Geographically, North America and Europe are expected to maintain leadership due to established aerospace manufacturers and strong defense sectors. The Asia Pacific region, particularly China and India, is projected for rapid growth, driven by aviation infrastructure expansion and increased defense procurement. Market restraints, such as regulatory compliance and high development costs, are present but are outweighed by strong growth drivers.

This report provides an in-depth analysis of the dynamic Aerospace Actuation System market from 2019 to 2033, focusing on the base year 2025 and the forecast period 2025-2033. It examines market trajectory, key trends, drivers, challenges, and significant developments, highlighting dominant segments and leading players.

The global Aerospace Actuation System market is poised for significant expansion, driven by an insatiable demand for advanced aircraft and evolving technological landscapes. Our study projects a market value that will transcend $5,000 million by the end of the forecast period. This growth is underpinned by several key trends. Firstly, the increasing complexity and sophistication of modern aircraft necessitate highly reliable and precise actuation systems. The integration of fly-by-wire and electric/hybrid-electric propulsion technologies is a prime example of this trend, demanding actuation systems that are lighter, more energy-efficient, and capable of handling higher loads and faster response times. The ongoing fleet modernization programs across both commercial and military aviation sectors are also a substantial driver, as older aircraft are retired and replaced with newer, more technologically advanced models that inherently incorporate cutting-edge actuation solutions.

Furthermore, the rise of unmanned aerial vehicles (UAVs), encompassing both military drones and emerging commercial applications like delivery services, is creating a new and rapidly growing segment for actuation systems. These platforms, often designed for autonomous or remotely piloted operations, require specialized and often miniaturized actuation solutions for control surfaces, landing gear, and payload deployment. Safety and reliability remain paramount, with continuous advancements in redundancy, fault tolerance, and diagnostic capabilities being integral to the evolution of actuation systems. This focus on enhanced safety features, driven by stringent regulatory requirements and the inherent risks associated with aviation, is pushing innovation in areas like electro-hydrostatic actuators and advanced control algorithms. The increasing emphasis on sustainable aviation is also influencing actuation system design, with a push towards electrification and reduced energy consumption. This translates to a demand for more efficient hydraulic systems, advanced electromechanical actuators, and innovative solutions that minimize power draw and environmental impact. The forecast period is expected to witness a notable shift towards more electric aircraft (MEA) architectures, further accelerating the adoption of electromechanical and electro-hydrostatic actuation systems at the expense of traditional hydraulic systems in certain applications. The market is also characterized by increasing consolidation and strategic partnerships, as companies seek to leverage synergistic capabilities and expand their product portfolios to meet the diverse needs of the aerospace industry. The robust research and development efforts by key industry players are continually pushing the boundaries of what is possible in terms of performance, efficiency, and weight reduction, thereby fueling sustained market growth.

Several powerful forces are collectively propelling the growth of the Aerospace Actuation System market. The most significant driver is the unabated demand for new aircraft, fueled by a burgeoning global population, increasing air travel, and the continuous need for modernization of existing fleets. Commercial aviation, in particular, is experiencing robust growth, necessitating the production of thousands of new passenger and cargo aircraft, each equipped with numerous actuation systems. Similarly, the defense sector's ongoing investment in advanced military aircraft, including fighter jets, bombers, and surveillance platforms, further bolsters this demand. The push towards more electric aircraft (MEA) architectures is a transformative trend, leading to a gradual but significant shift away from traditional hydraulic systems towards electromechanical and electro-hydrostatic actuators. This transition is driven by the advantages of MEA, including reduced weight, lower maintenance requirements, improved fuel efficiency, and enhanced system integration.

The rapidly expanding unmanned aerial vehicle (UAV) sector, encompassing military drones for reconnaissance and combat, as well as emerging commercial applications for package delivery, agriculture, and infrastructure inspection, is creating a substantial new market for specialized actuation systems. These UAVs often require highly integrated, compact, and energy-efficient actuators. Furthermore, government initiatives and defense budgets globally continue to allocate significant resources towards upgrading military capabilities, which directly translates to the development and procurement of new aircraft and associated actuation systems. The continuous pursuit of enhanced aircraft performance, including increased maneuverability, greater payload capacity, and improved operational efficiency, necessitates the development of more advanced and responsive actuation solutions. Finally, the stringent safety and reliability standards mandated by aviation authorities worldwide are a constant impetus for innovation, driving the development of more robust, fault-tolerant, and precisely controlled actuation systems.

Despite the promising growth trajectory, the Aerospace Actuation System market faces several significant challenges and restraints. One of the primary hurdles is the exceptionally long and stringent certification process for aerospace components. Any new actuation system or modification to existing ones must undergo rigorous testing and validation to meet the highest safety and reliability standards set by regulatory bodies like the FAA and EASA. This lengthy certification process can add considerable time and cost to product development, potentially delaying market entry for innovative solutions. The high capital investment required for research, development, and manufacturing of sophisticated aerospace actuation systems is another considerable barrier, particularly for smaller companies. The specialized tooling, advanced materials, and highly skilled workforce needed demand substantial upfront investment, which can be a deterrent.

The complex global supply chain, inherent in the aerospace industry, also presents challenges. Disruptions, whether due to geopolitical events, natural disasters, or material shortages, can significantly impact production timelines and costs. The specialized nature of many actuation components means that a single point of failure in the supply chain can have cascading effects. Furthermore, the industry is highly dependent on skilled engineers and technicians. A shortage of qualified personnel with expertise in areas like electro-mechanics, hydraulics, and advanced control systems can hinder innovation and production. The increasing demand for sustainable and environmentally friendly solutions also presents a challenge. While there is a strong push towards electrification and reduced energy consumption, developing actuation systems that meet these goals without compromising performance, weight, or cost is a complex engineering feat. Finally, the highly competitive nature of the market, with established players and emerging technologies vying for market share, can lead to pricing pressures and reduced profit margins.

Dominant Segments and Regions

This section highlights the key segments and regions poised to dominate the Aerospace Actuation System market. The insights presented here are crucial for understanding market dynamics and identifying areas of significant opportunity and influence.

Dominant Application Segments:

Dominant Type Segments:

Dominant Regions:

The interplay between these dominant segments and regions creates a dynamic market landscape. The continuous demand from commercial aviation for new aircraft, coupled with the high-value procurement from military aviation, ensures a steady stream of business. Within these applications, the critical nature of flight control systems and the widespread need for utility actuation ensure their consistent market relevance. Geographically, North America and Europe, with their robust aerospace manufacturing capabilities and significant aircraft production volumes, will continue to lead in terms of market share and influence.

The Aerospace Actuation System industry is experiencing a surge in growth, propelled by several key catalysts. The accelerating global demand for air travel, leading to increased aircraft production and fleet expansion, is a primary driver. Furthermore, the ongoing trend towards more electric aircraft (MEA) architectures is significantly boosting the adoption of electromechanical and electro-hydrostatic actuators, offering advantages in weight, efficiency, and integration. The burgeoning unmanned aerial vehicle (UAV) market, encompassing both military and emerging commercial applications, is creating entirely new avenues for actuation system demand. Lastly, continuous technological advancements in areas like digitalization, smart actuators with integrated sensors, and advanced control algorithms are enabling more precise, reliable, and efficient actuation solutions, further fueling industry growth.

The Aerospace Actuation System market is characterized by the presence of several prominent global players who are instrumental in driving innovation and meeting the diverse needs of the industry. These companies possess extensive expertise in hydraulic, electromechanical, and electro-hydrostatic actuation technologies.

The Aerospace Actuation System sector has witnessed numerous significant developments over the study period, showcasing a relentless pursuit of innovation and efficiency.

This comprehensive report offers an exhaustive analysis of the Aerospace Actuation System market, spanning the historical period of 2019-2024 and extending through the forecast period of 2025-2033. The study meticulously examines market trends, drivers, challenges, and opportunities, providing actionable insights for stakeholders. It features detailed segmentations by application (Commercial Aviation, Military Aviation) and type (Flight Control System, Utility Actuation, Auxiliary Control), alongside a granular regional analysis. The report delves into the technological advancements shaping the industry, including the growing adoption of electric and hybrid-electric actuation systems, and the integration of smart technologies. With detailed market size estimations, CAGR projections, and competitive landscape analysis featuring leading players like Honeywell, Moog, and Parker Hannifin, this report serves as an indispensable resource for strategic decision-making within the aerospace industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.9% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.9%.

Key companies in the market include Arkwin Industries, Inc., Beaver Aerospace & Defense, Inc., Cesa, Eaton Industries GmbH, Electromech Technologies., General Electric., Honeywell International Inc., Moog Inc., PARKER HANNIFIN CORP., UTC Aerospace Systems., .

The market segments include Application, Type.

The market size is estimated to be USD 577.1 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Aerospace Actuation System," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Aerospace Actuation System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.