1. What is the projected Compound Annual Growth Rate (CAGR) of the 6-Inch N-Type Silicon Carbide Wafer?

The projected CAGR is approximately 6.2%.

6-Inch N-Type Silicon Carbide Wafer

6-Inch N-Type Silicon Carbide Wafer6-Inch N-Type Silicon Carbide Wafer by Type (Conductive SiC Wafer, Semi-Insulating SiC Wafer), by Application (Power Device, Electronics & Optoelectronics, Wireless Infrastructure, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

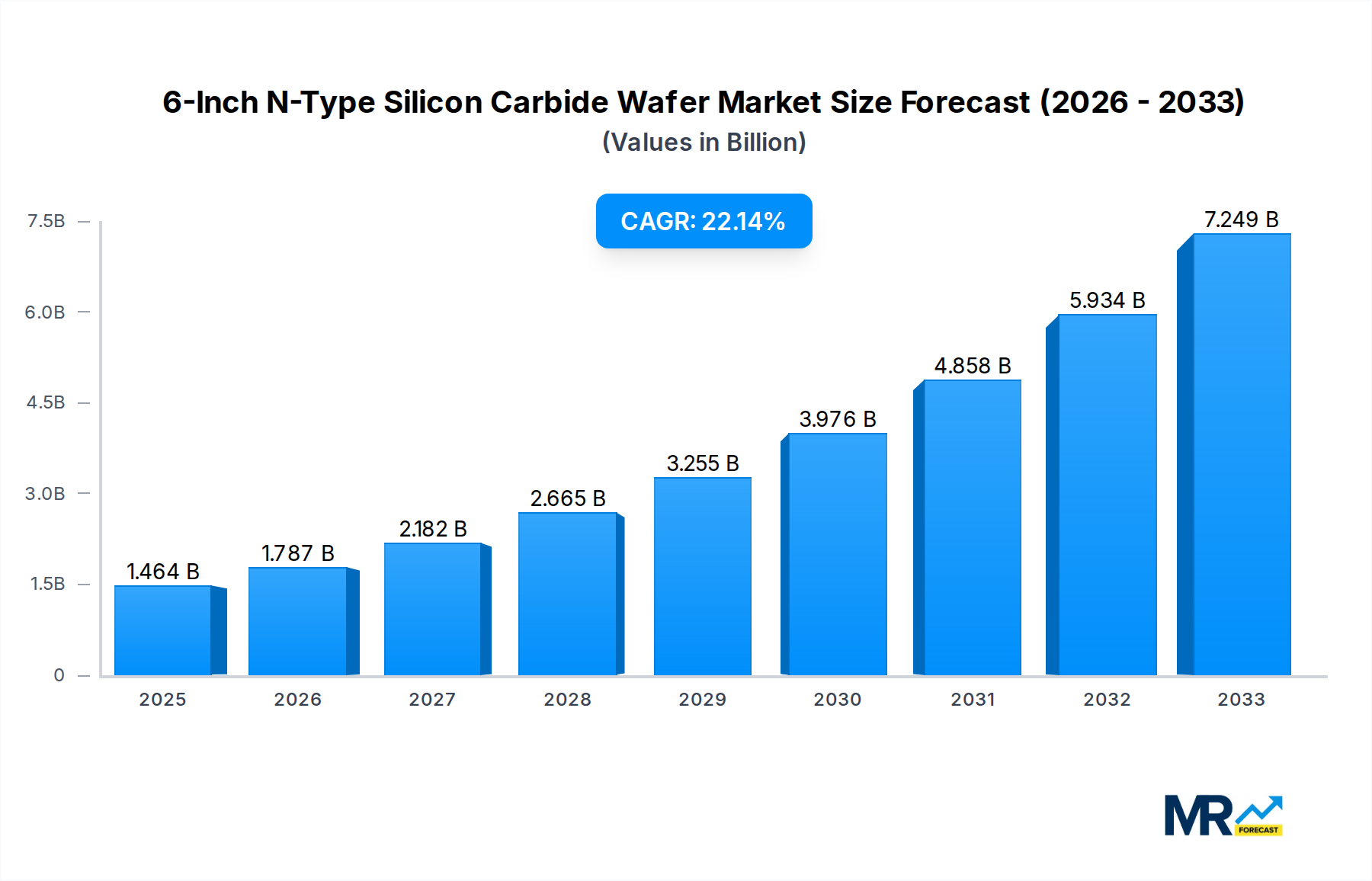

The 6-Inch N-Type Silicon Carbide (SiC) Wafer market is poised for exceptional growth, projected to reach an estimated $1579 million by 2025. This rapid expansion is fueled by a significant Compound Annual Growth Rate (CAGR) of 13.6% during the forecast period of 2025-2033. The burgeoning demand for higher efficiency and superior performance in power electronics, particularly for electric vehicles (EVs), renewable energy systems, and advanced consumer electronics, is a primary driver. SiC's inherent advantages over traditional silicon, such as higher breakdown voltage, lower switching losses, and better thermal conductivity, make it the material of choice for next-generation power devices. The shift towards higher voltage applications and the increasing adoption of SiC in wireless infrastructure for 5G deployment further bolster market prospects.

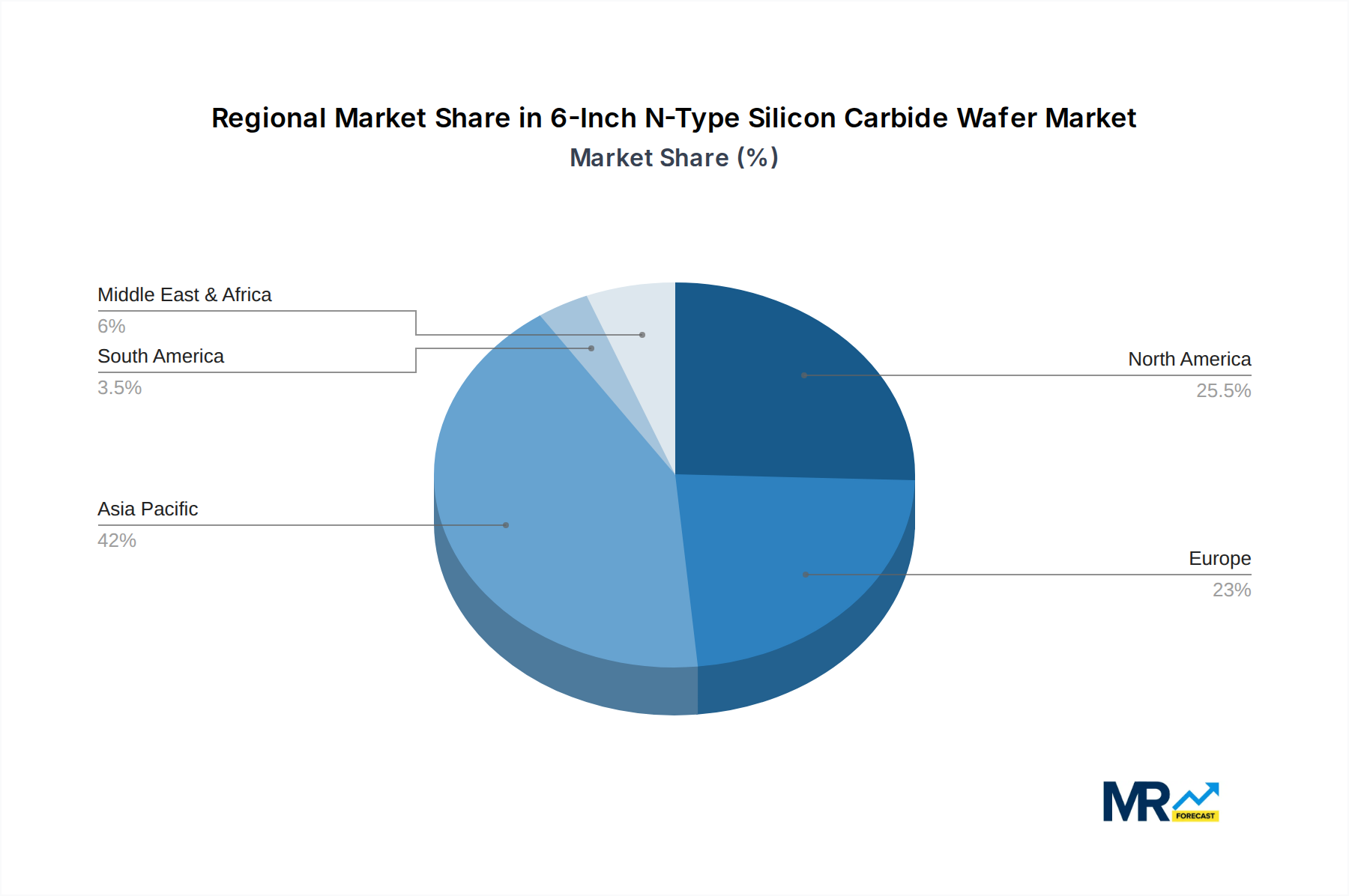

The market is segmented by wafer type, with Semi-Insulating SiC Wafers anticipated to witness stronger growth due to their critical role in high-frequency applications and power modules. Conductive SiC Wafers will also maintain steady demand, driven by their use in a broad spectrum of power devices. Geographically, Asia Pacific, led by China and Japan, is expected to dominate the market share, driven by robust manufacturing capabilities and extensive adoption in burgeoning sectors like EVs and renewable energy. North America and Europe are also significant markets, propelled by strong technological innovation and government initiatives promoting sustainable energy solutions. Key players like Wolfspeed, SK Siltron, and ROHM Group are actively investing in R&D and expanding production capacities to meet this escalating global demand, while emerging players are intensifying competition and driving innovation in wafer processing and quality.

Here is a unique report description for the 6-Inch N-Type Silicon Carbide Wafer market, incorporating your specified elements:

The global 6-Inch N-Type Silicon Carbide (SiC) wafer market is poised for an unprecedented surge, driven by a confluence of technological advancements and escalating demand across critical industries. From a historical perspective, the market has witnessed a steady but significant expansion during the 2019-2024 period, laying the groundwork for what is projected to be a transformative phase. The estimated market size in the base year of 2025 is expected to exceed a substantial value in the hundreds of millions of dollars, reflecting the growing adoption of SiC technology. This upward trajectory is not merely incremental; it signifies a fundamental shift in semiconductor material preference, particularly for high-performance applications. The study period, spanning from 2019 to 2033, underscores the long-term strategic importance of this market, with the forecast period of 2025-2033 anticipating exponential growth. A key insight into the trends reveals a pronounced shift towards higher purity and larger diameter wafers, with 6-inch N-type SiC wafers emerging as the dominant standard due to their optimal balance of performance, cost-effectiveness, and manufacturing scalability. The report will delve into the intricate interplay of supply chain dynamics, technological innovations in crystal growth and wafer processing, and the evolving regulatory landscape that collectively shapes these trends. Furthermore, the increasing integration of advanced packaging techniques and the continuous pursuit of reduced defect densities are pivotal factors influencing wafer quality and, consequently, market valuation. The report will meticulously analyze these granular details, presenting a comprehensive panorama of market dynamics that will undoubtedly influence strategic decision-making for stakeholders in the semiconductor ecosystem. The insights derived from the historical period will serve as a crucial benchmark for understanding the foundational growth, while projections for the forecast period will highlight the immense potential and the strategic imperatives for market participants to capitalize on the impending boom.

The relentless pursuit of higher energy efficiency and superior performance in electronic devices is the primary propellant behind the escalating demand for 6-inch N-type SiC wafers. As industries worldwide grapple with the imperative to reduce energy consumption and enhance the operational capabilities of their systems, SiC's inherent advantages over traditional silicon have become undeniable. Its ability to withstand higher temperatures, voltages, and frequencies translates directly into smaller, lighter, and more efficient power electronics. This is particularly critical in the burgeoning electric vehicle (EV) sector, where SiC power modules are revolutionizing onboard charging systems and inverters, leading to extended range and faster charging times. Beyond EVs, the proliferation of 5G infrastructure, data centers, and renewable energy systems, such as solar inverters and wind turbine converters, are significant beneficiaries of SiC technology. These applications demand robust and efficient power conversion, making 6-inch N-type SiC wafers an indispensable component. The intrinsic material properties of SiC, including its high thermal conductivity and breakdown electric field, enable devices to operate with significantly lower power losses compared to silicon counterparts. This translates into substantial cost savings in the long run, both in terms of energy expenditure and reduced cooling requirements, further solidifying its position as a material of choice for next-generation electronics.

Despite the overwhelmingly positive outlook, the 6-inch N-type Silicon Carbide wafer market is not without its hurdles. The primary challenge lies in the high cost of production associated with SiC wafers. The complex manufacturing process, involving high-temperature crystal growth (e.g., Physical Vapor Transport - PVT) and stringent wafer processing, is inherently more expensive than that for silicon. This elevated cost can be a significant barrier to widespread adoption, especially in cost-sensitive applications. Furthermore, the availability of raw materials and the complex supply chain can also present challenges. Sourcing high-quality silicon carbide powder and managing the intricate fabrication process requires specialized expertise and significant investment, which can lead to supply bottlenecks and price volatility. Another notable restraint is the technical complexity of device fabrication on SiC substrates. While SiC offers superior performance, designing and manufacturing devices that fully leverage its potential requires advanced semiconductor processing techniques and experienced engineering teams. This learning curve can slow down the adoption rate for some manufacturers. Lastly, competition from alternative materials and technologies also plays a role. While SiC currently holds a significant advantage in high-power applications, ongoing research and development in wide-bandgap materials and advanced silicon technologies could present future competitive pressures. The industry must continually innovate to maintain its lead and address these multifaceted challenges effectively to unlock the full market potential.

The global 6-Inch N-Type Silicon Carbide wafer market is characterized by a dynamic interplay of regional strengths and segment dominance, with certain areas and applications poised to lead the expansion.

Key Regions and Countries:

Asia Pacific (APAC): This region is emerging as a powerhouse in the SiC wafer market, driven by a confluence of factors including robust manufacturing capabilities, significant government support for semiconductor industries, and the presence of major consumer electronics and automotive manufacturers.

North America: The United States is a critical market for SiC wafers, driven by its leadership in the automotive industry (particularly EVs), advancements in renewable energy, and a strong defense and aerospace sector. Companies like Wolfspeed are global leaders in SiC technology, with significant manufacturing and R&D presence in the US. Government initiatives and substantial private sector investment in advanced manufacturing are further bolstering the market.

Europe: Europe is a significant consumer of SiC wafers, primarily due to its strong automotive industry, its commitment to renewable energy targets, and its growing focus on industrial automation. Germany, in particular, is a hub for SiC research and application development, with companies like Infineon Technologies (though not explicitly listed in your provided list, they are a major player in the broader SiC ecosystem) and STMicroelectronics with a growing presence in SiC.

Dominant Segment:

The synergy between advancements in 6-inch wafer technology, the increasing efficiency requirements of power conversion, and the rapid expansion of key end-use industries like automotive and renewable energy solidifies the Power Device segment as the cornerstone of the 6-inch N-Type SiC wafer market's current and future dominance.

Several key factors are acting as significant growth catalysts for the 6-inch N-type Silicon Carbide wafer industry. The insatiable demand from the electric vehicle (EV) sector for more efficient and compact power electronics is a primary driver. Furthermore, the global transition to renewable energy sources, requiring robust and high-performance power conversion systems, is significantly boosting adoption. Advancements in wafer manufacturing technologies, leading to improved quality, reduced defect densities, and increased yield, are making SiC more accessible and cost-competitive. Government incentives and supportive policies aimed at promoting advanced semiconductor manufacturing and clean energy technologies further accelerate market growth. The continuous innovation in device design, enabling higher power density and superior performance, also fuels the demand for high-quality SiC wafers.

This comprehensive report offers an in-depth analysis of the 6-inch N-type Silicon Carbide wafer market, encompassing a meticulous examination of market dynamics from the historical period of 2019-2024 through to robust projections for the forecast period of 2025-2033. The report meticulously details the current market landscape, with the base year of 2025 serving as a pivotal reference point, estimating market values in the hundreds of millions of dollars. It delves into the intricate trends, identifying the key drivers propelling the market forward, such as the insatiable demand from the electric vehicle sector and the global imperative for renewable energy solutions. The report also critically assesses the inherent challenges and restraints, including the high production costs and complex supply chains, offering strategic insights into overcoming these obstacles. Furthermore, it highlights the dominant regions and segments poised for significant growth, with a particular emphasis on the Power Device application and key geographical markets in Asia Pacific, North America, and Europe. The report also identifies crucial growth catalysts, such as technological advancements and supportive government policies. A comprehensive overview of the leading players and their strategic developments is also provided, offering a holistic understanding of the competitive landscape. This report is an indispensable resource for stakeholders seeking to navigate and capitalize on the burgeoning opportunities within the 6-inch N-type Silicon Carbide wafer market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.2% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.2%.

Key companies in the market include Wolfspeed, SK Siltron, ROHM Group (SiCrystal), Coherent, Resonac, STMicroelectronics, TankeBlue, SICC, Hebei Synlight Crystal, CETC, San'an Optoelectronics.

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in N/A and volume, measured in K.

Yes, the market keyword associated with the report is "6-Inch N-Type Silicon Carbide Wafer," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the 6-Inch N-Type Silicon Carbide Wafer, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.