1. What is the projected Compound Annual Growth Rate (CAGR) of the Wind Technology?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Wind Technology

Wind TechnologyWind Technology by Application (Maritime, Land), by Type (Hardware, Technology), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

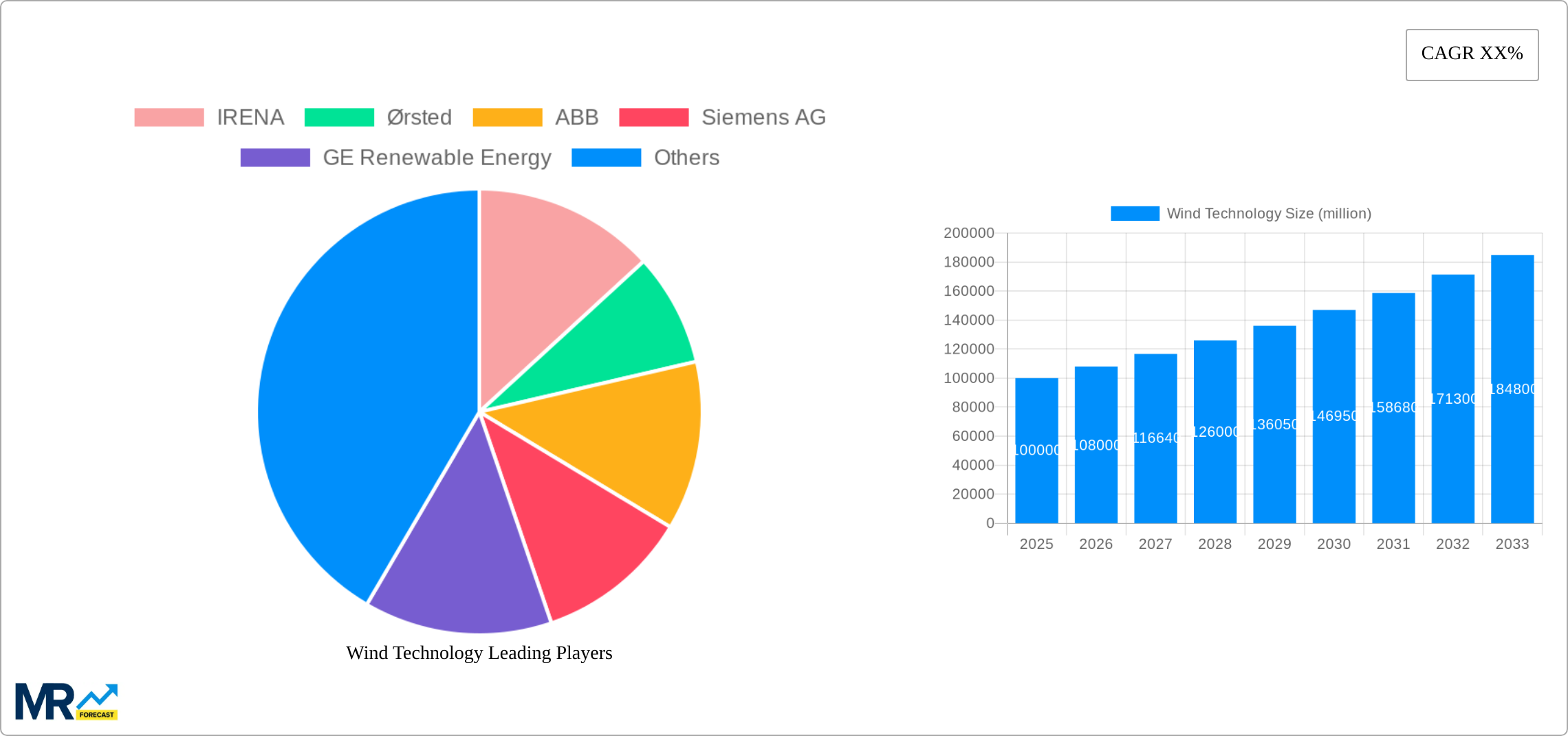

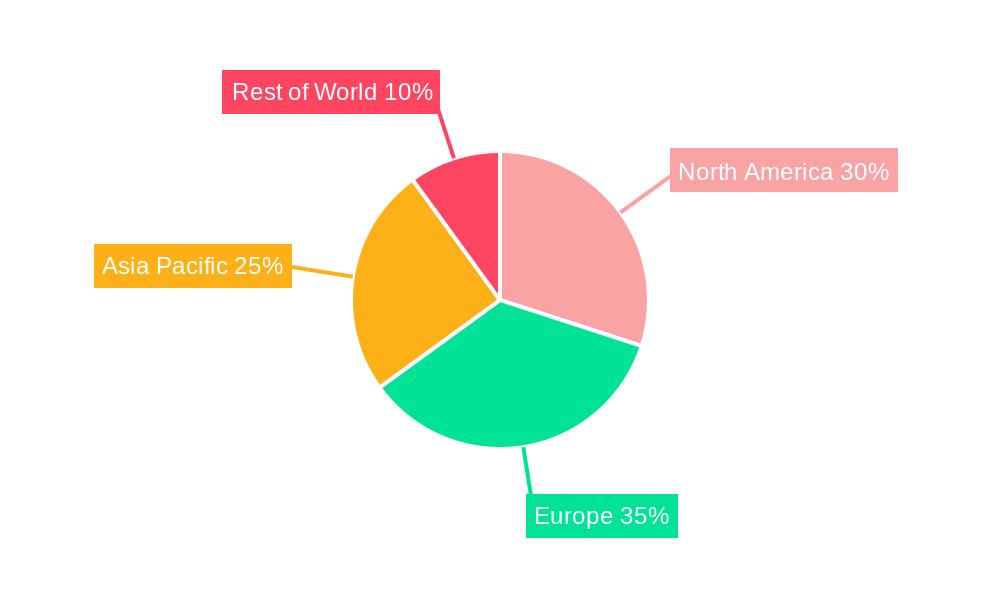

The global wind technology market is experiencing robust growth, driven by the increasing demand for renewable energy sources and supportive government policies aimed at mitigating climate change. The market, encompassing both onshore and offshore wind power generation, is segmented by application (maritime and land-based) and technology type (hardware and software solutions). While precise market size figures are unavailable, considering a plausible CAGR of 8% (a conservative estimate given industry trends) and assuming a 2025 market value of $100 billion, we can project substantial growth through 2033. Key drivers include falling technology costs, improved turbine efficiency, and expanding grid infrastructure accommodating renewable integration. Emerging trends such as floating offshore wind farms and advancements in energy storage solutions are further propelling market expansion. However, challenges remain, including the intermittent nature of wind power, the need for extensive grid upgrades in some regions, and potential environmental impacts requiring careful consideration. Major players like Vestas, Siemens Gamesa, and GE Renewable Energy are actively shaping the market through technological innovations and strategic partnerships. Geographical growth varies, with North America, Europe, and Asia-Pacific leading the charge, while regions in Africa and South America are showing increasing potential with targeted investments and supportive government initiatives.

The competitive landscape is characterized by a mix of established players and emerging companies vying for market share. Innovation is crucial for success, with companies focusing on developing more efficient and cost-effective turbines, improving maintenance strategies, and expanding into new geographical markets. The shift towards larger-scale offshore wind projects presents significant opportunities, necessitating substantial investments in specialized infrastructure and expertise. The integration of wind energy with other renewable sources, particularly solar power and energy storage, is also gaining momentum, leading to more robust and reliable power systems. Future market growth will depend on several factors, including government support through subsidies and tax incentives, technological advancements that drive down costs, and the successful integration of wind power into broader energy strategies. Addressing environmental concerns, ensuring responsible siting of wind farms, and establishing robust grid infrastructure will be vital for sustainable market expansion.

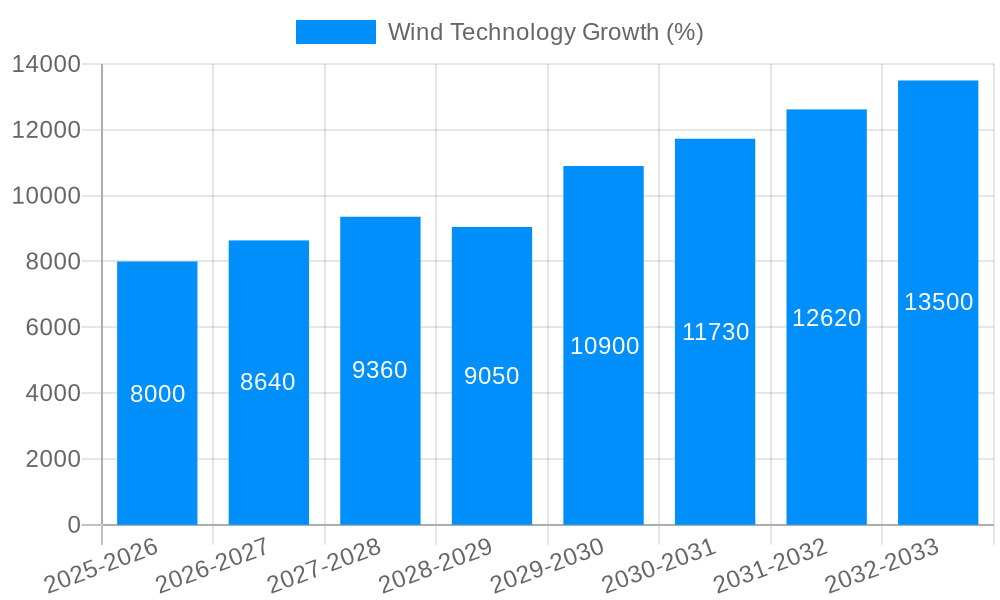

The global wind technology market is experiencing a period of unprecedented growth, driven by increasing concerns about climate change and the urgent need for renewable energy sources. The market, valued at XXX million in 2024, is projected to reach XXX million by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) during the forecast period (2025-2033). This expansion is fueled by several key factors, including supportive government policies and regulations promoting renewable energy adoption, decreasing technology costs, and advancements in turbine design leading to higher energy efficiency and capacity factors. The historical period (2019-2024) already showed significant expansion, paving the way for the projected boom. Key market insights reveal a strong preference for larger-scale onshore wind farms, coupled with a burgeoning offshore wind sector. The demand for advanced technologies like floating offshore wind platforms and improved energy storage solutions is also on the rise. Geographic diversification is another prominent trend, with several emerging markets showing significant investment in wind power infrastructure. This expansion is not limited to specific geographical locations; rather, it's a global phenomenon driven by the pressing need for cleaner energy sources. The increasing competitiveness among key players, driving down costs and fostering innovation, further contributes to the market's positive outlook. The shift towards larger turbine sizes signifies a trend towards higher capacity factors and reduced levelized cost of energy, making wind power increasingly competitive with traditional fossil fuel-based electricity generation. The market’s dynamism is also evident in the evolution of financing models, with increased participation from private equity and institutional investors. This diverse range of stakeholders reflects the growing confidence in the long-term viability and profitability of the wind energy sector. Finally, increasing corporate commitments to sustainability are driving significant corporate procurement of wind energy, further bolstering demand.

The surge in wind technology adoption is driven by a confluence of factors. Firstly, stringent government regulations and policies aimed at curbing greenhouse gas emissions and promoting renewable energy are providing significant impetus. Many countries have implemented renewable portfolio standards (RPS), carbon pricing mechanisms, and tax incentives to encourage the development of wind energy projects. Secondly, the continuous decline in the cost of wind turbine technology, particularly for onshore wind, has made it increasingly competitive with conventional energy sources. Advancements in turbine design, manufacturing efficiency, and economies of scale are responsible for this cost reduction. Thirdly, technological advancements are continually improving the efficiency and reliability of wind turbines. Innovations in blade design, control systems, and materials are leading to higher energy capture, reduced maintenance needs, and improved lifespan. Further, the increasing awareness of climate change and its potential impact is pushing individuals, businesses, and governments to embrace sustainable energy solutions. This growing societal concern contributes to a greater public acceptance and support for wind energy projects. Finally, the integration of wind energy into smart grids, alongside the development of advanced energy storage technologies, is resolving issues related to wind power's intermittency. This enhances the reliability and predictability of wind-generated electricity, bolstering its attractiveness as a mainstream power source. The interplay of these factors creates a powerful synergy that propels the sustained and rapid growth of the wind technology market.

Despite the significant growth, the wind technology sector faces several challenges. One major constraint is the intermittency of wind resources, making power generation unpredictable. This necessitates the development and integration of sophisticated energy storage solutions or grid management strategies to maintain a stable and reliable power supply. Furthermore, the environmental impact of wind farms, such as visual pollution and potential impacts on wildlife (e.g., birds and bats), requires careful consideration and mitigation strategies. Obtaining permits and approvals for wind farm projects can be a lengthy and complex process, involving multiple regulatory bodies and stakeholders, leading to project delays and increased costs. The geographic limitations of suitable wind resources also play a role. Not all locations are suitable for wind energy generation, limiting project siting options. Transmission infrastructure limitations can also hamper the integration of large-scale wind farms into existing grids. Finally, financing wind projects, particularly large-scale offshore wind farms, can require substantial capital investment and securing appropriate financing mechanisms. These financing challenges are often exacerbated by the long lead times associated with project development and construction. Addressing these challenges requires concerted efforts from governments, industry stakeholders, and researchers to develop innovative solutions that ensure the sustainable and responsible development of wind energy.

Segment: Onshore Wind (Hardware)

Key Regions: Europe (particularly Germany, Denmark, and the UK), North America (US and Canada), and China continue to dominate the onshore wind hardware market due to established infrastructure, supportive government policies, and substantial investment.

Market Dominance: The onshore wind hardware segment is projected to account for the lion's share of the market throughout the forecast period. The continuous cost reductions in turbine manufacturing, combined with the readily available land and established grid infrastructure in these regions, fuel this dominance. The growth in developing economies, while significant, is mainly focused on smaller projects and may not immediately surpass the established dominance of these mature markets. However, these developing economies will play an increasingly important role in future market growth.

Paragraph Explanation: The onshore wind sector, particularly concerning hardware components like turbines and associated infrastructure, maintains a commanding position due to its mature technology, lower capital expenditure compared to offshore solutions, and widespread accessibility. Established markets in Europe and North America benefit from pre-existing grid connections and well-defined regulatory frameworks, facilitating faster project deployment. China's significant manufacturing capacity and rapidly growing energy demands further consolidate its position as a key driver. While the offshore wind segment exhibits strong growth potential, the higher initial capital costs, complex installation processes, and specific site requirements present barriers to immediate market dominance. Thus, the onshore wind hardware segment is expected to remain the largest and most influential sector for the foreseeable future.

The wind technology industry's growth is fueled by several key catalysts. Decreasing technology costs make wind energy increasingly competitive with fossil fuels. Government policies and subsidies incentivize renewable energy adoption, further propelling market expansion. Technological advancements in turbine design and efficiency increase energy output and reduce the levelized cost of energy. The growing awareness of climate change and the need for decarbonization drives strong societal and corporate demand for clean energy solutions. The integration of smart grid technologies improves the reliability and predictability of wind power supply, making it a more attractive option for energy providers.

This report provides a comprehensive analysis of the wind technology market, encompassing historical data (2019-2024), current market estimations (2025), and future projections (2025-2033). The report offers valuable insights into market trends, driving forces, challenges, and growth catalysts. It covers key players, their market share, and significant developments in the sector. This in-depth analysis provides a detailed understanding of the wind technology market landscape, enabling strategic decision-making for investors, businesses, and policymakers.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include IRENA, Ørsted, ABB, Siemens AG, GE Renewable Energy, Mitsubishi Heavy Industries, RWE Renewables, NextEra Energy Resources, Vestas, Avangrid, EDP Renewables North America LLC, Renewable Energy Systems Americas, Suzlon, .

The market segments include Application, Type.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Wind Technology," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Wind Technology, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.