1. What is the projected Compound Annual Growth Rate (CAGR) of the Uranium Mining?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Uranium Mining

Uranium MiningUranium Mining by Type (Granite-Type Uranium Deposits, Volcanic-Type Uranium Deposits, Sandstone-Type Uranium Deposits, Carbonate-Siliceous-Pelitic Rock Type Uranium Deposits, World Uranium Mining Production ), by Application (Military, Electricity, Medical, Industrial, Others, World Uranium Mining Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

The global uranium mining market is experiencing moderate growth, driven primarily by the increasing demand for nuclear energy as a low-carbon alternative to fossil fuels. While concerns about nuclear waste disposal and safety remain, the urgency to mitigate climate change is fueling renewed interest in nuclear power, consequently boosting uranium demand. The market is segmented by deposit type (granite, volcanic, sandstone, carbonate-siliceous-pelitic), with sandstone-type deposits currently dominating global production. Application-wise, the electricity sector consumes the largest share of uranium, followed by military applications. Key players in the market include established multinational mining companies like Cameco, Kazatomprom, and Orano (formerly Areva), alongside significant state-owned enterprises in countries like China and Russia. Geopolitically, the market is concentrated, with Kazakhstan and Canada being major producers. However, exploration and development activities are expanding in other regions, including Australia and Africa, aiming to diversify supply chains and reduce reliance on a few key players. Challenges include fluctuating uranium prices influenced by global energy markets and regulatory hurdles related to environmental protection and nuclear security. The long-term outlook for the uranium mining market is positive, albeit with inherent volatility, reflecting the inherent complexity of the energy transition and the ongoing debate surrounding nuclear power's role.

The forecast period (2025-2033) anticipates a steady increase in uranium production, largely driven by the expansion of existing mines and the commissioning of new projects. Technological advancements, including improved exploration techniques and more efficient mining methods, are expected to enhance profitability and sustainability. However, the market will continue to be affected by factors such as geopolitical instability, fluctuating energy prices, and the regulatory landscape governing nuclear power development. Competitive dynamics will remain intense, with established players consolidating their positions and new entrants seeking to capitalize on growth opportunities. The market's growth trajectory will depend significantly on government policies supporting nuclear energy and ongoing innovation in nuclear reactor technology, particularly in areas like small modular reactors (SMRs), which could potentially drive a significant increase in uranium demand in the long term.

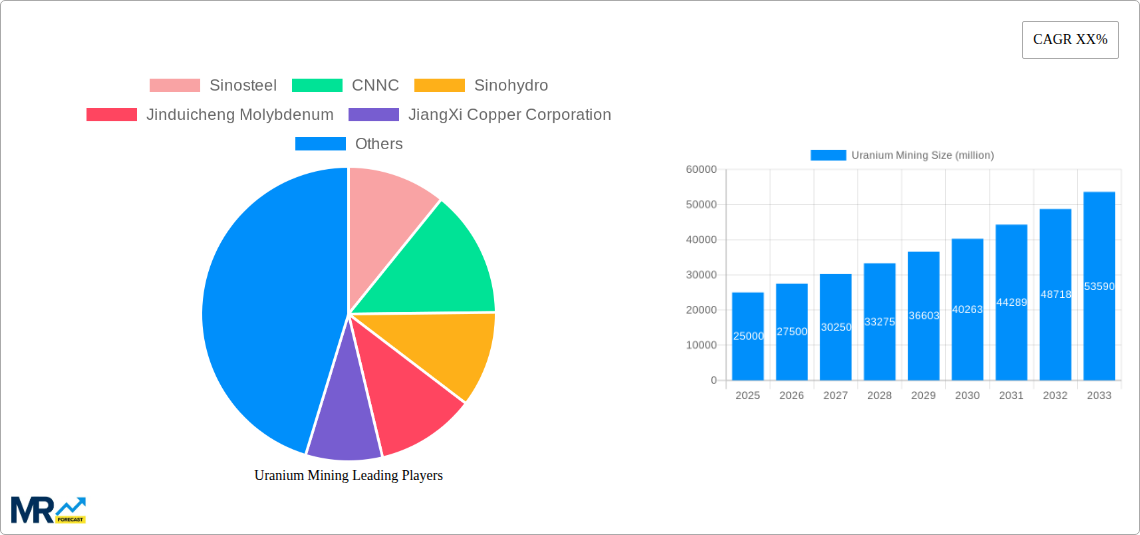

The global uranium mining industry experienced a period of fluctuating growth between 2019 and 2024, influenced by diverse geopolitical factors and evolving energy demands. Production levels, while showing some year-on-year increases in certain periods, did not achieve consistent, high growth. The historical period (2019-2024) revealed a complex interplay between established players like Cameco and Kazatomprom, and emerging entities seeking a foothold in the market. The base year of 2025 shows a stabilization and slight uptick in production, driven by increasing nuclear power plant construction globally. Estimates for 2025 indicate a production level exceeding 60 million kilograms of uranium, a figure projected to climb significantly by 2033, potentially reaching or exceeding 90 million kilograms. This growth is largely fueled by the predicted rise in demand for nuclear energy as countries seek carbon-neutral energy sources. The forecast period (2025-2033) presents a dynamic landscape where technological advancements, coupled with governmental policies encouraging nuclear power, could significantly impact production volumes and market shares of major players. The market is further characterized by ongoing consolidation, with larger companies acquiring smaller ones to strengthen their market position. Pricing also exhibits volatility, responding to global energy market fluctuations and the ongoing geopolitical uncertainties impacting the nuclear energy sector. The study period (2019-2033) showcases a trend of increased diversification of uranium sources, with exploration efforts extending to new regions and geological formations.

Several key factors are driving the growth of the uranium mining industry. The most significant is the rising global demand for nuclear energy as countries seek to diversify their energy portfolios and reduce reliance on fossil fuels. Nuclear power offers a carbon-free electricity generation alternative, aligning with climate change mitigation goals. Increased investments in nuclear power plant construction, particularly in Asia and parts of Europe, directly translate into a heightened demand for uranium. Governmental policies promoting nuclear energy, through subsidies, tax breaks, and streamlined permitting processes, are also providing crucial support. Additionally, technological advancements in uranium extraction and processing are making the mining process more efficient and cost-effective, boosting production capacity. Lastly, the strategic importance of uranium in national security and defense applications ensures a consistent level of demand, irrespective of fluctuations in civilian energy production. The overall increase in global energy consumption and the commitment of numerous nations to achieve carbon neutrality by 2050 contributes significantly to the positive growth outlook for the uranium mining sector.

Despite the positive growth trajectory, several challenges constrain the uranium mining industry. Firstly, the inherent environmental risks associated with uranium mining, including radioactive waste disposal and potential land degradation, necessitates rigorous environmental regulations and monitoring, increasing operational costs. Secondly, price volatility, influenced by global energy markets, geopolitical factors, and speculative trading, creates uncertainty for miners, impacting investment decisions and long-term project viability. Thirdly, the lengthy permitting and regulatory processes for new uranium mines, often spanning several years, can delay project development and hamper timely production increases. Fourthly, access to funding for exploration and development of new uranium projects can be challenging, especially for smaller companies, as investors often demonstrate risk aversion in this sector. Finally, the concentration of uranium production in a few key regions presents both opportunities and challenges; political instability or regulatory changes in these regions can significantly disrupt global supply chains and trigger price fluctuations.

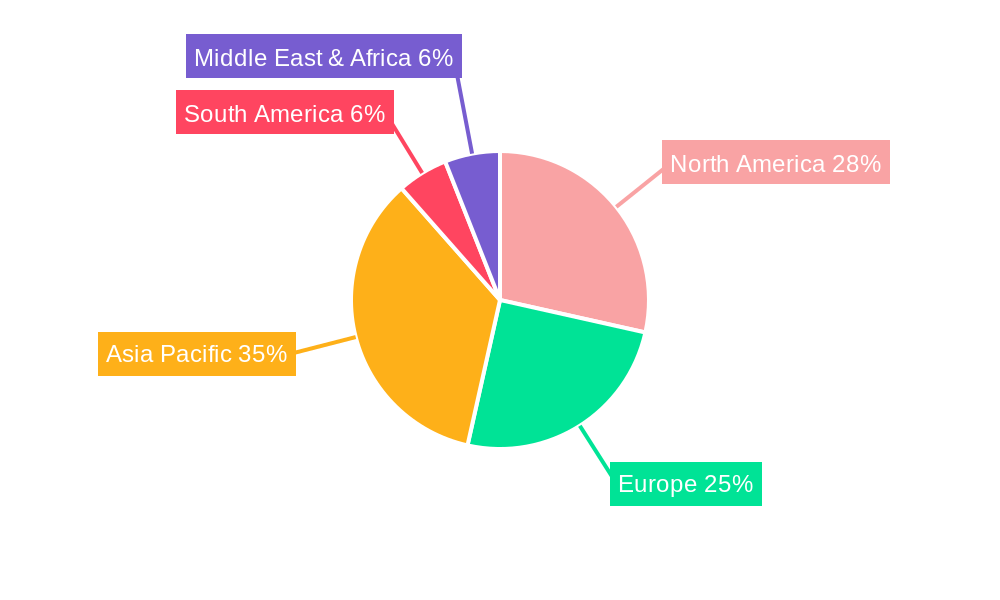

The global uranium market exhibits regional concentration, with several key players dominating. Kazakhstan, through Kazatomprom, maintains a leading position in global uranium production, boasting extensive reserves and well-established infrastructure. Other significant producing countries include Canada (Cameco), Australia (Paladin), and Namibia. These countries benefit from considerable reserves, supportive government policies, and established mining expertise.

In terms of uranium deposit types, Sandstone-Type Uranium Deposits currently represent a significant portion of global production due to their established infrastructure and extensive historical exploration and development. However, exploration for and development of other deposit types such as Granite-Type and Volcanic-Type deposits is likely to contribute to production growth in the coming years. The Electricity segment is the leading application of uranium, consuming the vast majority of global production, driven by the increasing demand for nuclear energy. While the Military and Medical sectors contribute to uranium demand, their volumes pale in comparison to the electricity sector's contribution.

The uranium mining industry's growth is catalyzed by a confluence of factors: the increasing global demand for nuclear energy as a low-carbon alternative, technological advancements increasing extraction efficiency and reducing costs, supportive government policies promoting nuclear power, and the stable and consistent demand from the military and medical sectors. These factors together create a positive growth outlook for the industry.

This report offers a detailed analysis of the uranium mining industry, encompassing historical data, current market dynamics, and future projections. It examines key driving forces, challenges, and growth catalysts, focusing on market trends and regional dominance. The report also provides in-depth profiles of leading players and key developments within the sector. The comprehensive nature of this report makes it a valuable resource for investors, industry professionals, and policymakers alike.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Sinosteel, CNNC, Sinohydro, Jinduicheng Molybdenum, JiangXi Copper Corporation, Cameco, Areva, BHP Billiton, Kazatomprom, APM3, ERA, AtomRedMetZoloto(ARMZ), Paladin, Navoi, Rio Tinto Group.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Uranium Mining," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Uranium Mining, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.