1. What is the projected Compound Annual Growth Rate (CAGR) of the Uranium Mine?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Uranium Mine

Uranium MineUranium Mine by Type (In Situ Leach Mining (ISL), Open-pit Mining, Underground Mining, By-product), by Application (Nuclear Power Generation, Military Weapons, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

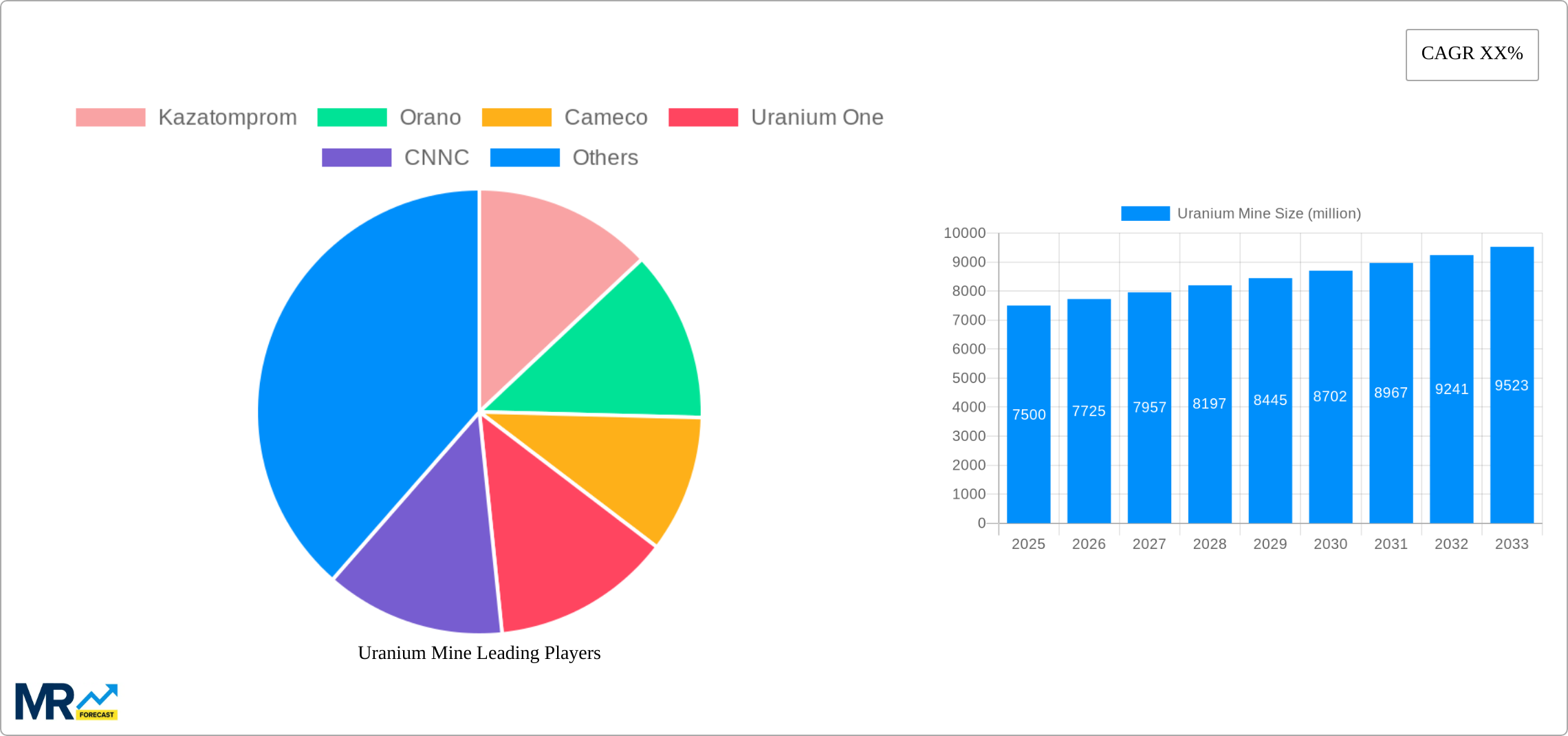

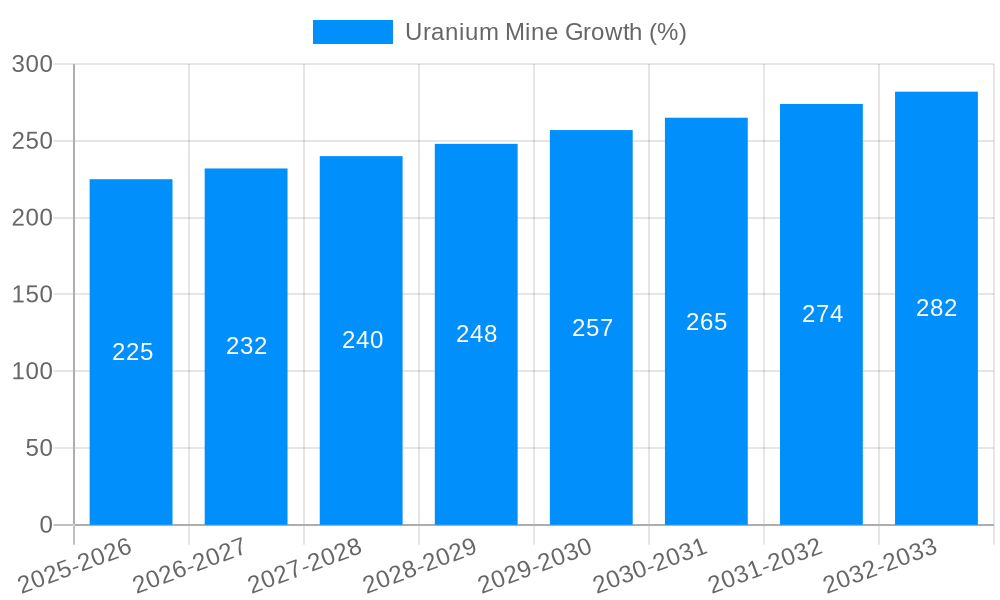

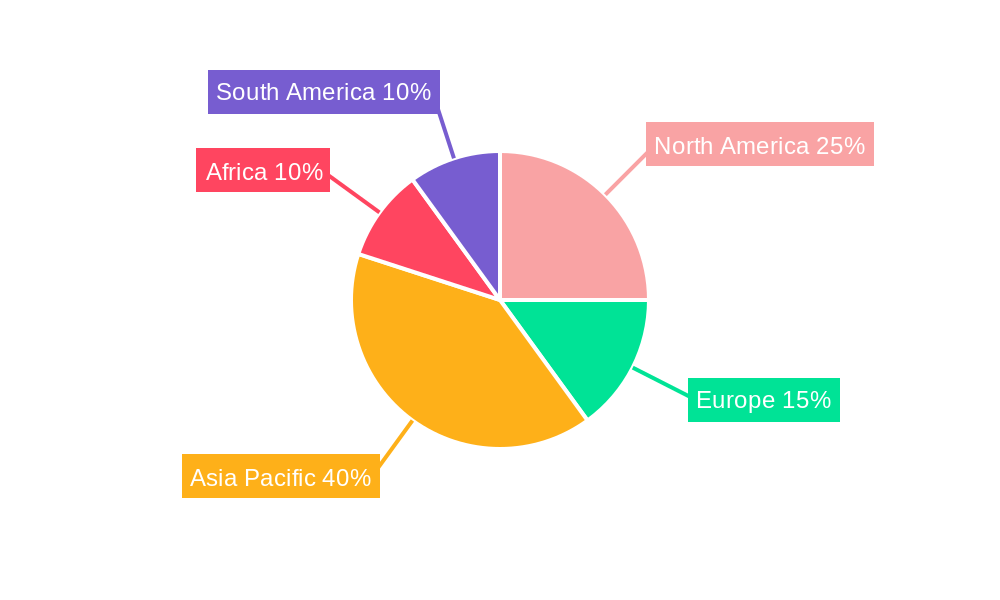

The global uranium mining market is experiencing a period of growth fueled by increasing demand from nuclear power generation, a sector witnessing a resurgence amidst concerns about climate change and energy security. While the historical period (2019-2024) may have seen fluctuations due to various factors including policy changes and market volatility, the forecast period (2025-2033) projects a positive trajectory. Let's assume a conservative Compound Annual Growth Rate (CAGR) of 3% for illustrative purposes. This growth is underpinned by several key drivers: the expansion of existing nuclear power plants, the construction of new reactors globally (particularly in Asia), and the increasing recognition of uranium's role as a low-carbon energy source. Technological advancements in mining techniques, like In Situ Leach Mining (ISL), are also contributing to efficiency gains and cost reductions. However, the market faces challenges. Environmental regulations are becoming stricter, leading to increased operational costs and permitting complexities. Fluctuations in uranium prices due to geopolitical factors and the availability of alternative energy sources remain a significant restraint. Segment-wise, nuclear power generation currently dominates application, with significant growth opportunities anticipated in this sector. Major players like Kazatomprom, Cameco, and Orano are strategically positioned to capitalize on this expanding market, while smaller companies focus on niche applications or specific geographic regions. The regional distribution of uranium mining activity is geographically concentrated, with North America, Asia-Pacific (particularly China and Kazakhstan) and parts of Africa and Europe holding significant market share.

The competitive landscape is characterized by a mix of state-owned enterprises and privately held companies. While some companies focus on diversified mining portfolios, others specialize exclusively in uranium production, creating a dynamic market interplay of vertical integration and specialization. Future market performance hinges on several factors: the pace of nuclear power plant construction, the price stability of uranium, the efficacy of environmental regulations, and successful innovation in resource extraction technologies. Successful companies will need to demonstrate a keen understanding of geopolitical risk, stringent environmental compliance, and sustainable operational practices to maintain profitability and capture market share throughout the forecast period. Continued growth in the nuclear sector is paramount for sustaining the overall growth of the uranium mining market.

The global uranium mining industry is poised for significant growth over the forecast period (2025-2033), driven by a resurgence in nuclear power generation and increasing demand from various sectors. The historical period (2019-2024) witnessed fluctuating uranium prices and production levels, impacted by factors such as the Fukushima disaster, shifting government policies, and the competition from renewable energy sources. However, the base year (2025) marks a turning point, with projections indicating a steady rise in uranium demand, primarily fueled by the expansion of nuclear power plants globally, particularly in Asia. This report, covering the study period of 2019-2033, analyzes the market dynamics and forecasts future trends. The estimated year 2025 reveals a market valued at several billion dollars, reflecting a significant increase from the previous years. This growth is not uniform across all segments, with some regions and mining methods experiencing faster expansion than others. The increasing focus on energy security and the role of nuclear power as a reliable, low-carbon energy source are key factors shaping the industry's trajectory. The competition among major players like Kazatomprom, Cameco, and Orano will continue to intensify as they strive to capture a larger market share in this expanding sector. Technological advancements in uranium extraction, particularly in situ leach (ISL) mining, contribute to higher efficiency and lower operational costs, further fueling the market's growth. The industry is also navigating environmental concerns and regulatory changes, requiring companies to adopt sustainable and responsible mining practices. The overall trend signifies a period of growth and transformation for the uranium mining industry, with opportunities for innovation and expansion. Market estimates indicate a potential market value exceeding tens of billions of dollars by 2033, signifying a significant upward trajectory.

Several factors are propelling the growth of the uranium mining industry. Firstly, the rising global demand for reliable and low-carbon energy sources is driving increased investment in nuclear power plants. Many countries, particularly in Asia, are expanding their nuclear power capacity, leading to a surge in uranium demand. Secondly, geopolitical uncertainties and the need for energy independence are making nuclear power a more attractive option for several nations. This factor contributes to the long-term stability and growth of the uranium market. Technological advancements in uranium extraction techniques, such as ISL mining, have improved efficiency and reduced costs, making uranium production more economically viable. Improved safety regulations and stricter environmental standards, although presenting challenges, also build trust in nuclear power and thereby influence uranium demand positively. Lastly, the growing use of uranium in various non-energy applications, such as medical isotopes and industrial uses, is contributing to the overall demand, albeit at a smaller scale compared to nuclear power generation. These combined factors create a robust and growing market for uranium mining, suggesting continued expansion throughout the forecast period.

Despite the positive growth projections, the uranium mining industry faces several challenges and restraints. Fluctuating uranium prices remain a significant concern, impacting profitability and investment decisions. Price volatility is influenced by factors such as global political events, changes in government policies regarding nuclear energy, and competition from renewable energy sources. Environmental regulations and concerns about the environmental impact of uranium mining, particularly radioactive waste management, impose significant costs and operational complexities on mining companies. Securing permits and licenses for uranium mining operations can be a lengthy and challenging process, adding to the overall investment risk. The long lead times required for building nuclear power plants create uncertainties in the long-term demand projections for uranium. Furthermore, the industry is subject to geopolitical risks and potential disruptions caused by international relations and political instability in regions where uranium is mined. Finally, competition from alternative energy sources like solar and wind power continues to exert pressure on the uranium market, demanding innovation and adaptation within the industry.

The uranium mining market is characterized by geographical concentration and specific segment dominance.

Key Regions: Kazakhstan, Canada, Australia, and Namibia are among the leading uranium-producing countries and are expected to maintain their dominance throughout the forecast period. These countries possess substantial uranium reserves and established mining infrastructure. Asia, particularly China and India, are major consumers of uranium due to their expanding nuclear power programs and contribute significantly to the growth of the market.

Dominant Segment: Nuclear Power Generation. This segment accounts for the vast majority of uranium demand globally, making it the key driver of market growth. The increasing reliance on nuclear power as a clean energy source continues to fuel this sector's demand.

Mining Methods: In Situ Leach (ISL) mining is gaining traction due to its lower environmental impact and reduced costs compared to open-pit and underground mining methods. However, open-pit and underground mining will remain significant in certain geological contexts.

Paragraph Summary: Kazakhstan, with its substantial reserves and established mining industry, including companies like Kazatomprom, is likely to retain its position as the leading uranium producer. Canada (Cameco), Australia, and Namibia also play crucial roles in supplying the global market. The unwavering dominance of the nuclear power generation segment, fueled by the expanding nuclear energy sector in Asia and elsewhere, reinforces the importance of these key regions in the global uranium landscape. While ISL mining is growing, traditional methods remain essential given the varying geological characteristics of uranium deposits worldwide. The interplay between geographic distribution of resources, mining technologies, and global nuclear energy demand shapes the market dynamics and forecasts over the next decade.

Several factors will act as growth catalysts for the uranium mining industry over the forecast period. A renewed focus on nuclear energy as a low-carbon alternative to fossil fuels, coupled with rising energy demand and concerns over energy security, will drive investment in nuclear power plants, fueling demand for uranium. Advances in uranium extraction technologies, particularly ISL mining, lead to increased efficiency and reduced environmental impact, making mining more economically attractive and sustainable. Government support for nuclear power in several countries, including policies promoting nuclear energy as a clean energy source, will positively influence uranium demand. Finally, the increasing use of uranium in medical and industrial applications, although a smaller contributor compared to nuclear power, adds further impetus to market growth.

This report provides a comprehensive analysis of the uranium mine market, encompassing historical data, current market trends, and detailed future projections. It offers insights into key market drivers, challenges, and opportunities, enabling stakeholders to make informed decisions and navigate the evolving landscape of the uranium mining industry. The report covers major players, regional trends, technological advancements, and regulatory changes, delivering a holistic perspective on the future of uranium mining.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Kazatomprom, Orano, Cameco, Uranium One, CNNC, CGN, Navoi Mining, BHP Billiton, ARMZ Uranium Holding, General Atomics/Quasar, Sopamin, Rio Tinto, VostGok, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million and volume, measured in K.

Yes, the market keyword associated with the report is "Uranium Mine," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Uranium Mine, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.