1. What is the projected Compound Annual Growth Rate (CAGR) of the Third Party & Supplier Risk Management Software?

The projected CAGR is approximately 18.5%.

Third Party & Supplier Risk Management Software

Third Party & Supplier Risk Management SoftwareThird Party & Supplier Risk Management Software by Type (Cloud Based, Web Based), by Application (Large Enterprises, SMEs), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

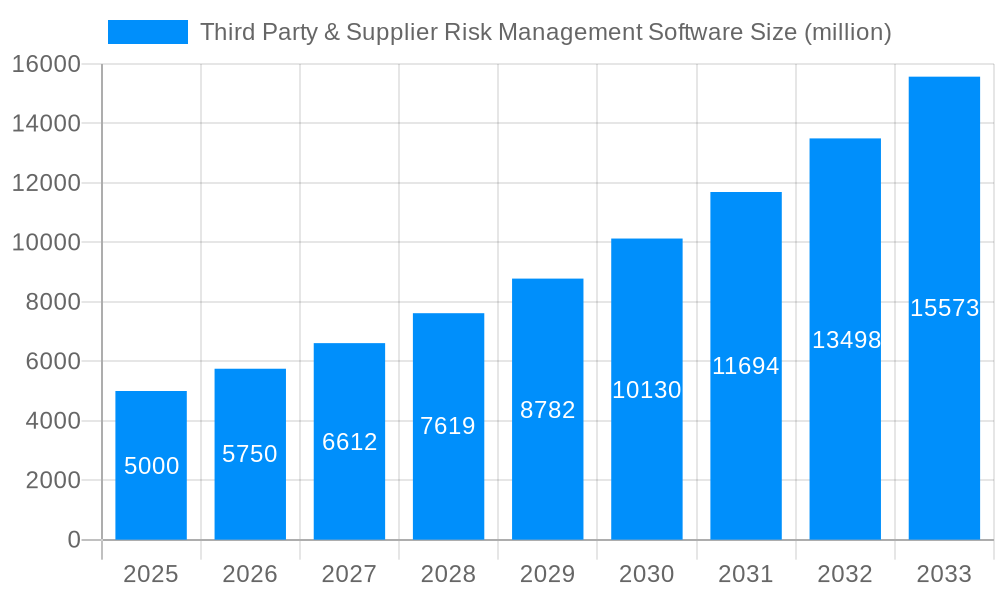

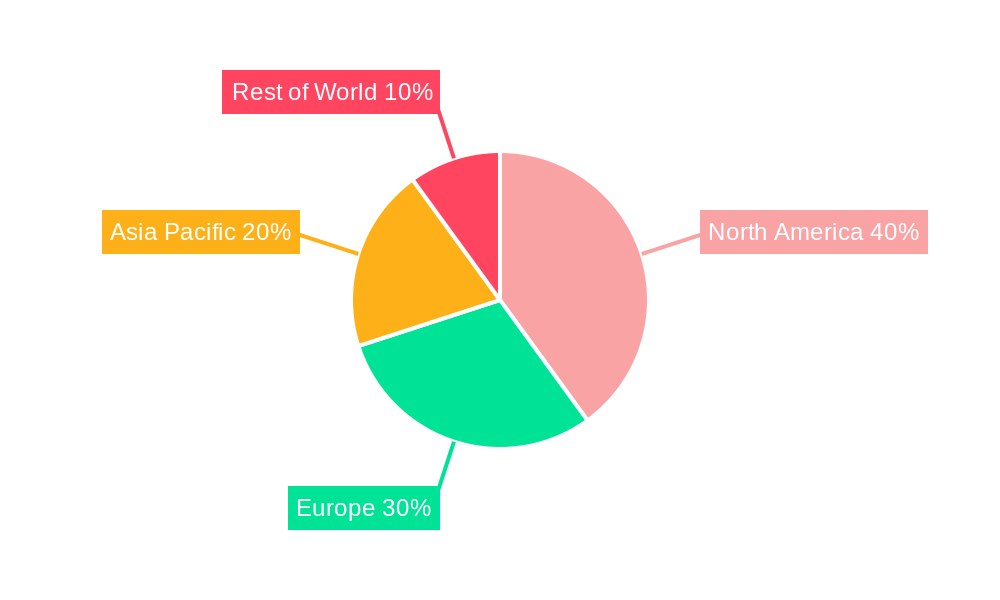

The Third-Party & Supplier Risk Management Software market is experiencing robust growth, driven by increasing regulatory scrutiny, globalization of supply chains, and the rising adoption of digital technologies. The market, currently estimated at $5 billion in 2025, is projected to achieve a Compound Annual Growth Rate (CAGR) of 15% from 2025 to 2033, reaching approximately $15 billion by 2033. This expansion is fueled by several key factors. Firstly, businesses are increasingly aware of the financial and reputational risks associated with inadequate third-party vendor management. Data breaches, supply chain disruptions, and ethical lapses are major concerns, prompting organizations to invest heavily in robust risk mitigation strategies. Secondly, stringent compliance regulations across various industries, like GDPR, CCPA, and industry-specific standards, mandate effective third-party risk management programs. This regulatory pressure acts as a significant driver for software adoption. Finally, the increasing sophistication of these software solutions, encompassing functionalities such as automated risk assessments, continuous monitoring, and integrated reporting, enhances efficiency and reduces manual effort, further driving market growth. The cloud-based segment dominates the market, owing to its scalability, accessibility, and cost-effectiveness. Large enterprises represent the largest customer segment, but the SME sector is rapidly adopting these solutions due to their enhanced affordability and ease of implementation. Geographic growth is uneven, with North America and Europe currently holding the largest market shares, however, the Asia-Pacific region is expected to witness significant growth in the coming years due to increasing digitization and expanding business operations.

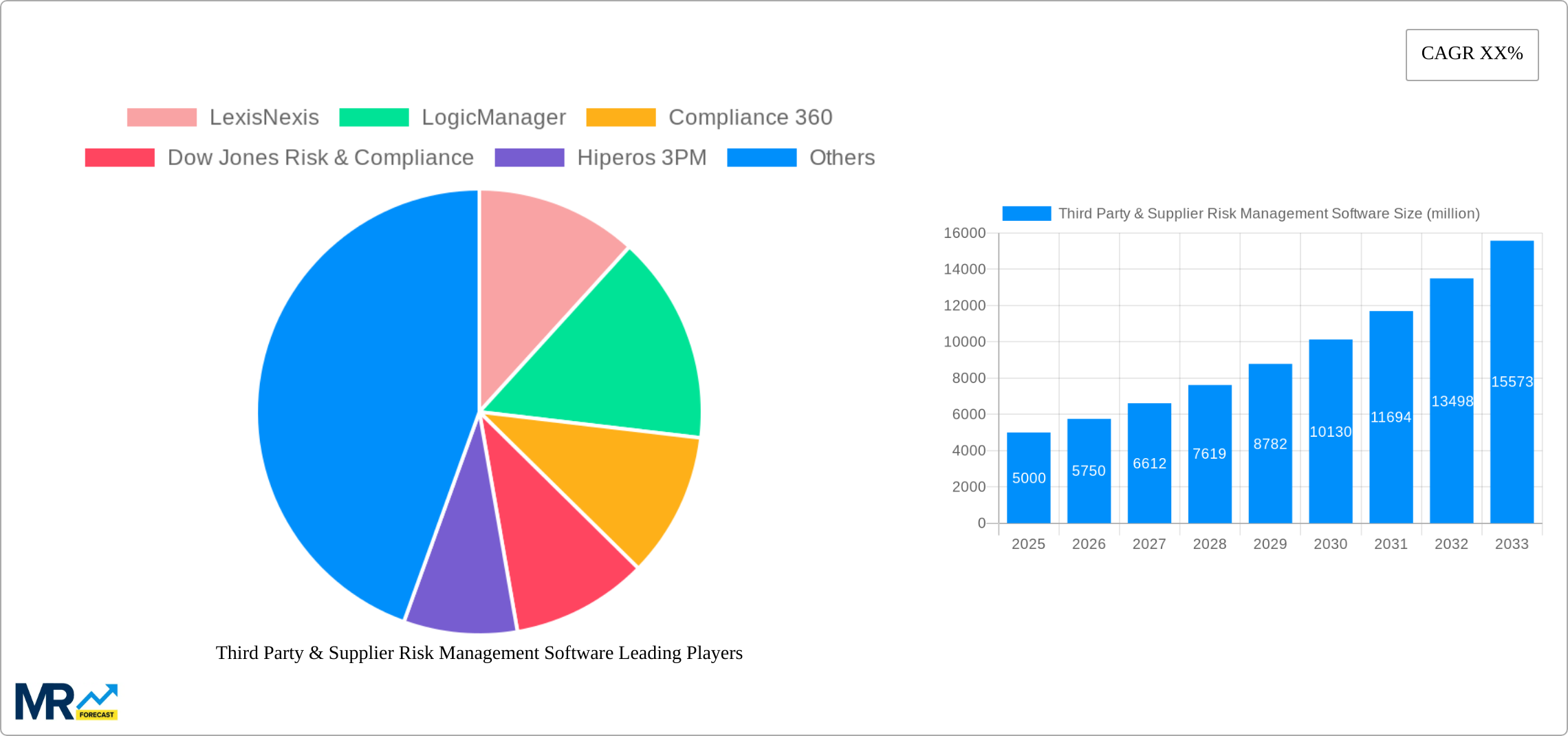

The competitive landscape is characterized by a mix of established players like LexisNexis and SAP, alongside emerging specialized vendors such as LogicManager and Resolver. Market consolidation and strategic partnerships are likely to shape the future. Key challenges include the need for continuous software updates to address evolving threats and regulatory changes, and the integration complexities with existing enterprise systems. Despite these challenges, the long-term outlook for the Third-Party & Supplier Risk Management Software market remains extremely positive, driven by the persistent need for businesses to effectively manage and mitigate the risks associated with their extended enterprise. This growth is projected to be propelled by ongoing digital transformation across industries and ever-increasing regulatory mandates worldwide.

The global third-party and supplier risk management software market is experiencing robust growth, projected to reach multi-billion dollar valuations by 2033. The period from 2019 to 2024 (historical period) laid the groundwork for this expansion, witnessing increasing adoption driven by stringent regulatory compliance requirements and a growing awareness of the potential financial and reputational damage stemming from inadequate third-party risk management. The estimated market value in 2025 (base year and estimated year) reflects this momentum. The forecast period (2025-2033) anticipates continued growth fueled by several factors, including the increasing complexity of global supply chains, the rise of digital transformation initiatives, and the escalating frequency and severity of cyber threats. Companies are recognizing the critical need for sophisticated software solutions to effectively manage the risks associated with their third-party ecosystem. This need is particularly acute in regulated industries like finance and healthcare, where non-compliance can lead to significant penalties. The market is dynamic, with ongoing innovation in areas such as artificial intelligence (AI) and machine learning (ML) enhancing the capabilities of these software solutions. This translates to improved risk assessment, automated monitoring, and more efficient remediation processes, all contributing to a stronger overall risk posture for organizations. The shift towards cloud-based solutions is also a prominent trend, offering scalability, accessibility, and cost-effectiveness compared to on-premise deployments. This is further amplified by the rising adoption of these solutions among SMEs, which are increasingly recognizing the importance of robust risk management strategies, even with limited resources. The competitive landscape is characterized by both established players and emerging innovative companies, resulting in a diverse range of solutions catering to specific industry needs and organizational sizes. This competitive pressure fuels innovation and keeps the market vibrant. The overall trend indicates a clear and sustained upward trajectory for the third-party and supplier risk management software market in the coming years.

Several powerful forces are driving the rapid expansion of the third-party and supplier risk management software market. Firstly, increasingly stringent regulatory compliance mandates across various industries are compelling organizations to adopt robust risk management frameworks. Failure to comply can result in hefty fines and reputational damage. Secondly, the growing complexity and globalization of supply chains introduce significant challenges in managing risk effectively. Organizations need comprehensive visibility into their entire network of suppliers to identify and mitigate potential vulnerabilities. Thirdly, the pervasive threat of cyberattacks and data breaches makes securing the third-party ecosystem a critical priority. Software solutions provide the necessary tools for continuous monitoring and threat detection. Fourthly, a shift towards proactive risk management is gaining traction. Organizations are moving beyond reactive measures towards predictive analytics and AI-powered risk assessment, enabling them to anticipate and address potential risks before they materialize. Fifthly, the rising adoption of cloud-based solutions offers organizations scalable, cost-effective, and accessible risk management capabilities. Finally, the increasing awareness of the financial and reputational consequences associated with third-party failures is motivating many companies to invest in advanced software solutions to minimize risk. This convergence of factors is creating a powerful surge in demand for effective third-party and supplier risk management software, driving market growth.

Despite the significant growth potential, several challenges and restraints hinder the widespread adoption of third-party and supplier risk management software. One major challenge is the initial investment cost, which can be substantial for some organizations, particularly SMEs. Implementing and maintaining these systems requires upfront investment in software licenses, infrastructure, and employee training. Another challenge is the complexity of integrating these solutions with existing organizational systems and workflows. Successful implementation necessitates careful planning and execution to avoid disruptions and data inconsistencies. Furthermore, the lack of standardization in risk assessment methodologies and data formats creates interoperability issues and hampers seamless data exchange across different organizations and systems. Data security and privacy concerns are another critical hurdle. Protecting sensitive data associated with third-party relationships is paramount, and organizations must ensure their chosen software complies with relevant regulations and best practices. Finally, resistance to change within organizations can hamper the effective adoption and utilization of new software solutions. Proper change management strategies are crucial to ensure user buy-in and successful implementation. These challenges require addressing to fully unlock the market’s potential for growth.

The North American market is projected to maintain its dominance in the third-party and supplier risk management software market throughout the forecast period (2025-2033). This is primarily driven by the region's robust regulatory environment, high concentration of large enterprises, and significant investments in digital transformation initiatives. Within the segment breakdown, Cloud-based solutions are expected to capture a substantial market share. The advantages of scalability, accessibility, and cost-effectiveness compared to web-based or on-premise solutions make them highly attractive to both large enterprises and SMEs.

Large enterprises are a key driver of growth due to their higher investment capacity and complex supply chains, necessitating sophisticated risk management solutions. However, the SME segment is also witnessing significant growth, fueled by increasing regulatory scrutiny and awareness of the financial and reputational consequences of inadequate risk management practices. The cloud-based segment offers accessibility and cost-effectiveness appealing to this segment. The increasing adoption of these solutions by SMEs is a particularly strong trend, signifying a broadening of the market's reach. This segment growth is expected to continue at a faster rate than the large enterprises segment throughout the forecast period. The market maturity and adoption levels are also significantly different between these two segments. Large Enterprises have already adopted these systems to varying degrees in the past years. However, the growth in the SME segment signifies a significant untapped market.

The increasing focus on proactive risk management, driven by the need to predict and mitigate potential risks before they materialize, is a major growth catalyst. This, combined with the rising adoption of AI and ML capabilities within these software solutions, enhances predictive capabilities and optimizes risk mitigation strategies. Furthermore, the rising adoption of cloud-based solutions by both large enterprises and SMEs, due to their affordability and accessibility, serves as a critical growth driver. This trend is supplemented by growing government regulations and heightened awareness of potential risks within third-party ecosystems.

This report provides a comprehensive analysis of the third-party and supplier risk management software market, covering market trends, driving forces, challenges, key players, and significant developments. It offers valuable insights into the market's growth trajectory, enabling stakeholders to make informed business decisions. The report's detailed segmentation analysis helps identify key opportunities within the market and understand the evolving dynamics of the third-party risk management landscape.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 18.5% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 18.5%.

Key companies in the market include LexisNexis, LogicManager, Compliance 360, Dow Jones Risk & Compliance, Hiperos 3PM, Resolver, NAVEX Global, Quantivate, Bwise, RiskWatch International, SAP, MetricStream, .

The market segments include Type, Application.

The market size is estimated to be USD XXX N/A as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in N/A.

Yes, the market keyword associated with the report is "Third Party & Supplier Risk Management Software," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Third Party & Supplier Risk Management Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.