1. What is the projected Compound Annual Growth Rate (CAGR) of the Third-Party Hardware Maintenance Service for Data Center and Network?

The projected CAGR is approximately XX%.

Third-Party Hardware Maintenance Service for Data Center and Network

Third-Party Hardware Maintenance Service for Data Center and NetworkThird-Party Hardware Maintenance Service for Data Center and Network by Type (Storage Maintenance, Server Maintenance, Network Maintenance, Others), by Application (SMEs, Large Enterprises), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The global market for third-party hardware maintenance services for data centers and networks is experiencing robust growth, driven by increasing demand for cost-effective solutions and the rising adoption of hybrid and multi-cloud environments. Businesses are increasingly seeking alternatives to expensive OEM maintenance contracts, recognizing the potential for significant cost savings without compromising service quality. The market is characterized by a diverse range of service providers, including both large multinational corporations and specialized niche players, catering to various customer needs and infrastructure complexities. This competitive landscape fosters innovation and drives down prices, further fueling market expansion. Key growth drivers include the escalating complexity of data center infrastructure, the need for extended lifecycle support for aging hardware, and the growing focus on sustainability through optimized resource utilization. While potential restraints such as security concerns and the perception of lower service quality compared to OEMs exist, these are being mitigated by the increased technological proficiency and robust service level agreements offered by many third-party providers. The market is segmented by service type (preventive, corrective, and comprehensive), hardware type (servers, storage, networking equipment), and deployment model (on-premise, cloud). This segmentation allows providers to tailor their offerings to specific customer requirements and maximize their market penetration. Future growth will likely be shaped by advancements in artificial intelligence (AI) and machine learning for predictive maintenance and the integration of IoT devices for real-time monitoring and optimized service delivery.

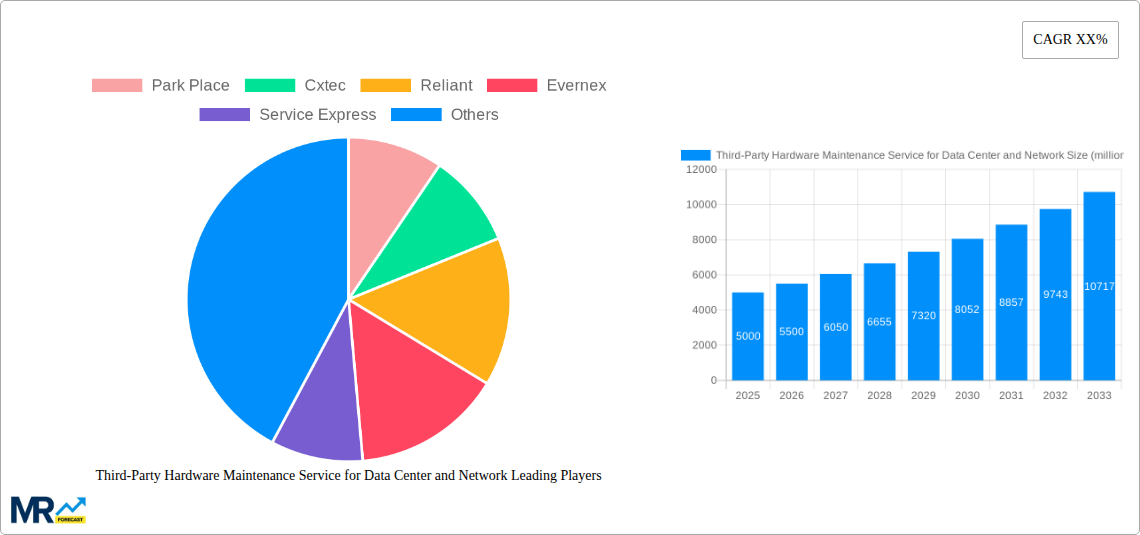

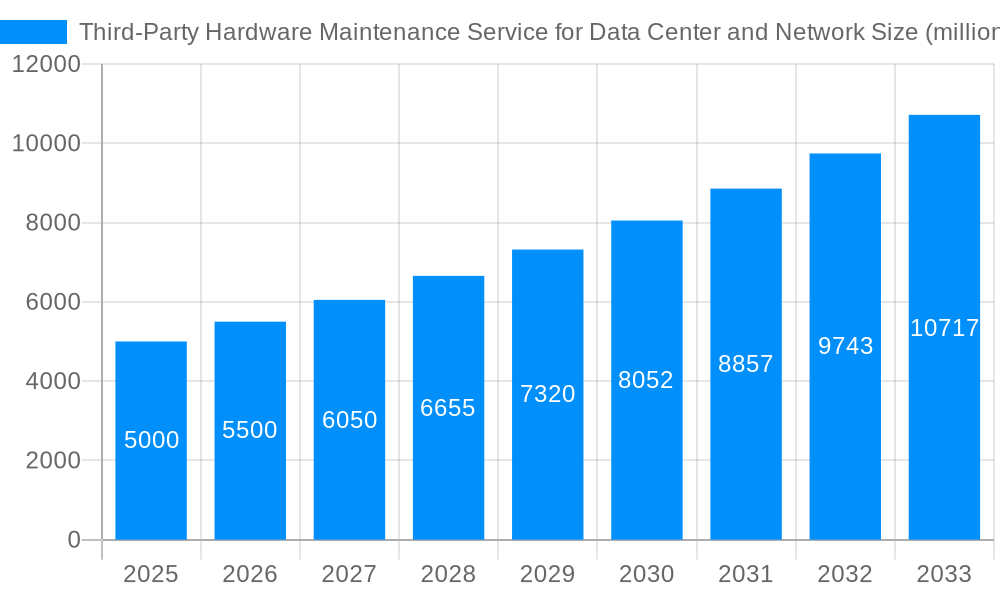

The market's expansion is projected to continue at a healthy Compound Annual Growth Rate (CAGR) throughout the forecast period (2025-2033). Assuming a conservative CAGR of 10% and a 2025 market size of $5 billion (a reasonable estimate considering the number of players and the overall IT infrastructure market), the market is poised to reach significant value by 2033. The success of individual providers will hinge on their ability to adapt to evolving technological advancements, develop strong customer relationships, and provide superior service levels while maintaining competitive pricing strategies. Key players are constantly innovating to improve service offerings and expand their geographical reach, resulting in a dynamic and rapidly evolving market landscape.

The global third-party hardware maintenance service market for data centers and networks is experiencing robust growth, projected to reach multi-billion dollar valuations by 2033. Driven by increasing data center infrastructure complexity, escalating vendor maintenance costs, and a growing preference for flexible, cost-effective solutions, this market segment shows significant promise. The historical period (2019-2024) witnessed a steady increase in market adoption, primarily fueled by enterprises seeking to optimize IT budgets and improve operational efficiency. The estimated market value in 2025 is expected to be in the hundreds of millions of dollars, setting the stage for substantial growth during the forecast period (2025-2033). Key market insights reveal a strong preference for multi-vendor support, highlighting the need for providers offering comprehensive services across diverse hardware platforms. Furthermore, the increasing adoption of cloud computing and hybrid IT models is indirectly boosting the third-party maintenance market as organizations seek cost-effective solutions for managing their legacy on-premise infrastructure alongside cloud-based resources. This trend is particularly pronounced in sectors with large data center footprints, such as finance, healthcare, and telecommunications. The rising demand for proactive maintenance and remote monitoring services further underscores the evolution of the market towards more comprehensive and preventative solutions, rather than solely reactive approaches. This shift is driven by the critical nature of data center uptime and the consequent need to minimize downtime risks. The market is also witnessing innovation in service delivery models, with a growing emphasis on AI-powered predictive maintenance and analytics to optimize service delivery and enhance overall customer experience. Finally, the increasing focus on sustainability and energy efficiency within data centers is creating new opportunities for third-party maintenance providers to offer specialized services that align with these environmental goals.

Several factors are propelling the growth of the third-party hardware maintenance service market. Firstly, the escalating costs associated with Original Equipment Manufacturer (OEM) maintenance contracts are a major driver. OEMs often charge premium rates, particularly for older equipment still in use, making third-party options significantly more attractive from a cost-saving perspective. Secondly, the increasing complexity of data center and network infrastructure necessitates expertise across diverse vendor platforms. Third-party providers offer this multi-vendor support capability, a crucial advantage over OEMs who primarily focus on their own products. Thirdly, the growing demand for enhanced flexibility and customization is driving adoption. Third-party providers can often tailor their service level agreements (SLAs) to specific customer needs, offering options unavailable through rigid OEM contracts. Fourthly, the increasing importance of proactive maintenance and remote monitoring is fueling this trend. Third-party providers are investing heavily in sophisticated monitoring tools and predictive analytics, enabling faster issue resolution and minimizing downtime. Finally, the need for extended support lifecycles for legacy equipment, which may no longer be covered by OEMs, presents another key opportunity. Third-party providers offer continued support for these systems, preventing premature hardware replacement and extending the useful life of existing investments. These factors converge to create a compelling case for businesses to adopt third-party hardware maintenance, optimizing both cost and operational efficiency.

Despite the market’s strong growth trajectory, several challenges and restraints exist. Firstly, concerns about the quality and reliability of third-party support compared to OEMs remain a significant obstacle for some organizations. Building trust and demonstrating comparable or superior service levels is crucial for gaining wider adoption. Secondly, the highly fragmented nature of the market can create complexity for customers trying to navigate the numerous providers and their differing service offerings. This necessitates thorough due diligence and a clear understanding of service level agreements. Thirdly, the management of spare parts inventory poses a significant operational challenge for third-party providers. Ensuring timely access to critical parts is crucial for maintaining service levels and meeting customer expectations. Maintaining a robust and readily accessible inventory necessitates significant upfront investment. Furthermore, potential legal issues, including intellectual property concerns and warranty considerations associated with non-OEM parts and services, can add complexity and risk for both providers and customers. Finally, the intense competition in the market puts pressure on pricing and profit margins, particularly for smaller players lacking the economies of scale of larger competitors. Successfully navigating these challenges requires a combination of strategic investment in quality assurance, robust inventory management, strong customer relationships, and a focus on innovative service delivery models.

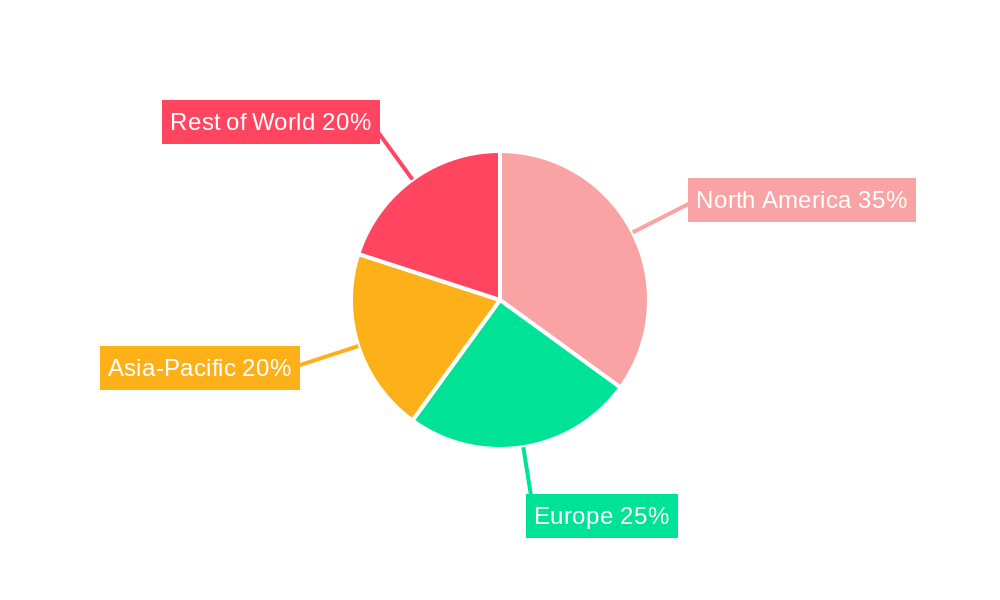

The North American market is anticipated to hold a significant share, driven by a high concentration of data centers and a substantial number of organizations adopting third-party maintenance services. The strong IT infrastructure and the early adoption of advanced technologies in this region contribute to its leading position. Europe is also a key market, exhibiting substantial growth potential due to the increasing adoption of cloud computing and the demand for cost-effective IT solutions across various industries. The Asia-Pacific region displays the most rapid growth, fueled by the rapid expansion of data centers and the escalating demand for IT services in emerging economies. Within market segments, the data center segment is expected to hold a larger market share compared to the networking segment due to the increasing complexity and criticality of data center infrastructure. This high complexity makes specialized third-party maintenance highly attractive.

The paragraph above elaborates on the reasons behind the dominance of these regions and segments. The high concentration of data centers and technologically advanced infrastructure in North America leads to a high demand for efficient and cost-effective maintenance solutions. Similarly, the rapid growth in cloud computing and the drive towards cost optimization in Europe and Asia-Pacific propel market growth in these regions. Within the segments, the data center segment benefits from a higher reliance on specialized maintenance due to the critical nature and complexity of data center infrastructure.

Several factors are catalyzing growth within this industry. The rising adoption of hybrid cloud models requires robust management of both on-premise and cloud infrastructure, creating a significant demand for flexible and cost-effective third-party maintenance solutions. Moreover, the increasing focus on operational efficiency and the desire to optimize IT budgets are pushing companies to seek alternatives to high-priced OEM contracts. Finally, innovations in service delivery, such as AI-powered predictive maintenance and remote diagnostics, are further enhancing the value proposition of third-party maintenance services, contributing significantly to the market's overall expansion.

This report offers a comprehensive overview of the third-party hardware maintenance service market for data centers and networks, providing in-depth analysis of market trends, driving forces, challenges, key players, and significant developments. It covers the historical period (2019-2024), the base year (2025), the estimated year (2025), and forecasts for the period 2025-2033. The report also includes detailed regional and segment analysis, providing valuable insights for businesses seeking to capitalize on the growth opportunities in this dynamic market.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Park Place, Cxtec, Reliant, Evernex, Service Express, OSI Hardware, SBA, Atlantix, CentricsIT, Curvature, Hive Data Center, EmconIT, InKnowTech, ISC Group, Keltech, Aintech, Neeco, NorthSmartIT, Procurri, DataSpan, Thomastech, XS International, Maintech, M Global Services.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Third-Party Hardware Maintenance Service for Data Center and Network," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Third-Party Hardware Maintenance Service for Data Center and Network, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.