1. What is the projected Compound Annual Growth Rate (CAGR) of the Telecom Cyber Security Solution?

The projected CAGR is approximately 6.1%.

Telecom Cyber Security Solution

Telecom Cyber Security SolutionTelecom Cyber Security Solution by Type (Device, Service, Sofware), by Application (Small Businesses, Medium Businesses, Large Businesses), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

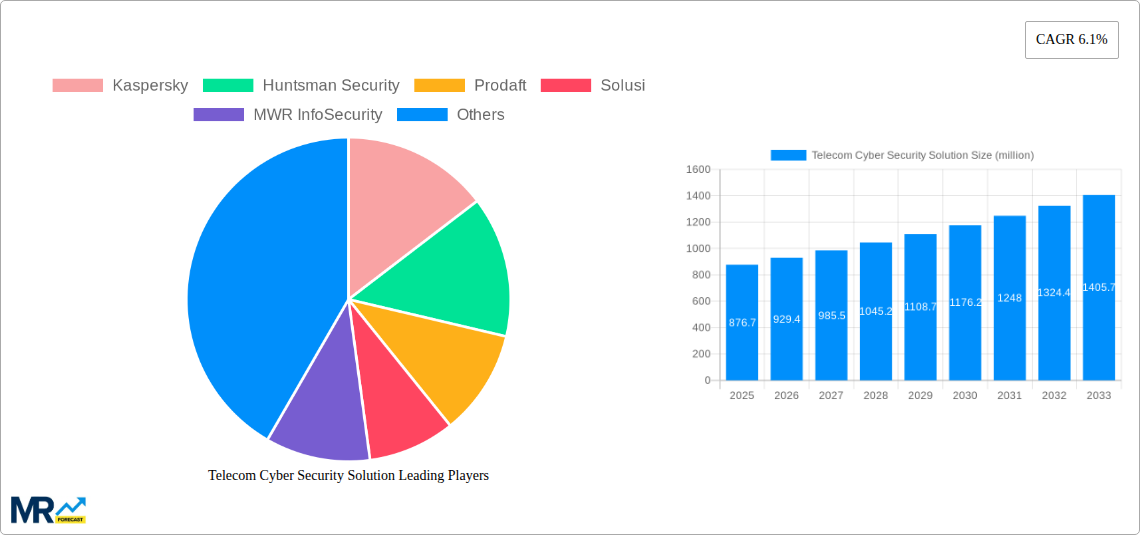

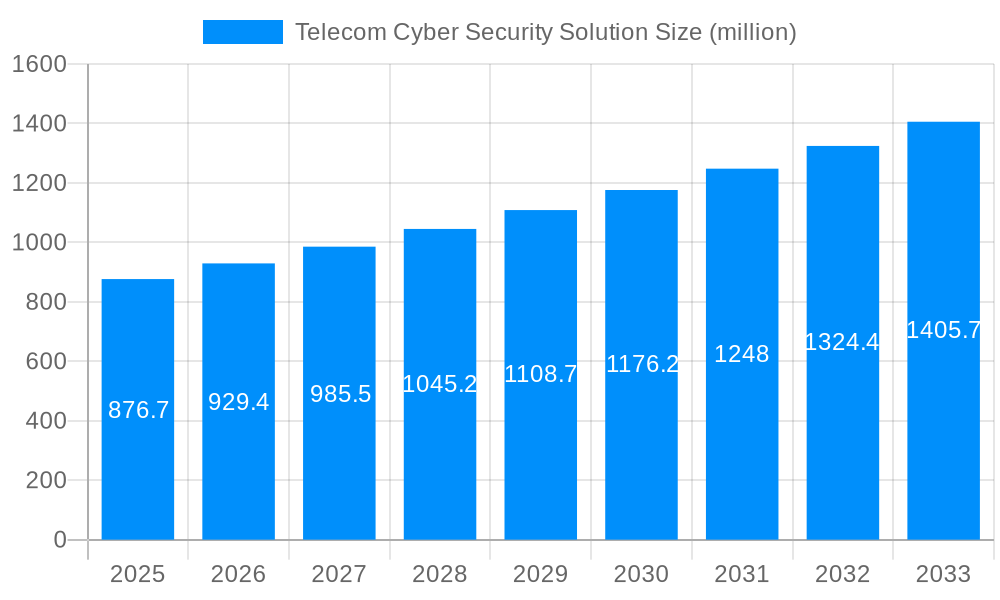

The global Telecom Cyber Security Solution market is poised for significant expansion, projected to reach an estimated $876.7 million by 2025, exhibiting a robust Compound Annual Growth Rate (CAGR) of 6.1%. This growth is primarily fueled by the escalating sophistication and frequency of cyber threats targeting telecommunication networks, which are increasingly becoming critical infrastructure. The imperative to protect sensitive customer data, ensure service continuity, and maintain regulatory compliance are paramount drivers for telecommunication providers to invest heavily in advanced cybersecurity measures. The proliferation of 5G technology, the Internet of Things (IoT), and the growing reliance on cloud-based services within the telecom sector further amplify the attack surface, necessitating comprehensive and adaptive security solutions. This escalating threat landscape, coupled with the immense value of the data processed and transmitted by telecom companies, creates a substantial demand for robust and forward-thinking cyber defenses.

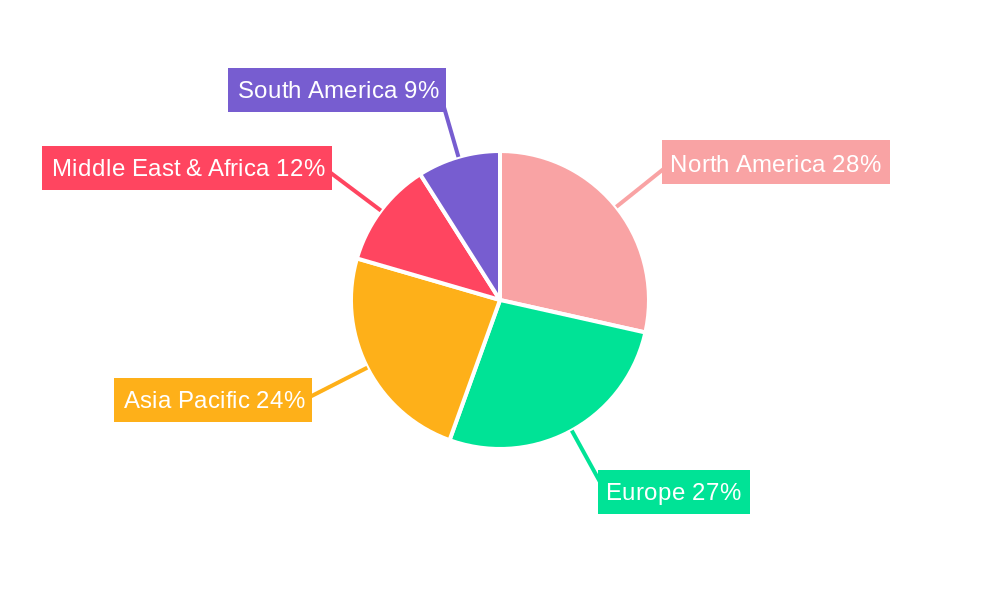

The market segmentation reveals a diverse range of offerings, with devices, services, and software all playing crucial roles. Services, in particular, are expected to see substantial adoption due to the complexity of modern cybersecurity challenges, encompassing threat intelligence, managed security services, and incident response. Geographically, North America and Europe are anticipated to lead the market in terms of adoption and investment, owing to their mature telecommunications infrastructure and stringent data protection regulations. However, the Asia Pacific region, driven by rapid digital transformation and the expansion of 5G networks in countries like China and India, presents a significant growth opportunity. Key players like IBM, Cisco, and Kaspersky are actively developing and deploying innovative solutions to address the evolving cybersecurity needs of telecommunication operators. The market's trajectory indicates a continuous evolution of security strategies, moving towards proactive threat detection, artificial intelligence-driven security, and a more holistic approach to network protection.

This comprehensive report delves into the dynamic and critical domain of Telecom Cyber Security Solutions. The telecommunications sector, the backbone of modern digital connectivity, faces an ever-escalating array of cyber threats. As the industry grapples with the complexities of 5G deployment, the Internet of Things (IoT), and the increasing reliance on cloud-based infrastructure, the imperative for robust cybersecurity measures has never been more pronounced. This study provides an in-depth analysis of the market dynamics, key trends, driving forces, challenges, and the dominant players shaping the telecom cybersecurity landscape from the historical period of 2019-2024 through to the forecast period of 2025-2033, with the base year and estimated year set at 2025. The projected market size for these solutions is estimated to reach USD 45,500 million by 2025, with a projected compound annual growth rate (CAGR) of 12.7% from 2025 to 2033, reaching an estimated USD 115,750 million by the end of the study period.

XXX The telecom cybersecurity market is undergoing a significant transformation, driven by the relentless evolution of cyber threats and the increasing sophistication of attack vectors targeting critical network infrastructure. A primary trend is the pervasive shift towards cloud-native security solutions, enabling telecom operators to leverage the scalability and agility of cloud environments for threat detection, response, and management. This includes the adoption of Security Information and Event Management (SIEM) and Security Orchestration, Automation, and Response (SOAR) platforms tailored for the specific needs of telcos. The proliferation of 5G networks presents a dual-edged sword: while offering enhanced capabilities, it also expands the attack surface, necessitating advanced security measures like Network Function Virtualization (NFV) and Software-Defined Networking (SDN) security, along with robust edge security solutions. The increasing volume and complexity of IoT devices connected to telecom networks present another critical area of focus, demanding specialized IoT security solutions that can manage vulnerabilities and secure device communication at scale. Furthermore, there's a growing emphasis on proactive threat intelligence and predictive analytics, allowing telcos to anticipate and mitigate potential attacks before they occur. The integration of Artificial Intelligence (AI) and Machine Learning (ML) into cybersecurity platforms is becoming indispensable for identifying anomalous behavior, detecting zero-day threats, and automating response mechanisms, thereby enhancing the efficiency and effectiveness of security operations. The regulatory landscape is also playing a crucial role, with stricter data privacy laws and cybersecurity mandates pushing telecom companies to invest heavily in compliance-driven security solutions. This includes robust data encryption, secure access controls, and comprehensive audit trails to meet stringent regulatory requirements. The market is also witnessing a rise in specialized security services, such as managed security services (MSSPs) and threat hunting, allowing telecom operators to outsource complex security operations and gain access to expert capabilities. The ongoing evolution of encryption techniques and post-quantum cryptography is also gaining traction as telcos prepare for future threats that could compromise current encryption standards. The demand for Zero Trust Architecture implementation within telecom networks is also accelerating, ensuring that no user or device is inherently trusted, regardless of its location within the network. The increasing adoption of containerization and microservices architectures within telecom infrastructure further necessitates granular security controls and DevSecOps practices to ensure secure software development and deployment pipelines. The market also sees a growing emphasis on identity and access management (IAM) solutions, including multi-factor authentication (MFA) and privileged access management (PAM), to secure sensitive network components and user credentials. Overall, the telecom cybersecurity landscape is characterized by a proactive, intelligent, and layered approach to security, driven by technological advancements and the escalating threat environment.

The rapid expansion of digital services and the increasing reliance on telecommunications infrastructure for critical operations are the primary catalysts propelling the growth of the telecom cyber security solution market. The ongoing digital transformation across industries, from finance and healthcare to manufacturing and government, has made robust and secure communication networks paramount. As these sectors become more interconnected and dependent on seamless connectivity, the potential impact of cyberattacks on telecom infrastructure escalates significantly, necessitating substantial investments in cybersecurity. The widespread adoption of 5G technology, with its promise of higher speeds, lower latency, and massive connectivity, introduces a vastly expanded attack surface. This necessitates sophisticated security solutions to protect the core network, edge computing resources, and the myriad of connected devices. Furthermore, the surge in remote work and the increasing use of cloud-based services have blurred traditional network perimeters, demanding more comprehensive and dynamic security strategies that can protect data and applications wherever they reside. The growing threat landscape, characterized by increasingly sophisticated and persistent cyberattacks, including ransomware, distributed denial-of-service (DDoS) attacks, and advanced persistent threats (APTs), is a significant driver. Telecom operators are prime targets due to the critical nature of their services and the vast amounts of sensitive data they handle. Regulatory compliance is another powerful force. Governments worldwide are implementing stringent regulations concerning data privacy, network security, and critical infrastructure protection, compelling telecom companies to enhance their cybersecurity posture to avoid hefty fines and reputational damage. The rise of the Internet of Things (IoT) ecosystem, with billions of connected devices, presents a unique set of security challenges. Securing these devices and the data they generate is crucial for preventing them from being exploited as entry points for malicious actors into the broader network.

Despite the robust growth trajectory, the telecom cyber security solution market is not without its significant challenges and restraints. A primary concern is the sheer complexity and scale of telecommunications networks. The intricate architecture of legacy systems intertwined with newer technologies like 5G and SDN creates a fragmented and difficult-to-secure environment. Integrating disparate security solutions across these diverse platforms often proves to be a formidable task, leading to potential gaps in protection. The shortage of skilled cybersecurity professionals is another critical bottleneck. The specialized knowledge required to manage and secure advanced telecom networks, coupled with the global demand for such talent, makes it difficult for telecom operators to recruit and retain the necessary expertise. This talent deficit can hinder the effective deployment and ongoing management of sophisticated security solutions. The rapidly evolving threat landscape poses a constant challenge. Cybercriminals are continuously developing new attack methodologies, often outpacing the development and deployment of corresponding security measures. This necessitates a continuous cycle of updating and adapting security strategies, which can be costly and resource-intensive. The high cost of implementing and maintaining comprehensive cybersecurity solutions can also be a restraint, particularly for smaller telecom providers or those operating in emerging markets with limited budgets. The initial investment in advanced hardware, software, and skilled personnel can be substantial. Furthermore, the perceived trade-off between security and performance can sometimes lead to resistance. Implementing certain security measures, such as deep packet inspection or extensive encryption, might introduce latency or impact network throughput, leading to concerns about service quality for end-users. The challenge of securing the vast and diverse ecosystem of IoT devices is also immense. The inherent vulnerabilities in many IoT devices, coupled with the lack of standardized security protocols, makes them attractive targets for attackers and difficult to secure comprehensively. Lastly, the fragmented regulatory landscape across different regions can create compliance complexities for multinational telecom operators, requiring tailored security approaches for various jurisdictions.

The global Telecom Cyber Security Solution market is experiencing significant regional and segment-driven growth, with certain areas and market segments poised to dominate the landscape in the coming years.

Dominant Regions:

North America: This region, particularly the United States, is expected to maintain its leading position in the Telecom Cyber Security Solution market. This dominance is driven by several factors:

Europe: Europe, with its strong emphasis on data privacy (e.g., GDPR) and the ongoing expansion of 5G networks, is another significant contributor to market growth.

Dominant Segments:

Type: Software

Application: Large Businesses

The Telecom Cyber Security Solution industry is experiencing accelerated growth fueled by several key catalysts. The relentless evolution of sophisticated cyber threats, including ransomware, APTs, and DDoS attacks, is forcing telecom operators to proactively enhance their defenses. The widespread adoption of 5G technology, with its expanded attack surface and increased connectivity, necessitates advanced security measures for network infrastructure and connected devices. The burgeoning Internet of Things (IoT) ecosystem presents unique security challenges, driving demand for specialized IoT security solutions. Furthermore, stringent government regulations and data privacy mandates worldwide are compelling telecom companies to invest significantly in compliance-driven cybersecurity.

The telecom cyber security solution market is characterized by the presence of established technology giants and specialized cybersecurity firms. Some of the leading players include:

This report provides an unparalleled, in-depth analysis of the Telecom Cyber Security Solution market, offering a comprehensive view of its trajectory from 2019 to 2033. It meticulously dissects key market insights, identifying the critical trends and their implications for telecom operators. The study highlights the potent driving forces, such as the digital transformation imperative and the advent of 5G, that are propelling market expansion. Simultaneously, it critically examines the pervasive challenges and restraints, including the complexity of networks and the cybersecurity talent shortage, that organizations must navigate. Furthermore, the report dedicates significant attention to identifying the dominant regions and market segments—focusing on Software as a Type and Large Businesses as an Application—that are shaping the future of telecom cybersecurity. It also pinpoints crucial growth catalysts and provides an exhaustive overview of the leading players and their recent strategic developments. This holistic approach ensures that stakeholders gain a thorough understanding of the market landscape, enabling informed strategic decisions and robust cybersecurity planning in this vital and rapidly evolving sector.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.1% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 6.1%.

Key companies in the market include Kaspersky, Huntsman Security, Prodaft, Solusi, MWR InfoSecurity, IBM, BAE Systems, Cisco, Senseon, .

The market segments include Type, Application.

The market size is estimated to be USD 876.7 million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Telecom Cyber Security Solution," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Telecom Cyber Security Solution, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.