1. What is the projected Compound Annual Growth Rate (CAGR) of the Surplus Lines Insurance?

The projected CAGR is approximately XX%.

Surplus Lines Insurance

Surplus Lines InsuranceSurplus Lines Insurance by Type (General Business Liability Insurance, Allied Lines Insurance, Fire Insurance, Inland Marine Insurance, Commercial Multi-Peril Insurance, Commercial Auto Insurance, Others), by Application (Commercial, Personal), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

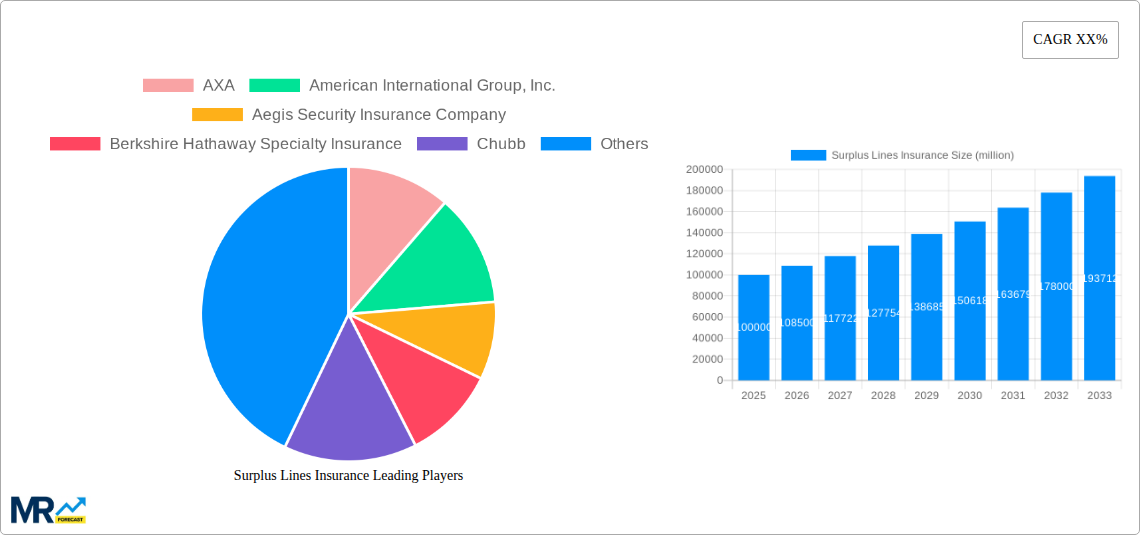

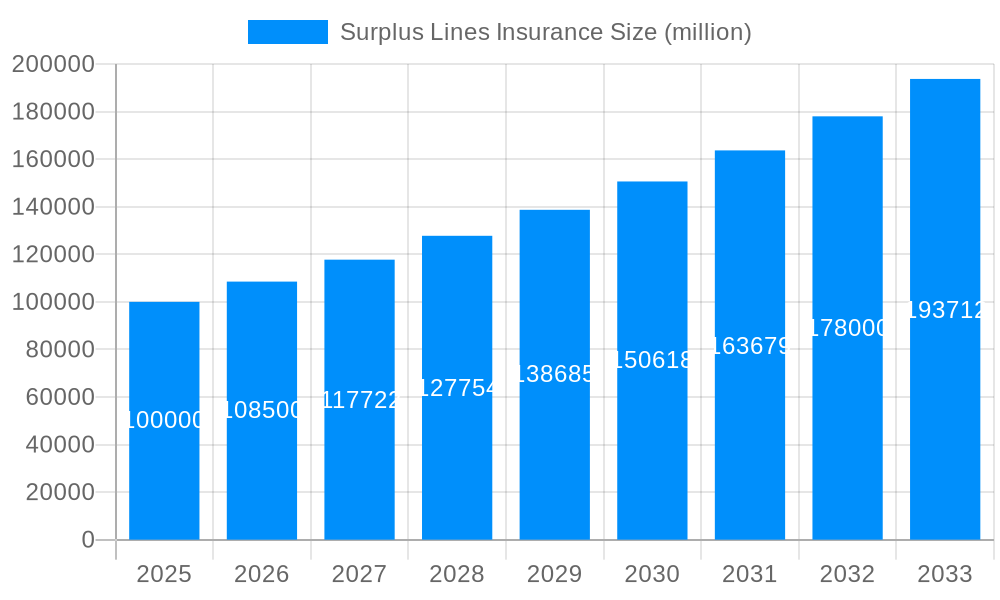

The Surplus Lines Insurance market is projected for substantial growth, estimated to reach approximately $100 billion by 2025, with a projected Compound Annual Growth Rate (CAGR) of around 8.5% through 2033. This expansion is primarily fueled by the increasing demand for specialized and customized insurance solutions that are not readily available in the standard admitted market. Key drivers include the growing complexity of business operations, rising cyber threats, and the escalating frequency and severity of natural catastrophes, all of which necessitate tailored coverage. Furthermore, a more flexible regulatory environment in certain regions is enabling insurers to offer more innovative products, contributing to market buoyancy. The market’s resilience is also a testament to its ability to cater to high-risk industries and unique exposures that traditional insurers may deem too volatile.

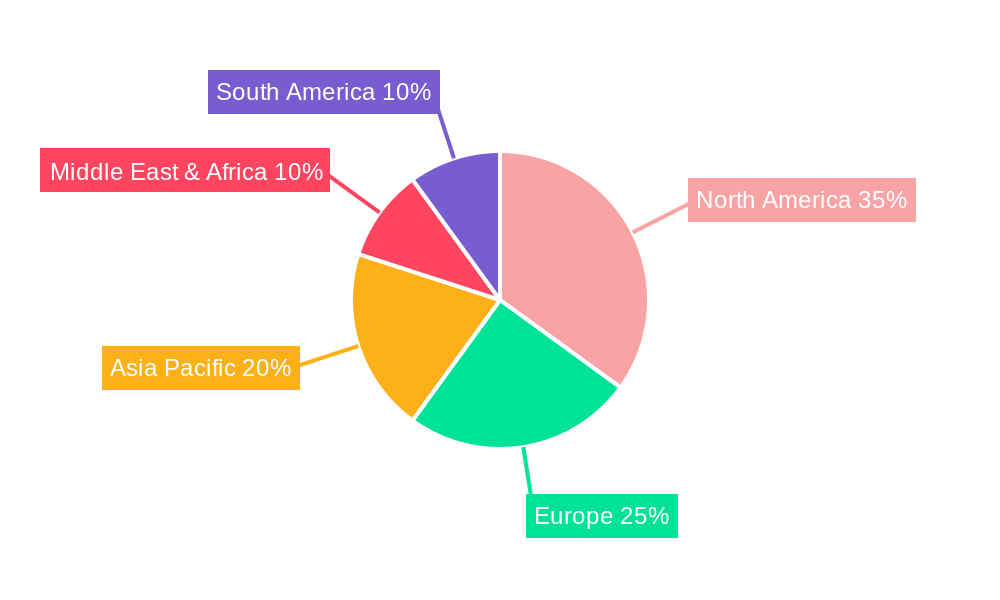

The market is segmented into various types of coverage, with General Business Liability Insurance and Commercial Multi-Peril Insurance expected to command significant shares due to their broad applicability to businesses. The application of surplus lines insurance spans both commercial and personal sectors, though the commercial segment is anticipated to dominate due to the higher value and complexity of risks involved. Geographically, North America is a leading region, driven by the mature insurance landscape in the United States and Canada, coupled with the increasing demand for specialized coverage in Mexico. Asia Pacific is emerging as a high-growth region, supported by rapid industrialization, infrastructure development, and a rising awareness of insurance needs in countries like China and India. Restraints include potential regulatory hurdles in certain jurisdictions and the inherent volatility associated with the risks covered.

This report offers an in-depth analysis of the global Surplus Lines Insurance market, a critical segment of the insurance industry that provides coverage for risks deemed uninsurable by standard admitted carriers. Spanning a study period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period from 2025 to 2033, this comprehensive study delves into historical trends, driving forces, significant challenges, and future growth trajectories. The report utilizes both quantitative data and qualitative insights to provide a robust understanding of market dynamics, player strategies, and segment-specific performance, valuable for stakeholders seeking strategic guidance and market intelligence.

The report's detailed segmentation covers various insurance types including General Business Liability Insurance, Allied Lines Insurance, Fire Insurance, Inland Marine Insurance, Commercial Multi-Peril Insurance, Commercial Auto Insurance, and Others. It also examines market penetration across Commercial and Personal applications. Key industry developments and the competitive landscape featuring major players such as AXA, American International Group, Inc., Aegis Security Insurance Company, Berkshire Hathaway Specialty Insurance, Chubb, Lloyd's, ProSight Specialty Insurance, Swiss Re, Travelers Insurance, and Zurich are meticulously analyzed.

The Surplus Lines Insurance market is characterized by a dynamic interplay of evolving risk landscapes, regulatory shifts, and the inherent capacity of admitted markets. Over the historical period (2019-2024), the market has demonstrated resilience and adaptability, consistently finding innovative solutions for complex and unique risks. A significant trend observed has been the increasing demand for specialty coverages driven by the burgeoning gig economy, cybersecurity threats, and the rise of new industries. For instance, in 2023, the global market saw a notable uptick in demand for cyber liability insurance within the surplus lines sector, with an estimated value of $15,000 million, as businesses grappled with an escalating number of sophisticated cyberattacks. Similarly, the Commercial Multi-Peril Insurance segment, particularly for businesses operating in high-risk geographic locations or with unique operational exposures, has consistently contributed a substantial portion to the market's overall value, estimated to be around $25,000 million in 2024.

Looking ahead, the forecast period (2025-2033) is expected to witness sustained growth, driven by several key factors. The projected market value for 2025 is estimated at $75,000 million, with a projected compound annual growth rate (CAGR) of approximately 6.5% through 2033. This growth is underpinned by an expanding array of specialized risks that admitted carriers are less inclined or equipped to underwrite. For example, the rise of environmental, social, and governance (ESG) related liabilities is creating new underwriting opportunities. The report anticipates a substantial increase in demand for Directors & Officers (D&O) liability insurance for companies navigating complex ESG reporting requirements and potential litigation, potentially reaching $8,000 million by 2030. Furthermore, advancements in technology, such as artificial intelligence and the Internet of Things (IoT), are creating novel risks that will necessitate the unique flexibility and expertise offered by surplus lines insurers. The inland marine segment, encompassing coverage for goods in transit and specialized equipment, is also poised for steady growth, estimated to reach $10,000 million by 2028, driven by global supply chain complexities and increased project-based construction activities. The market’s ability to tailor coverage to highly specific needs will remain its paramount advantage.

Several potent forces are actively propelling the growth and evolution of the Surplus Lines Insurance market. Foremost among these is the persistent capacity constraint within the traditional admitted insurance markets. As natural disasters become more frequent and severe, and as new and complex risks emerge, admitted insurers often find their risk appetite limited, leading them to withdraw from certain high-hazard classes or impose stricter underwriting guidelines. This creates a crucial opening for surplus lines insurers, who are specifically designed to absorb these harder-to-place risks. The increasing prevalence of climate-related events, such as hurricanes and wildfires, has significantly impacted sectors like property insurance, pushing businesses in vulnerable regions to seek coverage in the surplus lines market, contributing an estimated $12,000 million in new premiums in 2023 alone.

Furthermore, the proliferation of emerging risks, such as cyber threats, product liability for innovative technologies, and environmental liabilities, plays a pivotal role. These risks often lack historical data for actuarial analysis, making them difficult for standard insurers to price and underwrite. Surplus lines insurers, with their specialized expertise and flexible regulatory framework, are adept at developing innovative solutions for these novel exposures. For instance, the demand for cyber insurance has surged, with the surplus lines market providing coverage for high-limit cyber policies and complex data breach scenarios, estimated to be worth $7,000 million in 2024. The growing complexity of business operations, including global supply chains and intricate liability structures, also necessitates customized insurance solutions that the surplus lines market is uniquely positioned to provide, leading to substantial growth in segments like Inland Marine Insurance, which is projected to reach $10,000 million by 2028. The adaptability and specialized underwriting capabilities of surplus lines carriers allow them to cater to these evolving and intricate risk profiles effectively.

Despite its robust growth, the Surplus Lines Insurance market is not without its considerable challenges and restraints, which can temper its expansion. A primary concern is the fluctuating availability of capacity, particularly for very high-severity risks or in the aftermath of major catastrophic events. When large-scale natural disasters strike, reinsurers, who are crucial partners for surplus lines insurers, may pull back capacity, making it more difficult and expensive for surplus lines carriers to find reinsurance and, consequently, to offer coverage. This can lead to periods of market hardening, where premiums skyrocket and terms become more restrictive, potentially pushing some buyers back to the admitted market if their risks become more palatable. The impact of major hurricanes in 2022, for example, led to a noticeable reduction in property catastrophe reinsurance capacity, impacting the surplus lines market's ability to underwrite large coastal properties, potentially affecting an estimated $5,000 million in potential coverage.

Another significant restraint is the evolving regulatory landscape. While surplus lines operate under a more flexible state-based regulatory system compared to admitted carriers, there is a constant undercurrent of potential federal intervention or increased state-level scrutiny. Proposed changes to domicile requirements, capital standards, or consumer protection measures could impose additional burdens and compliance costs on surplus lines insurers. The market’s reliance on the "surplus lines broker" model also presents challenges. Ensuring that brokers are adequately trained and knowledgeable about the complex products they are offering is paramount to avoid misrepresentation or inadequate coverage, which can lead to regulatory action and reputational damage. The complexity of coverage terms and conditions in surplus lines policies, while necessary for unique risks, can also lead to disputes and misunderstandings with policyholders, impacting customer satisfaction and potentially leading to litigation, estimated to contribute to an additional $1,000 million in claims-related expenses in 2023. Furthermore, economic downturns can impact the demand for higher-premium surplus lines coverage as businesses seek to reduce expenses.

The global surplus lines insurance market is exhibiting strong growth across multiple regions and segments, with certain areas and product lines demonstrating particularly significant dominance. The United States continues to be the largest and most influential market for surplus lines insurance. Its mature financial sector, litigious environment, and a broad spectrum of specialized industries create a perpetual need for insurance solutions beyond the capacity or appetite of admitted carriers. The sheer scale of commercial enterprises and the complexity of their operations in the U.S. consistently drive demand across various segments. For instance, the Commercial Multi-Peril Insurance segment in the U.S. is a cornerstone of the surplus lines market. In 2023, this segment alone accounted for an estimated $20,000 million in gross written premiums within the U.S. surplus lines market, covering a vast array of businesses from small enterprises to large corporations with unique property exposures, those located in high-risk catastrophe zones, or those with specialized operational needs.

Within the U.S. market, the General Business Liability Insurance segment also holds substantial sway. The increasing frequency of liability claims, coupled with evolving legal interpretations and the rise of new liability exposures, ensures a consistent demand for surplus lines expertise. This segment is projected to contribute approximately $15,000 million to the U.S. surplus lines market by 2025. Another segment showing significant dominance, particularly due to its specialized nature, is Allied Lines Insurance. This encompasses a broad range of coverages, including professional liability (E&O), directors and officers (D&O), and cyber liability. The rapid technological advancements, the growing complexity of corporate governance, and the increasing threat landscape have made these coverages indispensable. The U.S. surplus lines market for cyber liability insurance alone was estimated at $7,000 million in 2024, with significant growth anticipated.

Geographically, beyond the dominant U.S. market, regions experiencing rapid industrialization and technological innovation are also showing increasing potential. While not yet on par with the U.S., markets in Europe, particularly the United Kingdom and continental European nations with strong financial centers, are significant contributors. The Lloyd's market, based in London, is a global powerhouse in specialty and surplus lines insurance, underwriting risks from around the world and influencing market trends significantly. Its diverse syndicates offer unparalleled capacity and expertise across a vast spectrum of challenging risks, including Inland Marine Insurance, which saw significant growth in Europe due to cross-border trade and project finance, estimated at $3,000 million in gross premiums by 2024. The Asia-Pacific region, particularly countries like Singapore and Australia, is also emerging as a growing market for surplus lines insurance, driven by their expanding economies and increasing exposure to natural catastrophes and complex commercial risks.

Several key factors are acting as powerful growth catalysts for the Surplus Lines Insurance industry. The increasing frequency and severity of catastrophic events, such as wildfires and floods, are pushing many businesses out of the standard admitted market, creating substantial demand for specialized coverage in the surplus lines sector. Furthermore, the rapid evolution of new technologies and business models, like the burgeoning drone industry and advanced manufacturing, generates novel and complex risks that admitted carriers are often ill-equipped to underwrite. This necessitates the flexible and innovative underwriting capabilities that surplus lines insurers provide.

This report provides a holistic view of the surplus lines insurance market, offering unparalleled insights into its intricate workings. It meticulously details the historical performance, current dynamics, and future projections of this vital sector, which acts as a crucial safety net for risks that fall outside the purview of traditional insurance. The report’s comprehensive analysis covers market size estimations in millions, including a projected market value of $75,000 million by 2025 and an anticipated CAGR of 6.5% through 2033, underpinned by robust quantitative data. It explores the drivers of growth, such as the increasing capacity constraints in admitted markets and the emergence of novel risks like advanced cyber threats, highlighting specific segments like Commercial Multi-Peril Insurance, estimated to be worth $25,000 million in 2024. Conversely, it also addresses the challenges, including regulatory complexities and the volatility of reinsurance capacity.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include AXA, American International Group, Inc., Aegis Security Insurance Company, Berkshire Hathaway Specialty Insurance, Chubb, Lloyd's, ProSight Specialty Insurance, Swiss Re, Travelers Insurance, Zurich, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Surplus Lines Insurance," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Surplus Lines Insurance, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.