1. What is the projected Compound Annual Growth Rate (CAGR) of the Silicon Carbide Porous Ceramic Vacuum Chucks for Semiconductor Wafers?

The projected CAGR is approximately 10.97%.

Silicon Carbide Porous Ceramic Vacuum Chucks for Semiconductor Wafers

Silicon Carbide Porous Ceramic Vacuum Chucks for Semiconductor WafersSilicon Carbide Porous Ceramic Vacuum Chucks for Semiconductor Wafers by Type (300 mm, 200 mm, Others, World Silicon Carbide Porous Ceramic Vacuum Chucks for Semiconductor Wafers Production ), by Application (IDM, Foundry, Semiconductor Equipment Suppliers, World Silicon Carbide Porous Ceramic Vacuum Chucks for Semiconductor Wafers Production ), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

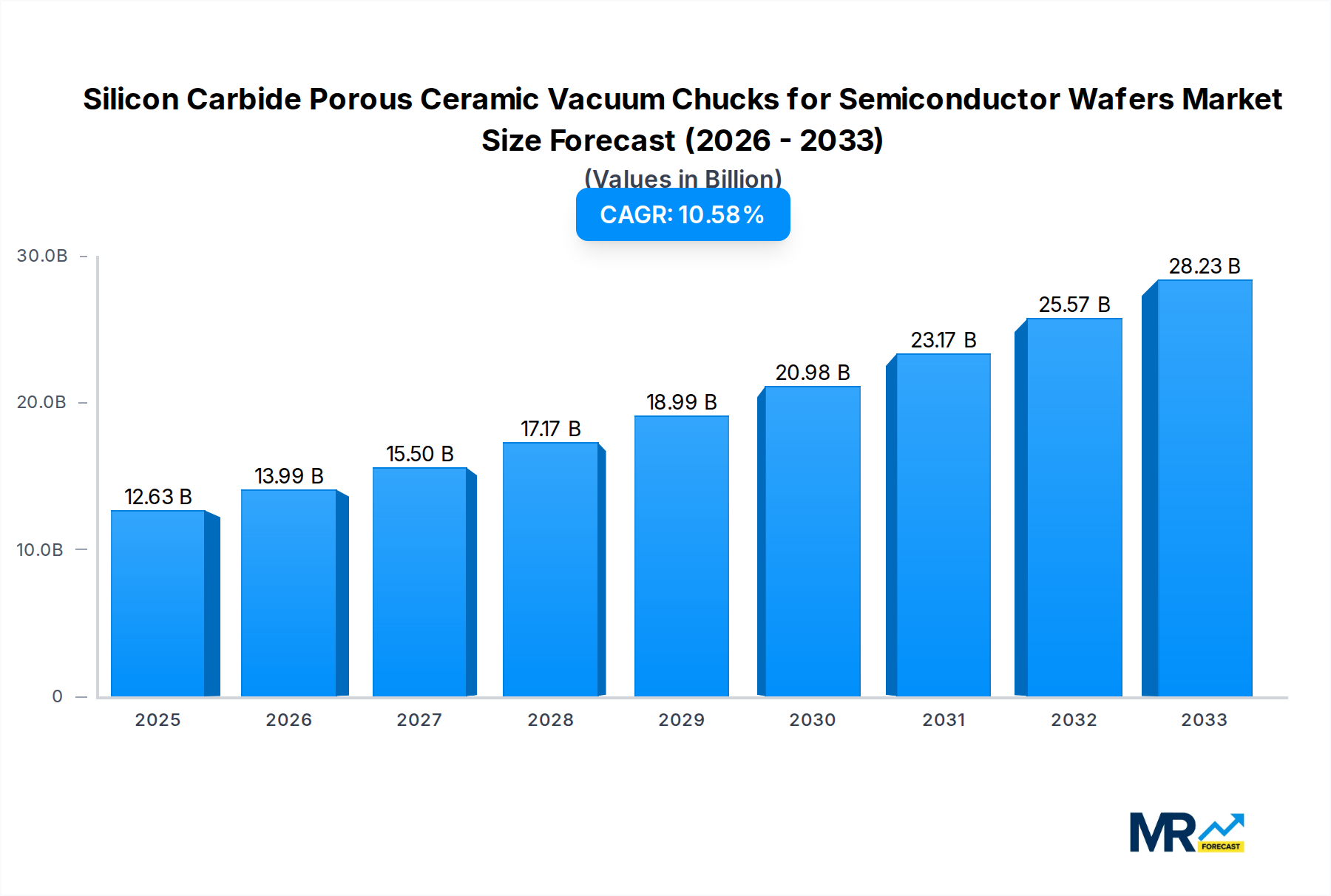

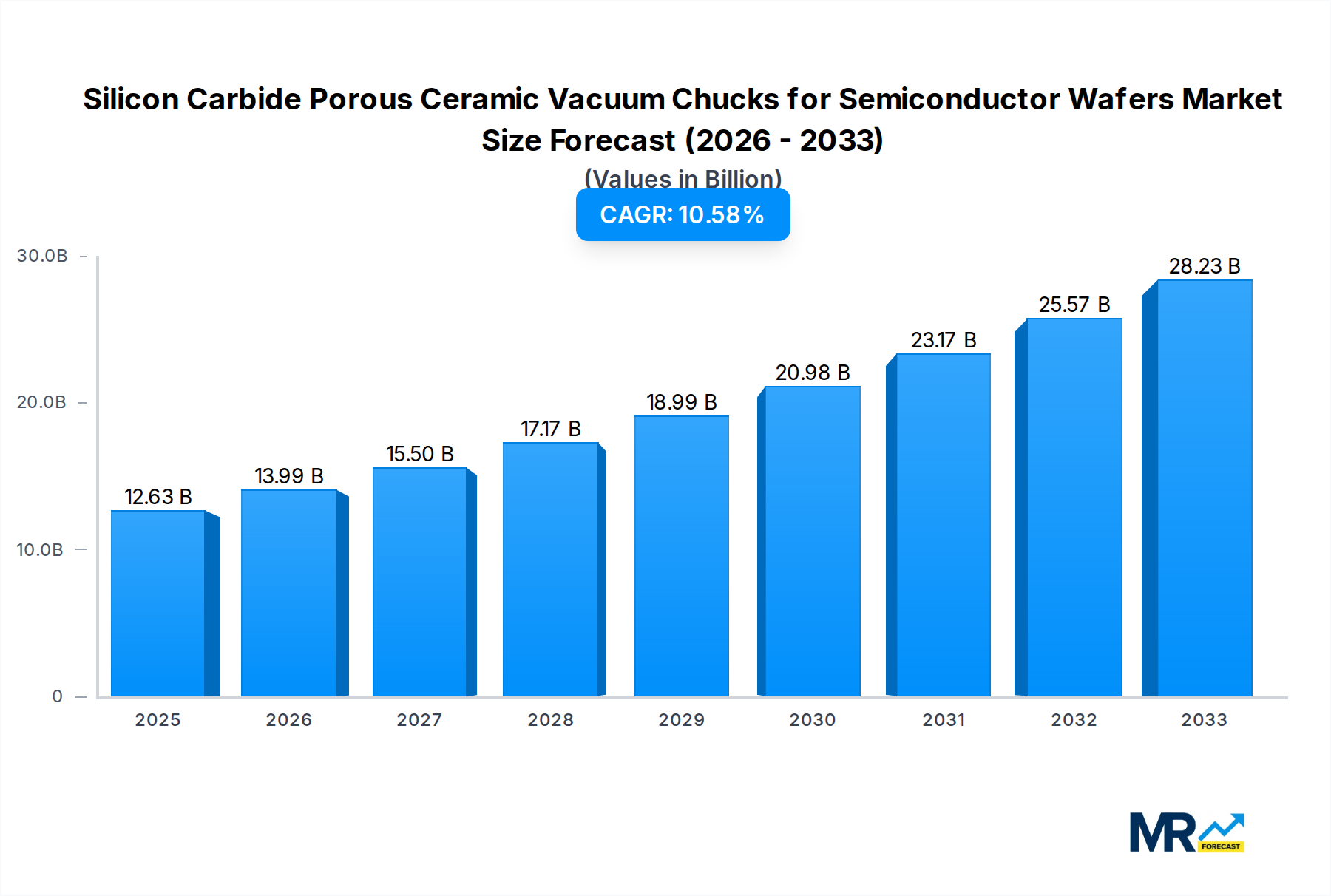

The global market for Silicon Carbide Porous Ceramic Vacuum Chucks for Semiconductor Wafer Production is experiencing robust growth, projected to reach an estimated USD 12.63 billion by 2025, with a compound annual growth rate (CAGR) of 10.97% anticipated through 2033. This upward trajectory is primarily fueled by the escalating demand for advanced semiconductors, driven by the proliferation of 5G technology, artificial intelligence, IoT devices, and high-performance computing. The increasing complexity and miniaturization of semiconductor components necessitate precision handling and reliable wafer support during various manufacturing processes, making these specialized ceramic vacuum chucks indispensable. Key drivers include the continuous innovation in semiconductor fabrication techniques, the growing need for higher yields and reduced wafer defects, and the inherent material advantages of silicon carbide, such as its excellent thermal conductivity, mechanical strength, and resistance to wear and chemical corrosion. The market's expansion is further supported by significant investments in semiconductor manufacturing facilities worldwide, particularly in regions with strong technological ecosystems.

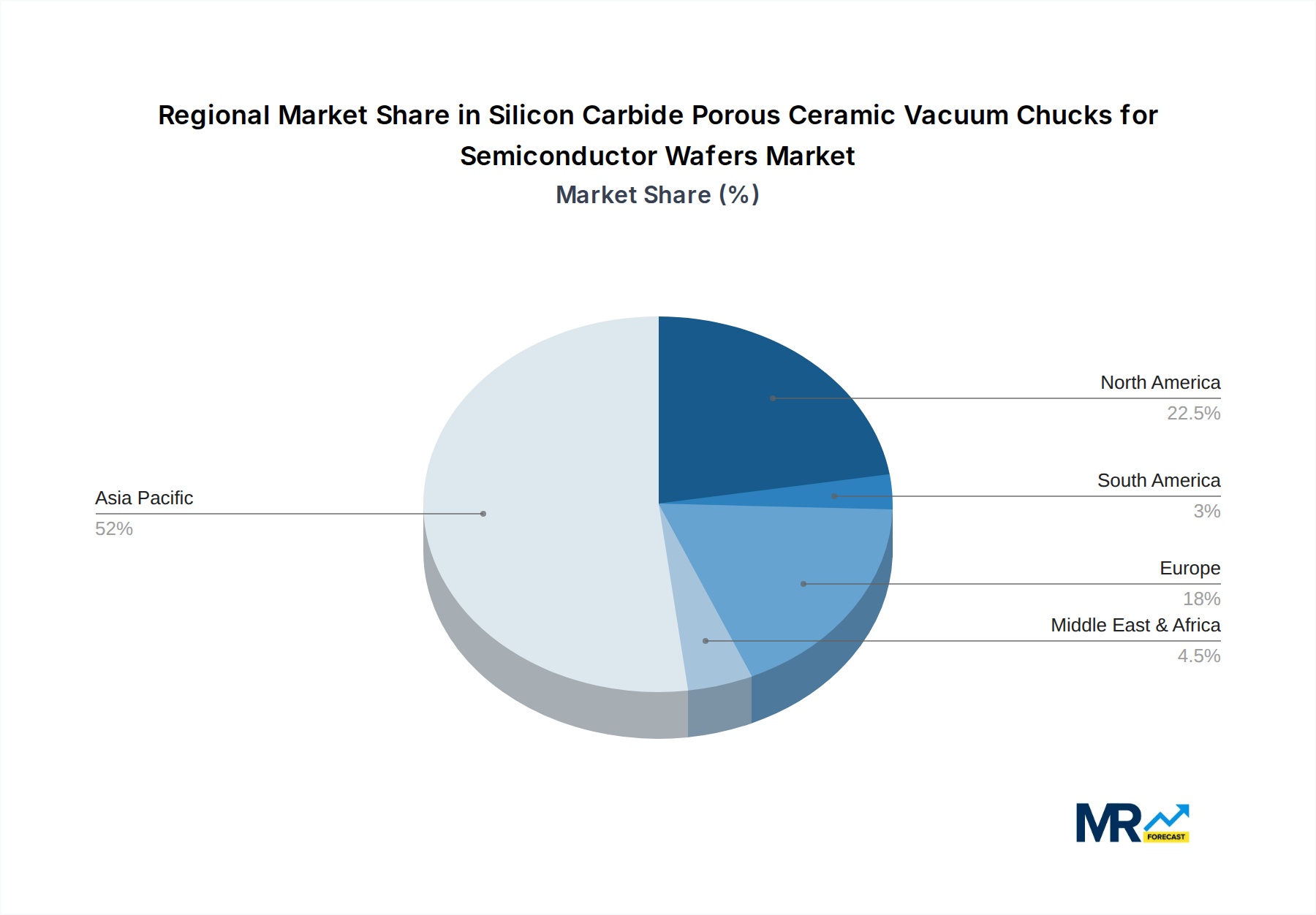

The market is segmented by wafer size, with 300 mm and 200 mm chucks dominating due to their prevalence in current wafer fabrication lines. The "Others" category, encompassing smaller wafer sizes and specialized applications, also presents growth opportunities. By application, Integrated Device Manufacturers (IDMs) and Foundries represent the largest consumer segments, directly benefiting from the enhanced precision and efficiency offered by these chucks. Semiconductor Equipment Suppliers are also crucial players, integrating these chucks into their advanced processing equipment. Geographically, Asia Pacific, led by China, Japan, and South Korea, is expected to remain the largest and fastest-growing market, owing to its significant concentration of semiconductor manufacturing hubs and ongoing capacity expansions. North America and Europe also contribute substantially, driven by technological advancements and a strong presence of key semiconductor players. Leading companies such as Kyocera, NTK CERATEC, and Tokyo Seimitsu are at the forefront of innovation, continuously developing higher-performance chucks to meet the evolving demands of the semiconductor industry.

Here's a unique report description for Silicon Carbide Porous Ceramic Vacuum Chucks for Semiconductor Wafers, incorporating your specific requests:

This comprehensive report delves into the dynamic global market for Silicon Carbide Porous Ceramic Vacuum Chucks, a critical component in advanced semiconductor manufacturing. Analyzing the market from a historical perspective (2019-2024) through to a robust forecast period (2025-2033), with a specific focus on the Base Year 2025, this study offers in-depth insights into market trends, driving forces, challenges, and future growth trajectories. The global market, valued in the tens of billions of dollars, is poised for significant expansion, driven by the relentless demand for miniaturization, increased processing power, and the proliferation of advanced semiconductor devices across various industries. Our analysis meticulously dissects the market by wafer diameter (300 mm, 200 mm, and Others) and application segments (IDM, Foundry, Semiconductor Equipment Suppliers), providing a granular understanding of regional dominance and segment-specific opportunities.

The global market for Silicon Carbide (SiC) Porous Ceramic Vacuum Chucks for semiconductor wafer handling is experiencing a transformative growth phase, projected to reach a substantial market size measured in the tens of billions of dollars by the end of the forecast period in 2033. This upward trajectory is underpinned by several key trends that are reshaping the semiconductor manufacturing landscape. Foremost among these is the escalating demand for high-performance computing, artificial intelligence, and the ever-expanding Internet of Things (IoT) ecosystem, all of which necessitate increasingly sophisticated and densely packed semiconductor chips. The push towards advanced nodes and smaller feature sizes in chip fabrication directly translates to a heightened requirement for vacuum chucks that offer unparalleled precision, uniformity, and stability during wafer processing steps like etching, deposition, and lithography. SiC's inherent properties – its high thermal conductivity, superior mechanical strength, low thermal expansion coefficient, and excellent chemical resistance – make it the material of choice, effectively mitigating wafer distortion and contamination, which are critical concerns in sub-10 nanometer manufacturing. Furthermore, the increasing adoption of larger wafer diameters, particularly the transition towards 300 mm wafers, amplifies the need for robust and precisely engineered chucks capable of handling these larger substrates with utmost accuracy. This trend is further fueled by the drive for increased manufacturing throughput and reduced per-wafer costs, making advanced chuck technology a fundamental enabler of economic efficiency in wafer fabrication. The market is also witnessing a growing emphasis on customization and specialization, with manufacturers developing chucks tailored for specific process steps and wafer types, thereby optimizing performance and yield. The ongoing research and development into novel porous SiC structures and advanced surface treatments are also contributing to the evolution of vacuum chuck technology, promising enhanced vacuum integrity, improved particle control, and extended product lifecycles. This confluence of technological advancements and market demand paints a picture of a robust and expanding market, crucial for the future of semiconductor innovation.

The robust growth of the Silicon Carbide Porous Ceramic Vacuum Chucks for Semiconductor Wafers market is being propelled by a confluence of powerful forces that are fundamentally reshaping the semiconductor industry. The relentless pursuit of advanced computing power, driven by the exponential growth in data generation and consumption for AI, machine learning, and big data analytics, is a primary catalyst. As semiconductor manufacturers strive to shrink feature sizes and increase transistor density, the demand for precision wafer handling solutions intensifies, making SiC porous ceramic chucks indispensable for their superior dimensional stability and minimal particle generation. The burgeoning adoption of 5G technology and the associated proliferation of connected devices, from smartphones to autonomous vehicles, further fuels the need for more advanced and specialized semiconductor chips, thereby driving demand for the high-performance chucks required in their fabrication. Moreover, the strategic importance of semiconductor manufacturing for national economies, leading to increased governmental investments and incentives in domestic production capabilities, is creating a favorable environment for market expansion. This includes the growing trend towards building new fabrication plants and expanding existing ones, especially for advanced nodes, which directly translates to a surge in the requirement for essential equipment components like SiC vacuum chucks. The increasing complexity of semiconductor device architectures, necessitating more intricate and precise manufacturing processes, also plays a significant role. SiC porous ceramic chucks, with their ability to maintain uniform temperature distribution and provide consistent vacuum holding force, are critical for ensuring the integrity and yield of these complex wafer processing steps.

Despite the overwhelmingly positive growth outlook, the Silicon Carbide Porous Ceramic Vacuum Chucks for Semiconductor Wafers market is not without its inherent challenges and restraints that warrant careful consideration. One of the most significant hurdles is the high cost of raw materials and manufacturing. Silicon carbide, while offering superior performance, is inherently more expensive to produce and process compared to traditional materials. The intricate porous structures required for effective vacuum chucks demand highly specialized manufacturing techniques, including advanced sintering and grinding processes, which contribute to the overall high price point. This cost factor can be a barrier for smaller manufacturers or for applications where cost optimization is paramount. Furthermore, the complex and specialized nature of the manufacturing process necessitates significant investment in specialized equipment and highly skilled labor, creating a high entry barrier for new players. The stringent quality control and assurance requirements in the semiconductor industry add another layer of complexity. Any deviation in material properties or surface finish can lead to catastrophic yield losses for wafer fabrication, demanding meticulous testing and validation at every stage of production. This can extend lead times and increase operational costs. Moreover, the evolving technological landscape presents a continuous challenge. As semiconductor manufacturing processes advance, there is an ongoing demand for chucks with even tighter tolerances, enhanced thermal management capabilities, and improved resistance to plasma etching environments. Manufacturers must constantly innovate and invest in R&D to keep pace with these evolving demands, which can strain resources. Finally, reliance on a limited number of specialized suppliers for raw materials and critical manufacturing technologies can create supply chain vulnerabilities and potential price volatility.

The global Silicon Carbide Porous Ceramic Vacuum Chucks for Semiconductor Wafers market is characterized by a significant concentration of demand and supply, with certain regions and segments standing out as dominant forces.

Dominant Regions and Countries:

Dominant Segments:

300 mm Wafer Diameter: The transition and widespread adoption of 300 mm wafers represent the single most significant segment driving the demand for SiC porous ceramic vacuum chucks.

Foundry Application Segment: The foundry segment is expected to be a major driver of growth.

In summary, the Asia-Pacific region, particularly its leading semiconductor manufacturing hubs, will dominate the market. Within segments, the shift towards 300 mm wafer diameters and the robust growth of the foundry application segment will be the primary engines of demand, directly influenced by the global imperative for advanced semiconductor fabrication.

Several key growth catalysts are accelerating the expansion of the Silicon Carbide Porous Ceramic Vacuum Chucks for Semiconductor Wafers market. The relentless innovation in semiconductor technology, leading to smaller and more powerful chips for AI, 5G, and IoT, creates an indispensable demand for the precision and stability offered by SiC chucks. Furthermore, the global drive towards supply chain resilience and national semiconductor independence is fueling significant investments in new fabrication facilities worldwide, directly boosting the need for these critical manufacturing components. The ongoing transition to larger wafer diameters, especially 300 mm, amplifies the requirement for advanced chucks capable of handling these substrates with unparalleled accuracy and uniformity.

This report offers an unparalleled and comprehensive analysis of the Silicon Carbide Porous Ceramic Vacuum Chucks for Semiconductor Wafers market, providing actionable intelligence for stakeholders. Beyond market sizing and forecasts, the study meticulously examines the intricate interplay of technological advancements, regulatory landscapes, and evolving supply chain dynamics. Our in-depth segmentation by wafer type (300 mm, 200 mm, Others) and application (IDM, Foundry, Semiconductor Equipment Suppliers) allows for a granular understanding of segment-specific growth drivers and challenges. Furthermore, the report identifies key emerging markets and niche applications, offering a forward-looking perspective on future opportunities. With a detailed exploration of competitive strategies and the strategic developments of leading players, this report equips businesses with the critical insights needed to navigate this complex and rapidly evolving multi-billion dollar industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.97% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 10.97%.

Key companies in the market include Kyocera, NTK CERATEC, Tokyo Seimitsu, KINIK Company, Cepheus Technology, Zhengzhou Research Institute for Abrasives & Grinding, SemiXicon, MACTECH, RPS Co., Ltd..

The market segments include Type, Application.

The market size is estimated to be USD 12.63 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in K.

Yes, the market keyword associated with the report is "Silicon Carbide Porous Ceramic Vacuum Chucks for Semiconductor Wafers," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Silicon Carbide Porous Ceramic Vacuum Chucks for Semiconductor Wafers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.