1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Outsourcing?

The projected CAGR is approximately XX%.

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

Semiconductor Outsourcing

Semiconductor OutsourcingSemiconductor Outsourcing by Type (Test, Encapsulation), by Application (Communication, Automobile, Computer, Consumer Electronics, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

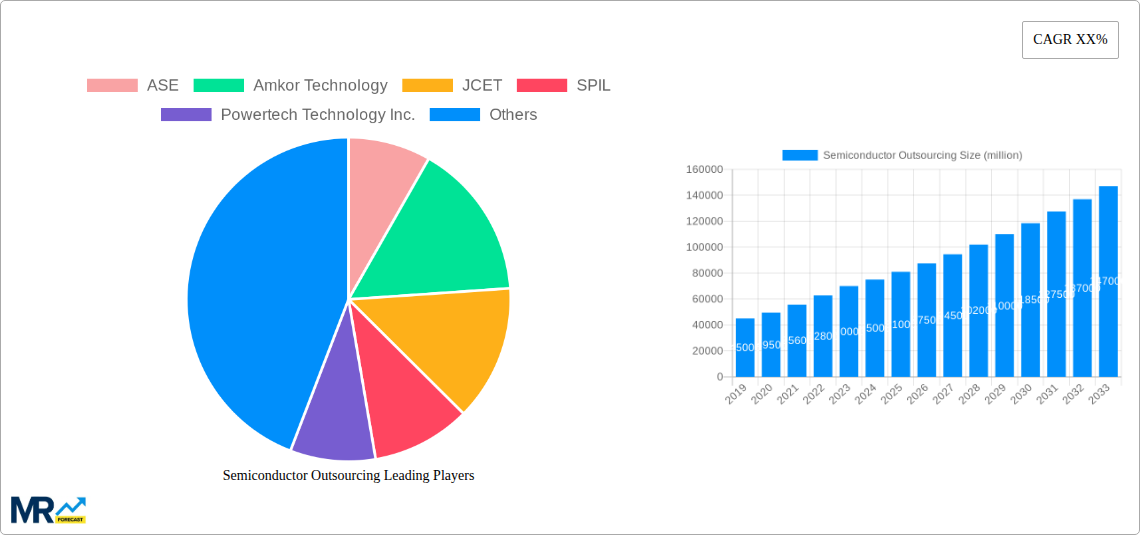

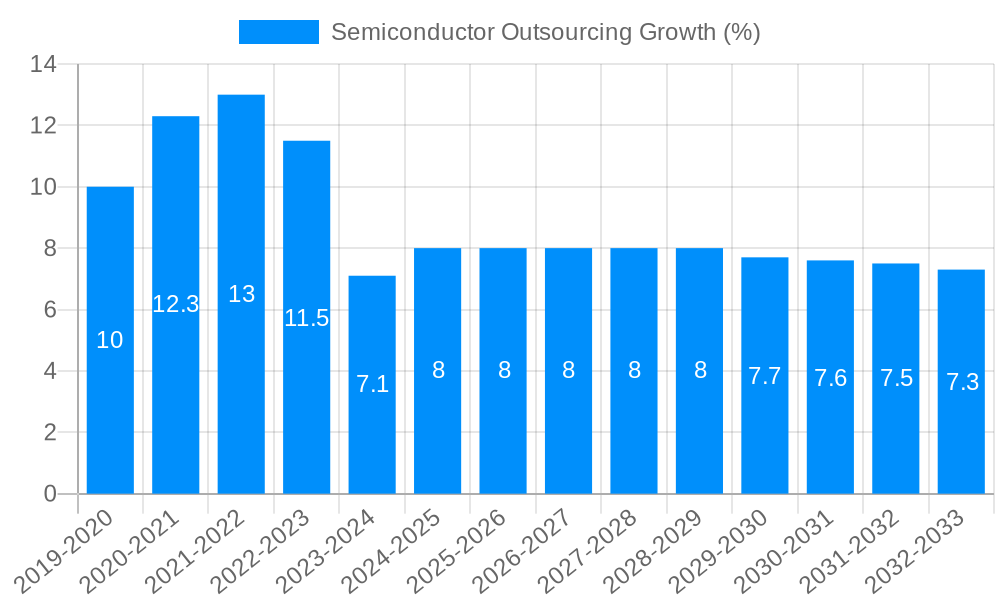

The semiconductor outsourcing market is poised for significant expansion, driven by the increasing complexity of chip design and manufacturing, coupled with the growing demand for advanced electronics across various sectors. With a projected market size of approximately $75 billion and a Compound Annual Growth Rate (CAGR) of around 12%, the industry is expected to reach a valuation of over $130 billion by 2033. This robust growth is primarily fueled by the insatiable demand from the communication sector, encompassing smartphones and 5G infrastructure, and the rapidly evolving automotive industry, with its increasing integration of sophisticated electronic components for autonomous driving and infotainment systems. The computer and consumer electronics segments also continue to be substantial contributors to market expansion. Furthermore, advancements in packaging technologies, such as advanced chip stacking and heterogeneous integration, are creating new opportunities for outsourced semiconductor assembly and testing (OSAT) providers to offer specialized solutions.

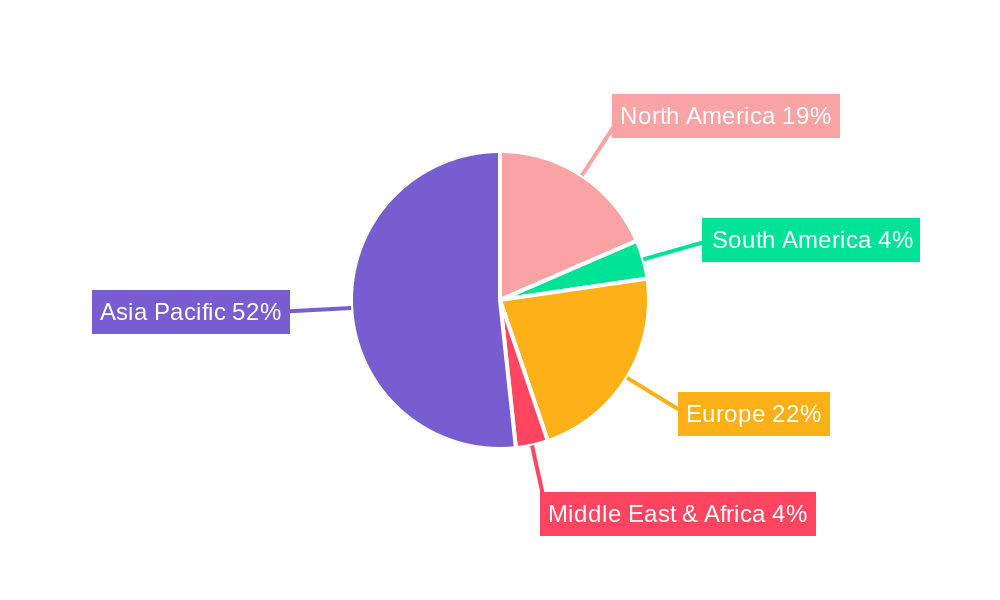

The market faces certain restraints, including escalating raw material costs and geopolitical tensions that can disrupt global supply chains. However, the relentless pursuit of innovation, miniaturization, and enhanced performance in semiconductors, coupled with the high capital expenditure required for in-house manufacturing, continues to propel companies towards outsourcing their fabrication and testing needs. Key players such as ASE, Amkor Technology, and JCET are strategically investing in advanced technologies and expanding their capacities to cater to this burgeoning demand. The Asia Pacific region, particularly China and South Korea, is expected to dominate the market due to the presence of major foundries and a strong ecosystem of semiconductor manufacturers and related industries, offering a competitive advantage in terms of cost-effectiveness and technological prowess.

Here's a unique report description on Semiconductor Outsourcing, incorporating your specified elements:

This comprehensive report delves into the dynamic and strategically vital world of semiconductor outsourcing, offering an in-depth analysis of market trends, growth drivers, and key players shaping the industry between 2019 and 2033. With a base year of 2025, the study meticulously examines the historical trajectory (2019-2024) and forecasts future market performance through 2033, providing actionable insights for stakeholders. The global semiconductor outsourcing market is projected to witness significant expansion, driven by increasing demand across diverse applications and a complex geopolitical landscape. Understanding the intricacies of outsourcing strategies, from advanced packaging and testing to specialized assembly, is paramount for companies seeking to optimize their supply chains, enhance innovation, and maintain competitive advantage. This report equips you with the knowledge to navigate these challenges and capitalize on emerging opportunities.

XXX report provides a panoramic view of the semiconductor outsourcing market, highlighting key insights and predicting its trajectory through 2033. The global market is witnessing a pronounced shift towards specialized outsourcing services, particularly in the advanced packaging and testing segments. As semiconductor complexity escalates and wafer fabrication capabilities become increasingly concentrated among a select few, foundries and fabless companies are leaning heavily on third-party providers for crucial post-fab processes. This trend is evidenced by the projected substantial growth in revenue for companies specializing in high-performance packaging solutions, such as wafer-level chip-scale packaging (WLCSP) and advanced 2.5D/3D integration, which are essential for next-generation processors powering AI, high-performance computing (HPC), and advanced automotive systems.

Furthermore, the report identifies a significant increase in outsourcing for high-volume, cost-sensitive applications, particularly within the consumer electronics and communication segments. While the total unit shipments for these segments remain robust, projected to reach hundreds of millions of units annually, the pressure to reduce costs and accelerate time-to-market is driving manufacturers to leverage the economies of scale and expertise offered by contract manufacturing organizations (CMOs). The geographical distribution of outsourcing activities is also undergoing transformation, with a continued dominance of Asia-Pacific, but with increasing attention on supply chain resilience and diversification strategies, potentially leading to new hubs of outsourcing activity. The integration of advanced testing methodologies, including AI-driven defect detection and yield optimization, is becoming a critical differentiator for outsourcing partners, further contributing to market growth. The report emphasizes that strategic partnerships and collaborative innovation between chip designers and outsource providers will be a defining characteristic of the market in the coming years, facilitating the development of cutting-edge semiconductor technologies. The market is on track to surpass billions of dollars in revenue, with specific segments like advanced testing and intricate packaging demonstrating annualized growth rates exceeding industry averages.

The semiconductor outsourcing market is experiencing robust growth fueled by a confluence of powerful drivers. Foremost among these is the ever-increasing complexity and miniaturization of semiconductor devices. As chips become more sophisticated, the capital investment required for advanced fabrication and testing equipment escalates dramatically. This makes it economically unfeasible for many companies, especially smaller fabless design houses and even some integrated device manufacturers (IDMs), to maintain in-house capabilities for every stage of production. Outsourcing allows them to access cutting-edge technology and expertise without incurring prohibitive upfront costs. Secondly, the accelerated pace of innovation in end-use applications, such as artificial intelligence, 5G communication, and autonomous driving, necessitates rapid development cycles and a flexible manufacturing infrastructure. Outsourcing partners offer the agility and scalability required to meet these demands, allowing companies to bring new products to market faster and respond effectively to evolving consumer needs. This is particularly evident in the Communication segment, where the demand for high-bandwidth, low-latency chips is driving rapid innovation and thus a reliance on specialized outsourcing capabilities.

Despite the significant growth, the semiconductor outsourcing market is not without its hurdles. A primary challenge revolves around intellectual property (IP) protection and data security. Entrusting sensitive chip designs and manufacturing processes to third-party vendors inherently carries risks. Ensuring robust security protocols and legal frameworks to safeguard proprietary information is paramount and requires significant due diligence from both outsourcing providers and their clients. Furthermore, geopolitical tensions and supply chain disruptions have emerged as significant restraints. The increasing focus on national security and economic sovereignty is leading to calls for localized production and diversification of supply chains, potentially impacting established outsourcing hubs. The COVID-19 pandemic highlighted the fragility of globalized supply chains, leading to production halts and increased lead times, which can significantly impact the reliability of outsourced manufacturing.

The semiconductor outsourcing market exhibits distinct regional strengths and segment dominance, driven by factors such as specialized infrastructure, skilled labor availability, and government support.

Asia-Pacific Dominance: This region is the undisputed powerhouse of semiconductor outsourcing, primarily driven by the robust capabilities of countries like Taiwan, South Korea, China, and Singapore.

Dominant Segment: Packaging and Testing: Within the semiconductor outsourcing landscape, the Packaging and Testing (OSAT) segments are by far the most dominant and are expected to continue their ascendancy.

The synergy between the Asia-Pacific region's manufacturing prowess and the critical need for specialized packaging and testing services underscores their joint dominance in the global semiconductor outsourcing market.

The semiconductor outsourcing industry is poised for sustained growth, propelled by several key catalysts. The accelerating demand for specialized chips in rapidly evolving sectors like Artificial Intelligence (AI), 5G, and the Internet of Things (IoT) necessitates access to advanced manufacturing and testing capabilities that many companies cannot afford to develop in-house. Furthermore, the growing trend towards chiplet architectures and heterogeneous integration, where multiple smaller dies are packaged together, heavily relies on the sophisticated packaging expertise of outsourcing partners. Government initiatives and investments aimed at bolstering domestic semiconductor supply chains, while creating some regional shifts, also indirectly fuel outsourcing by fostering innovation and the development of new manufacturing hubs.

This report offers a holistic view of the semiconductor outsourcing market, moving beyond a simple market size estimation to provide a deep dive into the underlying dynamics. It meticulously analyzes the historical performance of key players like ASE and Amkor Technology, examining their contributions to segments such as Test and Encapsulation for critical applications like Communication, Automobile, and Computer. The report identifies granular trends, such as the increasing average selling price per unit for advanced packaging solutions and the growing operational efficiency achieved through AI-driven testing protocols. It also explores the strategic implications of industry developments, including advancements in chiplet integration and the impact of government policies on manufacturing hubs. This comprehensive coverage equips businesses with the strategic foresight to navigate the complexities and capitalize on the significant growth opportunities present in the semiconductor outsourcing landscape through 2033.

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include ASE, Amkor Technology, JCET, SPIL, Powertech Technology Inc., TongFu Microelectronics, Tianshui Huatian Technology, UTAC, Chipbond Technology, Hana Micron, OSE, Walton Advanced Engineering, NEPES, Unisem, ChipMOS Technologies, Signetics, Carsem, KYEC.

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Semiconductor Outsourcing," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Semiconductor Outsourcing, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.