1. What is the projected Compound Annual Growth Rate (CAGR) of the Satellite Pay TV?

The projected CAGR is approximately XX%.

Satellite Pay TV

Satellite Pay TVSatellite Pay TV by Type (190 ~ 239 Channels, 240 ~ 289 Channels, ≥ 290 Channels), by Application (Residential, Commercial), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

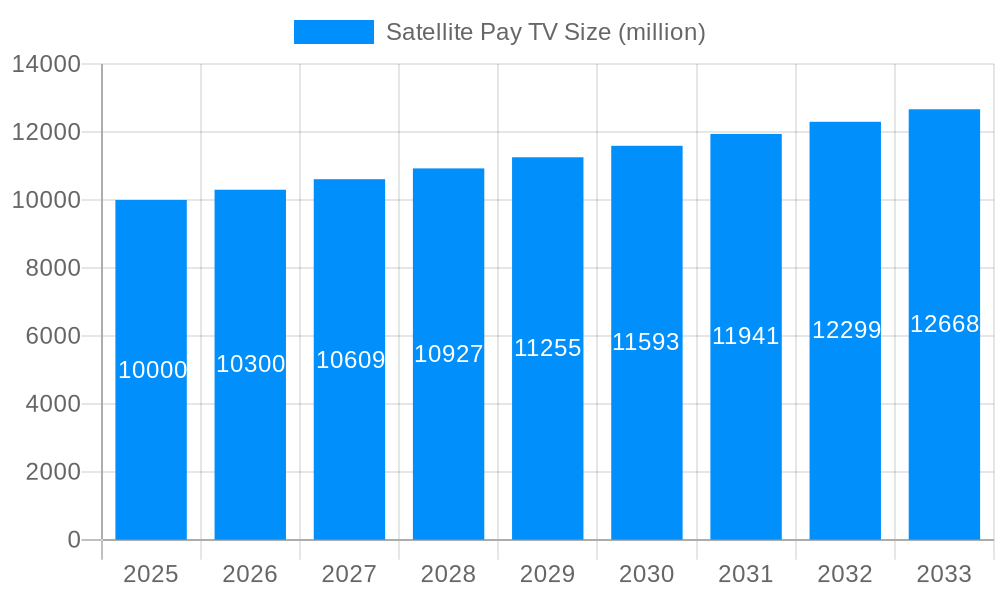

The global satellite pay TV market is a mature yet dynamic industry, exhibiting a complex interplay of growth drivers and restraining factors. While the market faces challenges from the rise of streaming services and cord-cutting, it continues to maintain a significant presence, particularly in regions with limited broadband infrastructure or a preference for high-quality broadcast television. The market's segmentation by channel count (190-239, 240-289, ≥290) reflects varying consumer preferences and pricing strategies, indicating a tiered approach to service offerings. Similarly, the application-based segmentation (residential vs. commercial) highlights distinct market needs and revenue streams. Growth is expected to be driven by increasing demand for premium content, particularly sports and entertainment packages, as well as ongoing investments in high-definition and 4K satellite technology. However, the market faces considerable restraints, including increasing competition from over-the-top (OTT) platforms offering on-demand content and the high cost of satellite infrastructure and maintenance. Regional variations are also substantial, with North America and Asia Pacific expected to be key contributors to market growth, while other regions might show more moderate expansion. Given the maturity of the market, a conservative Compound Annual Growth Rate (CAGR) of 3-4% over the forecast period (2025-2033) appears realistic, considering the competitive landscape and technological advancements.

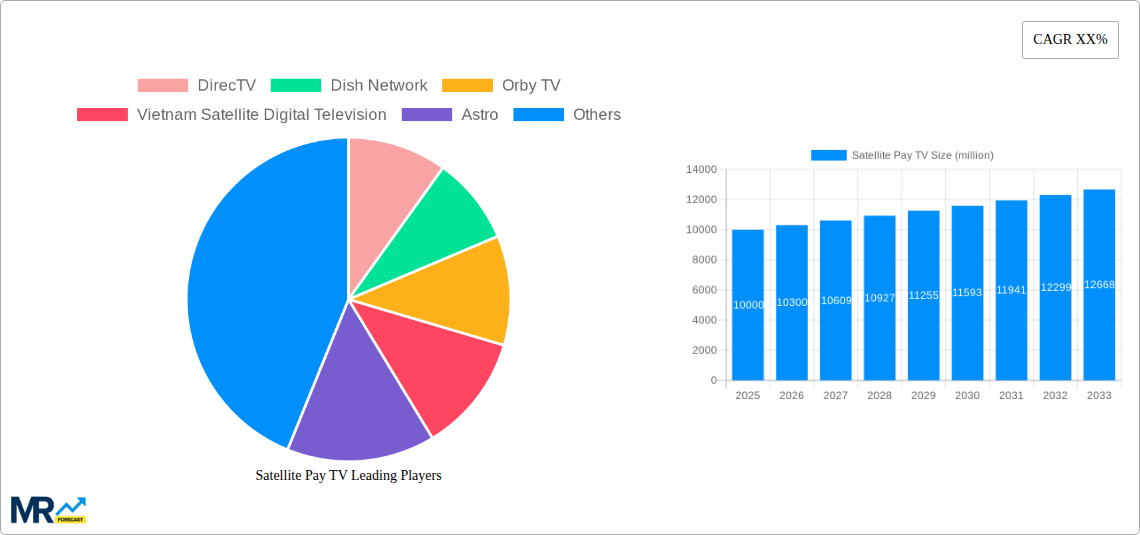

The competitive landscape is characterized by a mix of established global players like DirecTV and Dish Network and regional operators catering to specific markets. Successful companies are adapting to changing consumer preferences by offering bundled packages, integrating streaming services, and focusing on niche programming. The increasing availability of high-speed internet in developing economies poses a significant long-term threat; however, the enduring appeal of satellite TV's reliability and high-quality picture, especially in areas with poor internet penetration, ensures its continued relevance for a considerable segment of the population. Strategic partnerships and mergers & acquisitions are likely to shape the future of the industry, as companies seek to expand their reach and consolidate market share. The focus will likely shift towards offering flexible and cost-effective packages combined with complementary streaming services to remain competitive.

The global satellite pay TV market, encompassing giants like DirecTV and Dish Network alongside regional players such as Astro and Telkomvision, is undergoing a period of significant transformation. While the historical period (2019-2024) witnessed a decline in subscriptions driven by the rise of streaming services, the market exhibits resilience and a nuanced evolution, not a complete collapse. The estimated market size in 2025 sits at a substantial value, indicating continued relevance despite challenges. The forecast period (2025-2033) suggests a moderate growth trajectory, fueled by factors including improved satellite technology, targeted programming packages, and continued penetration in underserved regions. The shift is less about complete market shrinkage and more about a strategic adaptation. Providers are now focused on niche offerings, tailoring packages to specific demographics and incorporating interactive features to maintain a competitive edge against streaming platforms. This strategic shift is reflected in the varying channel package offerings: the market shows a steady demand for packages across all channel ranges (190-239, 240-289, and ≥290 channels), indicating consumer preferences for diverse content choices. The residential sector remains the dominant application, but the commercial sector shows promising growth, particularly in areas requiring reliable and widespread signal coverage. This suggests that satellite pay TV's future lies not in direct competition with streaming giants but in occupying a unique space defined by reliable, widespread coverage and carefully curated content strategies. The interplay between these factors will shape the industry's landscape over the coming decade.

Several key factors are driving the continued relevance of the satellite pay TV market despite the rise of streaming services. Firstly, superior reach and reliability in remote or underserved areas remain a significant advantage. Satellite technology provides consistent coverage where terrestrial or fiber-optic infrastructure is limited or nonexistent, ensuring access to television for a wide range of consumers, particularly in developing nations. Secondly, the introduction of high-definition (HD) and Ultra-High Definition (UHD) channels, along with improved picture quality and sound, continues to be a significant draw. Thirdly, bundled packages that include internet services are becoming increasingly common, offering a compelling value proposition for consumers. Fourthly, the ongoing investment in advanced satellite technology, offering better signal strength and higher bandwidth capacities, is enabling providers to enhance their services and deliver a more competitive product. Finally, the strategic shift toward customized content packages catering to specific consumer needs and preferences is proving effective in retaining and attracting subscribers, offering tailored content to niche audiences that streaming platforms may not fully cater to.

The satellite pay TV industry faces significant headwinds. The most prominent is the intense competition from over-the-top (OTT) streaming services such as Netflix, Hulu, and Disney+. These platforms offer consumers a wide range of content at a potentially lower price point with greater flexibility, impacting subscriber numbers significantly. Another major challenge is the high initial capital expenditure required for infrastructure development and maintenance. Satellite technology requires considerable investment in satellites, ground stations, and broadcasting equipment. Furthermore, regulatory hurdles and licensing requirements in different countries can create barriers to entry and operational complexities. The evolving technological landscape also presents a challenge: staying ahead of the curve in terms of technology upgrades and delivering an experience that competes with the user interface and convenience of streaming platforms is crucial for survival. Finally, piracy and content theft remain persistent threats to the industry, impacting revenue streams and threatening long-term viability.

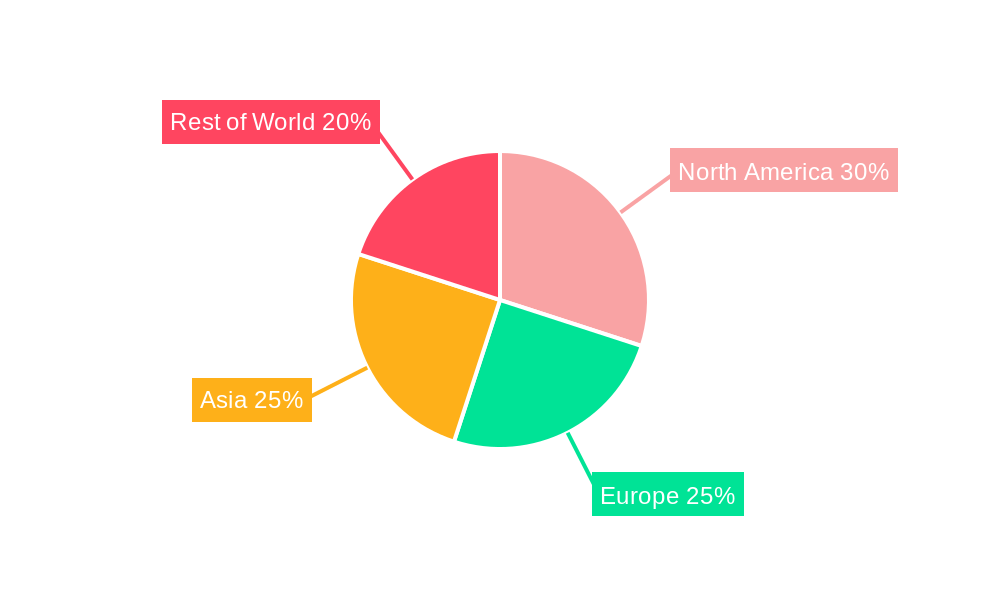

The market is characterized by regional variations in growth and market share. While specific market share data for each company across regions is not publicly available in a consolidated format, some insights can be gleaned:

Asia-Pacific: This region is expected to exhibit significant growth due to increasing urbanization, rising disposable incomes, and expanding digital infrastructure in developing countries. Companies like Astro (Malaysia), Telkomvision (Indonesia), and PT MNC Sky Vision Tbk (Indonesia) are key players in this region, benefiting from high demand and market penetration strategies. Within this region, the residential segment dominates, with a higher concentration of users in areas with limited terrestrial internet access. The high channel count packages (≥290 channels) are showing strong growth as consumers in this market seek diverse programming choices.

North America: While mature, the North American market continues to be a substantial contributor due to the presence of major players like DirecTV and Dish Network. While facing pressure from OTT services, these companies are implementing strategies to retain their subscriber base. The market here demonstrates a balanced demand across all channel count segments, highlighting the diversity of consumer preferences. The residential segment remains dominant.

Segments: The residential segment will continue to hold the largest market share throughout the forecast period. However, the commercial segment is poised for growth, driven by the demand for reliable and high-quality television services in various commercial settings, such as hotels, restaurants, and businesses. The type of package is highly correlated with this; we anticipate 240-289 channel packages will gain traction in the commercial segment due to their balance of content and cost-effectiveness.

In summary: While overall market growth might be moderate, specific regions and segments are demonstrating stronger performance. Asia-Pacific shows particularly strong potential for growth, fueled by expanding infrastructure and rising disposable incomes, specifically favoring high channel count packages within the residential segment.

The satellite pay TV industry is finding new avenues for growth through strategic diversification. Bundling satellite TV with high-speed internet services creates a compelling value proposition for consumers. Investing in advanced technology, such as 4K UHD channels and interactive features, enhances the viewer experience and helps in retaining subscribers. Finally, focusing on targeted content packages based on demographics and preferences, improves customer satisfaction and fosters loyalty. This strategic adaptation ensures continued relevance in a competitive market.

This report provides a comprehensive overview of the satellite pay TV market, analyzing historical trends, current market dynamics, and future growth prospects. It offers in-depth insights into key players, regional variations, and emerging technologies, providing valuable information for industry stakeholders seeking to navigate this evolving landscape. The report's detailed segmentation and forecasting provide a clear understanding of the market's trajectory and opportunities for growth.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include DirecTV, Dish Network, Orby TV, Vietnam Satellite Digital Television, Astro, Skynindo, Telkomvision, PT MNC Sky Vision Tbk, Next Step, LAOSAT, Sky Net, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Satellite Pay TV," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Satellite Pay TV, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.