1. What is the projected Compound Annual Growth Rate (CAGR) of the Satellite Operation Service?

The projected CAGR is approximately 10.7%.

Satellite Operation Service

Satellite Operation ServiceSatellite Operation Service by Type (Consumer Services, Fixed Satellite Services, Mobile Satellite Services, Remote Sensing, Space Flight Management Services, Others), by Application (Media & Entertainment, Government, Aviation, Defense, Aerospace, Retail & Enterprise, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

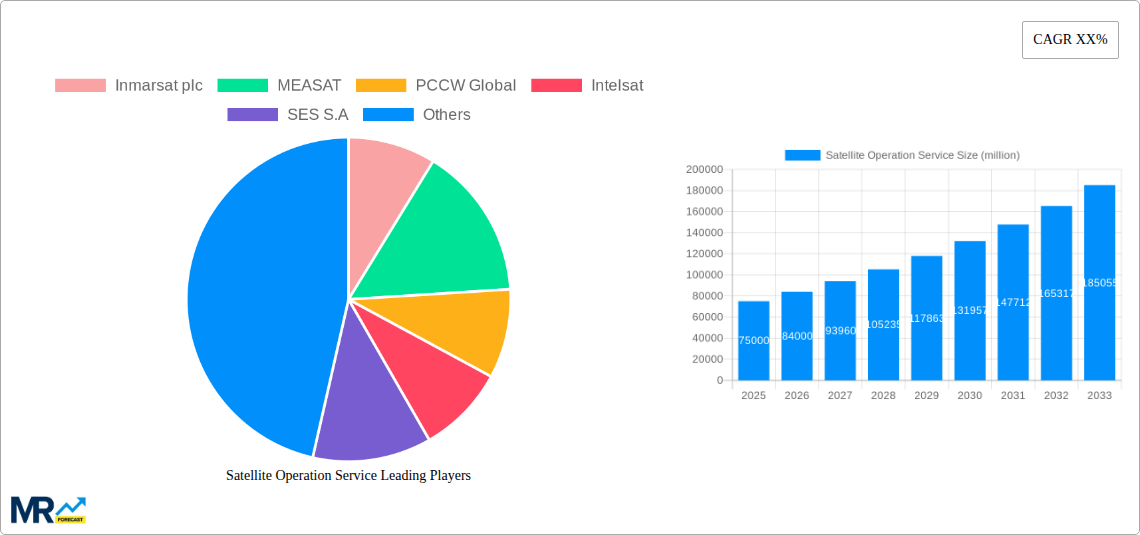

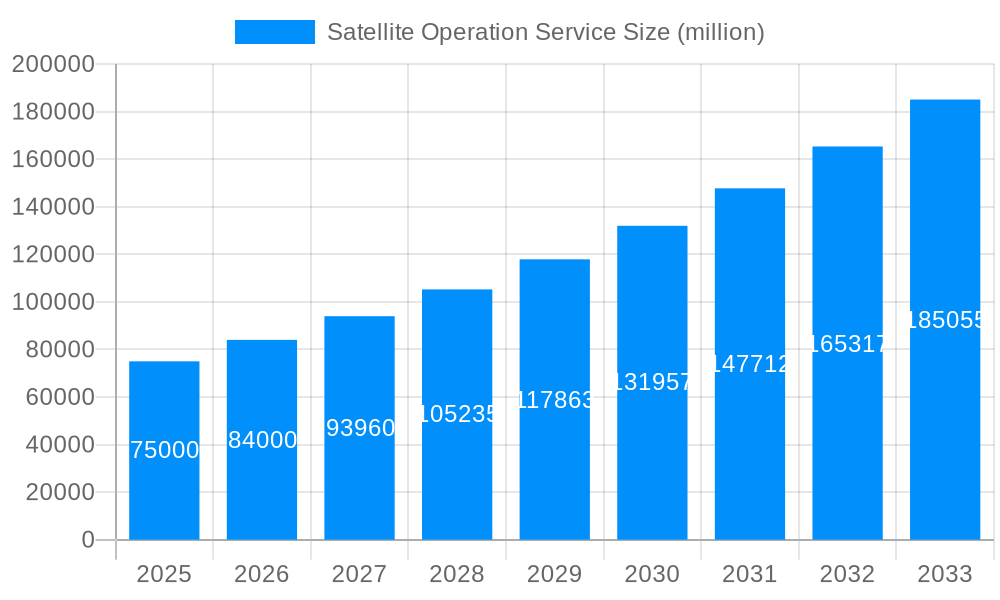

The global Satellite Operation Services market is projected for substantial growth, reaching an estimated $32.79 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 10.7% from 2025 to 2033. This expansion is driven by increasing demand for reliable connectivity in remote locations, the growing adoption of satellite services across industries such as media, government, and aviation, and continuous technological advancements in remote sensing and space flight management. Key factors include the reliance on satellite communication for critical applications like disaster management, broadcasting, and secure government communications, alongside the growth of satellite constellations providing broadband internet services.

The market features dynamic segments and key players. Consumer Services and Fixed Satellite Services are expected to maintain dominance, while Mobile Satellite Services are experiencing accelerated growth due to the proliferation of connected devices and the need for ubiquitous communication. Leading companies such as Inmarsat plc, Intelsat, and SES S.A. are investing in research and development and strategic partnerships. The Asia Pacific region is anticipated to be a significant growth market, driven by economic development and increasing digital penetration, complementing established markets in North America and Europe. Emerging trends like Low Earth Orbit (LEO) satellites and AI integration in satellite operations will further shape market dynamics.

This report offers an in-depth analysis of Satellite Operation Services, covering market trends, growth drivers, challenges, and future outlook. The study spans from 2019 to 2033, with a base year of 2025. The forecast period of 2025-2033 builds upon the historical data from 2019-2024, providing a comprehensive outlook. The global market is expected to show significant revenue growth, reflecting increased investments and technological advancements.

XXX The Satellite Operation Service market is poised for a significant surge, projected to reach an estimated value of USD 35 million by the estimated year of 2025. This growth trajectory is underpinned by a confluence of factors, most notably the escalating demand for high-speed, reliable connectivity across diverse applications, from consumer services to critical government and defense operations. The proliferation of remote sensing technologies, driven by applications in environmental monitoring, agriculture, and disaster management, is also a key trend shaping the market. Furthermore, the increasing adoption of satellite services by the aviation and maritime sectors for enhanced communication and navigation is contributing to market expansion. Fixed Satellite Services (FSS) continue to be a dominant segment, catering to broadcasting, broadband internet, and enterprise networking needs. However, the Mobile Satellite Services (MSS) segment is witnessing accelerated growth, fueled by the demand for ubiquitous connectivity for mobile platforms, including vehicles, ships, and even personal devices in underserved regions. The market is also observing a rising interest in specialized services such as Space Flight Management Services, driven by the burgeoning space economy and the increasing number of satellite launches. Innovations in satellite technology, including the development of Low Earth Orbit (LEO) constellations, are democratizing access to space-based services and fostering a more competitive market landscape. This evolution presents new opportunities for service providers to offer more agile, cost-effective, and high-performance solutions, thereby driving overall market value. The integration of artificial intelligence and machine learning in satellite operations for enhanced data analysis and predictive maintenance is another emerging trend that will redefine the efficiency and capabilities of satellite services. The report anticipates that the synergy between these trends will translate into sustained revenue growth throughout the forecast period, reaching an estimated USD 72 million by 2033. The increasing reliance on space-based infrastructure for global communication and data dissemination, coupled with governmental and private sector investments in satellite technology, solidifies the optimistic outlook for this vital sector.

The satellite operation service market is being propelled by a powerful combination of technological advancements and evolving global demands. The relentless pursuit of enhanced connectivity, especially in areas with limited terrestrial infrastructure, remains a primary driver. This includes the ever-growing need for broadband internet access for consumers and businesses, as well as specialized communication solutions for remote operations. The expansion of the Internet of Things (IoT) ecosystem further fuels this demand, with a growing number of devices relying on satellite networks for data transmission and remote management. Furthermore, the increasing digitization of industries, from agriculture to logistics, necessitates robust and reliable data collection and dissemination capabilities, which satellites are uniquely positioned to provide. The burgeoning space economy, characterized by an increase in satellite launches for various purposes, including scientific research, national security, and commercial ventures, directly translates into a greater need for sophisticated satellite operation and management services. Governments worldwide are also significantly investing in satellite capabilities for national security, defense, and critical infrastructure monitoring, creating a substantial and consistent demand for these services. The growing adoption of satellite technology in the aviation and maritime sectors for enhanced safety, navigation, and passenger connectivity is another significant growth propeller. This multifaceted demand landscape, coupled with ongoing innovation in satellite technology, is creating a fertile ground for the expansion of the satellite operation service market.

Despite the robust growth trajectory, the satellite operation service market is not without its hurdles. One of the primary challenges is the substantial capital investment required for satellite development, launch, and ongoing operations. The high upfront costs can be a significant barrier to entry for new players and a constraint on the scale of operations for existing ones. Regulatory complexities and the fragmentation of regulations across different countries can also pose challenges for global service providers, leading to increased compliance costs and operational complexities. The increasing congestion of orbital space and the growing threat of space debris present significant long-term challenges, necessitating responsible satellite deployment and debris mitigation strategies. Furthermore, the competitive landscape, with the emergence of numerous LEO constellation providers, is intensifying price pressures and demanding greater service differentiation. Cybersecurity threats are also a growing concern, as satellite systems are critical infrastructure that can be targeted by malicious actors, requiring robust security measures to protect sensitive data and ensure operational integrity. The dependence on launch service providers and the associated risks of launch failures can also impact service continuity and project timelines. Finally, the development and adoption of new technologies, while driving growth, also necessitate continuous investment in research and development and workforce training, which can be a considerable undertaking for some market participants.

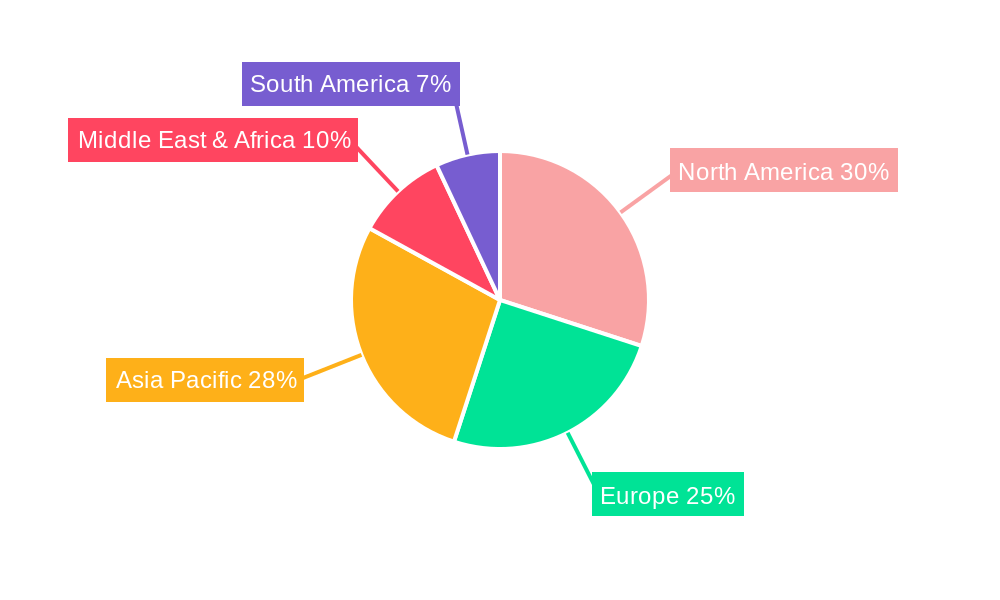

The global Satellite Operation Service market is characterized by the dominance of specific regions and segments, driven by unique demand drivers and technological adoption rates.

Dominant Region: North America

Dominant Segment: Fixed Satellite Services (FSS)

The Satellite Operation Service industry is experiencing robust growth driven by several key catalysts. The increasing demand for ubiquitous connectivity, particularly in remote and underserved regions, is a primary driver. Advancements in satellite technology, such as the development of Low Earth Orbit (LEO) constellations, are lowering latency and increasing bandwidth, making satellite services more competitive. The expanding use of satellite data for applications like remote sensing, Earth observation, and precision agriculture is creating new revenue streams. Furthermore, significant government investments in defense, national security, and scientific research are bolstering the market.

This report offers a comprehensive examination of the Satellite Operation Service market, providing a detailed outlook on its evolution and potential. It meticulously analyzes market trends, identifies key driving forces, and articulates the challenges and restraints that shape the industry landscape. The report details the dominant regions and segments, offering insights into their growth drivers and market share. Furthermore, it highlights the critical growth catalysts and profiles the leading players in this dynamic sector. With an in-depth look at significant developments and a projected market valuation expected to reach USD 72 million by 2033, this report serves as an indispensable resource for understanding the current state and future trajectory of the satellite operation service industry.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.7% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 10.7%.

Key companies in the market include Inmarsat plc, MEASAT, PCCW Global, Intelsat, SES S.A, Eutelsat Communications SA, Viasat, Inc, Echostar Corporation China Satellite Communications Co., Ltd, Thaicom Public Company Limited, Thuraya Telecommunications Company, Asia Satellite Telecommunications Co. Ltd, Vista, Spacecom International, Thaicom Public Compay Limited, .

The market segments include Type, Application.

The market size is estimated to be USD 32.79 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Satellite Operation Service," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Satellite Operation Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.