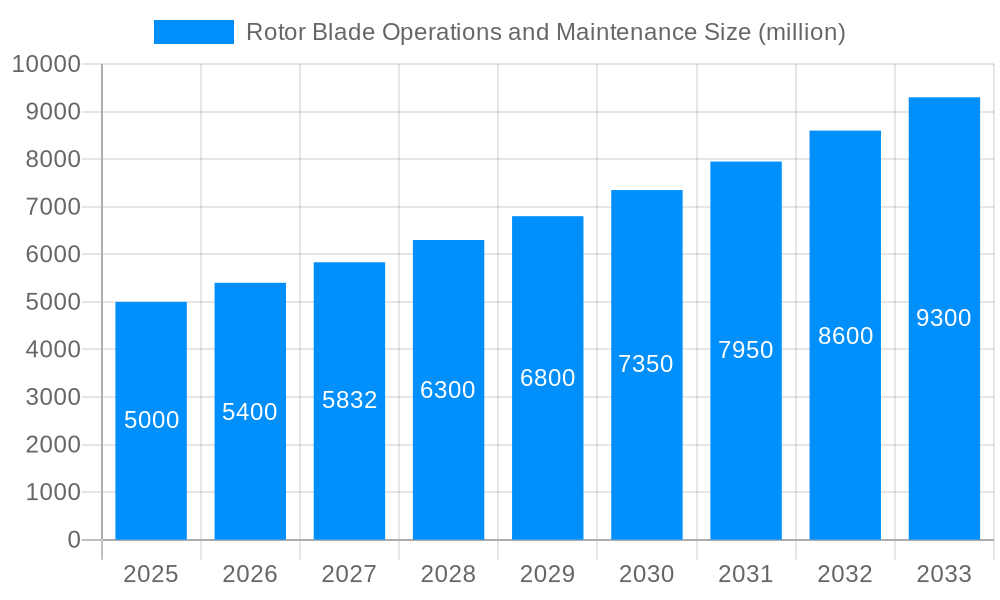

1. What is the projected Compound Annual Growth Rate (CAGR) of the Rotor Blade Operations and Maintenance?

The projected CAGR is approximately 10.67%.

Rotor Blade Operations and Maintenance

Rotor Blade Operations and MaintenanceRotor Blade Operations and Maintenance by Type (Recurring Inspections, Short Notice), by Application (Onshore Wind, Offshore Wind), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

The global Rotor Blade Operations and Maintenance (O&M) market is poised for significant expansion, driven by the burgeoning renewable energy sector and the aging fleet of wind turbine installations. The market is projected to reach $11.94 billion by 2025, demonstrating substantial growth. A Compound Annual Growth Rate (CAGR) of 10.67% is anticipated from 2025 to 2033, fueled by increasing global demand for renewable energy, supportive government initiatives, and policy frameworks. Technological advancements in O&M, including predictive maintenance and remote monitoring, are enhancing operational efficiency and minimizing downtime. Recurring inspections represent a key market segment, emphasizing the critical need for continuous monitoring to ensure asset reliability and longevity. While onshore wind currently leads in applications, the offshore wind sector is experiencing rapid growth due to increasing offshore wind farm deployments worldwide. Major market participants such as Vestas, Siemens Gamesa, and GE Renewable Energy are actively investing in innovative O&M solutions and expanding their service offerings to leverage this expanding market opportunity.

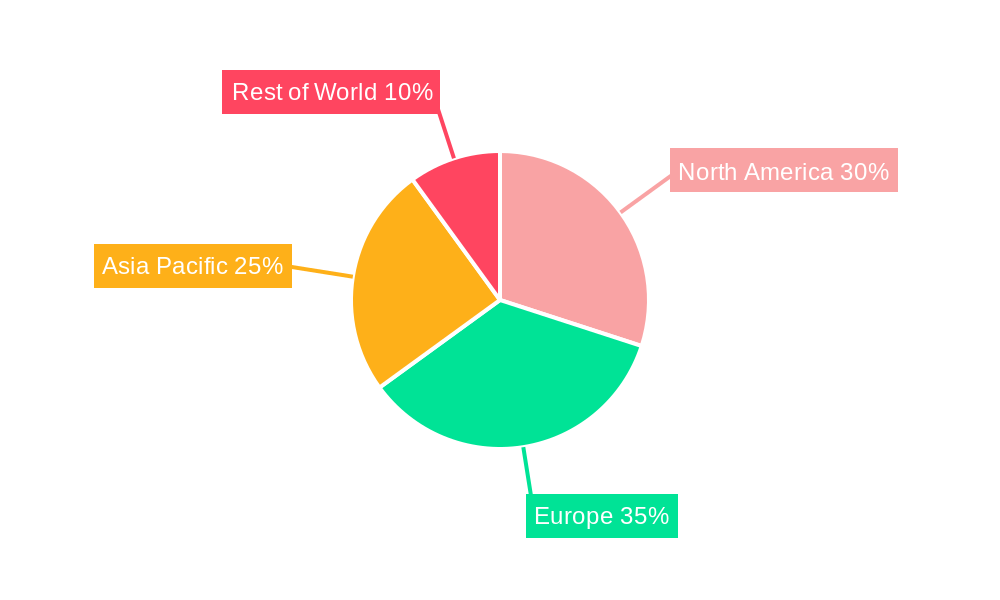

The competitive environment features established industry leaders and specialized O&M service providers. Turbine manufacturers typically provide integrated O&M services, capitalizing on their in-depth knowledge of turbine technology. Independent O&M providers concentrate on offering comprehensive services across diverse turbine brands and technologies. Market growth is further influenced by rising repair expenses, stringent safety regulations, and the demand for skilled personnel. Regional market shares are currently led by North America and Europe. However, the Asia-Pacific region is expected to experience accelerated growth in the forthcoming years, driven by rapid wind energy project development in countries like China and India. This growth trajectory will be shaped by continuous technological innovation, evolving regulatory landscapes, and the overall progression of the wind energy industry.

The global rotor blade operations and maintenance market is experiencing significant growth, projected to reach XXX million units by 2033. Driven by the burgeoning renewable energy sector and a global push towards carbon neutrality, the demand for efficient and reliable wind turbine maintenance is soaring. The historical period (2019-2024) witnessed a steady increase in market size, setting the stage for robust expansion during the forecast period (2025-2033). This growth is fueled by several factors, including the increasing age of existing wind turbines, technological advancements in blade inspection and repair techniques, and the emergence of specialized service providers. The base year of 2025 shows a substantial market value, highlighting the current momentum. Key market insights reveal a strong preference for recurring inspection services, particularly within the onshore wind segment, driven by cost-effectiveness and preventative maintenance strategies. However, the offshore wind sector is also exhibiting rapid growth, demanding specialized expertise and equipment to address the unique challenges posed by the marine environment. This necessitates significant investment in advanced technologies, including drones and AI-powered predictive maintenance tools. The competitive landscape is characterized by a mix of established original equipment manufacturers (OEMs) and specialized independent service providers, each vying for market share through innovation and service differentiation. The estimated year 2025 demonstrates a pivotal point in the market's trajectory, reflecting the maturing of the wind energy industry and the increasing importance of optimized operational efficiency. Further market segmentation analysis reveals significant variations in maintenance requirements across different blade designs and turbine models, leading to a complex yet lucrative market landscape.

Several key factors are propelling the growth of the rotor blade operations and maintenance market. The ever-increasing global demand for renewable energy sources is a primary driver, with wind power playing a crucial role in the energy transition. As the installed base of wind turbines expands exponentially, the need for robust maintenance and repair services increases proportionally. This is further amplified by the aging infrastructure of some earlier wind farms, demanding more frequent and extensive maintenance interventions. Technological advancements, such as advanced inspection techniques (drones, lidar, infrared thermography) and predictive maintenance algorithms using data analytics, are improving the efficiency and effectiveness of maintenance operations, ultimately reducing downtime and maximizing energy output. Furthermore, stringent regulatory frameworks and insurance requirements are pushing operators to prioritize comprehensive maintenance programs to ensure safety and compliance. The development of specialized service providers, offering niche expertise in specific areas like blade repair and refurbishment, also contributes to market expansion. Finally, the increasing adoption of larger and more complex wind turbine designs further complicates maintenance, requiring specialized skills and leading to increased demand for skilled technicians and specialized equipment.

Despite the substantial growth opportunities, the rotor blade operations and maintenance market faces several challenges. The harsh operating environment of offshore wind farms presents significant logistical and cost hurdles, impacting accessibility for inspections and repairs. The remoteness and challenging weather conditions can lead to delays and increased expenses. The specialized skills required for advanced maintenance and repair techniques pose a significant human resource challenge, resulting in a shortage of qualified technicians and potentially leading to increased labor costs. Moreover, the unpredictable nature of blade damage and the complexity of repair procedures create uncertainties in cost estimations and scheduling. Furthermore, the high capital investment required for advanced inspection and repair technologies can pose an entry barrier for smaller service providers. The need for constant technological adaptation to keep pace with evolving turbine designs and materials also adds to the operational and financial challenges faced by companies in this sector. Finally, maintaining a balance between cost-effective maintenance and ensuring optimal turbine performance remains a constant challenge for wind farm operators.

The onshore wind segment is currently the dominant segment within the rotor blade operations and maintenance market, primarily due to the higher number of existing onshore wind farms compared to offshore. However, the offshore wind sector is exhibiting exponential growth, with substantial potential for future expansion, driven by government support and favorable policy frameworks.

Onshore Wind: This segment benefits from relative accessibility and lower logistical challenges compared to its offshore counterpart. Recurring inspections are a dominant service type, driven by proactive maintenance strategies that maximize uptime. Regions like Europe and North America currently hold significant market share, with strong growth potential in emerging markets in Asia and Latin America. The established presence of major wind turbine manufacturers and a robust network of service providers further contribute to the onshore market's dominance. However, the increasing size and complexity of onshore wind turbines is gradually introducing challenges akin to those seen in the offshore sector.

Recurring Inspections: This service type is crucial for preventative maintenance, detecting potential problems before they escalate into major failures. The high frequency of these inspections contributes to a substantial portion of the overall market revenue. Recurring inspections provide valuable data for predictive maintenance models, enabling more efficient resource allocation and minimized downtime. This proactive approach is increasingly valued by wind farm operators, justifying the higher recurring costs.

Key Regions: Europe and North America continue to lead the market, with their mature wind energy sectors and existing infrastructure. However, significant growth is anticipated in Asia-Pacific, particularly in China and India, driven by rapid expansion of renewable energy projects.

The industry is experiencing robust growth fueled by a confluence of factors. The expansion of renewable energy initiatives globally, coupled with the aging of existing wind turbine fleets, necessitates increased maintenance activities. Technological innovations like advanced sensor technologies, predictive analytics, and drone-based inspections are enhancing the efficiency and effectiveness of maintenance operations. This improved efficiency reduces downtime, optimizes maintenance schedules, and ultimately increases the lifespan and profitability of wind farms. Furthermore, stringent environmental regulations and safety standards incentivize proactive maintenance practices, driving demand for sophisticated maintenance services.

This report provides a comprehensive analysis of the rotor blade operations and maintenance market, covering historical trends, current market dynamics, and future growth projections. It offers valuable insights into key market drivers, challenges, and growth opportunities, enabling stakeholders to make informed strategic decisions. The report also features detailed profiles of leading market players, providing an in-depth understanding of the competitive landscape. The information presented is based on rigorous market research and data analysis, ensuring accuracy and reliability.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.67% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 10.67%.

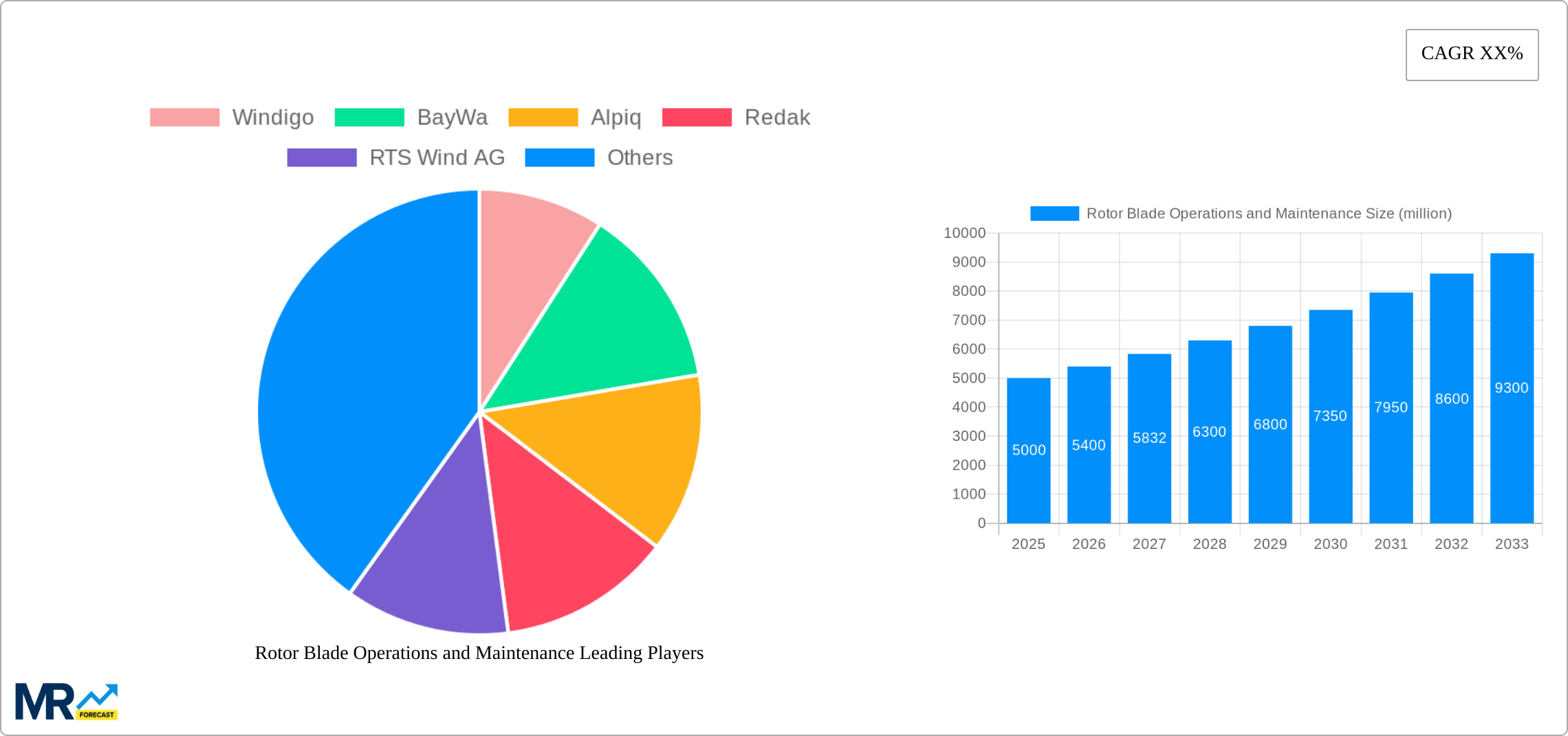

Key companies in the market include Windigo, BayWa, Alpiq, Redak, RTS Wind AG, Windea, SGS Poland, Vestas, Siemens gamesa, GE Renewable Energy, Enercon, Goldwind, Global Wind Service, Deutsche Windtechnik, Stork, Mingyang Smart ENERGY, Ingeteam, Envision Group, Olympus, ThermoFisher, Centre Testing International Group, China General Certification Center, Standard Testing Group, .

The market segments include Type, Application.

The market size is estimated to be USD 11.94 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Rotor Blade Operations and Maintenance," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Rotor Blade Operations and Maintenance, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.