1. What is the projected Compound Annual Growth Rate (CAGR) of the Retail Banking Service?

The projected CAGR is approximately XX%.

Retail Banking Service

Retail Banking ServiceRetail Banking Service by Type (Traditional, Digital Led), by Application (Transactional Accounts, Savings Accounts, Debit Cards, Credit Cards, Loans, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

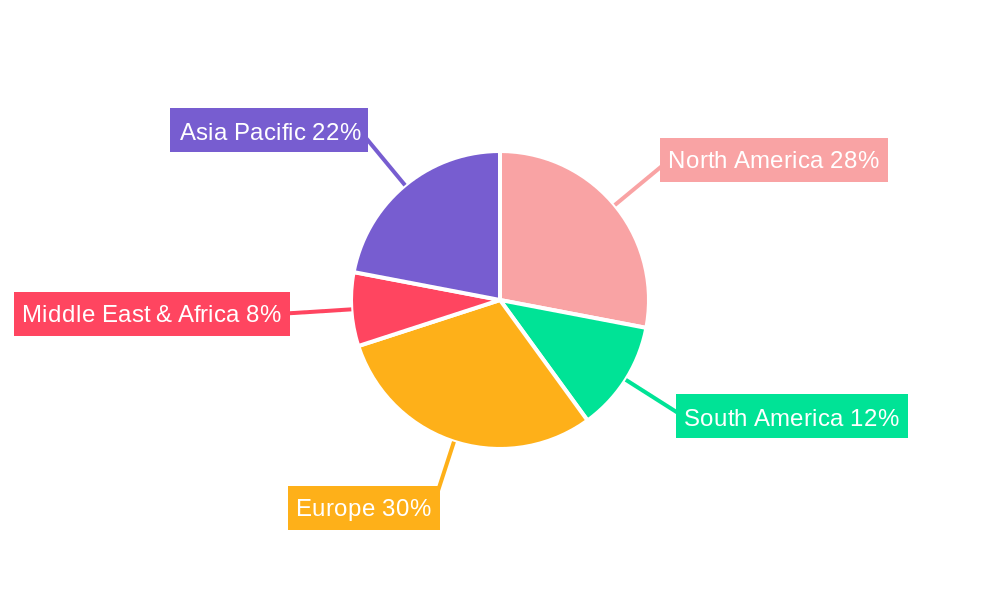

The global retail banking services market is experiencing robust growth, driven by the increasing adoption of digital banking channels and the expanding demand for diverse financial products. The market, estimated at $5 trillion in 2025, is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 8% from 2025 to 2033, reaching a market value exceeding $9 trillion by 2033. Key drivers include the rising adoption of mobile banking, fintech innovations offering personalized services and competitive pricing, and the growing need for financial inclusion across emerging economies. The shift towards digital banking is significantly impacting traditional banking models, with digital-led services witnessing faster growth compared to their traditional counterparts. Transaction accounts, savings accounts, and debit cards continue to form the core of retail banking services, but the increasing demand for loans, investment products, and other specialized financial services is also contributing to market expansion. Geographical variations in market penetration and regulatory frameworks influence regional growth. North America and Europe currently hold the largest market shares, but Asia-Pacific is poised for substantial growth due to its expanding middle class and increasing smartphone penetration. However, challenges such as stringent regulatory compliance, cybersecurity threats, and the need for continuous technological upgrades pose potential restraints to market growth.

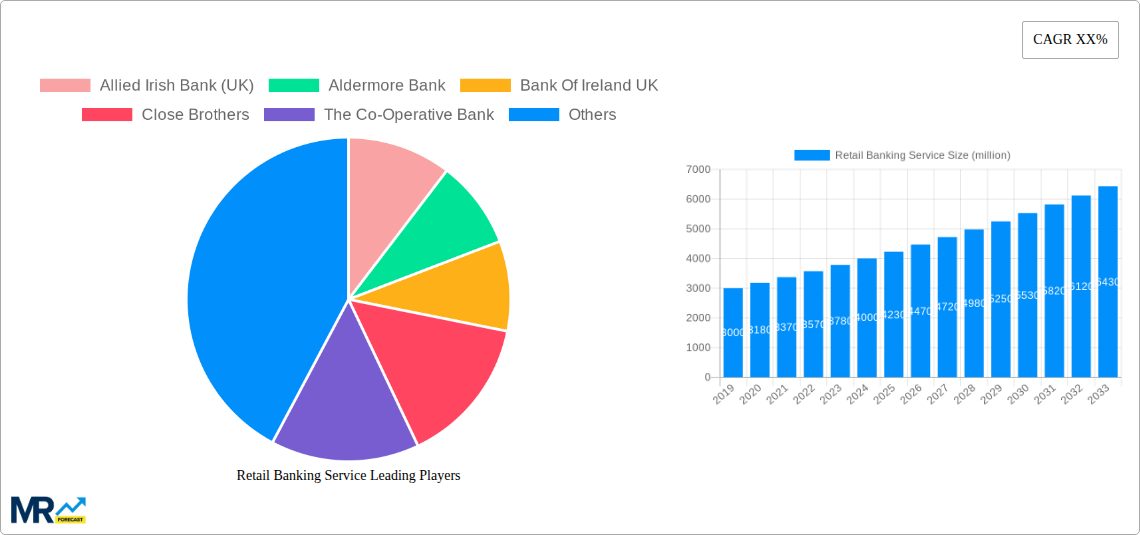

Within the retail banking landscape, competition is fierce among established players like Allied Irish Bank (UK), Bank of Ireland UK, and TSB, and newer, digitally focused entrants. Differentiation strategies focusing on personalized customer experiences, superior digital interfaces, and innovative product offerings are crucial for success. The segmentation of the market into traditional and digital-led services, along with the diverse range of applications (transactional accounts, savings accounts, debit cards, credit cards, loans, etc.), provides multiple avenues for growth and investment. The future of retail banking hinges on adapting to technological advancements, maintaining strong cybersecurity measures, and effectively meeting the evolving needs and expectations of a digitally-savvy customer base. Successful players will need to balance the benefits of digital transformation with the importance of personalized customer service and trust.

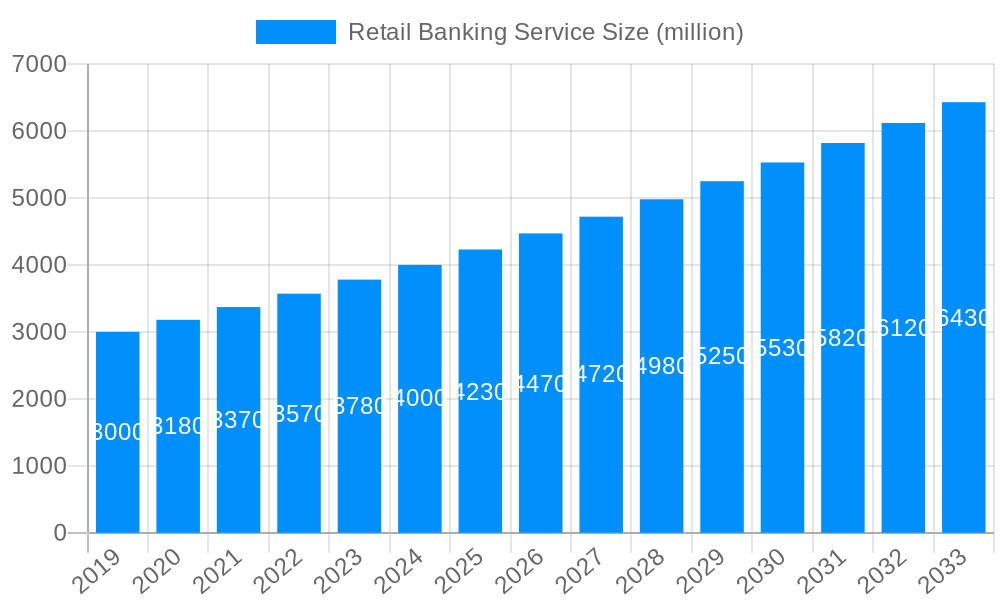

The UK retail banking sector, encompassing players like Allied Irish Bank (UK), Aldermore Bank, and Virgin Money, witnessed significant transformation during 2019-2024. The market, valued at XXX million in 2025, is projected to reach XXX million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of X%. This growth is fueled by several interconnected trends. Firstly, the increasing adoption of digital banking solutions, driven by younger demographics and advancements in fintech, has fundamentally reshaped customer expectations. Traditional brick-and-mortar banks are responding by investing heavily in online and mobile platforms, improving user interfaces, and integrating advanced functionalities like AI-powered chatbots and personalized financial management tools. This digital shift, while creating new opportunities, also presents challenges for established players needing to adapt to changing customer preferences and compete with agile fintech disruptors.

Secondly, regulatory changes and increased scrutiny regarding financial security and customer protection have significantly impacted the industry. Compliance costs have risen, demanding investments in robust security systems and stringent data protection protocols. Conversely, these regulations also foster greater consumer trust and confidence, potentially leading to increased market penetration. Thirdly, economic fluctuations, including periods of low interest rates and periods of economic uncertainty, have influenced consumer behavior, shifting the demand for specific financial products. For example, during periods of economic uncertainty, the demand for savings accounts and secure investment options tends to increase, while demand for loans might decrease. Conversely, periods of economic growth may see an increase in demand for loans for mortgages and business expansion. Finally, the increasing demand for specialized financial services, such as ethical banking and sustainable finance options, is presenting new avenues for banks that adapt to meet changing consumer values and priorities. These interwoven trends shape the competitive landscape and guide the strategic decisions of retail banking institutions.

Several key factors are driving growth in the UK retail banking service market. The ongoing digitalization of banking services, as already mentioned, is a primary catalyst. Consumers are increasingly comfortable managing their finances online and through mobile apps, leading to higher adoption rates of digital banking platforms. This trend is not only enhancing convenience but also prompting banks to innovate and improve their digital offerings. Furthermore, the rise of open banking initiatives is fostering greater competition and innovation by allowing third-party providers to integrate with banking systems, offering consumers more choice and customized financial solutions. This increased competition incentivizes established banks to enhance their services and introduce new products to remain competitive.

Another significant driver is the increasing focus on personalized customer experiences. Banks are leveraging data analytics to understand customer needs better and tailor their offerings accordingly, leading to increased customer loyalty and satisfaction. Moreover, the growing demand for financial inclusion and access to banking services for underserved populations is creating new opportunities for retail banks. This requires innovative solutions, particularly in remote areas, and drives initiatives to enhance financial literacy and provide accessible banking options for a wider range of customers. Finally, the increasing awareness of financial security and fraud prevention is prompting banks to invest in more robust security systems and technologies, creating a more secure environment that builds confidence and trust amongst consumers.

Despite the considerable growth potential, the UK retail banking sector faces significant challenges. Maintaining profitability in a low-interest-rate environment remains a primary concern. Banks need to find innovative ways to generate revenue while offering competitive interest rates to attract and retain customers. This necessitates a keen focus on efficiency and cost optimization, a challenge exacerbated by increased regulatory compliance costs. The cybersecurity landscape is also a critical challenge. The increasing sophistication of cyber threats requires substantial investments in robust security infrastructure to protect customer data and prevent fraud.

Further, intense competition from both established players and fintech disruptors necessitates continuous innovation and investment in technology and customer service to maintain market share. Regulatory changes and evolving consumer expectations demand adaptation and agility, requiring banks to invest in training and development to upskill their workforce and adapt to the changing landscape. Finally, managing the risks associated with economic fluctuations and geopolitical uncertainty remains a key concern, necessitating proactive risk management strategies and diversification of revenue streams.

The UK retail banking market is geographically concentrated, with London and other major cities representing significant hubs for banking activity. However, significant growth opportunities exist across various regions, especially as digital banking expands access to services beyond major urban areas.

Digital-Led Segment Dominance: The digital-led segment is expected to exhibit the most significant growth in the forecast period (2025-2033). This is because consumers increasingly favor convenience and accessibility provided by digital banking platforms. Digital banking offers services like mobile apps and online banking platforms which provide efficient customer experience and personalized banking experience. These features have propelled the segment's growth and are anticipated to further contribute to its market dominance.

Transactional Accounts: Transactional accounts, including current accounts and checking accounts, represent a fundamental banking product and constitute a consistently large portion of the market. The sheer volume of transactions processed makes this segment a crucial component of overall retail banking revenue. The wide usage of transactional accounts, coupled with the continued demand for seamless and secure transactions, positions this segment for robust growth throughout the forecast period.

Credit Cards: The credit card market, a segment within retail banking's applications, is predicted to experience robust growth, driven by increasing consumer spending and credit card acceptance among businesses. Convenience and rewards programs drive demand for credit cards among consumers, resulting in increased transaction volumes and overall revenue.

The growth of digital-led banking, transactional accounts, and credit cards is further amplified by the widespread adoption of mobile payments and the increasing integration of financial technology within these services.

Several factors will significantly propel the growth of the retail banking service industry during the forecast period. The expanding adoption of digital banking channels offers enhanced convenience and accessibility, attracting a wider customer base. Open banking initiatives foster innovation and create new opportunities for partnerships and value-added services. Increased focus on personalized financial solutions, tailored to individual customer needs, is building stronger customer relationships and loyalty. Finally, growing demand for specialized services, such as sustainable and ethical banking options, caters to emerging market segments with specific values and preferences.

This report provides a detailed analysis of the UK retail banking service market, covering historical data (2019-2024), an estimated year (2025), and forecasts (2025-2033). It offers insights into market trends, driving forces, challenges, and opportunities, alongside a comprehensive analysis of key players and market segments. The report presents valuable information for stakeholders, including banks, investors, fintech companies, and regulatory bodies, providing a clear understanding of the dynamic landscape of UK retail banking and its future prospects. This analysis considers the implications of digital transformation, regulatory changes, and evolving consumer behaviors on the industry's development and competitiveness.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include Allied Irish Bank (UK), Aldermore Bank, Bank Of Ireland UK, Close Brothers, The Co-Operative Bank, Cybg (Clydesdale And Yorkshire Banks), First Direct, Handelsbanken, Masthaven Bank, Metro Bank, Onesavings Bank, Paragon Bank, Secure Trust Bank, Shawbrook Bank, TSB, Virgin Money, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Retail Banking Service," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Retail Banking Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.