1. What is the projected Compound Annual Growth Rate (CAGR) of the Private 5G?

The projected CAGR is approximately 35.4%.

Private 5G

Private 5GPrivate 5G by Application (Manufacturing, Energy, Utilities and Mining, Transportation & Logistics, Education and Hospitality, Government & Public Safety, Corporates & Enterprises, Healthcare, Others), by Type (Sub-6 GHz, mmWave), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

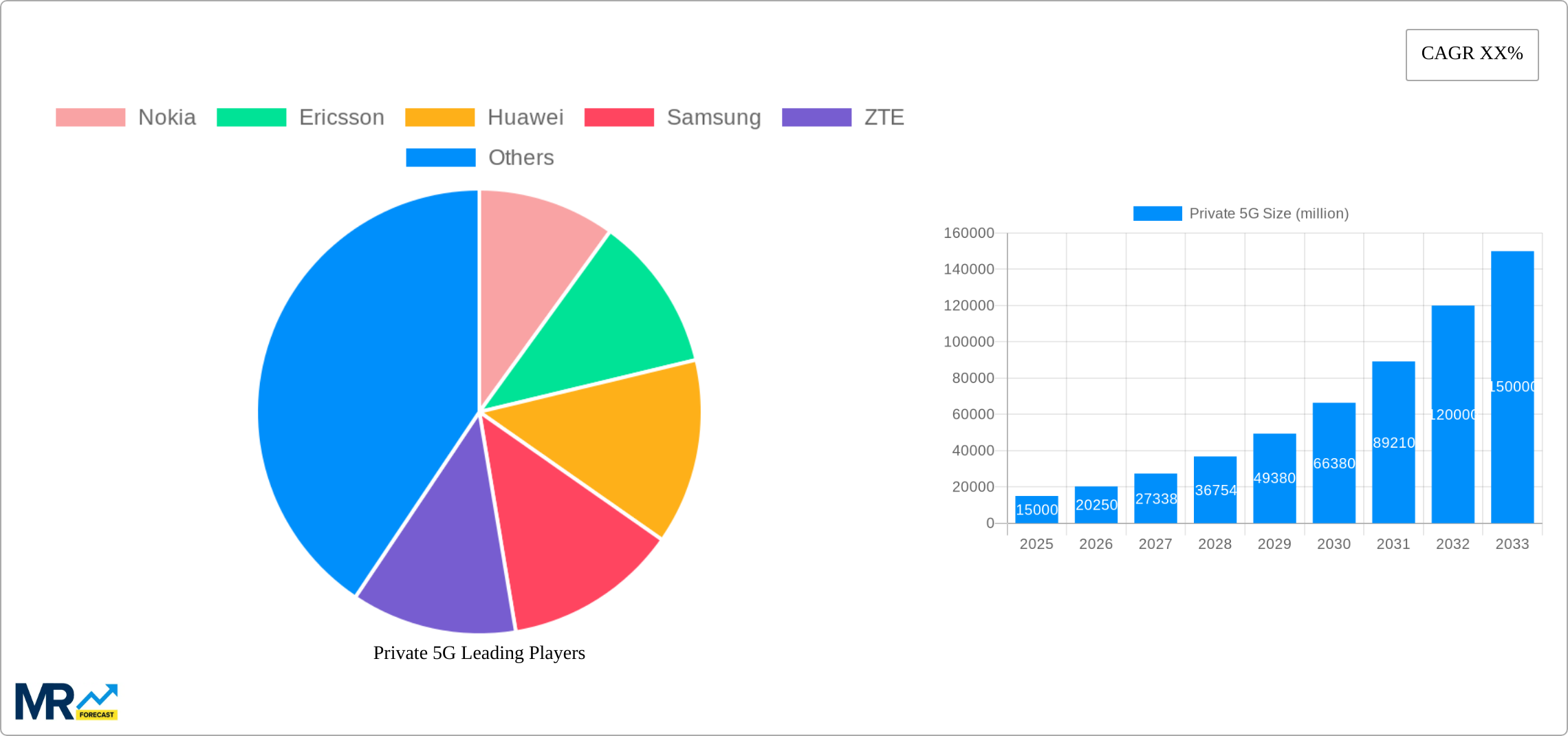

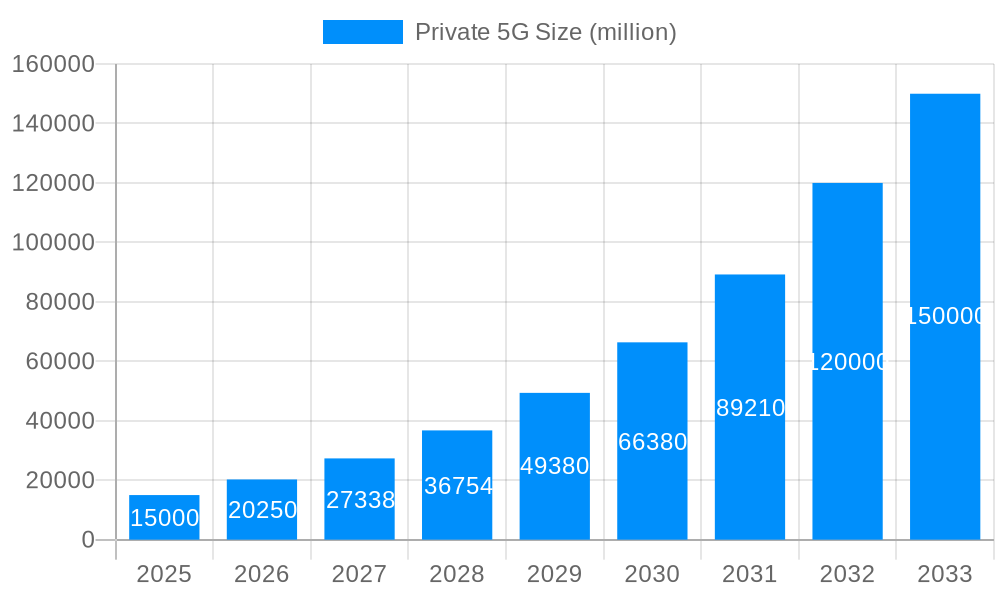

The private 5G market is experiencing robust expansion, driven by the escalating need for secure, high-bandwidth, low-latency connectivity across various industries. The market is projected to reach $3.86 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 35.4%, anticipating a valuation of approximately $150 billion by 2033. Key growth drivers include the widespread adoption of Industry 4.0 and smart manufacturing, necessitating reliable private networks for managing extensive data from connected devices. Sectors like energy, utilities, and mining are leveraging private 5G for enhanced operational efficiency, remote monitoring, and improved safety. Transportation and logistics are utilizing it for real-time tracking and autonomous vehicle operations, while healthcare benefits from its application in remote surgery, telemedicine, and secure data exchange. Government and public safety agencies are also adopting private 5G for improved communication and situational awareness. Currently, Sub-6 GHz technology leads due to its broad coverage and cost-effectiveness, with mmWave poised for significant growth due to its superior bandwidth.

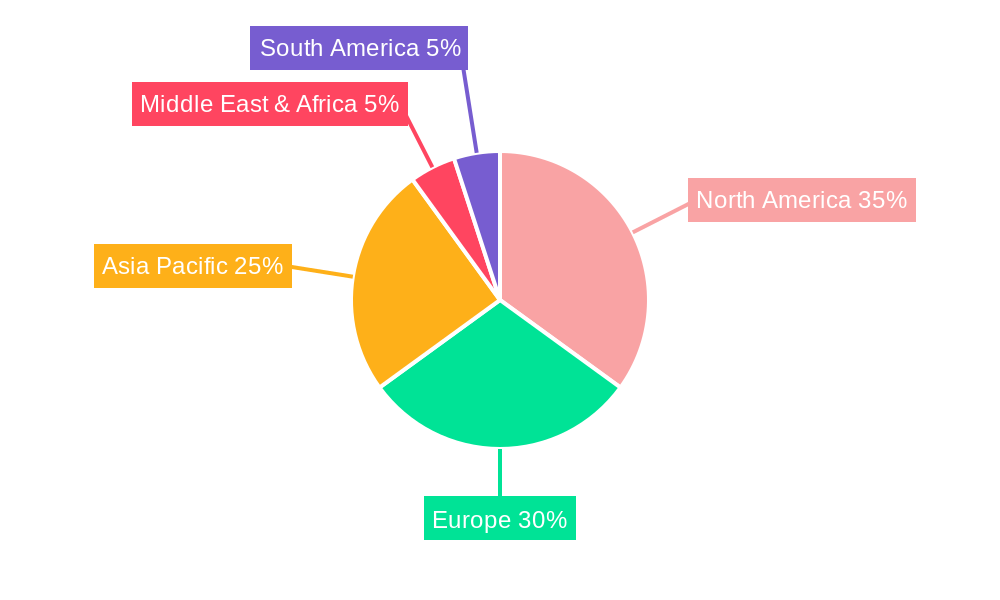

The private 5G market is characterized by intense competition among major players such as Nokia, Ericsson, Huawei, Samsung, and Qualcomm. These leaders are forging strategic alliances with system integrators and cloud providers, including AWS, Cisco, and HPE, to offer comprehensive solutions. Emerging niche players and specialized service providers are also contributing to market dynamism. Geographically, North America and Europe currently dominate, with Asia Pacific following closely. Developing regions in the Middle East, Africa, and South America are anticipated to witness substantial growth, propelled by digitalization trends and infrastructure investments. Regulatory frameworks and spectrum allocation policies are critical factors that will shape the future landscape of this dynamic market.

The private 5G market is experiencing explosive growth, projected to reach tens of billions of USD by 2033. The study period (2019-2033), with a base year of 2025 and a forecast period spanning 2025-2033, reveals a compelling narrative. Early adoption, particularly by large enterprises in sectors like manufacturing and energy, has fueled significant expansion during the historical period (2019-2024). By 2025, the market is estimated to surpass several billion USD in revenue, with continuous expansion anticipated throughout the forecast period. This growth is driven not only by technological advancements but also by the increasing recognition of private 5G's potential to transform operational efficiency and unlock new revenue streams across various industries. Key market insights reveal a strong preference for Sub-6 GHz deployments due to their wider coverage and lower infrastructure costs, while mmWave solutions are gradually gaining traction in specific applications requiring ultra-high bandwidth. The competitive landscape is intensely dynamic, with established players like Nokia, Ericsson, and Huawei vying for market share alongside emerging vendors specializing in private network solutions. The industry is also witnessing a surge in partnerships and collaborations, as operators, equipment vendors, and system integrators work together to deliver comprehensive private 5G solutions tailored to individual customer needs. Furthermore, the market demonstrates a clear shift towards cloud-native architectures and edge computing, enabling seamless integration with existing IT infrastructure and enhancing the scalability and manageability of private 5G networks. This trend underscores the increasing importance of software-defined networking (SDN) and network functions virtualization (NFV) in the private 5G space. Finally, the rising demand for enhanced security and reliability, particularly in critical infrastructure sectors, is driving innovation in private 5G security solutions and network management tools.

Several key factors are propelling the rapid expansion of the private 5G market. Firstly, the increasing need for high-bandwidth, low-latency connectivity is paramount across diverse industries. Manufacturing, for example, benefits immensely from real-time data transfer for automation and improved production processes. Similarly, the energy sector utilizes private 5G for remote monitoring and control of critical infrastructure, enhancing safety and operational efficiency. Secondly, the enhanced security and reliability offered by private 5G networks are crucial. Unlike public networks, private 5G networks offer greater control over data security and network management, reducing vulnerability to cyber threats. This is especially appealing to industries handling sensitive data or operating critical infrastructure. Thirdly, the growing availability of affordable and readily deployable private 5G solutions is playing a crucial role. Equipment vendors are constantly innovating to reduce the cost and complexity of private network deployment, making this technology more accessible to a wider range of businesses. Finally, supportive government initiatives and regulatory frameworks in various regions are incentivizing private 5G adoption, offering grants, funding, and streamlined licensing processes to facilitate deployment. This collaborative ecosystem is further accelerating the private 5G revolution, driving rapid market growth.

Despite the significant potential, several challenges and restraints hinder the widespread adoption of private 5G. Firstly, the high initial investment costs associated with deploying and maintaining private 5G infrastructure can be a major barrier, particularly for smaller businesses. This includes expenses related to network equipment, installation, and ongoing operational costs. Secondly, the complexity of private 5G network management requires specialized skills and expertise, often resulting in a need for specialized personnel or outsourcing, adding to overall operational costs. Thirdly, regulatory hurdles and spectrum allocation policies can vary significantly across different regions, causing uncertainty and potential delays in network deployments. Furthermore, ensuring interoperability between different private 5G vendors' equipment and solutions remains a challenge, potentially limiting flexibility and hindering seamless network expansion. Lastly, the lack of widespread awareness and understanding of private 5G's potential benefits among potential users can also slow down adoption rates. Addressing these challenges through cost reductions, streamlined deployment processes, enhanced interoperability standards, and improved educational initiatives is crucial for unlocking the full potential of the private 5G market.

The Manufacturing segment is projected to dominate the private 5G market throughout the forecast period (2025-2033), driven by the increasing need for automation, real-time data analytics, and improved operational efficiency. This segment's substantial investment capacity and the clear return on investment (ROI) offered by private 5G networks are key factors underpinning its dominance.

Manufacturing: Private 5G enables advanced automation, robotics, predictive maintenance, and improved quality control, leading to increased productivity and reduced operational costs. This segment is expected to account for several billion USD in revenue by 2033.

North America (USA, Canada): North America is a leading adopter of private 5G due to a mature technology ecosystem, substantial funding for technological advancements, and the presence of significant players in the technology and telecom sectors. This region’s early and substantial investments are expected to further cement its dominant position.

Europe (Germany, UK, France): Europe is also expected to significantly contribute to market growth with strong government support and considerable investment in digital infrastructure. Companies in various industries are aggressively exploring the capabilities of private 5G for digital transformation initiatives.

Asia Pacific (China, Japan, South Korea): The Asia Pacific region, particularly China, Japan, and South Korea, shows significant potential due to strong economic growth and the rapid adoption of advanced technologies across diverse industries. The burgeoning manufacturing sector in this region greatly benefits from private 5G deployments.

Sub-6 GHz: This frequency band offers a wider coverage area and is therefore favoured for initial deployments, contributing to the majority of private 5G network installations, accounting for billions of USD in market revenue by 2033. MmWave, while offering higher bandwidth, faces challenges in terms of limited range and penetration, limiting its adoption for the time being.

In summary, while various regions and segments are poised for significant growth, the confluence of high demand within the manufacturing sector and the strong initial adoption in North America and Europe positions them for market dominance, with the Sub-6 GHz band leading the technology adoption due to its wider coverage and affordability.

Several factors are accelerating the private 5G market’s growth. The convergence of declining hardware costs, increasing enterprise digitalization initiatives, and supportive government regulations is fueling widespread adoption. Moreover, the development of innovative applications tailored to specific industries, such as autonomous vehicles and smart factories, is driving further demand. The increasing availability of scalable and manageable cloud-based private 5G solutions is also making deployment easier and more cost-effective, thereby accelerating growth.

This report offers a comprehensive overview of the private 5G market, providing detailed insights into market trends, driving forces, challenges, and future growth prospects. It features in-depth analysis of key regions, segments, and leading players, providing valuable information for stakeholders across the value chain. The detailed market projections allow for informed strategic decision-making and offer a valuable resource for understanding the evolving landscape of private 5G.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 35.4% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 35.4%.

Key companies in the market include Nokia, Ericsson, Huawei, Samsung, ZTE, China Mobile, China Unicom, Verizon, Deutsche Telekom, Vodafone, Qualcomm, NEC, Fujitsu, NTT, Advantech, Amazon Web Services (AWS), Cisco, HPE, .

The market segments include Application, Type.

The market size is estimated to be USD 3.86 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3480.00, USD 5220.00, and USD 6960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Private 5G," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Private 5G, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.