1. What is the projected Compound Annual Growth Rate (CAGR) of the Pet Dog Insurance?

The projected CAGR is approximately 17.53%.

Pet Dog Insurance

Pet Dog InsurancePet Dog Insurance by Type (Lifetime Cover, Non-lifetime Cover, Accident-only), by Application (Small Breed, Large Breed), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

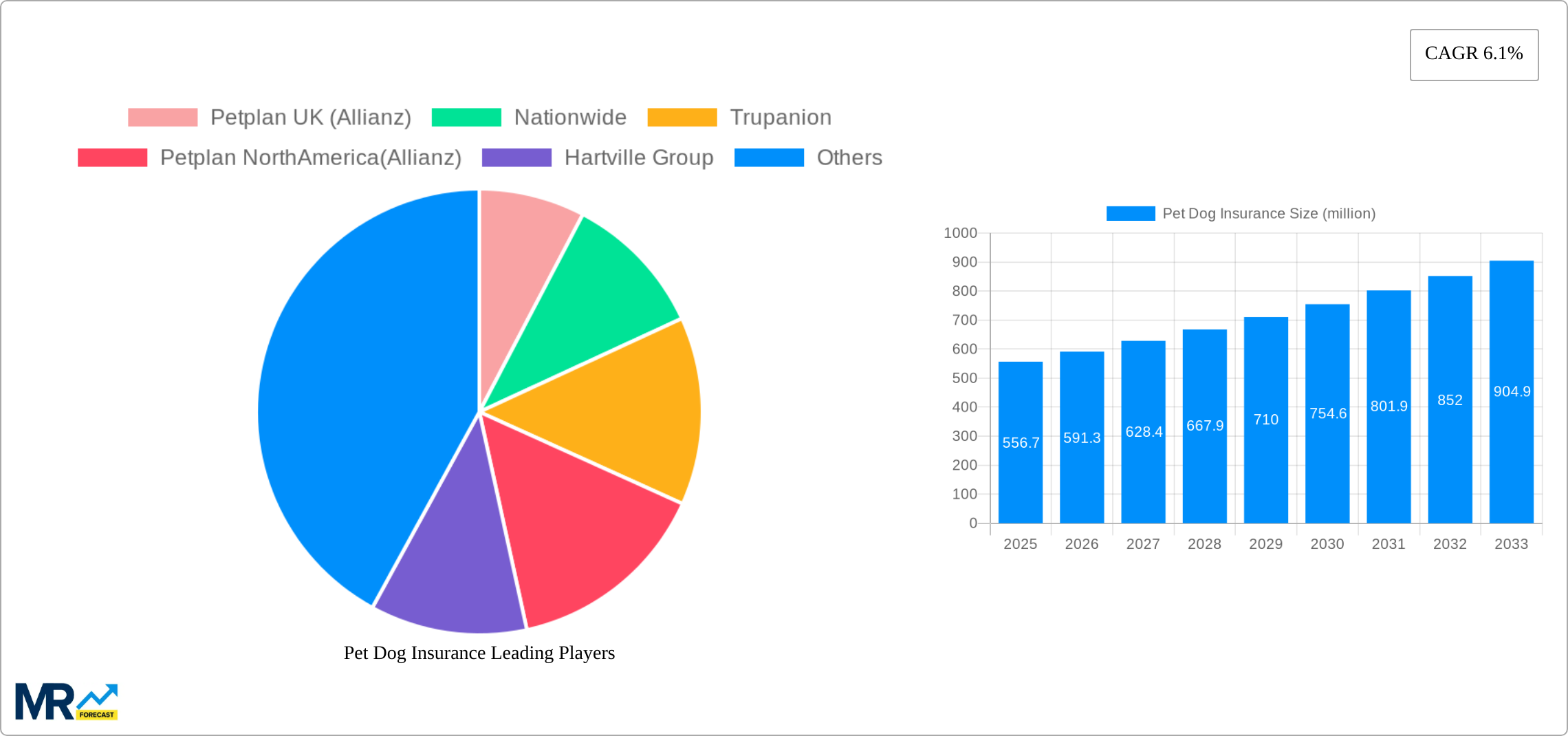

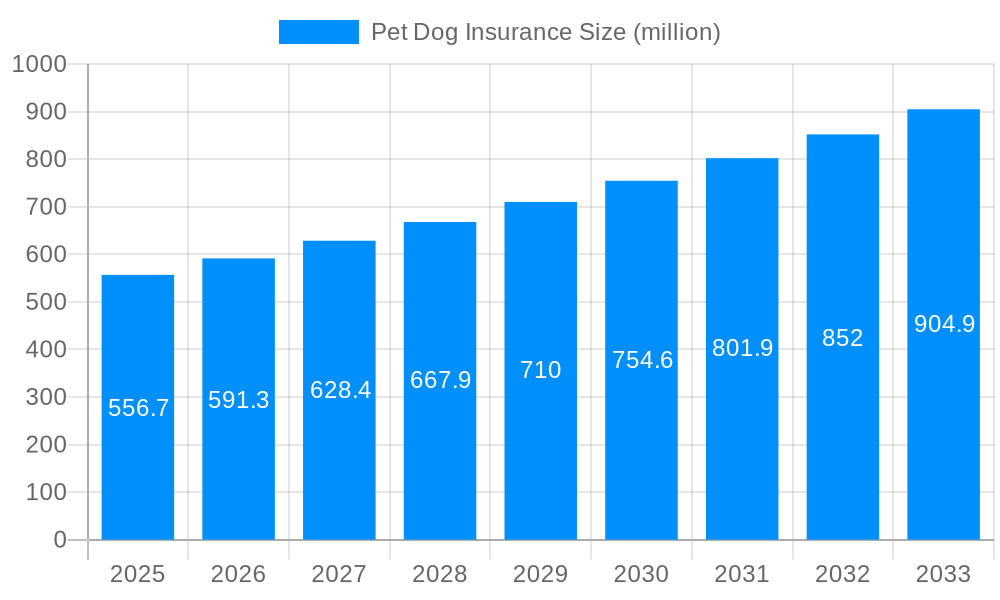

The global pet dog insurance market, valued at $843.9 million in 2025, is experiencing robust growth driven by increasing pet ownership, rising pet healthcare costs, and a growing awareness of pet insurance benefits among pet owners. The market is segmented by coverage type (lifetime, non-lifetime, accident-only) and dog breed (small, large), reflecting the diverse needs and preferences of pet owners. North America currently holds a significant market share, attributed to high pet ownership rates and developed pet insurance markets in the United States and Canada. However, Asia-Pacific is projected to witness substantial growth over the forecast period (2025-2033), fueled by rising disposable incomes and increased pet humanization in countries like China and India. Key players like Petplan, Nationwide, and Trupanion are leveraging technological advancements, such as online platforms and mobile apps, to enhance customer experience and expand their market reach. Competitive pressures are driving innovation in policy offerings, with companies increasingly offering customizable plans and value-added services. While the market faces restraints such as affordability concerns and limited awareness in certain regions, the overall growth trajectory is positive, driven by the increasing emotional bond between humans and their pets and the rising willingness to invest in their health and well-being.

The competitive landscape is characterized by a mix of established multinational insurers and regional players. The market's future depends heavily on factors such as regulatory changes impacting insurance policies, evolving consumer preferences toward comprehensive coverage and preventive care, and the continuous development of sophisticated pet healthcare technologies. Furthermore, the increasing availability of telehealth services for pets is likely to positively influence the adoption of pet insurance plans, as these services offer convenient and cost-effective ways to access veterinary care. The market is expected to witness consolidation through mergers and acquisitions, as larger players seek to expand their market share and diversify their product offerings. Expansion into emerging markets, particularly in Asia-Pacific and parts of Africa, remains a key strategic focus for many players in the years to come.

The global pet dog insurance market is experiencing robust growth, projected to reach multi-million dollar valuations by 2033. Over the historical period (2019-2024), the market witnessed a steady expansion driven by increasing pet ownership, heightened awareness of pet healthcare costs, and a shifting societal perception of pets as integral family members. The estimated market value in 2025 signifies a significant milestone, reflecting the culmination of these trends. The forecast period (2025-2033) promises continued expansion, fueled by factors such as rising disposable incomes in many regions, the growing popularity of pet insurance amongst younger demographics, and the increasing sophistication of insurance products tailored to specific dog breeds and needs. The market is dynamic, with constant innovation in policy offerings, including the rise of bundled services that combine insurance with wellness plans and preventative care. This trend reflects a proactive approach to pet health management, shifting the focus from reactive treatment to preventative care. This proactive approach and the increasing availability of digital platforms for managing insurance policies are likely to further boost market penetration during the forecast period. The competitive landscape is characterized by both established players and new entrants, resulting in a diverse range of policy options and pricing structures. This competition further contributes to the overall market growth, pushing companies to innovate and improve their offerings to attract and retain customers. The base year of 2025 represents a pivotal point, with market consolidation likely to occur as companies adapt to an increasingly competitive and regulated environment.

Several key factors are driving the expansion of the pet dog insurance market. The escalating cost of veterinary care is a significant motivator; unexpected illnesses or injuries can lead to substantial financial burdens for pet owners. Insurance provides a financial safety net, mitigating these risks and allowing owners to prioritize their pet's health without compromising their financial stability. The increasing humanization of pets is another critical driver. Pets are increasingly viewed as family members, leading owners to invest more in their well-being, including insurance coverage. This trend is particularly strong among younger generations, who are more likely to view pets as integral family units, rather than simply animals. Furthermore, the growing availability of comprehensive insurance plans, often bundled with preventative care services, is attracting a wider range of pet owners. These plans provide value beyond simple accident and illness coverage, offering a holistic approach to pet health management. Improved marketing and awareness campaigns, along with the convenience of online purchasing and management of policies, contribute significantly to the expansion of the market. The ease of access and increased understanding of the benefits of pet insurance are driving higher adoption rates across demographics.

Despite the considerable growth potential, several challenges impede the market's expansion. One key restraint is the relatively high cost of premiums, particularly for larger or certain breeds perceived as high-risk. This cost can be prohibitive for some pet owners, especially those on tighter budgets. The prevalence of pre-existing conditions is another factor limiting market penetration. Many policies exclude coverage for pre-existing conditions, meaning that pets with prior health issues might not be eligible for comprehensive insurance, or the coverage might be limited and more expensive. Furthermore, the complexity of insurance policies and the process of filing claims can deter some potential customers. Simplified policy language and streamlined claims processes are necessary to address these barriers to entry and broaden the market's appeal. Regulatory changes and differences in regulations across countries can also pose challenges for insurers, adding complexity and potentially increasing costs. Finally, fraud and inaccurate claims can lead to higher premiums for all policyholders and represent a significant financial burden for the industry.

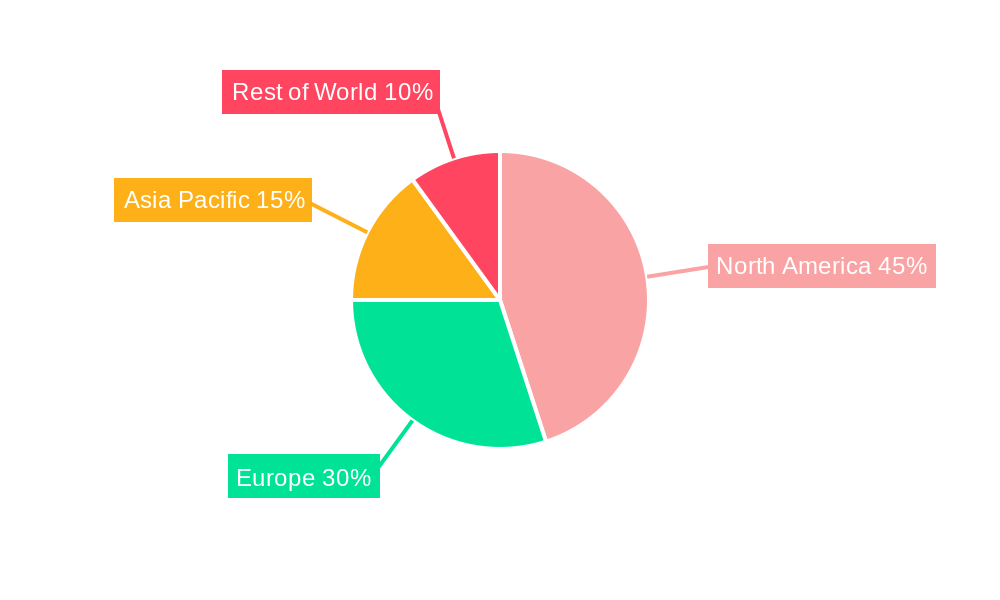

The North American market (specifically the US and Canada) is expected to dominate the pet dog insurance sector during the forecast period (2025-2033), driven by high pet ownership rates, rising disposable incomes, and increasing awareness of pet insurance benefits. Within this region, the lifetime cover segment is poised for significant growth.

The large breed segment also displays strong growth potential within the North American market due to the higher veterinary costs associated with their care and higher propensity for breed-specific health issues. This segment commands higher premiums but reflects a segment of the market willing to pay for more extensive and targeted coverage.

In summary, the combination of a high pet ownership rate, high disposable incomes, increasing awareness of the benefits of insurance and the appeal of lifetime coverage for large breed dogs in North America positions this segment to be the most dominant market force within the forecast period.

The increasing affordability of pet insurance policies, facilitated by competitive pricing strategies and innovative product bundling, serves as a significant catalyst for market growth. Coupled with heightened consumer awareness through targeted marketing campaigns and educational initiatives, the accessibility of comprehensive plans, including preventative care options, is further driving expansion.

This report offers a comprehensive overview of the pet dog insurance market, encompassing detailed analysis of historical trends, current market dynamics, future projections, and key players. The study provides invaluable insights for businesses operating in or seeking to enter this dynamic and rapidly expanding sector, with detailed segmentation that facilitates informed strategic decision-making. Specific market valuation data in millions of dollars, segmented by product type, breed, and region, provides a clear picture of the market's size and growth potential.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 17.53% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately 17.53%.

Key companies in the market include Petplan UK (Allianz), Nationwide, Trupanion, Petplan NorthAmerica(Allianz), Hartville Group, Pethealth, Petfirst, Embrace, Royal & Sun Alliance (RSA), Direct Line Group, Agria, Petsecure, PetSure, Anicom Holding, Ipet Insurance Co, .

The market segments include Type, Application.

The market size is estimated to be USD 21.84 billion as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in billion.

Yes, the market keyword associated with the report is "Pet Dog Insurance," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Pet Dog Insurance, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.