1. What is the projected Compound Annual Growth Rate (CAGR) of the Pet Death Insurance?

The projected CAGR is approximately XX%.

Pet Death Insurance

Pet Death InsurancePet Death Insurance by Type (Accidental Death Insurance, Death Due To Illness Insurance, Euthanasia Insurance), by Application (Dog, Cat, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2026-2034

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.

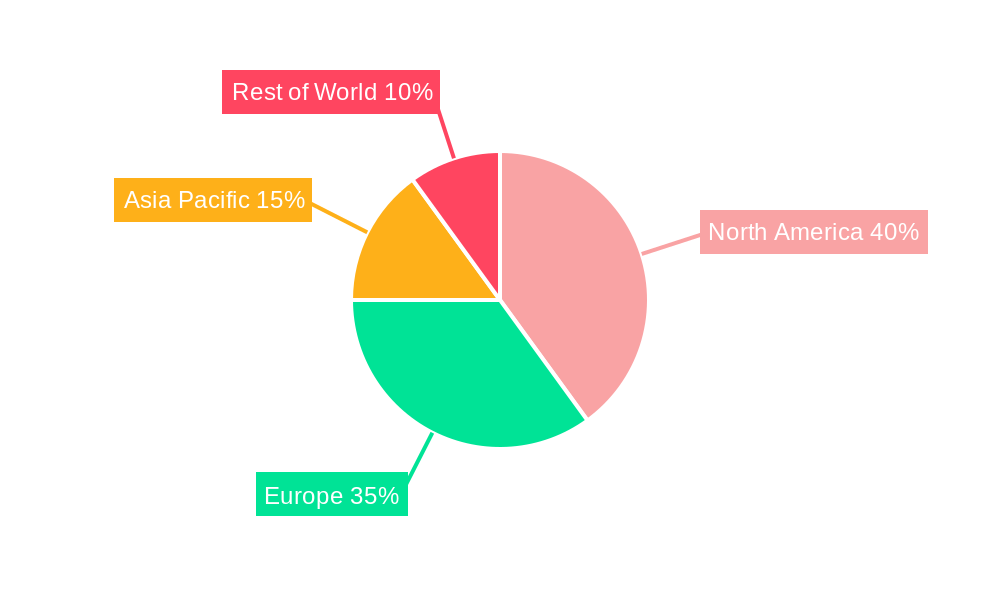

The pet death insurance market is experiencing robust growth, driven by increasing pet ownership, heightened pet humanization, and a rising awareness of the financial burden associated with unexpected pet loss. The market, segmented by insurance type (Accidental Death, Illness-related Death, Euthanasia) and pet type (Dog, Cat, Other), shows significant potential for expansion. Dogs and cats currently dominate the market, reflecting their widespread popularity as companion animals. However, the "Other" category is expected to see growth as owners of exotic pets and other animals increasingly seek similar protection. The market's Compound Annual Growth Rate (CAGR) is estimated to be around 15% based on the observed market trends in related insurance sectors and the increasing adoption of pet insurance globally. This growth is further fueled by technological advancements making insurance procurement more convenient and accessible. While regional variations exist, North America and Europe currently hold the largest market shares due to higher pet ownership rates and higher disposable incomes. However, the Asia-Pacific region demonstrates significant growth potential, driven by a burgeoning middle class with increasing pet ownership and a growing awareness of pet insurance benefits. Key restraining factors include varying regulatory frameworks across different regions, lack of awareness about pet insurance in emerging markets, and relatively high premiums compared to human life insurance.

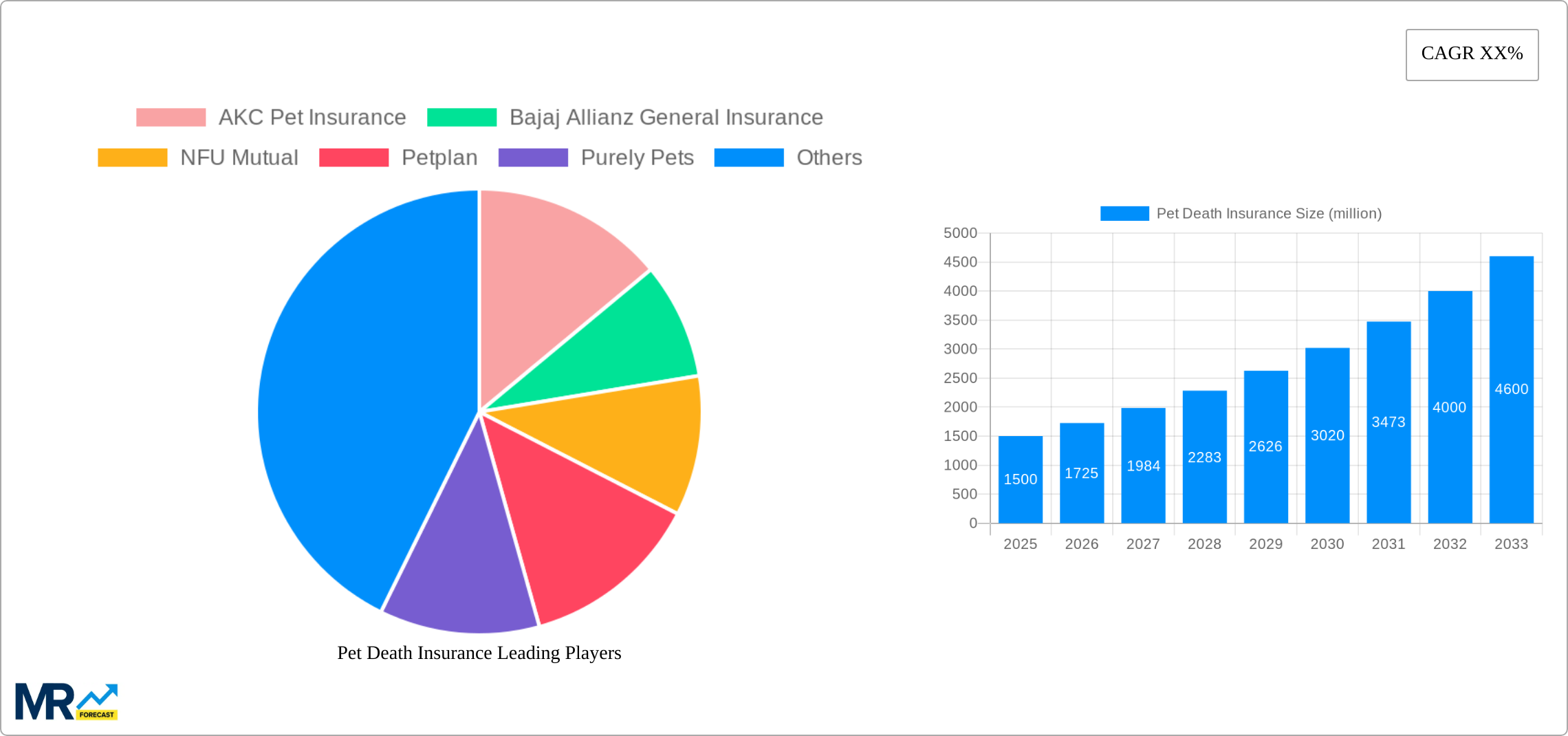

Further growth hinges on insurers developing more competitive and comprehensive products, tailored to specific pet needs and owner demographics. Education campaigns focused on the financial implications of unexpected pet loss are essential to broaden market penetration. The market landscape is competitive, with a mix of specialized pet insurers and diversified general insurance companies. The presence of large international players like Bajaj Allianz and Ping An, alongside niche pet insurance providers like AKC Pet Insurance and Petplan, indicates a healthy and dynamic market. Future expansion will likely involve increased use of technology, data analytics, and personalized insurance offerings, responding to individual pet profiles and risk assessments to offer more competitive pricing.

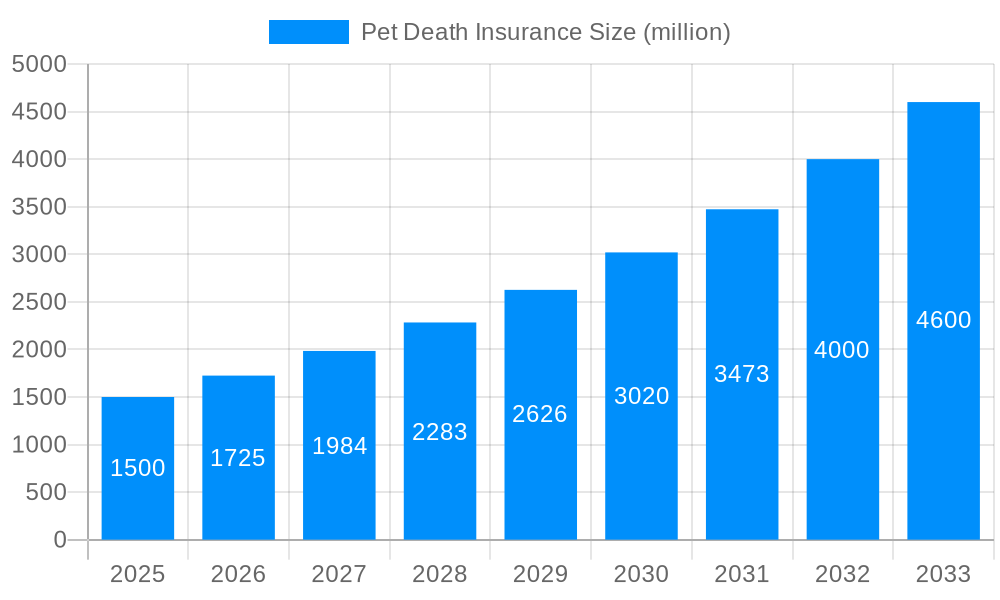

The global pet death insurance market is experiencing significant growth, projected to reach tens of millions of dollars by 2033. Driven by increasing pet ownership and humanization of pets, particularly in developed nations, pet owners are increasingly seeking financial protection against the unexpected costs associated with pet loss. The market's evolution reflects a broader societal shift; pets are no longer simply animals but integral members of families, prompting a demand for services mirroring human life insurance. The historical period (2019-2024) saw steady growth, laying the foundation for the accelerated expansion predicted for the forecast period (2025-2033). The estimated market value in 2025 underscores the current momentum. This growth isn't uniform; certain segments, like dog insurance, consistently outperform others due to higher ownership rates and potentially higher veterinary costs associated with larger breeds. Furthermore, the market is witnessing innovation in product offerings, with insurers tailoring policies to specific breeds, ages, and pre-existing conditions. This trend toward customized coverage reflects a move beyond basic death benefits to encompass broader pet welfare considerations. The rise of online platforms and digital insurance distribution channels is also streamlining the purchasing process and expanding market reach, particularly amongst younger demographics. Competitive pressures are driving insurers to offer more comprehensive benefits and competitive pricing, contributing to the overall market expansion. Geographical variations in pet ownership and insurance penetration rates will continue to shape market dynamics, with regions exhibiting higher pet ownership and disposable incomes expected to lead the growth trajectory. The base year of 2025 provides a crucial benchmark to measure the projected growth trajectory against.

The burgeoning pet death insurance market is propelled by several key factors. Firstly, the increasing humanization of pets is a significant driver. Pets are no longer simply animals but integral family members, leading owners to seek financial protection against the emotional and financial distress of pet loss. This emotional connection translates into a willingness to invest in insurance to mitigate the costs associated with end-of-life care, such as euthanasia and cremation. Secondly, rising veterinary costs are another critical factor. Veterinary care, particularly for serious illnesses or emergencies, can be extremely expensive, placing a considerable financial burden on pet owners. Pet death insurance provides a financial safety net, reducing the stress of unexpected expenses during an already difficult time. Thirdly, the growing middle class in developing economies, coupled with increasing pet ownership, is expanding the market's potential. As disposable incomes rise, more pet owners have the financial capacity to purchase insurance products, leading to market penetration in previously underserved regions. Furthermore, the increasing availability and accessibility of online insurance platforms are simplifying the purchasing process and making pet death insurance more convenient for potential customers. Finally, improved marketing and public awareness campaigns are effectively communicating the benefits and value of pet death insurance, leading to higher adoption rates.

Despite the promising growth trajectory, the pet death insurance market faces several challenges. One significant restraint is the relatively low awareness and understanding of the product among potential customers. Many pet owners are unaware of the existence or benefits of pet death insurance, hindering market penetration. Educating consumers about the product's value proposition and overcoming perceived barriers to entry is crucial for industry growth. Another challenge lies in accurately assessing risk and setting appropriate premiums. Predicting the lifespan and health trajectory of a pet is complex, making accurate risk assessment difficult. This complexity can lead to either underpricing, potentially jeopardizing insurer profitability, or overpricing, which can deter potential customers. Moreover, the regulatory landscape surrounding pet insurance varies significantly across different jurisdictions, creating complexities for insurers operating in multiple markets. Navigating these varying regulations and ensuring compliance can be costly and time-consuming. Furthermore, fraud and claims management represent challenges. Verifying the cause of death and preventing fraudulent claims requires robust claims processing systems and careful investigation procedures. Finally, the competition among existing and new entrants in the market is intense, putting pressure on pricing and profitability margins.

The dog segment is projected to dominate the pet death insurance market throughout the forecast period. This is primarily due to the significantly higher ownership rates of dogs compared to cats and other pets globally. The larger size and higher veterinary costs associated with many dog breeds also contribute to a higher demand for insurance coverage.

The overall market dominance of the dog segment coupled with the significant demand for illness-related coverage creates a potent combination for market expansion. However, the increasing awareness and adoption within the cat and "other pets" segments should not be disregarded; these segments are showing steady growth and are predicted to experience accelerated market penetration as consumer understanding of pet insurance increases.

Several factors are accelerating the growth of the pet death insurance industry. The rising trend of pet humanization and increasing pet ownership are fundamental drivers. Improved veterinary care awareness and the associated high costs are pushing owners to consider preventative measures such as insurance. Furthermore, advancements in technology, particularly in online insurance platforms, are enhancing accessibility and convenience, fostering wider market adoption. Lastly, effective marketing and awareness campaigns are key to boosting consumer understanding and promoting market penetration.

This report provides a comprehensive overview of the pet death insurance market, encompassing market size estimations, trend analysis, key drivers and restraints, regional performance, leading players, and significant industry developments. It offers crucial insights into current market dynamics and provides a robust forecast for future growth, allowing businesses to make informed strategic decisions. The report's data-driven approach, incorporating both historical and projected market values, helps stakeholders understand the evolving landscape of pet death insurance.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Note*: In applicable scenarios

Primary Research

Secondary Research

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

The projected CAGR is approximately XX%.

Key companies in the market include AKC Pet Insurance, Bajaj Allianz General Insurance, NFU Mutual, Petplan, Purely Pets, Mapfre Middlesea, AZPetVet, Agria, Animal Friends, The New India Assurance Company Limited, Oriental Insurance Company Limited, Fubon Insurance, The People's Insurance Company (Group) of China Limited, Ping An Insurance, ZhongAn Online P&C Insurance, China Continent Property & Casualty Insurance, China Pacific Insurance, Sunshine Insurance Group, .

The market segments include Type, Application.

The market size is estimated to be USD XXX million as of 2022.

N/A

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4480.00, USD 6720.00, and USD 8960.00 respectively.

The market size is provided in terms of value, measured in million.

Yes, the market keyword associated with the report is "Pet Death Insurance," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Pet Death Insurance, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.